Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

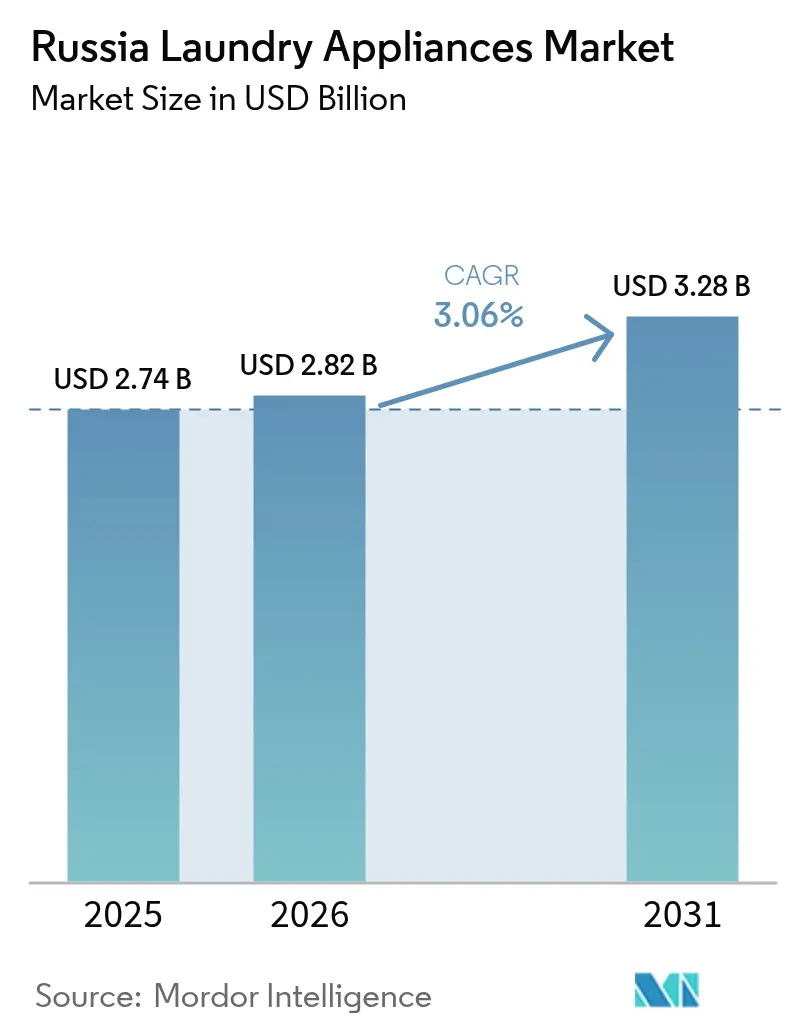

| Base Year Market Size (2025) | USD 2.74 Billion |

| Market Size (2026) | USD 2.82 Billion |

| Market Size (2031) | USD 3.28 Billion |

| Growth Rate (2026 - 2031) | 3.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Laundry Appliances Market Analysis by Mordor Intelligence

The Russia laundry appliances market size was USD 2.74 billion in 2025, is projected to reach USD 2.82 billion in 2026, and is forecast to reach USD 3.28 billion by 2031, reflecting a 3.06% CAGR during 2026-2031. Domestic production expanded in 2024, with output rising 7.3% to 2.7 million washing machines, signaling a real supply-side recovery in the Russia laundry appliances market after earlier disruptions. Early-2025 rouble gains temporarily reduced retail appliance prices by 10-20%, which lifted short-term volumes before renewed currency volatility pressured pricing again in mid-2025. Portfolio depth stabilized as Chinese and Turkish brands filled shelves, with Haier reaching a 14% unit share in Q1 2025 while multi-brand retail chains restored availability across price tiers in the Russia laundry appliances market. Online channels strengthened reach and convenience as e-commerce surpassed 50% of appliance unit sales in 2024, providing a reliable demand conduit even when import routes shifted.

Key Report Takeaways

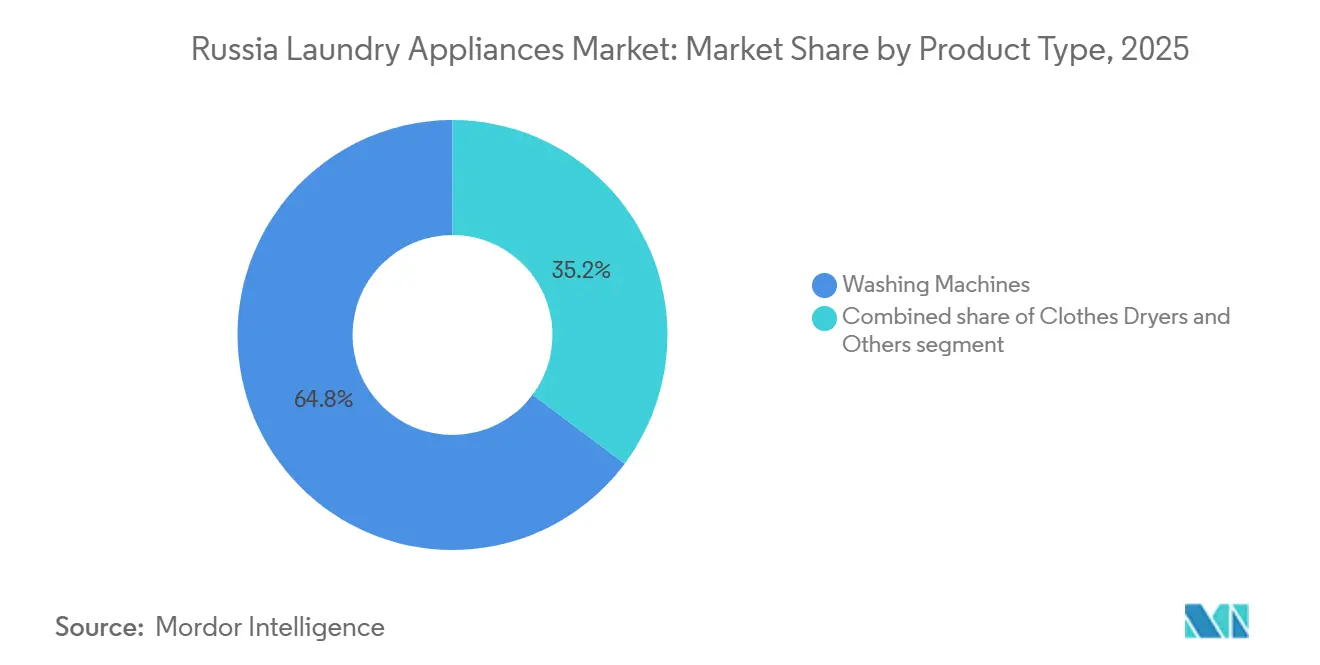

- By product type, standalone washing machines led with 64.79% revenue share in 2025 in the Russia Laundry Appliances market. Clothes dryers are projected to grow at a 3.54% CAGR through 2031.

- By technology, fully automatic machines led by share in 2025 in the Russia Laundry Appliances market and posted the fastest growth through 2031. Retailer merchandising and connected features reinforced adoption across urban households.

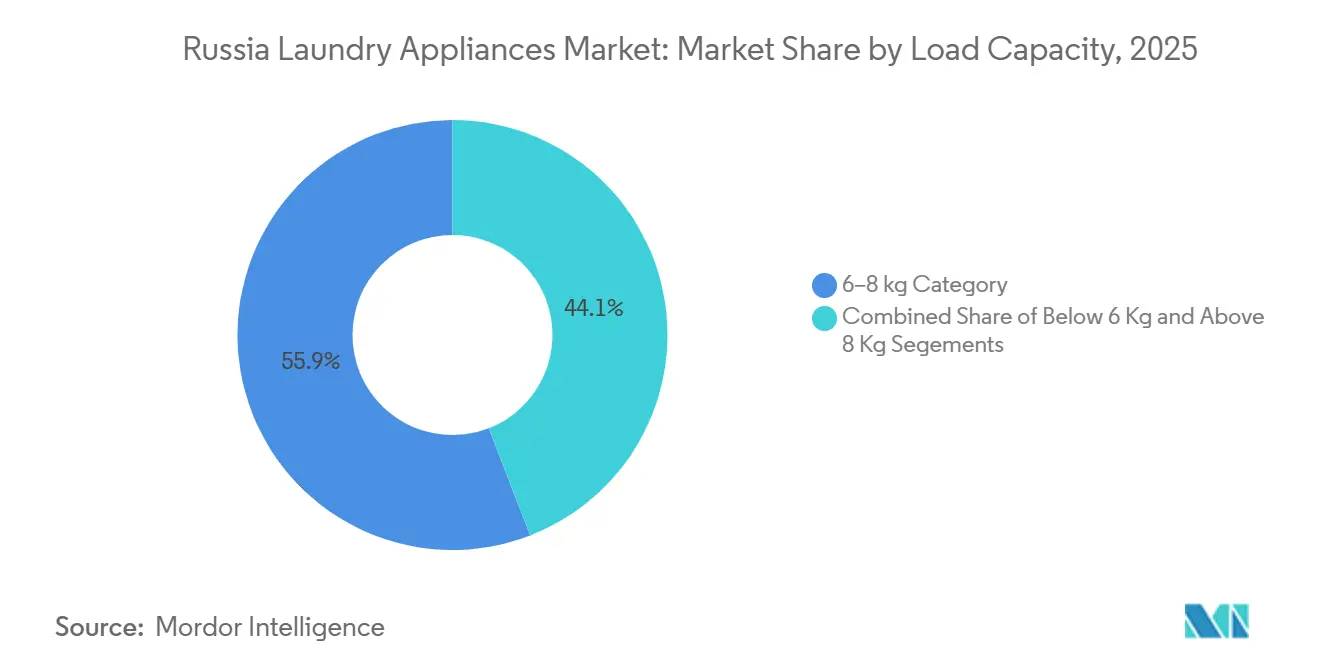

- By load capacity, the 6–8 kg bracket accounted for 55.89% of the market share in 2025 in the Russia Laundry Appliances market. Larger-capacity machines above 8 kg are the fastest risers as families and shared apartments target fewer, larger wash cycles.

- By distribution channel, multi-brand chains held a 51.24% share in the Russia Laundry Appliances market in 2025. Online marketplaces are expanding at a 4.12% CAGR through 2031, driven by dense pickup-point networks and rapid delivery.

- By geography, the Central Federal District accounted for 33.10% of revenue in the Russia Laundry Appliances market in 2025. The Northwestern Federal District is advancing at the fastest 4.52% CAGR through 2031 as local assembly resumes and logistics improve.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Laundry Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Assortment recovery and demand rebound led by Chinese and Turkish brands | +0.7% | National, with the highest penetration in Central, Northwestern, and Southern FD | Medium term (2-4 years) |

| E-commerce and omnichannel expansion lifts reach and convenience | +0.5% | National and urban centers lead rapid adoption in the Far Eastern and North Caucasian FD. | Medium term (2-4 years) |

| Localization and nearshoring of washer manufacturing | +0.6% | Central FD and Volga FD spill over to Northwestern FD | Long term (≥ 4 years) |

| Shift toward 6–8 kg, fully automatic machines in urban households | +0.4% | Central, Northwestern, Southern FD, major cities | Medium term (2-4 years) |

| Parallel-import regime sustaining the availability of global brands | +0.3% | National, import-dependent regions, transit corridors | Short term (≤ 2 years) |

| TR EAEU 048/2019 postponement eases near-term compliance burden | +0.2% | EAEU member states, manufacturers nationally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Assortment Recovery and Demand Rebound Led by Chinese and Turkish Brands

Chinese and Turkish manufacturers rapidly expanded to fill shelf space as several Western and South Korean brands curtailed official supply, restoring choice and steady pricing across the Russian laundry appliance market. Haier reached a 14% unit share in washing machines in Q1 2025, marking a leadership shift and setting a new benchmark for locally assembled volume at mid-tier price points. Beko ranks among the top five and leverages domestic production to mitigate currency swings and shipping delays, which helps stabilize the Russia laundry appliances market during import route adjustments. Retailers broadened brand assortments so consumers could prioritize features and availability over legacy brand prestige, which supported consistent replacement demand through 2025. Service networks tied to local assembly also reassured buyers who avoided parallel-import units without official warranties, which sustained conversion at the point of sale.

E-commerce and Omnichannel Expansion Lifts Reach and Convenience

E-commerce and omnichannel share in appliances reached more than half of the units in the year 2024, driven by marketplaces that established a significant pickup-point footprint, which simplified last-mile collection in both major cities and smaller towns. Wildberries and Ozon converted dense pickup networks into reliable three-day delivery windows in Tier-3 cities, and this convenience supported steady sell-through even during logistics swings that affected inbound imports. M.Video-Eldorado’s hybrid model illustrates the shift as 71% of its 2024 GMV came from online orders, while 1,100 stores functioned as showrooms and same-day pickup hubs across the Russia laundry appliances market [1]M.Video-Eldorado Group, “Store Network, Pickup Hubs, and Online GMV Highlights,” M.Video-Eldorado Group, mvideoeldorado.ru. The showroom-plus-pickup format gives buyers hands-on validation before checkout while keeping fulfillment fast, and this omnichannel mix is now a structural feature in the Russia laundry appliances market. Algorithmic pricing and flash promotions in peak holidays further reduce time to purchase and encourage upgrades to models with higher efficiency or capacity within the Russia laundry appliances market.

Localization and Nearshoring of Washer Manufacturing

Capital investment in deeper localization accelerated in 2024-2025, led by programs that target higher domestic content and shorter supply lines for the Russia laundry appliances market. Haier announced a 13.7 billion rouble expansion plan in 2024 to increase local content in large appliances and set a roadmap toward full localization for mid-tier washing machines by 2027. Local R&D and quality labs tailor products to power and water conditions in key regions, improving durability and reducing service costs in the Russia laundry appliances market. Gazprom Household Systems restarted washing-machine assembly at the former Bosch plant in St. Petersburg in April 2025, restoring over 1 million units of annual capacity and employing 385 workers. Local assembly cuts freight costs and lead times compared to distant imports, helping brands respond faster to seasonal surges in demand and dampening exposure to currency volatility in the Russia laundry appliances market.

Shift Toward 6–8 kg, Fully Automatic Machines in Urban Households.

The 6–8 kg capacity band captured 55.89% in 2025, which aligns with average household sizes and standard 60 cm installation spaces across urban housing stock in the Russia laundry appliances market. Front-load formats held 78.44% in 2025 because under-counter placement and higher spin speeds reduce drying time in space-constrained apartments. Fully automatic machines now account for most sales and continue to expand faster than semi-automatic units, as buyers prefer hands-off operation and app-enabled diagnostics that reduce trial-and-error in cycle selection. Energy-efficient A-class and A+++ models are gaining traction as households respond to tiered electricity tariffs introduced in January 2025, nudging the replacement of older, less efficient units in the Russian laundry appliances market. Larger-capacity models above 8 kg are also gaining momentum among larger families and shared apartments that prioritize fewer weekly cycles and lower per-kilogram operating costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Western/South Korean brand exits and supply-chain constraints | -0.5% | National, urban centers are most affected, with premium gaps in the largest cities. | Medium term (2-4 years) |

| Ruble volatility and inflation curb affordability | -0.7% | National, import-dependent regions, component procurement via Asia and Europe | Short term (≤ 2 years) |

| Warranty and after-sales uncertainty on parallel imports | -0.3% | National consumer-trust erosion in gray-market channels | Medium term (2-4 years) |

| Component dependency limits deep localization scale-up | -0.4% | Central FD and Volga FD, reliance on imported semiconductors and motors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Western/South Korean Brand Exits and Supply-Chain Constraints

Suspensions and exits by key Western and South Korean brands removed premium assortments and weakened service ecosystems, increasing reliance on alternative suppliers and stretching repair capacity in the Russian laundry appliances market. LG partially restarted production in the Moscow region in March 2025 to preserve capabilities, yet broader sourcing remains conditional and has not restored premium availability to pre-disruption norms [2]LG Electronics, “Production Operations Update in Russia,” LG Electronics, kedglobal.com. Parallel imports fill some product gaps but typically arrive without official warranties or certified service coverage, which deters risk-averse buyers from high-end parallel units. Retailers must balance inventory between re-entering global brands and rising Asian alternatives, complicating assortment planning in flagship stores across the Russia laundry appliances market. The net effect is a slower pace of innovation diffusion in premium features and a tilt toward mid-tier models that combine efficiency with reliable support networks.

Ruble Volatility and Inflation Curb Affordability

Currency swings and routing via alternative corridors, such as Kazakhstan or the UAE, add 10-12% to logistics and handling costs, and these overheads are passed through to shelf prices for mid-range models in the Russia laundry appliances market. Early-2025 rouble strength created a temporary price window that lifted unit sales by lowering ticket sizes 10-20%, but a reversion in mid-2025 squeezed that uplift as inputs repriced. Retail buyers in the Russia laundry appliances market are highly sensitive to threshold prices in the mid-tier brackets, and volatility forces retailers to adjust promotions to protect conversion rates. Housing affordability pressures also reduce discretionary budgets for durables, which makes energy savings and after-sales reliability decisive in final purchase decisions. Together, these factors cap premium segment recovery speed while anchoring most of the growth to value and mid-premium tiers in the Russia laundry appliances market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dryers Accelerate as Space Constraints Drive Combo Units

Standalone washing machines accounted for 64.79% of sales in 2025, anchoring replacement demand as households swapped older units for efficient A-class and A+++ models within the Russia laundry appliances market. The policy shift to tiered electricity tariffs in January 2025 sharpened this focus on efficiency and nudged faster replacement of high-consumption legacy machines, which supported steady volumes despite currency swings. Clothes dryers, though a smaller category in absolute terms, are projected to grow at a 3.54% CAGR through 2031 as urban buyers in compact apartments adopt heat-pump designs that fit tight spaces and lower operating costs. The Russia laundry appliances market is also seeing stronger adoption of features that reduce noise and improve water management, which matters for apartment dwellers concerned about neighbor impact and leakage risk. Regional patterns favor heat-pump dryers in colder climates, where outdoor drying is impractical during winter months, and homeowners seek compact, efficient year-round solutions.

A clear pivot from volume-led expansion to value-led upgrades has taken hold since 2024 as buyers emphasize efficiency, capacity, and reliability over basic first-time purchases in the Russia laundry appliances market. Narrow-depth appliances that fit standard 60 cm spaces are a common response to apartment constraints, and marketing emphasizes total cost of ownership to justify upgrades to higher-efficiency machines. Dryer adoption remains below Western European penetration rates, yet positive word of mouth on heat-pump performance and retailer-led financing has started to normalize the category’s appeal beyond early adopters. Product safety and materials compliance remain in focus, with manufacturers aligning designs with EAEU requirements and updated labeling norms to simplify consumer comparisons in showrooms and online listings.

By Technology: Fully Automatic Machines Dominate, Inverter Motors Standard

Fully automatic models accounted for 81.91% of sales in 2025 and are projected to grow at a 3.74% CAGR through 2031, while continuing to outpace semi-automatic machines as urban buyers prioritize convenience, smart presets, and app-connected diagnostics in the Russia laundry appliances market. Inverter motors have become standard in many mid-tier and premium models, reducing noise during spin cycles and extending service life compared with legacy belt-driven designs. This motor platform also reduces energy use relative to earlier-generation machines, aligning with buyers' focus on monthly utility savings following the introduction of tiered tariffs in 2025. Retailers amplify this shift by merchandising connected features and promoting no-interest installment plans that bring premium capabilities within reach for households upgrading from older models in the Russia laundry appliances market.

Smart-home features add day-to-day utility by letting users set cycles and receive alerts, reducing laundry time spent planning and helping avoid re-washes due to forgotten loads. Updated energy-efficiency labels under GOST in early 2024 improved transparency for buyers comparing models online or in store, and that clarity supports the premium for efficient, fully automatic machines across the Russia laundry appliances market. Together, these technology upgrades reinforce a durable value proposition that drives steady replacement demand even when discretionary budgets are under pressure.

By Load Capacity: Mid-Range 6–8 kg Aligns with Household Norms, Larger Units Surge

The 6–8 kg band captured 55.89% in 2025, aligned with common apartment footprints and the weekly laundry volume of three to four-person households in the Russia laundry appliances market. These models balance purchase price, energy per cycle, and installation ease, which sustains their position as the default upgrade path for mainstream buyers. Larger-capacity units above 8 kg are gaining momentum among larger households and shared apartments that prefer fewer, larger cycles, which optimize time and reduce per-cycle overhead in the Russia laundry appliances market. Below-6 kg models remain relevant for micro-apartments and certain rental formats, yet their share trends modestly lower as developers deliver more layouts with space for standard 60 cm appliances.

Since 2024, manufacturers have focused on fine-tuning drum sizes and cabinet depths to fit common installation constraints while maintaining efficiency at higher capacities, helping upsell buyers from 6 kg to 7-8 kg machines. Clearer labeling and retailer comparison tools also ease cross-shopping between 7 kg and 10 kg models, reducing friction and supporting a steady move up the capacity curve in the Russia laundry appliances industry. Over time, these products and merchandising shifts should keep the 6–8 kg segment at the center of the category while larger drums steadily rise from a smaller base across the Russia laundry appliances market.

By Distribution Channel: Multi-Brand Stores Steady, Online Marketplaces Ascendant

Multi-brand chains held a 51.24% share in 2025, led by nationwide networks that offer hands-on evaluation, expert guidance, and immediate pickup for heavy appliances in the Russia laundry appliances market. Showrooms allow buyers to test door openings, assess noise levels, and confirm installation measures before committing to delivery windows, thereby reducing returns and improving satisfaction. Retailers reinforce conversion with 0% APR installment plans, which help spread payments for higher-efficiency or larger-capacity models without price shocks at checkout in the Russia laundry appliances market. Online channels are expanding at a 4.12% CAGR through 2031 as marketplaces leverage dense pickup-point networks and algorithmic pricing to serve buyers nationwide.

Marketplaces scale regional reach by opening thousands of pickup points annually, enabling two- to three-day fulfillment for a growing share of the Russia laundry appliances market. As a result, share shifts are likely to continue favoring online through 2031, although multi-brand stores remain crucial for high-touch consultation and same-day pickup in large urban areas.

Geography Analysis

The Central Federal District accounted for 33.10% of revenue in 2025, with Moscow’s dense retail infrastructure and widespread under-counter installation norms anchoring steady upgrade cycles in the Russia laundry appliances market. New apartments across the district frequently include standardized washing-machine hookups, which simplifies initial purchase decisions for first-time movers and supports faster replacement timing. Tiered electricity tariffs, effective from January 2025, are driving the faster retirement of older, energy-intensive units in favor of A-class and A+++ appliances that reduce monthly bills, thereby supporting value-led growth in the region. The district’s proximity to Tatarstan and St. Petersburg plants lowers inbound logistics costs and shortens lead times for warranty parts, which helps sustain service levels in the Russia laundry appliances market.

The Northwestern Federal District is posting the fastest projected CAGR of 4.52% to 2031, underpinned by the April 2025 restart of washing-machine assembly at the former Bosch plant in St. Petersburg, which restored more than 1 million units of annual capacity and added 385 jobs. Baltic port access also shortens replenishment cycles for inbound components compared with inland routes, which supports rapid restocking around seasonal demand peaks in the Russia laundry appliances market. Local tourism and hospitality activity across the district drives consistent demand for larger-capacity units to support guest turnover, supporting a resilient commercial base for selected models. Public housing modernization initiatives expand the household base by installing standardized hookups that convert into first-time purchases or timely replacements across the district.

Outside the core poles of Central and Northwestern districts, regional shares are smaller, but momentum vectors vary across the Russia laundry appliances market. The Volga Federal District benefits from proximity to Tatarstan’s manufacturing cluster, which reduces freight costs and supports steady service coverage for surrounding municipalities. The Southern and North Caucasus regions emphasize e-commerce pickup and flexible delivery models due to variable retail densities in suburban and rural areas, which keep online share rising [3]Government of the Republic of Tatarstan, “Industrial Footprint and Logistics Advantages,” Made in Tatarstan, madeintatarstan.ru. In Siberia and the Urals, cross-docking hubs opened by marketplaces have shortened delivery times for bulky goods, improving unit sell-through even in remote settlements and stabilizing demand during winter months. The Far East continues to benefit from port proximity and logistics innovations that reduce lead times from Northeast Asian factories, and these structural tailwinds are supporting faster-than-average growth in the Russia laundry appliances market.

Competitive Landscape

The Russia laundry appliances market remains moderately concentrated, with the top five players holding an estimated 50-60% combined share as of 2025, while mid-tier and niche brands compete for the remainder. Haier’s 14% unit share in Q1 2025 reflects scale benefits tied to local assembly and consistent mid-tier pricing in major urban centers. Indesit maintained a sizable presence at 13% in available 2025 snapshots, while Beko, LG, and Candy round out the top five with competitive pricing, connected features, and service networks that address buyer risk around long-term ownership in the Russia laundry appliances market. Since early 2024, retailer shelf sets have prioritized locally assembled, well-supported models to reduce warranty friction, helping stabilize conversion and repeat purchases.

Two capability paths define the current race. Brands with local assembly are deepening component localization to reduce foreign-exchange exposure and compress lead times, while re-entering global players are focusing on higher-margin connected models where brand equity sustains pricing in the Russia laundry appliances market. LG’s partial restart of the Moscow-region facility in March 2025 preserved manufacturing readiness and sent a signal on premium-segment re-engagement contingent on broader conditions [4]LG Electronics, “Factory Operations Status,” LG Electronics, kedglobal.com. Gazprom Household Systems returned the washing-machine assembly to St. Petersburg in April 2025 and implemented AI-driven quality controls to reduce warranty claims, a competitive lever as buyers rank after-sales reliability alongside efficiency in the Russia laundry appliances market.

Manufacturers are also aligning portfolios to the most resilient demand pockets. Narrow-depth, under-counter front-loaders with 6–8 kg drums anchor volume, while high-capacity models serve larger households and commercial operators that prioritize fewer cycles and faster turnover. Technology differentiators revolve around inverter motors, efficient wash programs, and app-based diagnostics, which lower lifetime costs and simplify ownership across the Russia laundry appliances market. As warranty and service remain decisive, established networks with broad parts availability are a durable source of advantage that parallel-import channels cannot easily replicate.

Russia Laundry Appliances Industry Leaders

Haier

LG Electronics

Samsung Electronics

Beko (Arçelik)

Hotpoint

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Gazprom Household Systems completed reconstruction of its washing-machine facility at the former Bosch plant in St. Petersburg, restoring annual production capacity to over 1 million units and employing 385 workers, with AI-driven quality-control cameras for real-time defect detection.

- April 2025: Midea Group acquired Küppersbusch’s parent company, adding European premium design capabilities and signaling intent to introduce mid-premium laundry appliances supported by localized manufacturing.

- March 2025: LG Electronics partially restarted washing-machine and refrigerator production at its Moscow-region facility after a multi-year suspension, producing limited quantities to preserve operational capabilities.

- September 2024: Iranian Entekhab Group initiated negotiations to acquire a Tatarstan appliance plant, reflecting fluid ownership dynamics for regional manufacturing assets in Russia.

Russia Laundry Appliances Market Report Scope

A laundry appliance is a machine used for cleaning and rinsing textiles with water, but is not limited to washing. It can also be used for drying purposes. The Russia laundry appliances market is segmented by product type (washing machines, clothes dryers, and others (garment steamers, electric irons, laundry dehumidifiers)), by technology (fully automatic and semi-automatic/ manual), by laod capacity (below 6 kg, 6-8 kg, and above 8 kh), by distribution channel (multi brand stores, exclusive brand outlets, online, and other distribution channels), and by geography (Central, Northwestern, Southern, Volga, Rest Of Russia FDs). The report offers market size and forecasts for the United States laundry appliances market in value (USD) for all the above segments.

By Product Type

| Washing Machines |

| Clothes Dryers |

| Others (Garment Steamers, Electric Irons, Laundry Dehumidifiers) |

By Technology

| Fully Automatic |

| Semi-Automatic / Manual |

By Load Capacity

| Below 6 kg |

| 6–8 kg |

| Above 8 kg |

By Distribution Channel

| Multi-brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| Central FD |

| Northwestern FD |

| Southern FD |

| Volga FD |

| Rest Of Russia |

| By Product Type | Washing Machines |

| Clothes Dryers | |

| Others (Garment Steamers, Electric Irons, Laundry Dehumidifiers) | |

| By Technology | Fully Automatic |

| Semi-Automatic / Manual | |

| By Load Capacity | Below 6 kg |

| 6–8 kg | |

| Above 8 kg | |

| By Distribution Channel | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Geography | Central FD |

| Northwestern FD | |

| Southern FD | |

| Volga FD | |

| Rest Of Russia |

Key Questions Answered in the Report

What is the Russia laundry appliances market size today, and how fast will it grow?

The Russia laundry appliances market size was USD 2.74 billion in 2025, is projected at USD 2.82 billion in 2026, and is forecast to reach USD 3.28 billion by 2031 at a 3.06% CAGR during 2026-2031.

Which product categories are leading demand in the Russia laundry appliances market?

Standalone washing machines led with a 64.79% share in 2025, and clothes dryers are the fastest-growing segment, with a 3.54% CAGR through 2031 as heat-pump models spread in cities.

What company strategies are most effective in the Russia laundry appliances market?

Local assembly and deeper component localization reduce currency and logistics risks, while premium connected models supported by strong service networks defend pricing and trust.

What factors could restrain near-term growth for laundry appliances in Russia?

Rouble volatility that lifts component costs and limited warranty coverage on parallel imports can slow upgrades to premium units compared with locally supported models.

Page last updated on: