Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

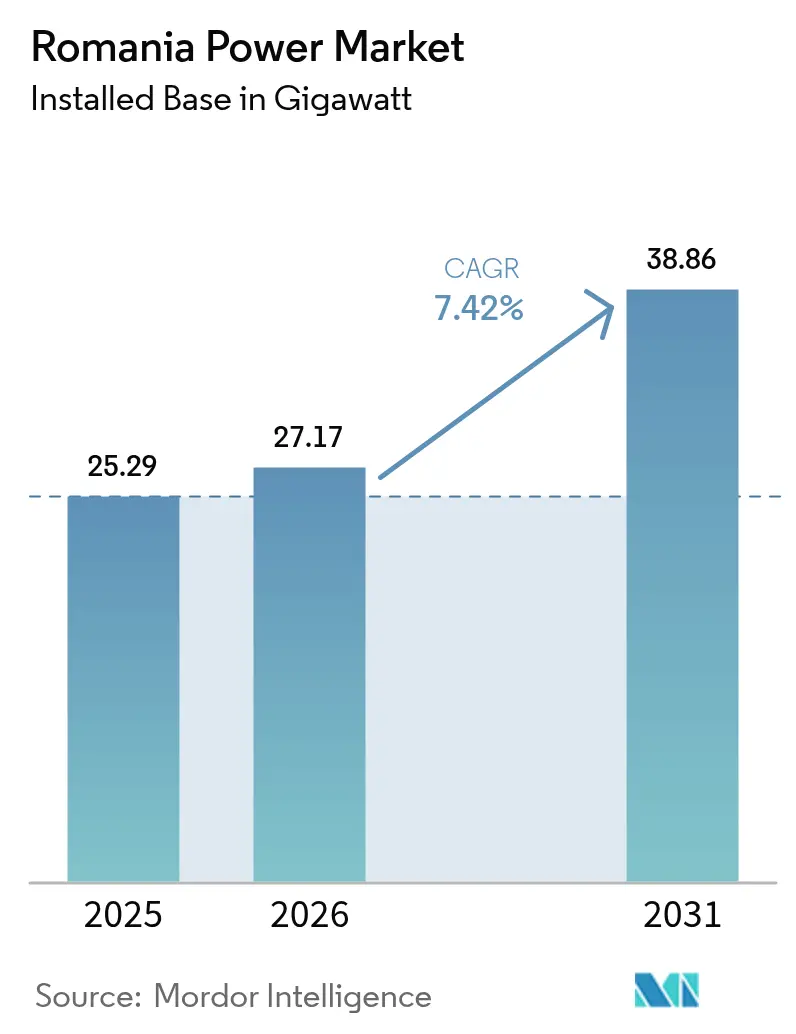

| Base Year Market Size (2025) | 25.29 gigawatt |

| Market Volume (2026) | 27.17 gigawatt |

| Market Volume (2031) | 38.86 gigawatt |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

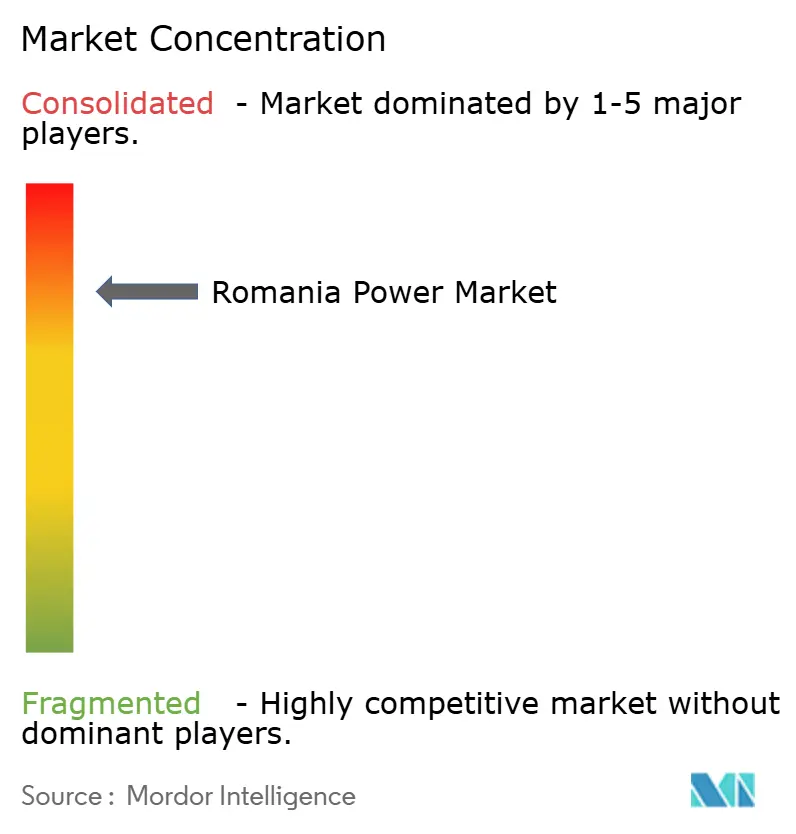

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Romania Power Market Analysis by Mordor Intelligence

The Romania Power Market size was valued at 25.29 gigawatt in 2025 and estimated to grow from 27.17 gigawatt in 2026 to reach 38.86 gigawatt by 2031, at a CAGR of 7.42% during the forecast period (2026-2031).

Current growth hinges on three structural shifts: steady retirement of coal assets, rapid solar and wind build-out enabled by the 2024 Contracts for Difference (CfD) scheme, and visible progress on grid-modernization projects supported by EU grants. Developers now face fewer regulatory hurdles after 2022 permitting reforms, while auction-indexed strike prices below wholesale averages have derisked merchant exposure and attracted broad international equity interest. Rising corporate demand for long-term renewable power-purchase agreements (PPAs) is amplifying investment in behind-the-meter solar-plus-storage, and fresh capital from the Hidroelectrica IPO and OMV Petrom’s renewables acquisitions is intensifying competition across asset classes. Simultaneously, the Black Sea offshore wind framework unlocks a large maritime resource that can diversify the generation mix, provided transmission upgrades arrive on schedule.

Key Report Takeaways

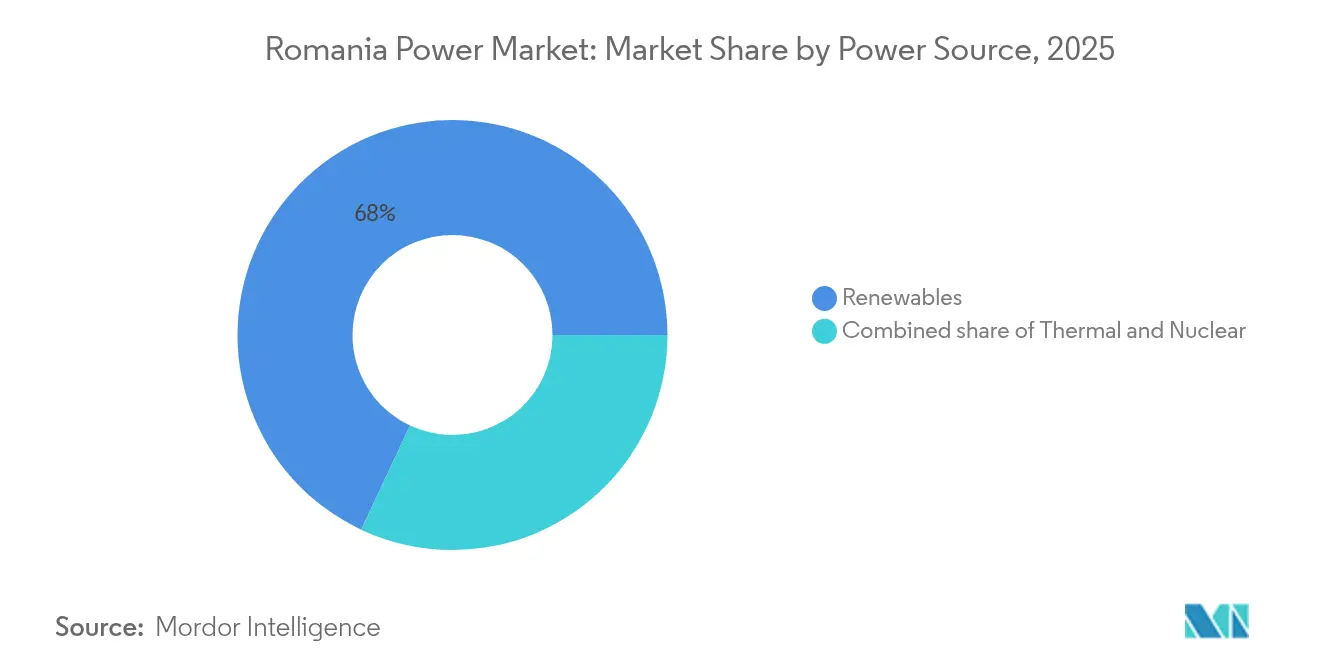

- By power source, renewables led with 68.02% of Romania's power market share in 2025, and the segment is forecast to grow at an 8.48% CAGR through 2031.

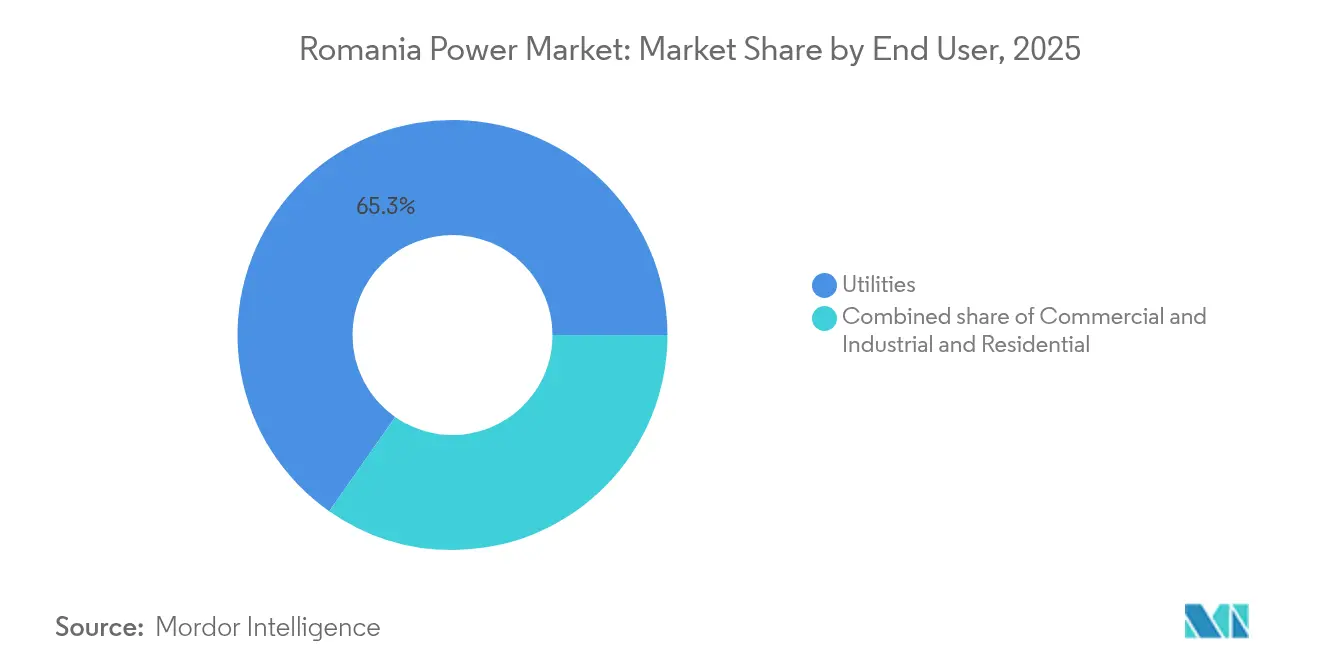

- By end user, utilities accounted for 65.28% of the market in 2025, while the commercial and industrial segment is projected to expand at a 8.98% CAGR to 2031, outpacing utilities and residential customers.

- Hidroelectrica, OMV Petrom, and Nuclearelectrica together controlled more than 55% of total installed capacity in 2024, highlighting the weight of state-influenced incumbents.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Romania Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Green Deal decarbonisation targets | +1.8% | National, strongest momentum in Dobrogea and Transylvania | Long term (≥ 4 years) |

| Rising corporate PPA demand from energy-intensive exporters | +1.2% | Prahova, Argeș, Timiș industrial corridors | Medium term (2-4 years) |

| EU-funded grid-modernisation grants | +1.0% | Priority high-voltage corridors and smart-meter zones | Medium term (2-4 years) |

| Newly-approved Black Sea offshore-wind framework | +1.5% | Coastal counties Constanța and Tulcea | Long term (≥ 4 years) |

| Smart-meter rollout enabling prosumers & VPPs | +0.7% | Major urban centers | Short term (≤ 2 years) |

| Cross-border interconnector upgrades | +0.5% | Border regions Banat and Oltenia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Green Deal Decarbonisation Targets Drive Capacity Additions

Romania’s pledge to supply 38% of electricity from renewables by 2030 has reoriented national planning toward wind, solar, and hydropower build-out. Approval of a EUR 3 billion CfD program in November 2024 allocated 5 GW at winning strike prices of EUR 65/MWh for wind and EUR 51/MWh for solar, well below the 2024 day-ahead wholesale average.[1]European Commission, “State Aid SA.109966 (2023/N)–Romania–Contracts for Difference Scheme,” europa.eu Utility-scale solar installations jumped by 2 GW in 2024 alone, illustrating how quickly projects move once grid links and land permits are secured. Wind growth lags due to longer environmental assessments, yet Dobrogea’s 7 m/s resource remains attractive for developers with seasoned local partners. The upcoming carbon border adjustment mechanism further encourages domestic manufacturers to switch to low-carbon electricity, reinforcing demand certainty for new plants.

Rising Corporate PPA Demand from Energy-Intensive Exporters

Romanian automotive, steel, and chemicals groups now favor multi-year PPAs to hedge OPCOM price swings and satisfy Scope 2 reporting under the Corporate Sustainability Reporting Directive. NextE’s 42.9 MW on-site solar deal signed in 2024 priced power near EUR 50/MWh, beating the prior year’s EUR 90–120/MWh wholesale range. This differential triggered fresh tenders in Timiș and Argeș and pushed local lenders to refine credit benchmarks for long-term offtakes. An EIB survey found 81% of firms rating energy costs a top competitiveness threat, with 57% spending on on-site efficiency upgrades and 90% on greenhouse-gas measures.[2]European Investment Bank, “EIB Investment Survey 2024–Romania Factsheet,” eib.org As the PPA ban lifted in 2022, bankable offtakes became feasible, transferring volume risk away from utilities and into bilateral contracts.

EU-Funded Grid-Modernisation Grants Unlock Transmission Capacity

Transelectrica received EUR 56.2 million in 2024 to pilot solar-plus-storage at 29 high-voltage substations, aiming to smooth renewable ramps and defer costly line upgrades.[3]Transelectrica, “RRF Pilot Projects,” transelectrica.ro The EBRD’s EUR 100 million loan to PPC’s distribution arm and Electrica’s EUR 171 million smart-meter rollout anchors wider digitalization that improves load forecasting and voltage management. Romania’s vintage 1970s network lacks dynamic line rating, leading to midday solar curtailment in southern counties. Competitive auctions for scarce grid-connection capacity, proposed by ANRE in 2024, intend to prioritize projects offering firm capacity or co-located batteries. Without these upgrades, the 5 GW awarded under the CfD scheme risk commissioning delays and squeezed returns.

Newly-Approved Black Sea Offshore Wind Framework

Law 128/2024 opened Romania’s exclusive economic zone to 3–7 GW of offshore wind by 2035, giving developers access to capacity factors above 45% and avoiding much of the onshore permitting pushback.[4]World Bank, “Romania Offshore Wind Roadmap,” worldbank.org The BSOG consortium targets a 3 GW shallow-water array with the first turbines expected in 2027, while Verbund secured leases for adjacent sites. Absence of a pre-built offshore grid requires private financing of subsea cables, adding EUR 1–2 million/km and lengthening payback periods. A Germany-style centralized grid model could cut costs and accelerate schedules, but would need fresh legislation and public funding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX & permitting lead-times | -1.3% | Natura 2000 zones, archaeological clusters | Medium term (2-4 years) |

| Ageing grid causes renewable curtailment risk | -0.9% | Constanța, Tulcea, Dolj | Short term (≤ 2 years) |

| Wholesale price caps undermine PPA bankability | -0.6% | All merchant generators | Short term (≤ 2 years) |

| Biodiversity pushback against onshore wind repowering | -0.4% | Dobrogea plateau, Carpathian foothills | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX & Permitting Lead-Times

Utility-scale PV typically clears permits within three years, yet wind projects average 6.5 years because multi-agency reviews include environment, heritage, and land-use approvals. Archaeological rules require digs within 500 m of ancient sites, impacting roughly 30% of planned Dobrogea wind locations. Developers also shoulder substation costs that can exceed EUR 50 million before grid access is guaranteed. ANRE’s proposal for capacity auctions adds further uncertainty, potentially pushing smaller independent power producers out of contention, given higher carrying costs.

Ageing Grid Causes Renewable Curtailment Risk

Legacy conductors lack phase-shifting transformers, so Transelectrica cuts renewable output during high-irradiance or high-wind intervals to preserve system frequency. Curtailment reached 150 GWh in 2024, equal to -1% of renewable production, and could double by 2027 without accelerated upgrades. Battery pilots at 29 substations help, yet nationwide reinforcement needs EUR 2–3 billion, well beyond the current EU grant envelope. Distribution feeders in rural solar clusters also breach voltage limits, requiring reactive-power devices that add unforeseen OPEX for utilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Renewables Dominate Amid Coal Phase-Out

Renewables contributed 68.02% of 2025 capacity, and their 8.48% growth pace keeps the Romania power market size expansion aligned with EU emission goals. Hydropower alone held a 33.12% share, courtesy of Hidroelectrica’s 6.5 GW fleet that supports peak shaving and frequency response. Wind capacity reached 3 GW, with 2.5 GW more awarded in the CfD auction at EUR 65/MWh, pricing that underlines a maturing cost curve. Solar jumped past 5.3 GW after 2 GW was connected in 2024, helped by modules priced below USD 0.18/W and fast-track permits for projects under 10 MW. The Black Sea offshore framework could add 3–7 GW by 2035, giving Romania a fresh nucleus for high-factor generation and bolstering energy-security margins. Gas-fired capacity rises modestly as flexible CCGTs linked to Neptun Deep output replace retiring coal. Nuclear remains vital; Cernavoda Units 1-2 generate one-fifth of supply, while Units 3-4 plus the 462 MW Doicești SMR will anchor firm, low-carbon baseload later in the decade.

The shift reshapes asset economics, as capacity-weighted average LCOE for new projects reaches EUR 48/MWh for solar and EUR 56/MWh for onshore wind, both below 2024 wholesale prices. Curtailment risk tempers enthusiasm in congestion-prone southern counties, yet co-located storage can secure higher balancing fees. Accordingly, project sponsors aggregate PV with 4-hour batteries sized at 25% of nameplate capacity to capture arbitrage spreads.

By End User: Industrial Offtakers Accelerate PPA Adoption

Utilities still owned 65.28% of capacity in 2025, but the 8.98% CAGR expected for commercial and industrial offtakers signals a decisive decentralization of the Romania power market. Automotive hubs in Timiș and Argeș host rooftop solar arrays coupled with lithium-ion batteries that flatten demand peaks and cut grid fees. NextE’s 42.9 MW PPA at EUR 50/MWh triggers competitive follow-ons, with multinationals demanding supply chain carbon cuts ahead of the 2026 carbon border adjustment. Lenders restrict PPAs to investment-grade buyers, limiting access for SMEs and concentrating deals among export-oriented corporates.

Residential prosumers already add meaningful volume: systems average 13 kW and feed surplus into distribution networks under yearly net-billing terms, raising the Romania power market size for distributed generation. Smart-meter deployment unlocks time-of-use rates and prospective VPP remuneration, though settlement backlogs frustrate early adopters. Utilities respond by proposing tariff structures that reward afternoon self-consumption to relieve network stress.

Geography Analysis

Dobrogea hosts the largest wind clusters and will likely anchor the first Romanian offshore projects, giving the region both onshore and maritime leverage over future renewable additions. Transmission corridors to Bucharest are mid-upgrade, and sustained curtailment risk remains until 2027 line reinforcements come online. Oltenia’s high irradiance propels solar greenfield activity, with over 40% of the 2 GW PV built in 2024 situated here. Retiring lignite assets in Turceni and Rovinari free up skilled labor and grid nodes ideally suited to solar-plus-storage retrofits.

Transylvania blends moderate wind and solar resources with strong industrial demand, making it fertile ground for corporate PPAs. Cross-border lines into Hungary and Serbia enable exporters to arbitrage spot spreads, improving project bankability. Banat benefits from the new 400 kV Serbia link, which trimmed redispatch costs for wind farms during winter 2024 congestion events.

Bucharest and Ilfov account for roughly one-fifth of national consumption. Lacking local generation, the capital relies on inland hydropower, Dobrogea wind, and imported baseload. Smart-meter rollouts improve peak-load visibility and support demand-response pilots that shave evening ramps. Ongoing synchronization work with Ukraine and Moldova positions Romania as a continental transit hub, enhancing merchant revenue options for generators grappling with domestic price caps.

Competitive Landscape

Romania's power market competition intensified after Hidroelectrica's EUR 1.3 billion IPO in July 2024, which funds a 1.4 GW wind-solar pipeline and signals a shift from hydro-only dominance toward integrated renewables. OMV Petrom's 50% stake in Electrocentrale Borzești added a 1 GW green portfolio, illustrating oil majors' rapid pivot into low-carbon assets. Independent power producers such as Tinmar and nextE differentiate by bundling storage and offering sub-EUR 60/MWh long-term corporate PPAs.

Technology now underpins strategic advantage: developers that integrate batteries or commit to synthetic inertia win grid-connection priority. Nuclearelectrica's EUR 20 billion roadmap includes two CANDU expansions and a Doicești SMR, promising 1.9 GW of zero-carbon baseload toward decade-end. Meanwhile, CEZ Romania expanded Europe's largest onshore wind complex to 733 MW, bolstering scale economies.

White-space exists in virtual power plants and offshore wind. Aggregators plan to pool 500 MW of distributed storage once ANRE finalizes VPP rules, while Verbund and BSOG advance Black Sea leases requiring capital-intensive subsea connections. Market incumbents, therefore, confront a dual challenge: defend retail margins as prosumers grow, and secure grid access ahead of capacity auctions that may penalize projects lacking firming capabilities.

Romania Power Industry Leaders

Hidroelectrica SA

OMV Petrom SA

Nuclearelectrica SA

PPC (PPC Renewables/ former Enel)

CEZ Romania

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Simtel Team commissioned a 52 MWp solar power plant in Giurgiu County. The facility boasts over 85,000 solar modules, all managed by 170 smart inverters. It's connected to the national grid through six transformer stations and a newly constructed high-voltage substation.

- November 2025: In a bid to bolster Romania's energy security, the European Bank for Reconstruction and Development (EBRD) has orchestrated a financing package worth EUR 192 million. This funding is earmarked for the establishment of three new solar power plants in south-eastern Romania, boasting a combined installed capacity of 531 MW.

- November 2025: In Romania, Greek utility PPC SA has successfully connected a 130-MW solar farm to the grid, marking a significant expansion of its renewable energy portfolio in the nation. Situated in Calugareni, just 40 km (24.9 miles) south of Bucharest, the plant boasts over 227,000 bifacial solar panels, projecting an annual production of approximately 193 GWh.

- October 2025: Greenvolt Power secured a deal with GE Vernova to supply, install, and commission 42 turbines, each boasting a capacity of 6MW and a height of 158m, for its Gurbanesti wind farm located in Calarasi county, Romania.

Romania Power Market Report Scope

Power is generated through various primary sources such as coal, hydro, solar, thermal, etc. In utilities, it's a step before its delivery to its end users. Then the process is followed by Transmission and distribution. Under this, the power generated is distributed via high-voltage lines (transmission lines) and low-voltage lines (distribution lines) as per the requirement of the end user.

The Romania power market report is segmented by power sources and end-user. By power sources, the market is segmented into thermal (Coal, Natural Gas, Oil, and Diesel), nuclear, renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal). By end-user, the market is segmented into utilities, commercial and industrial, and residential. The market sizing and forecasts have been done based on electricity generation capacity (GW).

By Power Source

| Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) |

By End User

| Utilities |

| Commercial and Industrial |

| Residential |

By T&D Voltage Level (Qualitative Analysis only)

| High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) |

| Medium-Voltage Distribution (13.2 to 34.5 kV) |

| Low-Voltage Distribution (Up to 1 kV) |

| By Power Source | Thermal (Coal, Natural Gas, Oil and Diesel) |

| Nuclear | |

| Renewables (Solar, Wind, Hydro, Geothermal, Biomass & Waste, Tidal) | |

| By End User | Utilities |

| Commercial and Industrial | |

| Residential | |

| By T&D Voltage Level (Qualitative Analysis only) | High-Voltage Transmission (Above 230 kV) |

| Sub-Transmission (69 to 161 kV) | |

| Medium-Voltage Distribution (13.2 to 34.5 kV) | |

| Low-Voltage Distribution (Up to 1 kV) |

Key Questions Answered in the Report

How large is the Romania power market in 2026?

The Romania power market size stands near 27.17 GW in 2026, on track with the 7.42% CAGR that points toward 38.86 GW by 2031.

How fast is renewable capacity growing in the Romania power market?

Renewable installations are forecast to rise at an 8.48% CAGR through 2031, lifting their share above 70% of total capacity.

What role do corporate PPAs play in new project financing?

Long-term PPAs priced near EUR 50/MWh give industrial buyers price certainty and supply certificates, anchoring financing for on-site and utility-scale solar projects.

Will offshore wind meaningfully diversify Romania's generation mix?

Yes, the Black Sea framework targets 3-7 GW by 2035, offering capacity factors above 45% and lowering reliance on onshore resources.

How are grid constraints being addressed?

EU-funded upgrades include 400 kV line reinforcements, substation-level batteries, and a 2.8 million smart-meter rollout to handle bi-directional flows.

Is nuclear power expanding in Romania?

Nuclearelectrica plans to add 1,448 MW at Cernavoda and a 462 MW SMR at Doicesti, securing carbon-free baseload for the early 2030s.

What is the outlook for coal plants?

All lignite units are slated for retirement by 2032, making room for gas-fired flexibility and accelerating renewable deployment.

Page last updated on: