Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Russia Data Center Rack Market is Segmented by Rack Size (Quartely Rack, Half Rack, Full Rack), Rack Height (42U, 45U and More), Rack Type (Cabinet (Closed) Racks, Open-Frame Racks, Wall-Mount Racks), Data Center Type (Colocation Facilities, Hyperscale and Cloud Service Provider DCs, Enterprise and Edge), Material (Steel, Aluminum, Other Alloys and Composites). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

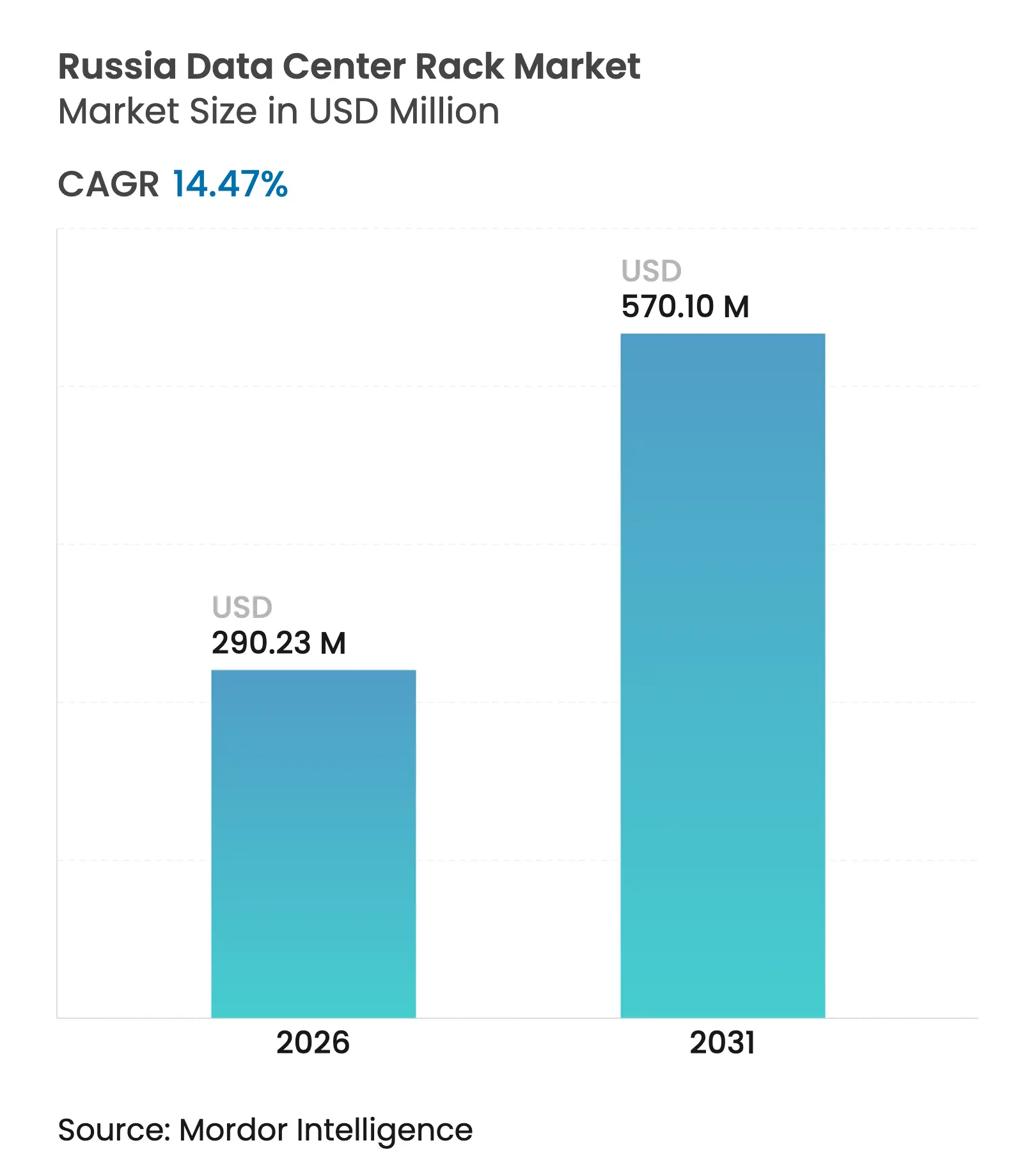

| Market Size (2026) | USD 290.23 Million |

| Market Size (2031) | USD 570.1 Million |

| Growth Rate (2026 - 2031) | 14.47 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Russia data center rack market size in 2026 is estimated at USD 290.23 million, growing from 2025 value of USD 253.53 million with 2031 projections showing USD 570.1 million, growing at 14.47% CAGR over 2026-2031. Adoption of sovereign cloud platforms, stricter data-localisation mandates, and the push for AI-ready infrastructure are steering demand toward high-density, liquid-ready racks. Government programs such as the Digital Economy national initiative and Resolution 1875 are directing state entities toward Russian-origin hardware, giving local manufacturers sustained visibility over order pipelines. At the same time, cold-region conversions in Norilsk, Karelia and Irkutsk are lowering operating costs and enabling 40-140 kW rack densities with limited additional cooling investment. Supply-chain turbulence caused by Western sanctions has inflated component prices, yet it has also catalysed domestic production lines, with companies such as YADRO and Trinity adding engineering capacity and investing in new sheet-metal and powder-coating lines. The resulting interplay between localisation policies and rising computational loads underpins the upward trajectory of the Russia data center rack market.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Accelerating shift to cloud & hybrid IT architectures

Accelerating shift to cloud & hybrid IT architectures

| +2.8% | Moscow & St Petersburg | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+2.8%

|

Geographic Relevance

:

Moscow & St Petersburg

|

Impact Timeline

:

Medium term (2-4 years)

|

Surge in edge-computing / IoT deployments

Surge in edge-computing / IoT deployments

| +2.1% | Regional hubs, Siberia, Far East | Long term (≥ 4 years) | |||

Digital Economy national program & data-localisation

laws

Digital Economy national program & data-localisation

laws

| +3.2% | National | Short term (≤ 2 years) | |||

Rising rack density for AI/HPC colocation workloads

Rising rack density for AI/HPC colocation workloads

| +2.4% | Moscow region, nuclear-powered sites | Medium term (2-4 years) | |||

Sovereign AI clouds driving high-thermal-load racks

Sovereign AI clouds driving high-thermal-load racks

| +1.9% | Priority AI regions | Long term (≥ 4 years) | |||

Conversion of cold-region industrial sites into green DCs

Conversion of cold-region industrial sites into green DCs

| +1.3% | Arctic, Siberia, Far East | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Accelerating Shift to Cloud & Hybrid IT Architectures

Domestic providers are scaling rapidly as government restrictions phase out foreign cloud services, compelling enterprises to migrate workloads to Russian platforms. Selectel’s 1,000-rack Tier III facility in St Petersburg, built with a RUB 1 billion(USD 0.041 billion) investment, illustrates the magnitude of build-outs required to absorb repatriated workloads. These projects standardise on full-height cabinet racks supporting 40 kW+ densities and direct-to-chip liquid loops, ensuring seamless integration of on-premises and sovereign-cloud nodes. In parallel, ministries shifting to hybrid models are issuing multi-year framework contracts that specify common rail depths, perforation ratios, and monitoring interfaces, amplifying volume demand across the Russia data center rack market.

Surge in Edge-Computing / IoT Deployments

Russia’s vast geography creates natural edge computing corridors for oil, gas, and mining. The Republic of Sakha’s distributed-energy optimisation programme uses ruggedised 15- 22U racks built to IP55 for permafrost environments.[1]Natalia Voloshina, “Edge Racks for Permafrost Sites,” IOP Conference Series, iopscience.iop.org Anticipated nationwide 5G roll-outs by 2030 will scatter micro-modular data centres across regional cities, increasing demand for lightweight aluminum frames that can be craned onto rooftops. Providers are piloting sealed immersion columns to cope with desert-to-arctic temperature swings without adding moving parts. These innovations collectively widen the footprint of the Russia data center rack market, penetrating previously underserved locales. Long-term contracts from energy majors and rail operators are already visible on order books, supporting a forward pipeline beyond 2028.

Digital Economy National Program and Data-Localisation Laws

Amended personal-data legislation now obliges storage and processing inside national borders, enforcing stricter uptime and security targets. State bodies have ring-fenced budgets to deploy federated clusters across at least three regions, each requiring 100-200 standardized 42U cabinets per site. Moscow’s AI regulatory sandbox additionally mandates hardware-level isolation for algorithm training datasets, favouring lockable cabinet doors, dual-factor access panels, and tamper-proof rail kits government. Local manufacturers compliant with Resolution 1875 win preference, pushing foreign-branded open-frame imports to niche status.

Rising Rack Density for AI/HPC Colocation Workloads

Sovereign banks and research institutes are installing GPU-heavy nodes to bridge compute gaps with global peers. Sber’s projected RUB 400-450 billion AI revenue for 2024 translates into capacity calls for 35-45 kW racks in its Moscow campus. Elbrus-B and 128-core platforms are pushing rack power envelopes toward 100 kW, necessitating rear-door heat exchangers and cold-plate loops. Colocation operators capturing this wave pre-plumb racks for warm-water returns above 40 °C, lowering chiller loads and unlocking higher white-space revenues per square metre. Standardisation on 48U heights keeps cable management clear of cooling manifolds, illustrating how workload trends keep re-shaping rack bill-of-materials and deepening the Russia data center rack market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Supply-chain disruption & sanctions on western

components

Supply-chain disruption & sanctions on western

components

| -2.7% | National, acute in Moscow | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-2.7%

|

Geographic Relevance

:

National, acute in Moscow

|

Impact Timeline

:

Short term (≤ 2 years)

|

High power tariffs & grid bottlenecks in Moscow region

High power tariffs & grid bottlenecks in Moscow region

| -1.8% | Moscow metro, major cities | Medium term (2-4 years) | |||

Scarcity of suitable real estate in Tier-1 metros

Scarcity of suitable real estate in Tier-1 metros

| -1.4% | Moscow, St Petersburg | Medium term (2-4 years) | |||

Shortage of skilled labour for liquid-cool racks

Shortage of skilled labour for liquid-cool racks

| -1.1% | Technical hubs | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Supply-Chain Disruption & Sanctions on Western Components

September 2024 curbs on IT service exports increased lead times for PDUs, busways and server rails sourced from Europe. Spot aluminum prices jumped after Rusal’s alumina imports were disrupted, inflating metal costs for local rack fabricators. [2]Arnold Porter, “New Sanctions and Export Controls Restrict Russia’s Access to IT Services and Software | Advisories,” arnoldporter.com In response, domestic firms doubled down on vertical integration, with YADRO opening a laser-cutting line and Trinity shifting to locally sourced fasteners. Although these pivots cushion supply-risk over the long term, the immediate effect clips near-term output, shaving 2.7 percentage points off the Russia data center rack market CAGR

High Power Tariffs & Grid Bottlenecks in Moscow Region

Moscow’s distribution grid cannot keep pace with data centre loads, forcing new projects to queue behind 12-18-month upgrade cycles, mirroring London and Dublin backlogs. Operators divert builds to Kalinin’s nuclear-adjacent campus, where 80 MW captive capacity eliminates tariff premiums.[3]Self-regulatory organization in the field of energy audit, “The Scheme and program for the development of electric power systems of Russia for 2025-2030 have been approved.” sro150.ruHowever, migrating beyond the capital raises latency for financial-trading clients, limiting uptake. Consequently, designers are prioritising high-efficiency rack power trains, 48VDC busbars, 98%-efficient PSUs—to stretch every kilowatt secured in Moscow, partly offsetting the restraint’s 1.8 percentage-point drag on overall growth.

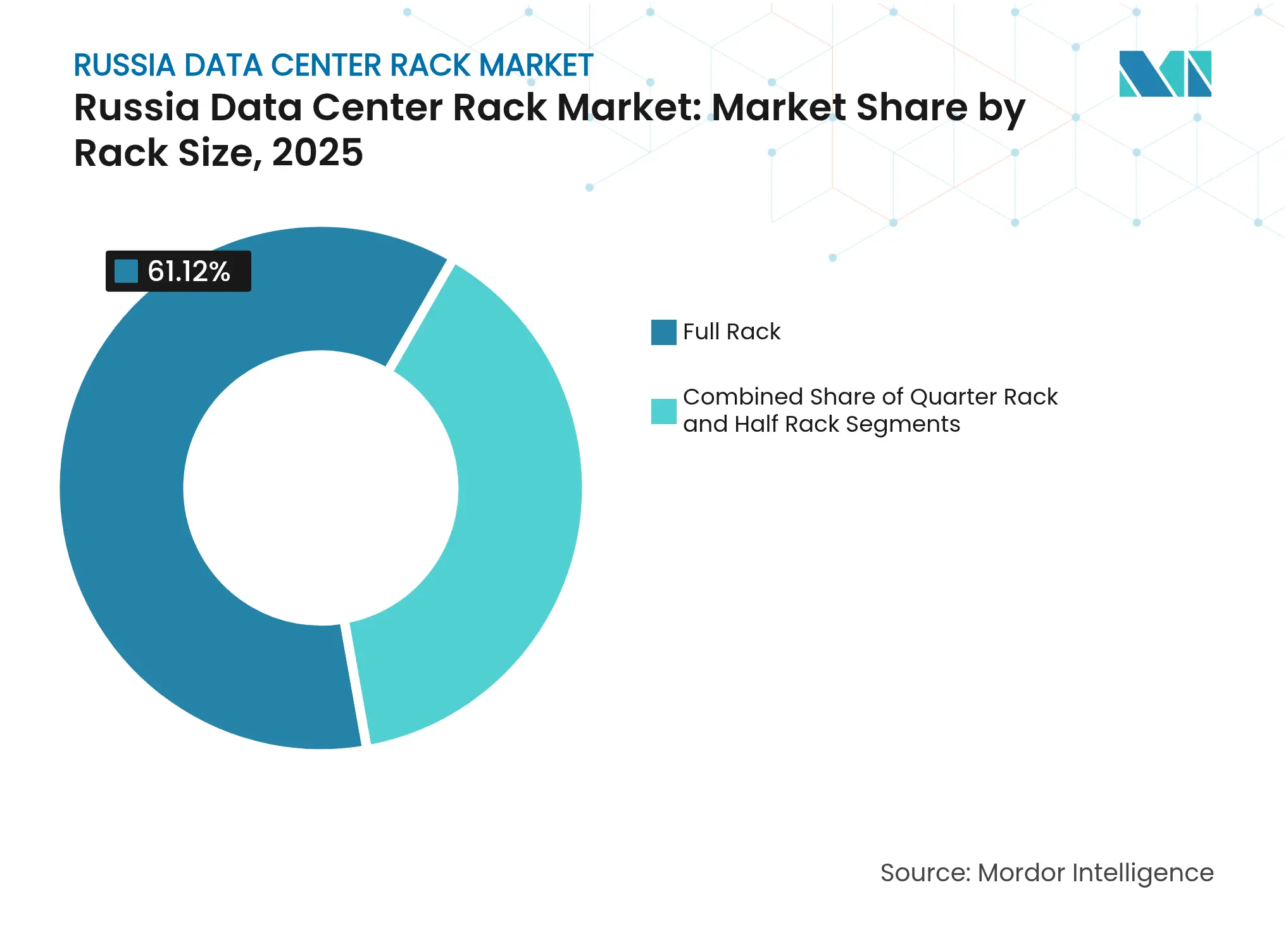

By Rack Size: Full Rack Dominance Drives Standardisation

Full-size cabinets captured 61.12% of Russia data center rack market share in 2025 and hold the fastest 15.41% CAGR through 2031. Their popularity reflects federal digitisation contracts that specify 42U-47U enclosures for consistent asset management across ministries. In value terms, the Russia data center rack market size for full racks is projected to surge to USD 367.4 million by 2031, nearly triple quarter-rack revenues. Quarter and half racks remain relevant in Siberian edge nodes where smaller footprints fit telecom shelters, yet their combined growth trails at 9.38%.

Full-rack standardisation lets manufacturers optimise production around fewer SKUs, reducing die-change downtime and enabling batch powder-coating. Operators benefit from uniform cable ladders, blanking panels and airflow patterns, cutting provisioning time for AI clusters. Selectel’s latest campus in St Petersburg reserved 95% of floorspace for full racks, with each row pre-equipped for 50 kW liquid loops, illustrating the efficiency-reliability mix that keeps full racks at the core of the Russia data center rack market

Note: Segment shares of all individual segments available upon report purchase

By Rack Height: 42U Standard Meets 48U Innovation

The 42U segment commanded 51.02% Russia data center rack market share in 2025. Yet 48U skews lead growth at 14.62% CAGR as AI nodes demand more vertical real estate for in-rack manifolds and GPU sleds. The Russia data center rack market size for 48U cabinets may hit USD 145.8 million by 2031, aided by hyperscalers retrofitting existing halls without widening aisles.

48U adoption also stems from immersion baths requiring taller tank liners and raised pump assemblies. Conversely, 45U frames satisfy legacy telco sites where ceiling heights restrict expansion. Supercomputing labs occasionally specify >52U, but volumes stay niche. The ensuing mix ensures fabricators keep multiple bending profiles yet focus automation on the two leading heights, balancing innovation and throughput across the Russia data center rack market.

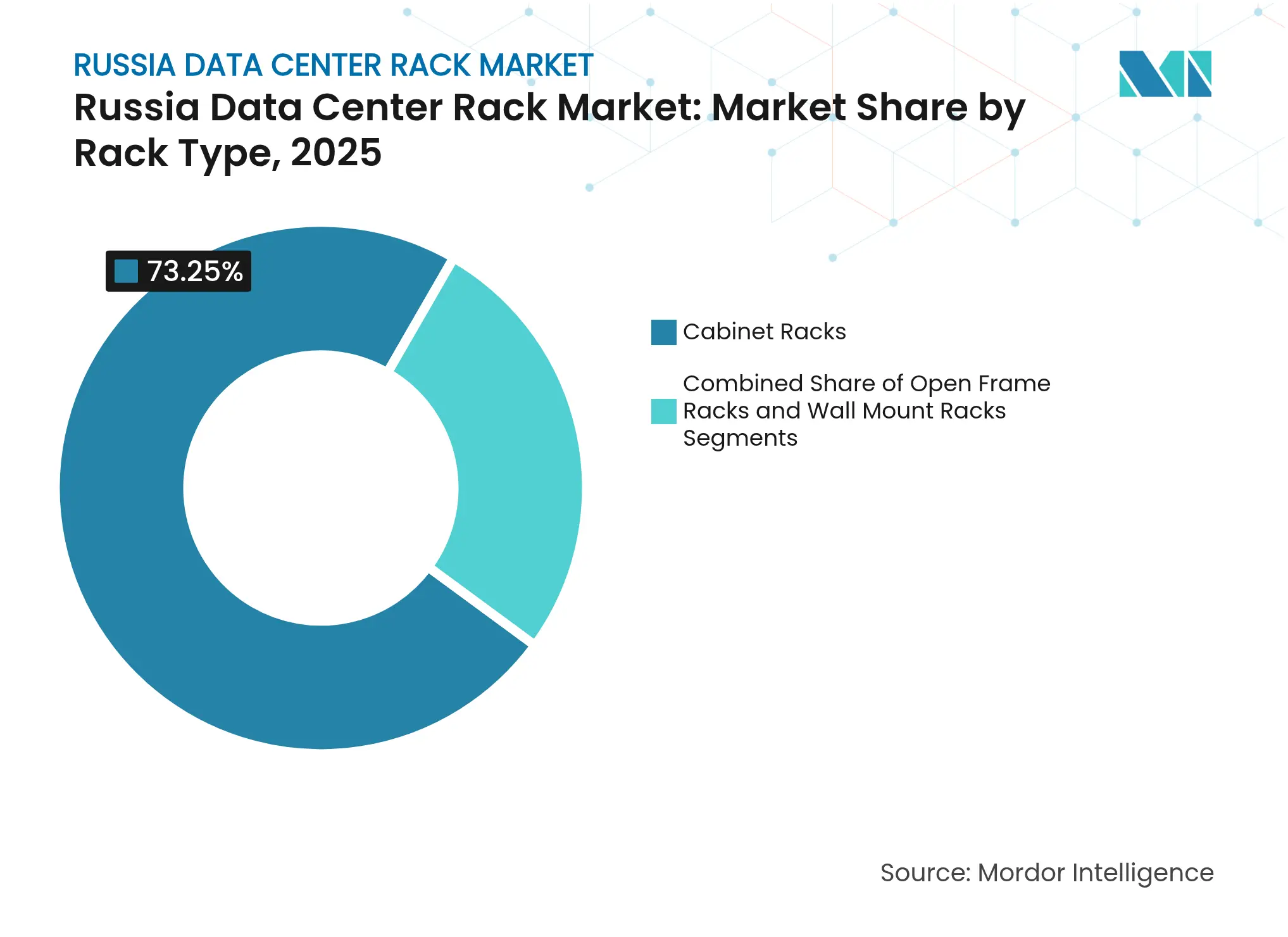

By Rack Type: Cabinet Security Drives Market Leadership

Cabinet (closed) enclosures owned 73.25% share in 2025 and are set for a 16.23% CAGR as cybersecurity law tightens. Cabinet locks, mesh doors, and gasketed panels help agencies comply with new secrecy clauses covering genomic, defense, and geospatial data. Accordingly, the Russia data center rack market size for cabinets should exceed USD 456.8 million by 2031. Open-frame racks cater to labs needing rapid re-cabling, whereas wall-mount units stay critical for roadside 5G edge deployments.

The cabinet trend dovetails with liquid-cool retrofits. Sealed chassis confines leaks and maintains airflow segregation, reducing mean-time-to-repair. Suppliers integrate drip-lining trays and quick-disconnect couplers as standard, turning cabinets into containment ecosystems rather than passive shells, thereby reinforcing their primacy in the Russia data center rack market.

Note: Segment shares of all individual segments available upon report purchase

By Data Center Type: Colocation Leadership Faces Hyperscale Challenge

Colocation providers held 51.64% Russia data center rack market share in 2025. Nevertheless, hyperscale builds led by Nebius and Rostelecom Cloud show a 16.72% CAGR, steering the market toward campus-level repeatability. Hyperscalers insist on integrated busway channels, fixed airflow baffles, and blind-mate power shelves to enable robotised deployment. Colocation operators remain essential for mid-market customers and sovereign-state agencies that prefer cage-level control. Edge micro-sites progress steadily in rail and pipeline corridors, yet their low density caps revenue share. Together, the mix keeps supply diversified, but growth gravitates toward hyperscale-friendly rack templates across the Russia data center rack market.

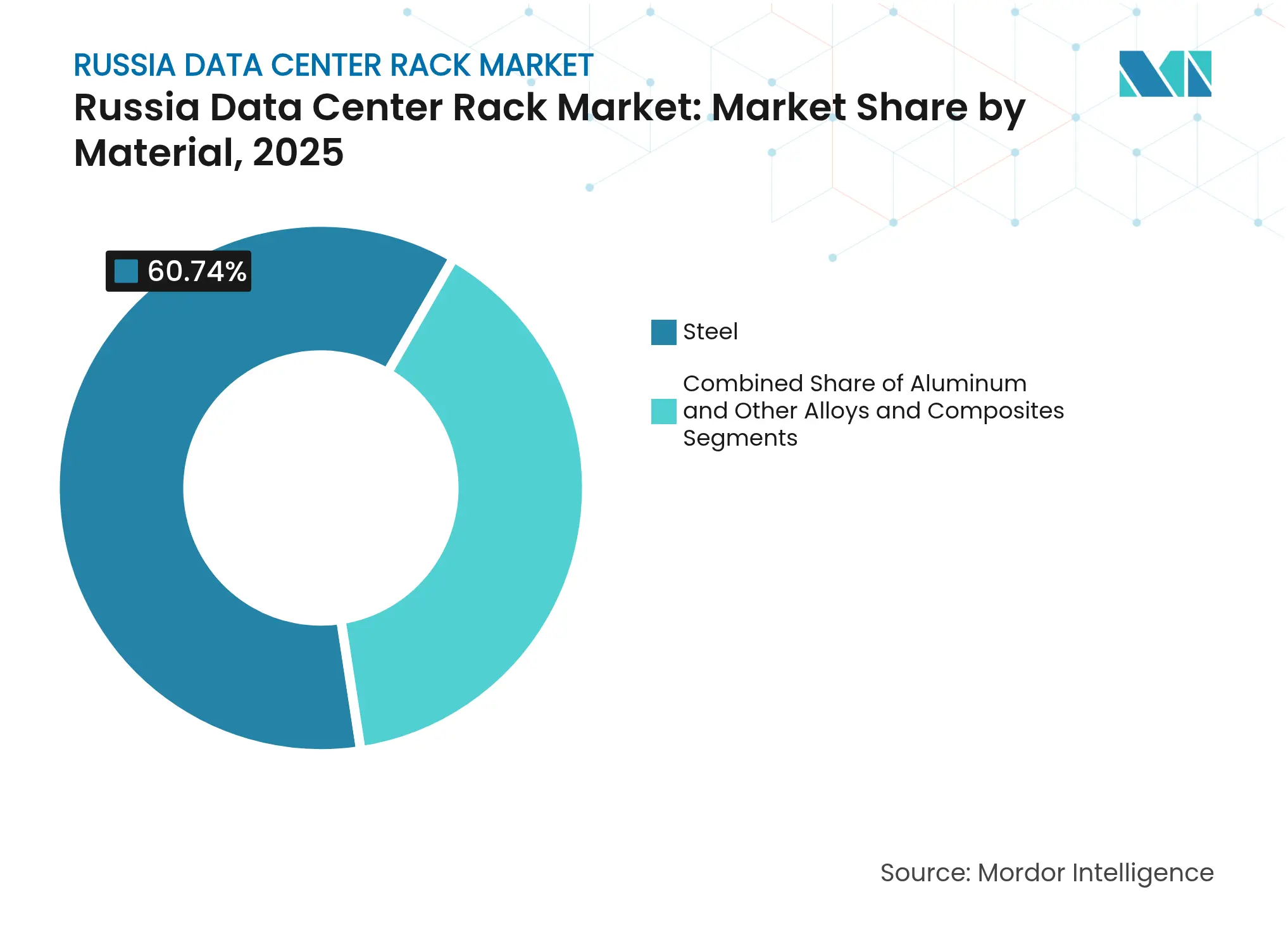

By Material: Steel Dominance Challenged by Aluminum Innovation

Steel racks retained 60.74% share in 2025 owing to cost and entrenched metallurgy capacity. However, aluminum variants are rising at 15.93% CAGR, poised to claim 43.15% share by 2031. Lighter frames cut freight and floor-loading, crucial for high-rise Moscow facilities. The Russia data center rack market size for aluminum could climb to USD 246.3 million by 2031, narrowing the gap with steel.

Aluminum’s thermal conductivity also enhances passive heat dissipation around busbars. Sanction-driven alumina shortages prompted smelters to retool for domestic ore blends, aligning price curves with long-run contract needs. Composite hybrids—steel uprights with aluminum doors—are entering pilot production, signalling the next innovation wave that will keep material science central to competitive positioning within the Russia data center rack market.

Note: Segment shares of all individual segments available upon report purchase

Moscow and St Petersburg remain the gravitational centres of the Russia data center rack market. Demand clusters around financial trading, central government and content-delivery hubs, even as power-connection queues stretch beyond 600 MW. Operators mitigate grid risk by deploying 40-55 kW racks with high-efficiency rear-door exchangers, extracting more compute from scarce megawatts.

The Siberian Federal District leverages cheap hydroelectricity and ambient temperatures below 0 °C for eight months of the year. Arctic and Far-East deployments create an emerging third pole. Norilsk’s BitCluster Nord exploits average annual temperatures of -12 °C to eliminate chillers, supporting 140 kW liquid-immersion racks. Buryatia and Khabarovsk projects ride surplus hydropower to host energy-intensive compute, including blockchain and AI-render farms. Though connectivity lags, government fibre corridors under the Arctic Development Strategy will close gaps by 2027, bringing new addressable volume to the Russia data center rack market.

Market Concentration

The market is moderately fragmented. Schneider Electric, operating locally as Systeme Electric, still tops volume shipments but faces accelerating share erosion as Resolution 1875 channels state orders to domestic firms.. Huawei sustains share through joint ventures that localise cabinet final assembly inside the Vladimir region, circumventing tighter import rules.

Competitive vectors split along high-density capability and compliance features. YADRO’s new 48U liquid-loop rack rated at 120 kW won the Kalinin nuclear-campus tender, while Systeme Electric emphasises tool-less fastening and rapid earthing bars for edge cabinets.

Strategic alliances are also redefining the field. A six-centre supercomputing consortium standardised on a common 45U cabinet footprint, giving the selected vendor recurring demand across research institutes. Simultaneously, cold-region specialists co-develop immersion-ready aluminum frames with mining companies, blending sectoral knowledge into product roadmaps. This flurry of localisation, specialisation and partnership keeps competitive intensity high and sustains innovation throughout the Russia data center rack market.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE and GROWTH FORECASTS(VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES and FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the Russia data center rack market as factory-built, stand-alone enclosures, open-frame, wall-mount, or cabinet style, used to mount servers, storage, and networking equipment inside Russian commercial and institutional data centers.

Scope Exclusion: Telecom street cabinets, modular container frames, and refurbished racks are not covered.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

Conversations with colocation operators, hyperscale facility contractors, and rack OEM channel partners across Moscow, St. Petersburg, Novosibirsk, and Ekaterinburg provided run-rate prices, preference shifts toward 48U frames, and realistic replacement cycles that reconcile with the secondary inputs.

Desk Research

Mordor analysts began with open statistics from the Ministry of Digital Development, Rosstat customs codes 847330 and 940320, and Federal Tax Service import declarations that reveal unit flows and declared values. We next tapped technical papers in IEEE Xplore on high-density liquid-ready frames, white papers from the Association of Russian Data Centers, and regional power-tariff datasets published by the System Operator of the Unified Power System to gauge rack power ratings. Company filings and tender documents on D&B Hoovers and Dow Jones Factiva supplied real purchase prices, while patent counts pulled from Questel highlighted emerging 48U-plus designs. This list is illustrative; many other public and paid sources informed data collection, validation, and clarification.

Market-Sizing & Forecasting

We reconstructed 2025 revenue through a top-down import and production reconciliation, then validated it with selective bottom-up roll-ups of sampled average selling price multiplied by rack shipments shared by interviewed vendors. Core variables feeding the model include installed data center floor area, average density (kW per rack), ruble-dollar conversion, sanctions-related component mark-ups, and hyperscale capacity additions announced in public filings. A multivariate regression with these drivers produces the 2026-2030 trajectory; scenario analysis adjusts for potential easing or tightening of technology export controls. Gaps in bottom-up estimates are bridged by triangulating adjacent indicators such as PDU sales and containment aisle orders.

Data Validation & Update Cycle

Outputs pass anomaly checks against historic rack counts, energy consumption, and customs trends. Senior analysts review variances and re-contact key sources when deviations exceed five percent. Reports refresh every twelve months with interim revisions if major policy or supply events occur; an analyst performs a fresh pass before client delivery.

Why Our Russia Data Center Rack Baseline Commands Reliability

Benchmark comparison

Published figures often diverge because providers pick unlike rack definitions, pricing ladders, and update cadences. Awareness of these levers lets purchasers judge which baseline aligns with their own planning horizon.

Key gap drivers include counting physical racks rather than revenue, applying global splits to Russia without ruble inflation alignment, or omitting higher-priced 48U transitions that our model captures.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 253.53 million (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

70.31 k racks (2024) | Regional Consultancy A | Quantity metric only; ignores ASP variation and forecast price shifts | ||

USD 5.17 billion (2025, global) | Global Consultancy A | Allocates value to Russia via GDP weight; narrower rack-height scope | ||

USD 2.71 billion (2025, global) | Trade Journal B | Uses OEM shipment totals; excludes retrofit racks and currency conversion nuances |

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.