Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

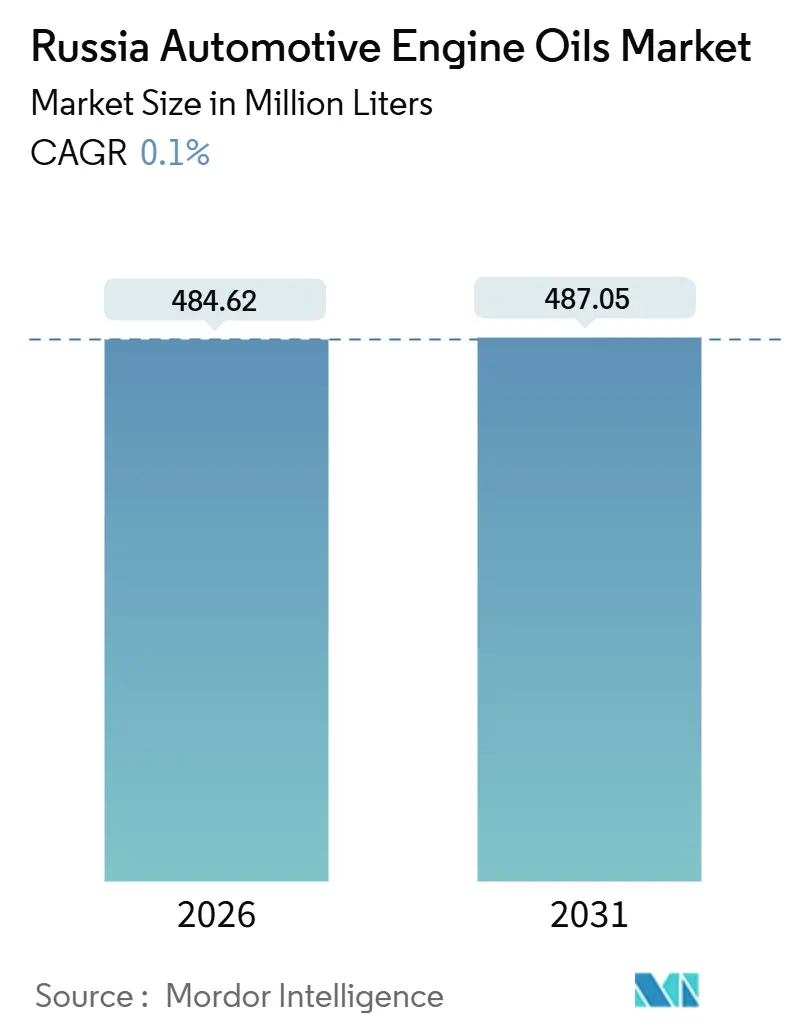

| Market Volume (2026) | 484.62 Million liters |

| Market Volume (2031) | 487.05 Million liters |

| Growth Rate (2026 - 2031) | 0.10% CAGR |

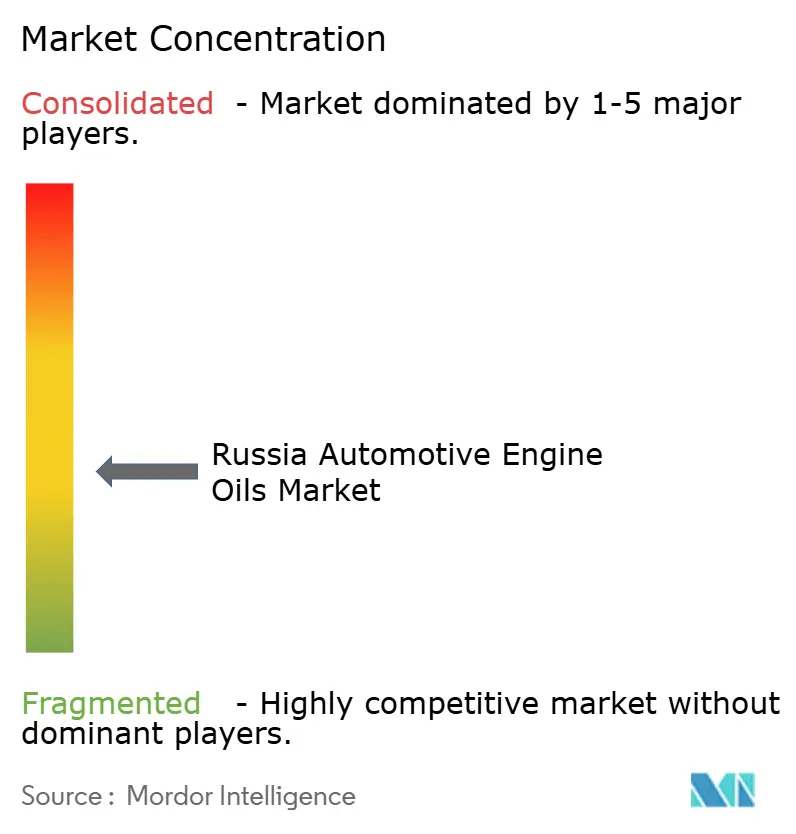

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Russia Automotive Engine Oils Market Analysis by Mordor Intelligence

The Russian Automotive Engine Oils Market size is estimated at 484.62 million liters in 2026, and is expected to reach 487.05 million liters by 2031, at a CAGR of 0.10% during the forecast period (2026-2031). This near-flat trajectory conceals a structural overhaul in supply chains and consumption patterns. The rapid departure of Western OEMs after 2022 collapsed local vehicle assembly, yet the national fleet keeps aging, so total mileage and lubricant change-outs remain broadly intact. Domestic refiners now lead the shift from imported to locally blended oils as Gazpromneft-Lubricants, Lukoil, and Rosneft channel crude-to-retail integration advantages into price and logistics resilience. Demand is also tilting toward higher-margin synthetics as the Omsk GIDP complex unlocks Group III base-oil capacity. Meanwhile, a mandatory digital product-marking regime effective September 2025 raises compliance costs for small blenders and funnels share toward IT-capable majors.

Key Report Takeaways

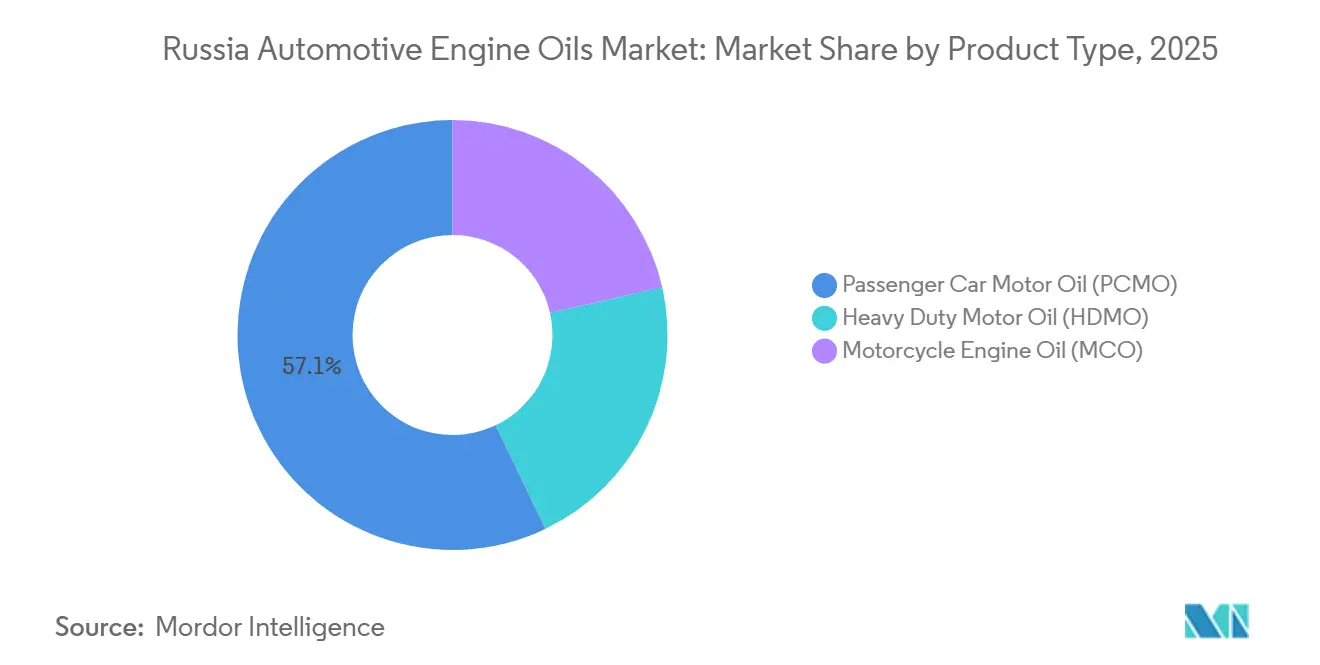

- By product type, passenger car motor oil commanded 57.12% of the Russia automotive engine oils market share in 2025, while motorcycle engine oil is projected to record the fastest 0.24% CAGR through 2031.

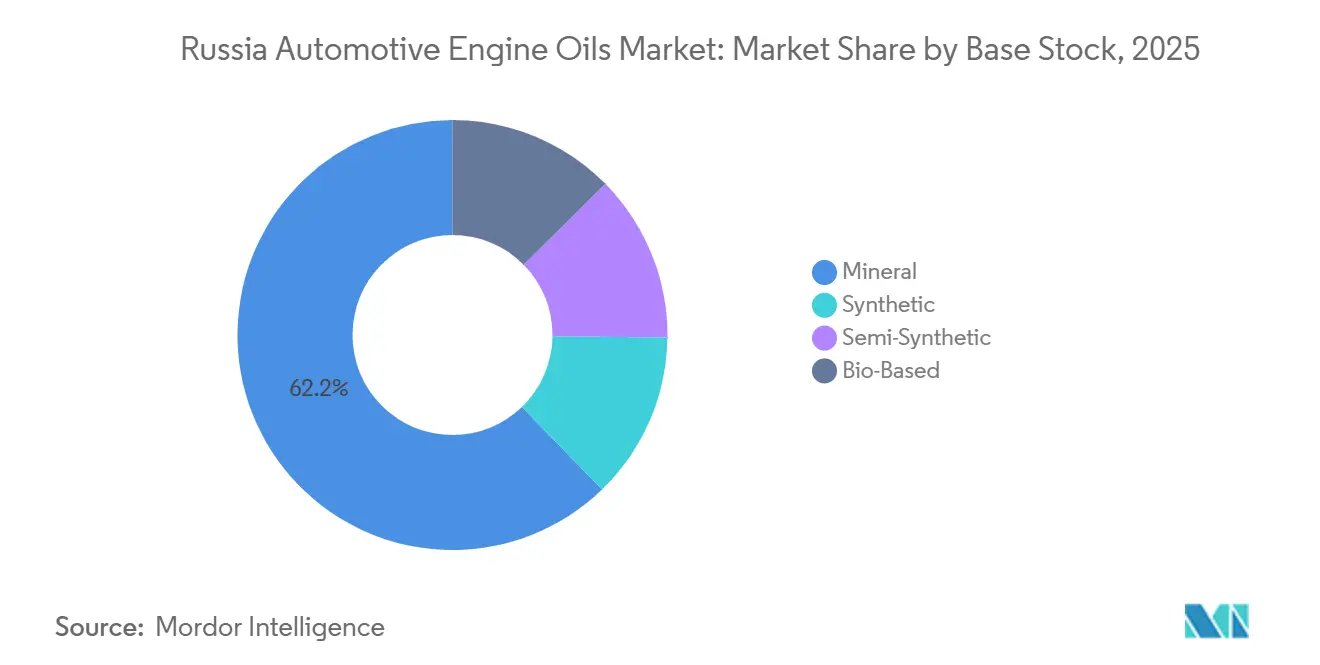

- By base stock, mineral oils captured 62.23% of the 2025 Russia automotive engine oils market size, whereas synthetic oils are forecast to expand at a 0.35% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Russia Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet-mileage rebound amid aging parc | +0.04% | Moscow, St. Petersburg, Far East | Medium term (2-4 years) |

| Accelerating shift to synthetic and low-viscosity oils | +0.03% | National; early uptake in cold-climate Far East | Medium term (2-4 years) |

| Import-substitution and localization of blending capacity | +0.02% | Omsk, Volgograd, Nizhnekamsk, Kaluga | Short term (≤ 2 years) |

| Expansion of e-commerce lubricant channels | +0.01% | Tier-1 cities | Long term (≥ 4 years) |

| Mandatory digital product-marking regime | +0.01% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fleet-Mileage Rebound Amid Aging Parc

The average age of the Russian vehicle fleet rose in 2025 because owners delayed replacement after Western OEMs withdrew. Older engines consume more oil due to worn components, so every extra kilometer traveled increases lubricant replacement frequency. Passenger-car travel recovered to pre-pandemic levels in 2025 according to national highway-toll statistics, amplifying oil sales in the aftermarket. Light-commercial vans that service e-commerce and grocery delivery are also clocking higher mileage, reinforcing baseline demand. This driver provides a modest but steady uplift that offsets volume lost from the slump in new-car sales.

Accelerating Shift to Synthetic and Low-Viscosity Oils

Gazpromneft-Lubricants restarted the Omsk GIDP hydro-isomerization complex in 2024, tripling synthetic base-oil output and removing a critical import bottleneck[1]Gazpromneft-Lubricants, “Company Overview and Production Capabilities,” gazpromneft-lubricants.ru. Domestic Group III supply cuts freight costs and shields buyers from currency volatility, so fleets in Siberia and the Far East are migrating from 10W-40 mineral grades to 0W and 5W synthetics that improve cold-start protection. Lukoil and Rosneft quickly followed with formulation upgrades that align with Euro 5 emission norms still applied to domestic fuels. Although synthetics remain a premium purchase, higher drain intervals and fuel-economy gains make the total-cost-of-ownership argument compelling for taxis, ride-hailing fleets, and corporate car-sharing operators.

Import-Substitution and Localization of Blending Capacity

Rosneft operates around six lubricant plants, while Lukoil runs nine facilities that cover Group I to Group III production. These refiners gained market share as foreign majors exited in 2022, leaving volumes and blending lines idle. Gazpromneft achieved “technological sovereignty” in October 2025 by launching Russia’s first in-country synthetic sulfonate additive production, enabling 100% domestic content in premium oils. Localization cushions the Russia automotive engine oils market from sanctions risk and currency swings, while also fulfilling state import-substitution mandates that give priority in public tenders.

Expansion of E-Commerce Lubricant Channels

Online sales accounted for a single-digit share of lubricant retail volume in 2025 but are rising fast on the back of nationwide courier networks. Major platforms now bundle next-day delivery with used-oil collection, appealing to do-it-yourself consumers in Moscow and St. Petersburg. Gazpromneft’s 2025 partnership with ROLF integrates click-and-collect ordering into its G-Energy Service centers, where customers book oil changes online and arrive at pre-staged bays. The forthcoming digital marking regime will generate real-time inventory data that e-commerce operators can mine to optimize regional stock, widening the price gap with brick-and-mortar outlets.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM exits shrink new-vehicle production base | -0.03% | Kaliningrad, Kaluga, Togliatti | Short term (≤ 2 years) |

| Gradual electrification dampening long-term demand | -0.01% | Moscow, St. Petersburg | Long term (≥ 4 years) |

| Expiry of foreign quality certificates | -0.02% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

OEM Exits Shrink New-Vehicle Production Base

AvtoVAZ output fell in 2025 after global brands withdrew capital and parts support, and most foreign assembly plants in Kaluga and Kaliningrad remain mothballed. New-car sales consequently collapsed, reducing factory-fill lubricant volumes and aftermarket upgrades linked to warranty compliance. Chinese marques now dominate imports, yet their smaller displacement engines hold less oil and specify longer drain intervals, trimming per-unit fluid demand. Regional economies that depended on vehicle assembly have also lost freight movements, squeezing heavy-duty oil consumption tied to component logistics.

Gradual Electrification Dampening Long-Term Demand

In 2025, Russia had a limited number of battery-electric passenger cars on its roads. However, with the influx of affordable Chinese SUVs through Far Eastern ports, this number is set to grow rapidly. Each electric vehicle's operation reduces engine oil consumption. The procurement of electric buses by municipalities in Moscow and St. Petersburg is poised to amplify this trend, especially concerning commercial-vehicle lubricant volumes in the 2030s. While the immediate impact on Russia's automotive engine oils market remains minimal, major refiners' strategic planners are already forecasting a potential decline in volume should EV penetration increase significantly by 2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominates While MCO Gathers Speed

Passenger car motor oil generated 57.12% of the 2025 Russia automotive engine oils market size as the aging light-duty fleet continues to rely on routine oil changes for reliability. Volume growth remains muted, yet price-mix is improving because older engines increasingly accept 5W-30 synthetics when mineral stockouts occur. Heavy-duty motor oil sales track freight traffic; refrigerated and long-haul operators prioritize drain-interval extension to cut downtime, favoring semi-synthetic formulations blended by Rosneft.

Motorcycle engine oil is small in absolute liters but will post the quickest 0.24% CAGR to 2031. Two-wheeler registrations hit a record in 2024 as Chinese brands such as Regulmoto and Racer filled the vacuum left by European and Japanese exits[2]Iz.ru, “Motorcycle Sales in Russia Set a New Record in 2024,” iz.ru. Entry-level bikes use single-cylinder engines that shear oil rapidly, so annual drain frequency is high. Urban riders in Moscow prefer branded semi-synthetics, whereas provincial users stay with low-priced mineral MCOs. The combined effect leaves total liters small yet strategically important for brand diversification.

By Base Stock: Mineral Still Leads, Synthetic Expands

Mineral oils accounted for 62.23% of Russia's automotive engine oils market share in 2025 because many engines designed before 2010 still specify Group I formulations. However, synthetic products will advance at a 0.35% CAGR to 2031 thanks to Gazpromneft’s Group III stream that underpins competitively priced 0W-20 and 5W-30 grades. Semi-synthetics remain the bridge option for vehicles 8-12 years old as owners seek better cold-crank performance without the full cost of PAO-based fluids.

TAIF-SM’s Nizhnekamsk facility uniquely produces domestic Group IV PAO ranging from PAO-2 to PAO-1000, offering pour points down to -60 °C and enabling niche products for Arctic service fleets. Price sensitivity still caps broad adoption, yet corporate fleets with telematics-monitored fuel-economy targets are shifting procurement toward synthetics. Rising excise taxes on high-viscosity mineral oils also tilt the cost equation and nudge distributors to stock more 5W-30 synthetic SKUs.

Geography Analysis

Across the vast expanse of Russia, the automotive engine oils market showcases pronounced regional disparities, influenced by both climate and economic conditions. In Moscow and St. Petersburg, a high vehicle density combined with a consumer inclination towards premium synthetics results in these cities generating a significant portion of the market's value. For instance, taxi fleets in Moscow, opting for 5W-30 synthetic blends and changing oil regularly, ensure a consistent demand for quick-service chains run by industry giants Gazpromneft and Lukoil.

In the Far East, where winter temperatures plunge below –40 °C, the necessity for 0W-XX viscosity grades becomes evident. Gazpromneft, capitalizing on this demand, dispatches finished lubricants from its Omsk refinery. These are transported by rail to depots in Vladivostok and Magadan, where local dosing of cold-flow improvers takes place. Meanwhile, in the southern agricultural centers of Krasnodar and Rostov, the summer heat and dusty conditions lead to a preference for thicker 10W-40 mineral oils in tractors and harvesters. Rosneft, recognizing this demand, utilizes its Volgograd refinery's proximity to these markets, often bundling bulk oil deliveries with diesel-fuel contracts.

Industrial cities like Kaluga, Kaliningrad, and Togliatti, once bustling with foreign OEM assembly, now grapple with dwindling lubricant demand. The shutdown of local plants has curtailed both commuter traffic and supply-chain trucking. On the other hand, clusters in Siberian mining and Ural steel continue to drive a robust demand for heavy-duty motor oils. Starting September 2025, a nationwide digital marking regime aims to close regional loopholes that have historically allowed counterfeit oils to infiltrate border areas, paving the way for a more unified brand portfolio across Russia.

Competitive Landscape

The Russian Automotive Engine Oils Market is moderately fragmented. Vertically integrated energy majors now set the tone in the Russia automotive engine oils market. These companies own the bulk of base-oil refining, blending, additive production, and retail forecourts, giving them unrivaled supply-chain control. Second-tier domestic producers carve niches in premium PAO-based synthetics and private-label mineral oils, respectively. Parallel imports of Shell and Castrol brands continue but are gradually squeezed by traceability rules and tighter customs inspection.

Russia Automotive Engine Oils Industry Leaders

Shell Plc

BP plc

Exxon Mobil Corporation

Gazpromneft-Lubricants Ltd.

Lukoil

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Gazpromneft-Lubricants Ltd. began commercial production of synthetic sulfonate additives at its Omsk plant, enabling fully domestically sourced high-performance oils.

- June 2025: BP plc initiated the sale of its Castrol lubricants division, valued at up to USD 10 billion, as part of a broader divestment strategy that could reshape brand availability across Europe, including Russia.

Russia Automotive Engine Oils Market Report Scope

Automotive engine oil, a blend of base oils and additives, plays a crucial role in minimizing friction, heat, and wear among the moving parts of an internal combustion engine. Beyond lubrication, it cleans, cools, and shields engine components from sludge, corrosion, and harmful deposits.

The Russia automotive engine oils market is segmented by product type and base stock. By product type, the market is segmented into passenger car motor oil (PCMO), heavy-duty motor oil (HDMO), and motorcycle engine oil (MCO). By base stock, the market is segmented into mineral, synthetic, semi-synthetic, and bio-based. For each segment, the market sizing and forecasts have been done based on revenue (Litres).

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

What is the volume outlook for the Russia automotive engine oils market?

The market is forecast at 484.62 million litres in 2026 and is forecast to reach 487.05 million litres, registering a CAGR of 0.10%.

Why are synthetic oils gaining share in Russia?

Domestic Group III and PAO capacity from Gazpromneft and TAIF-SM reduces import reliance and narrows the price premium, prompting fleet buyers to switch for better cold-start and fuel-saving benefits.

How will electric vehicles affect lubricant demand?

EV penetration is still low, but each additional EV removes annual engine oil demand.

Which product segment is growing the fastest?

Motorcycle engine oil is projected to grow at a 0.24% CAGR to 2031, thanks to record two-wheeler sales led by Chinese brands.

What regulation could reshape market competition?

The digital product-marking system that becomes mandatory nationwide in September 2025 will raise entry barriers for small blenders and curb counterfeit sales.

Which companies dominate the supply chain?

Gazpromneft-Lubricants, Lukoil, and Rosneft together control most Russian base-oil refining, blending, and branded retail distribution.

Page last updated on: