Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

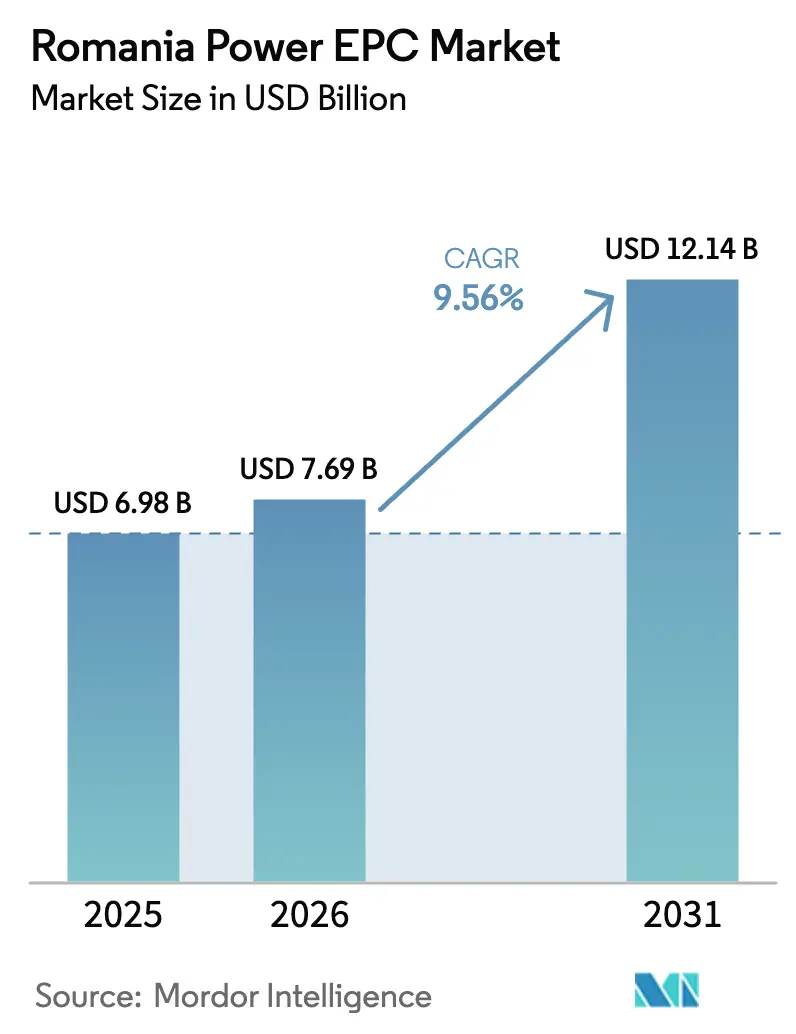

| Base Year Market Size (2025) | USD 6.98 Billion |

| Market Size (2026) | USD 7.69 Billion |

| Market Size (2031) | USD 12.14 Billion |

| Growth Rate (2026 - 2031) | 9.56% CAGR |

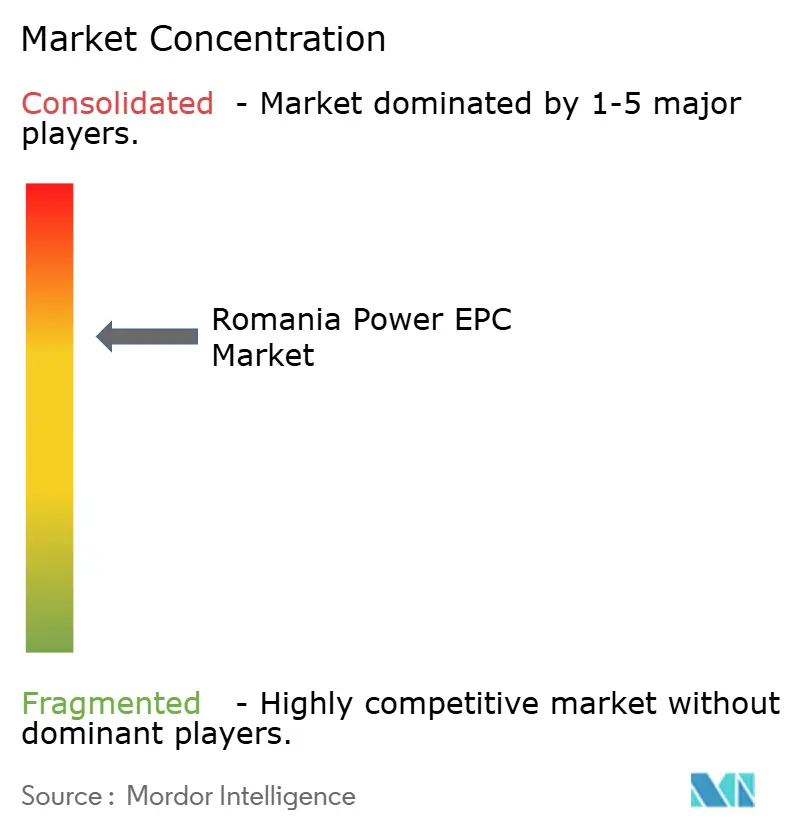

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Romania Power EPC Market Analysis by Mordor Intelligence

The Romania Power EPC Market size was valued at USD 6.98 billion in 2025 and is estimated to grow from USD 7.69 billion in 2026 to reach USD 12.14 billion by 2031, at a CAGR of 9.56% during the forecast period (2026-2031).

The up-cycle is propelled by a 4.2 GW Contracts for Difference (CfD) pipeline, accelerated coal-unit retirements, and grid-modernization programs jointly financed by the European Union and multilateral lenders. Investment momentum is reinforced by offshore-wind licensing, residential rooftop solar subsidies, and a liberalized bilateral-trading regime that unlocks corporate power-purchase agreements (PPAs). Competition is intensifying as Greek, Austrian, and German EPC majors vie with state-owned incumbents for turnkey contracts, while local integrators exploit distributed-generation niches. Financing conditions continue to ease, sub-5% project debt is now standard for CfD-backed renewables, supporting cash-flow visibility and expanding addressable capacity across wind, solar, gas, and storage.

Key Report Takeaways

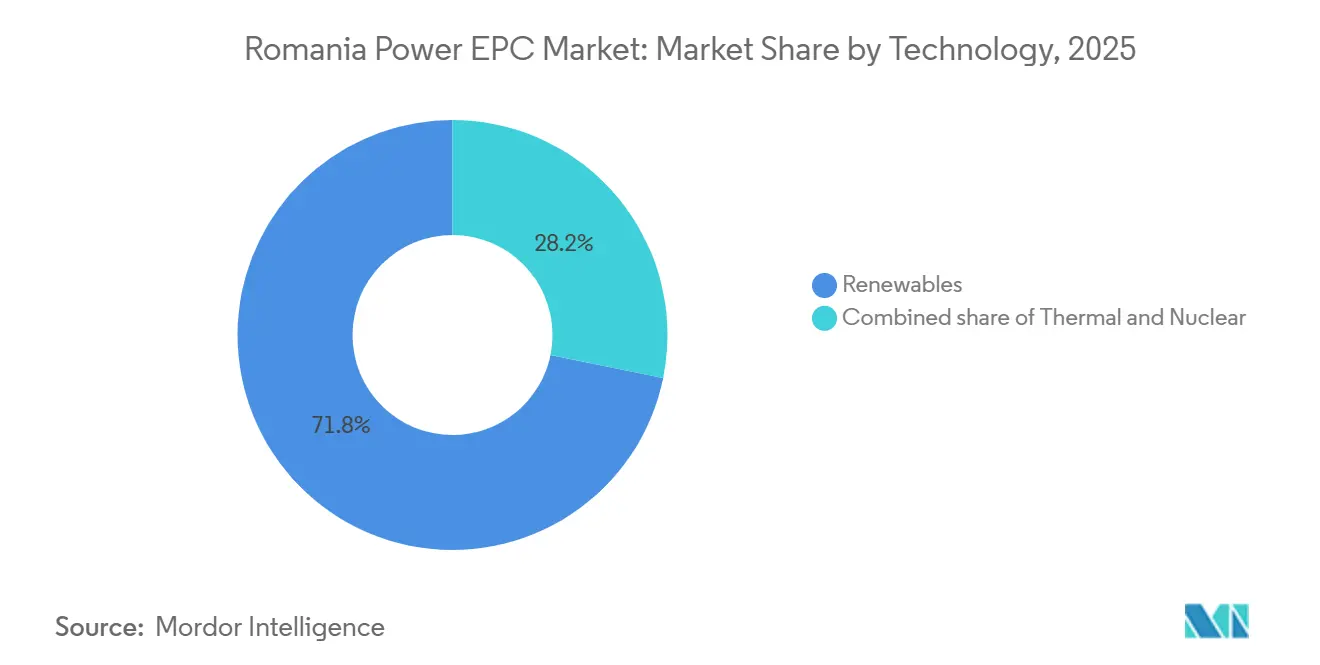

- Romania's power EPC market is segmented into power generation EPC and power transmission and distribution (T&D) EPC. Power generation EPC captured 64.6% revenue share in 2025, and the same is projected to grow at 10.15% CAGR through 2031.

- By technology, renewables led with 71.8% share of the Romania power generation EPC market in 2025 and are advancing at a 10.7% CAGR through 2031.

- By capacity band, the 100–499 MW tier held 65.1% share in 2025; the sub-100 MW distributed-energy segment is forecast to expand at a 12.1% CAGR through 2031.

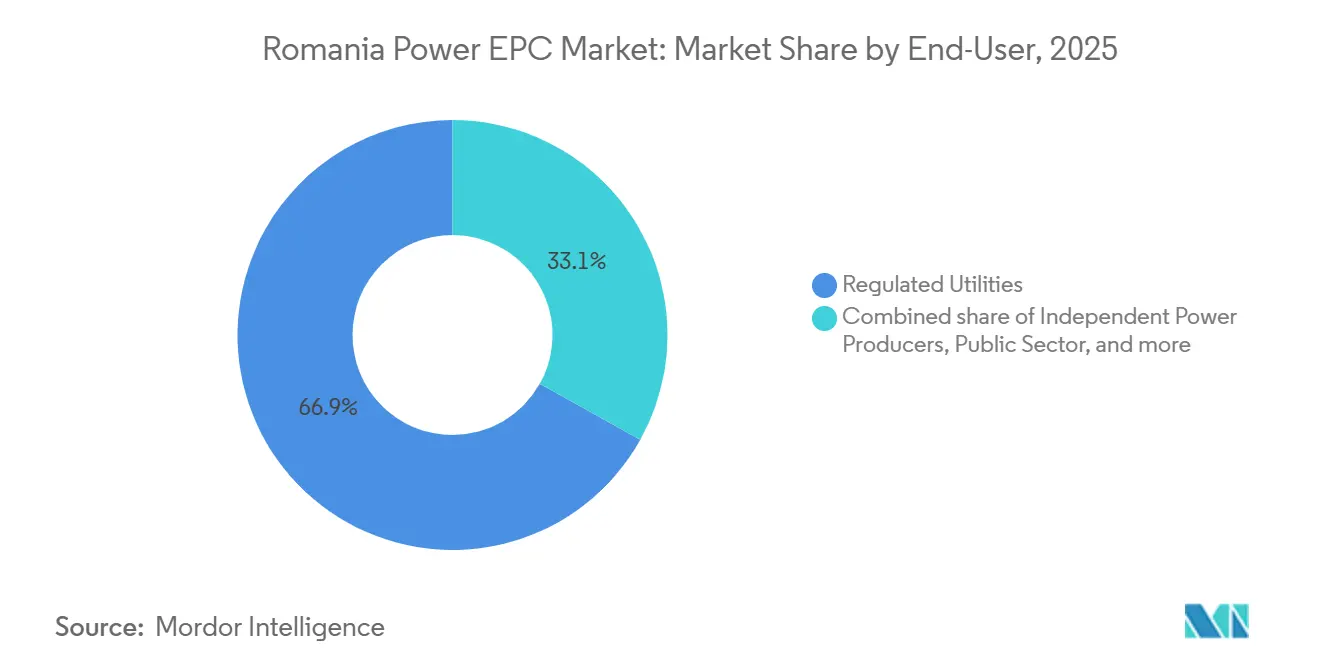

- By end-user, regulated utilities accounted for 66.9% of Romania's power generation EPC market share in 2025, while independent power producers (IPPs) recorded the highest projected CAGR at 11.3% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Romania Power EPC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-backed 5 GW CfD scheme for on-shore wind & solar | +2.8% | National, concentrated in Dobrogea, Banat, and Oltenia regions | Medium term (2-4 years) |

| Modernisation-Fund-financed grid digitalisation wave | +1.5% | National, with priority corridors in Transylvania and Muntenia | Long term (≥4 years) |

| Accelerated coal phase-out driving replacement CAPEX | +2.1% | Oltenia and Hunedoara coal basins; replacement capacity dispersed nationally | Medium term (2-4 years) |

| Building-renovation program bundling rooftop PV + HVAC EPC | +0.9% | Urban centers (Bucharest, Cluj-Napoca, Timișoara, Iași) and peri-urban municipalities | Long term (≥4 years) |

| Offshore-wind framework unlocking Black Sea pilot farms | +1.2% | Constanța maritime zone, with onshore grid reinforcement in Dobrogea | Long term (≥4 years) |

| Corporate PPAs rising after bilateral-trading reform | +0.7% | Industrial clusters in Prahova, Argeș, Dolj, and Timiș counties | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

EU-Backed 5 GW CfD Scheme Accelerates Renewable Deployment

Romania’s CfD mechanism, capitalized with EUR 3 billion from the EU Modernisation Fund, awarded 4.2 GW across 2024-2025 auctions, surpassing the original 3.5 GW target. Strike prices slid to EUR 35/MWh for solar, underscoring module-cost deflation and lower risk premiums. The 15-year revenue floor enables IPPs to secure project finance below 5%, compressing levelized costs and sharpening competitiveness against regulated utilities. Early movers such as Rezolv Energy and Low Carbon financed the 192 MW Vifor wind farm on these terms, achieving commercial operation by the end of 2025. From January 2026, grid-connection slots above 5 MW are auctioned with financial guarantees, filtering speculative bids and prioritizing shovel-ready assets.[1]National Energy Regulatory Authority, “Grid Connection Auction Guidelines,” anre.ro

Modernisation-Fund-Financed Grid Digitalisation Unlocks Hosting Capacity

Transelectrica’s 2024-2033 plan allocates EUR 56.2 million to deploy solar-and-storage systems at 29 substations, replacing diesel sets and enabling black-start capability.[2]Transelectrica, “Ten-Year Network Development Plan 2024-2033,” transelectrica.ro Complementary distribution upgrades include a EUR 100 million EBRD loan to PPC-owned Rețele Electrice for 500,000 smart meters and a EUR 200 million EIB facility to Electrica Group’s DEER for SCADA rollouts, trimming technical losses below 8%. Four new 400 kV corridors will evacuate offshore wind and integrate CfD-awarded solar, relieving curtailment that currently reaches 12% in Dobrogea. Government targets call for 2 GW of battery storage by 2026, providing frequency services and deferring USD 300 million of transmission CAPEX.

Accelerated Coal Phase-Out Drives Replacement CAPEX Wave

Romania aims to retire 2.25 GW of coal by 2032; interim derogations extend key units to 2029 for grid security. CE Oltenia’s pivot mixes 1,325 MW of gas and 690 MW of solar, although scheduling slippage has shifted gas completions to 2028. Gas backfill also includes Romgaz’s 430 MW Iernut CCGT, featuring 56% efficiency and carbon-capture readiness. Private developers are layering renewables and storage onto legacy coal sites, leveraging extant grid ties while absorbing displaced labor. Coal-reserve refurbishments, exemplified by Rovinari Unit 5’s EUR 100 million overhaul, underscore the urgency for dispatchable gas and storage as renewable penetration deepens.

Building-Renovation Program Bundles Rooftop PV and HVAC EPC

The Casa Verde Fotovoltaica scheme disbursed RON 3 billion to 87,500 households, covering up to 90% of rooftop-solar costs, while REPowerEU added EUR 1.2 billion for 60,000 more systems. Integrating photovoltaics with HVAC upgrades steers procurement toward contractors with dual mechanical-electrical capabilities, prompting Simtel Team and Monsson Group to launch residential divisions. Municipal add-ons such as Bucharest’s RON 150 million battery-plus-solar program aim to co-finance 385 MW and enroll assets in demand-response markets. Vocational partnerships with Transelectrica and Electrica trained 2,400 installers in 2024, narrowing the 40% skilled-labor gap. Yet rural permitting delays of up to 12 months nudge households toward off-grid systems that bypass conventional EPC channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic grid-connection bottlenecks & curtailment risk | -1.4% | Dobrogea, Banat, and Oltenia renewable-rich zones | Medium term (2-4 years) |

| FDI screening ≥€2 m delaying foreign EPC awards | -0.8% | National, disproportionately affecting Chinese, Russian, and Middle Eastern investors | Short term (≤2 years) |

| Domestic skilled-labour shortage in high-voltage projects | -0.6% | National, acute in Transylvania and Muntenia transmission corridors | Long term (≥4 years) |

| Performance-guarantee escalation squeezing SME cash-flows | -0.5% |

National, concentrated among contractors with |

Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Bottlenecks and Curtailment Risk Compress Returns

Hosting capacity in Dobrogea is saturated, forcing curtailment of up to 12% of wind output and delaying approvals for the 2.75 GW CfD tranche by as long as 24 months. From 2026, 400 kV build-outs and a financial-guarantee-based queue attempt to triage projects, yet developer capital remains locked for up to 18 months. Battery storage offers a hedge: Nova Power & Gas commissioned a 200 MW/400 MWh standalone system in December 2025, capturing frequency revenues that offset curtailment. National storage targets of 2 GW by 2026 could defer USD 300 million in transmission upgrades, but medium-voltage connection studies in Brăila and Constanța still face 9-12-month backlogs.

FDI Screening Above EUR 2 Million Delays Foreign EPC Awards

Romania’s FDI filter subjects non-EU investors to a 45-day review, extendable to 90 days, delaying financial close by four-to-six months. Mytilineos experienced a four-month lag on a 2 GW project pipeline acquisition in 2024, pushing CODs into 2027. Chinese vendors JinkoSolar and Trina Solar now ship equipment-only packages below the threshold, ceding EPC margin to local firms. Policy debate to lift the cap to EUR 5 million lacks a definitive timetable, keeping deal pipelines vulnerable to administrative drag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Renewables Extend Lead as Grid Bottlenecks Ease

Renewables seized 71.8% of the Romania power generation EPC market in 2025 and are forecast to grow at a 10.7% CAGR through 2031, anchored by the 4.2 GW CfD pipeline. Wind remains dominant at 3 GW installed, but solar is closing fast as OMV Petrom’s Brazi complex adds 400 MW and CE Oltenia’s 690 MW portfolio advances toward 2026 COD. Offshore wind could inject 3-7 GW by 2035 under the new Black Sea framework, dwarfing legacy coal capacities and reshaping dispatch patterns. Gas-fired CCGTs such as Romgaz’s 430 MW Iernut plant provide mid-merit flexibility, while nuclear stays a 1.4 GW baseload anchor through the EUR 1.9 billion Cernavoda Unit 1 overhaul. The Romania power EPC industry is therefore pivoting toward integrated renewable-and-storage portfolios that minimize curtailment and monetize ancillary services.

By Capacity Band: Distributed Energy Surges on Corporate Demand

The 100 to 499 MW tier held 65.1% share in 2025, reflecting utility-scale wind and solar parks tied to CfD awards.[3]Vestas, “Rezolv Energy Vifor Project Press Release,” vestas.com Yet sub-100 MW assets are rising at a 12.1% CAGR as industrials deploy captive solar to lock in sub-EUR 40/MWh tariffs; Automobile Dacia’s 36 MW array at Mioveni exemplifies this trend.[4]Renault Group, “Dacia Mioveni Solar Park Commissioning,” renaultgroup.com Hybrid projects co-locating 50 MW wind, 35 MW solar, and 24 MWh batteries highlight evolving design norms aimed at arbitraging day-ahead and balancing markets. Above-500 MW capacity will re-emerge once Black Sea offshore wind enters execution, inserting high-voltage direct-current links into the Romania power generation EPC market roadmap.

By End-User: IPPs Gain Ground Amid PPA Boom

Regulated utilities commanded 66.9% of Romania's power generation EPC market size in 2025, led by Transelectrica, Hidroelectrica, and Nuclearelectrica. IPPs, however, are expanding at 11.3% CAGR, leveraging CfD cash-flow visibility and corporate PPAs to finance pipelines above 3.4 GW. Industrial off-takers embrace self-generation and virtual PPAs, prompting utilities to invest in grid services and reserve margins rather than pure generation.

Geography Analysis

Dobrogea, Banat, and Oltenia dominate project allocation, absorbing most of the 4.2 GW CfD awards because of superior wind and solar resources. Dobrogea already hosts 3 GW of onshore wind and is earmarked for 4.9 GW of offshore capacity; the Constanța Nord–Medgidia Sud 400 kV upgrade, due 2029, will curtail losses now hitting 12%. Oltenia pivots from coal to gas and solar, with CE Oltenia’s 690 MW PV portfolio and Romgaz’s 430 MW Iernut CCGT slated for 2026-2028 completion. Banat and Transylvania are magnets for industrial captive power; OMV Petrom’s Brazi hub in Prahova feeds automobile and petrochemical clusters.

Urban centers, Bucharest, Cluj-Napoca, Timișoara, and Iași, benefit from rooftop solar subsidies and municipal battery schemes that defer distribution upgrades. Muntenia and Moldova lead in smart-meter density as PPC-owned Rețele Electrice deploys 1.7 million meters, while DEER hardens medium-voltage lines across 42 counties with EIB backing. The Black Sea offshore zone promises long-run job creation, port revitalization, and turbine manufacturing, contingent on timely HVDC rollouts and supply-chain localization.

Despite these opportunities, medium-voltage connection studies in Brăila, Constanța, and Tulcea face 9-12-month backlogs, squeezing developer returns and deterring smaller IPPs. Government storage incentives aim to smooth load profiles and postpone expensive transmission expansion, yet administrative friction persists in rural distribution queues.

Competitive Landscape

The Romania power EPC market shows moderate concentration: state-owned Transelectrica, Hidroelectrica, Nuclearelectrica, and CE Oltenia account for roughly 40% of CAPEX via captive procurement. European majors Enel, Siemens, ABB, and Schneider Electric command about 25% through technology supply and turnkey services, while Greek entrants Mytilineos and PPC Renewables, and local integrators Simtel Team and Monsson Group split most of the balance. State firms focus on refurbishment, Hidroelectrica’s EUR 188 million Vidraru upgrade, and Nuclearelectrica’s EUR 1.9 billion Cernavoda overhaul, whereas IPPs chase greenfield renewables funded by CfDs and PPAs.

Large-scale storage signals a white-space opportunity; Nova Power & Gas’s 200 MW/400 MWh system in Cluj sets a domestic benchmark. Offshore wind, led by Bluebridge Energy, Parkwind, and Ocean Winds, remains unconsolidated, providing entry for specialized marine EPC contractors. Bond-requirement hikes to 10-15% accelerate consolidation, favoring firms with robust balance sheets. Chinese module suppliers pivot to equipment-only contracts to bypass FDI filters, ceding EPC margin to local firms yet retaining module share via competitive pricing.

Technology differentiation is sharpening: Siemens and GE Vernova vie for gas-turbine orders that replace coal, while ABB and Schneider Electric deploy grid-automation suites aligned with Transelectrica’s digitalization drive. Nuclearelectrica’s merger with SNN introduces North American EPC standards, potentially disrupting established European nuclear contractors.

Romania Power EPC Industry Leaders

-

Transelectrica SA

-

Electrica SA (DEER & Sunwind)

-

Mytilineos SA

-

Hidroelectrica SA

-

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Nuclearelectrica inked a financing deal worth EUR 540 million (USD 634 million) with a banking consortium spearheaded by JP Morgan. The funds are earmarked for the refurbishment of Cernavoda Unit 1. Additionally, Nuclearelectrica secured an EUR 80 million loan to advance the Cernavoda units 3 and 4 project.

- October 2025: Israeli firm Econergy, which boasts the title of owning Romania's largest photovoltaic park, tapped Shanghai Electric to serve as the engineering, procurement, and construction contractor. This new facility will feature double the capacity of its predecessor, alongside a robust 150 MW battery energy storage system.

- June 2025: In southwestern Romania, Ameresco SUNEL Energy, a collaboration of Ameresco and SUNEL Group, clinched EPC contracts totaling EUR 303.4 million for three solar parks. The 466MWp projects, dubbed Rovinari, Tismana 1, and Tismana 2, are under the joint development of OMV Petrom and CE Oltenia, each holding a 50% stake.

- June 2024: First Look Solutions, a subsidiary of Rezolv Energy and Low Carbon, has ordered a 192 MW EPC solution from Vestas for the Vifor project in south-eastern Romania. The order includes 30 V162-6.2 MW EnVentus turbines operating in a 6.4 MW mode.

Romania Power EPC Market Report Scope

Power Engineering, Procurement, and Construction (EPC) refers to a comprehensive approach in the energy sector. It involves designing, engineering, procuring, and constructing power plants, including conventional and renewable energy projects. The EPC model is commonly employed for large-scale energy infrastructure projects, such as thermal power plants, hydroelectric plants, wind farms, solar farms, and transmission and distribution networks.

The Romanian Power Engineering, Procurement & Construction (EPC) market is segmented by power generation EPC, power T&D EPC, and geography. By technology, the market is segmented into thermal, nuclear, and renewables. By capacity band, the market is segmented into up to 100 MW, 100-499 MW, and above 500 MW. By end-user, the market is segmented into regulated utilities, IPPs, industrial captive, and the public sector. The market sizing and forecasts for each segment are based on revenue.

Power Generation EPC

| By Technology | Thermal |

| Nuclear | |

| Renewables | |

| By Capacity Band | Up to 100 MW (DER, micro-grid) |

| 100 to 499 MW | |

| Above 500 MW | |

| By End-User | Regulated Utilities |

| Independent Power Producers | |

| Industrial Captive Power | |

| Public Sector and SOE |

| Power Generation EPC | By Technology | Thermal |

| Nuclear | ||

| Renewables | ||

| By Capacity Band | Up to 100 MW (DER, micro-grid) | |

| 100 to 499 MW | ||

| Above 500 MW | ||

| By End-User | Regulated Utilities | |

| Independent Power Producers | ||

| Industrial Captive Power | ||

| Public Sector and SOE | ||

Key Questions Answered in the Report

How large is Romania's power EPC opportunity today and what is its growth pace through 2031?

Total EPC spending reached USD 7.69 billion in 2026 and is projected to climb to USD 12.14 billion by 2031, equal to a 9.56% compound annual growth rate.

Which project-types capture the majority of current engineering, procurement, and construction spending?

Power-generation work accounts for 64.6% of 2025 activity, led by renewables that already hold 71.8% share and are expanding at a 10.7% CAGR.

How is the Contracts for Difference scheme reshaping investment decisions?

The EU-backed CfD program has awarded 4.2 GW of capacity across two auctions with 15-year revenue guarantees; the visibility allows developers to raise sub-5% project debt and bid solar as low as EUR 35/MWh, accelerating project pipelines to 2028.

What role will battery storage play over the next five years?

Government targets call for 2 GW of storage operating by end-2026, highlighted by Nova Power & Gas's 200 MW/400 MWh system commissioned in 2025; storage earns frequency-regulation revenue, mitigates curtailment, and can defer roughly USD 300 million in grid upgrades.

How significant are coal-replacement and gas projects in maintaining grid stability?

Romania plans to retire 2.25 GW of coal by 2032; replacement includes 1,325 MW of gas-fired capacity from CE Oltenia and Romgaz's 430 MW Iernut CCGT, both designed for fast-ramp and black-start capability that complements intermittent renewables.

What administrative or financial hurdles could slow project execution?

Grid-connection studies can stretch 9-12 months in high-resource zones, foreign-investment reviews over EUR 2 million add up to 90 days, and banks now require 10-15% performance bonds, all of which raise working-capital needs and lengthen construction schedules.

Page last updated on: