Rolling Stock Market Size and Share

Market Overview

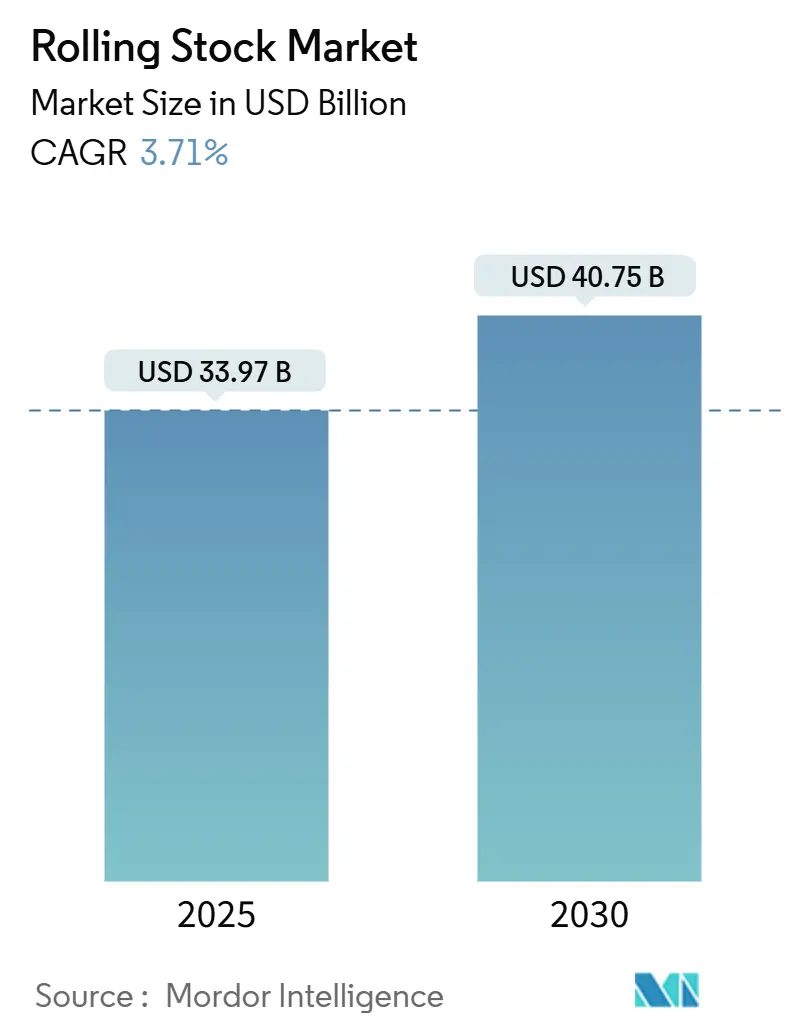

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 33.97 Billion |

| Market Size (2030) | USD 40.75 Billion |

| Growth Rate (2025 - 2030) | 3.71% CAGR |

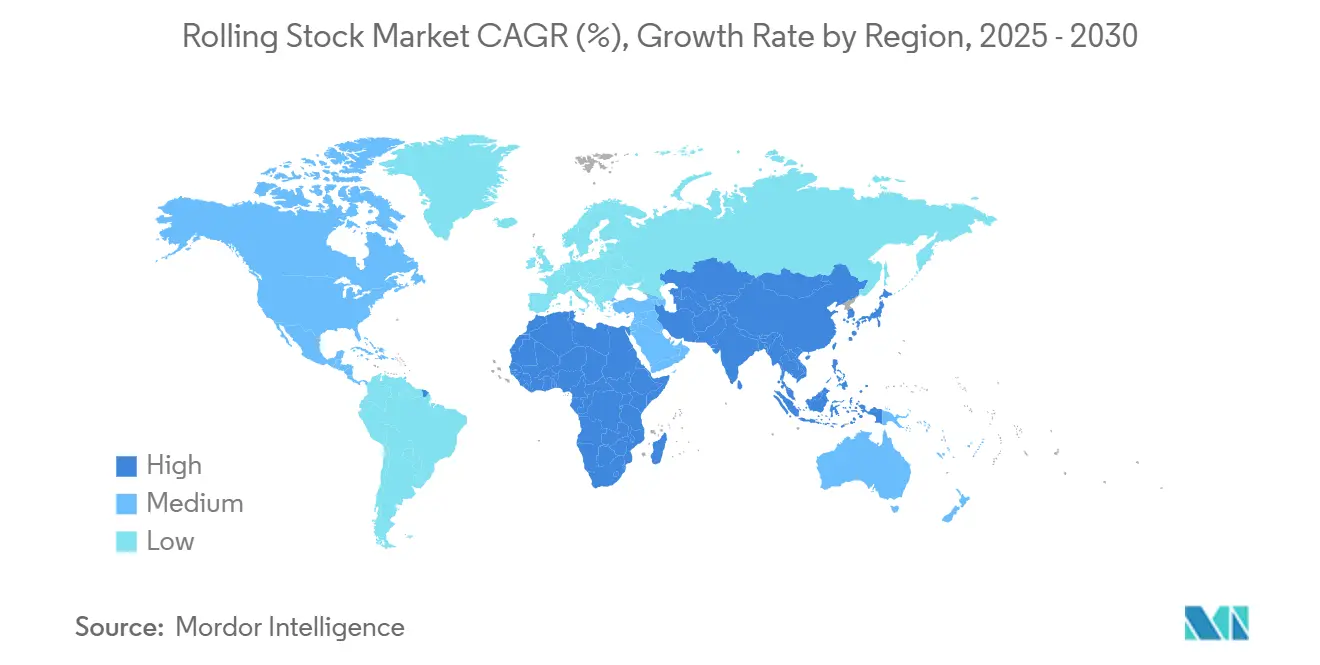

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Rolling Stock Market Analysis by Mordor Intelligence

The Rolling Stock Market size is estimated at USD 33.97 billion in 2025, and is expected to reach USD 40.75 billion by 2030, at a CAGR of 3.71% during the forecast period (2025-2030). City planners are responding to rising population density, as evidenced by a surge in metro and light-rail orders. Urban rapid-transit expansions, decarbonization initiatives, and sustained public-sector capital investments primarily drive this growth momentum. These factors collectively highlight the increasing focus on sustainable and efficient urban transportation systems.

Key Report Takeaways

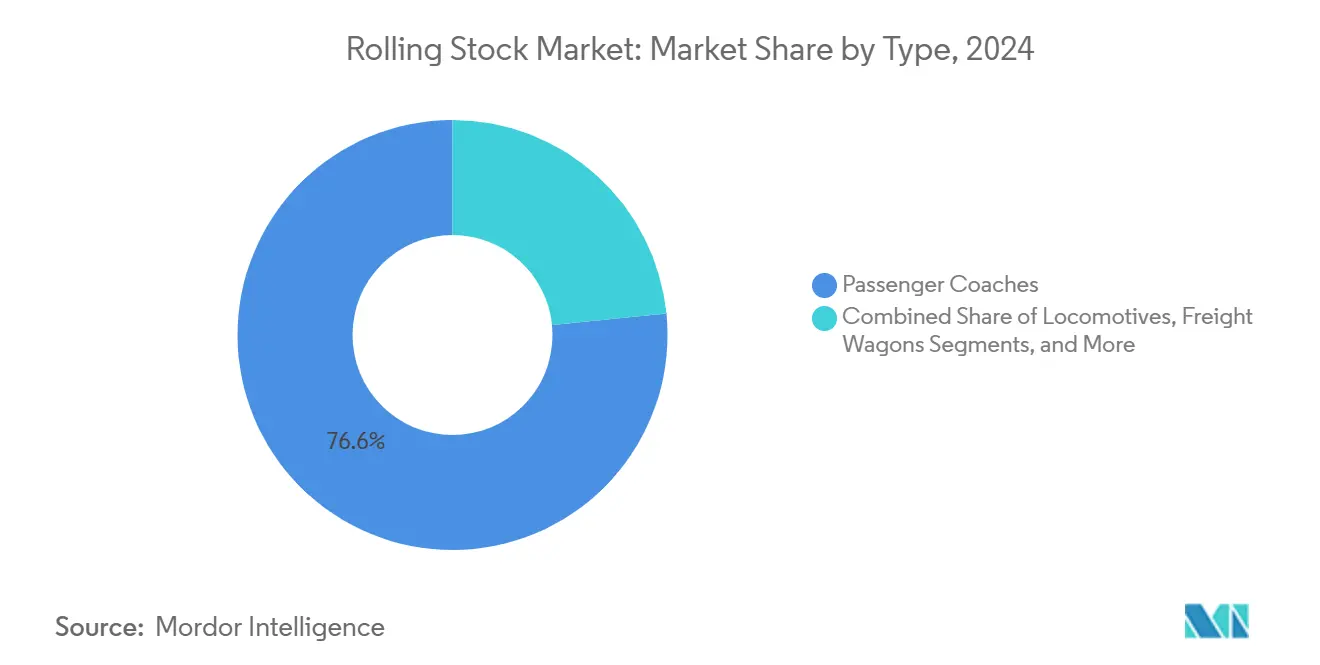

- By type, passenger coaches led with 76.62% of rolling stock market share in 2024, while metros and light rail are forecast to grow at a 12.81% CAGR to 2030.

- By propulsion type, electric systems commanded a 61.73% share of the rolling stock market size in 2024 and are advancing at a 5.63% CAGR through 2030.

- By application, passenger rail captured 63.52% revenue in 2024 and is projected to expand at a 4.94% CAGR through 2030.

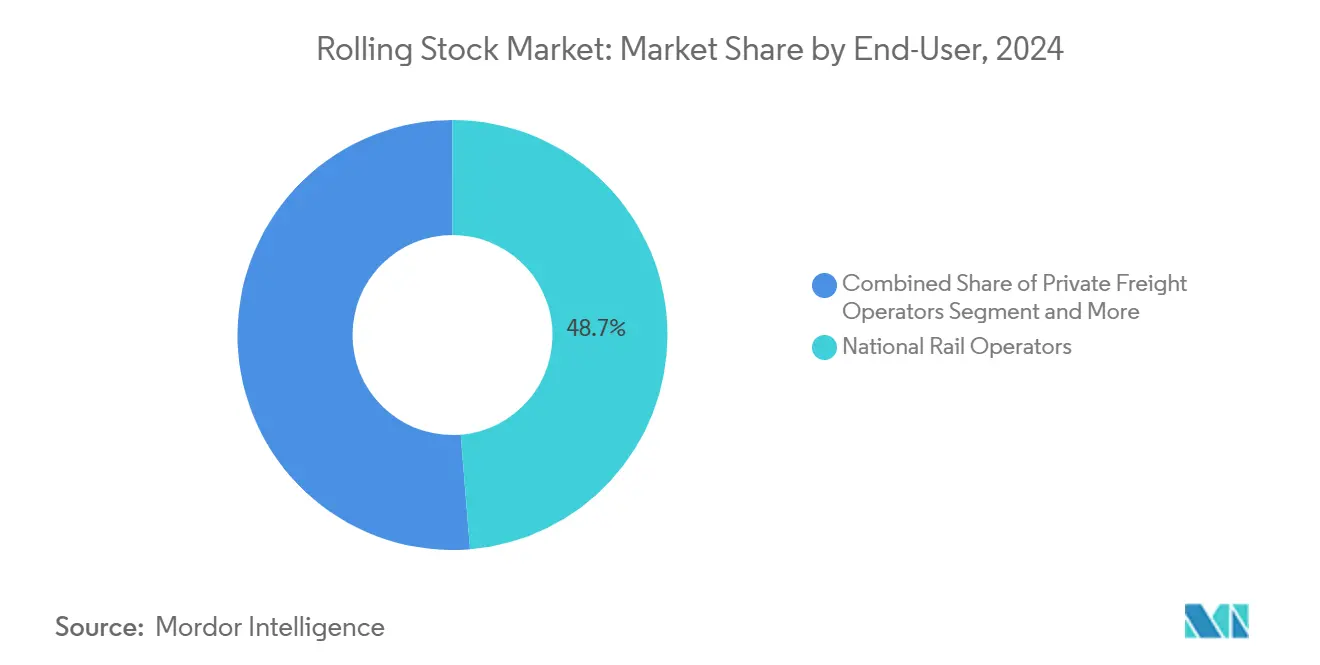

- By end-user, national rail operators held 48.71% share in 2024, whereas urban transit agencies posted the highest 7.11% CAGR to 2030.

- By technology, conventional systems kept a 93.46% share in 2024, yet autonomous platforms record an 11.55% CAGR through 2030.

- By geography, Asia-Pacific owns 53.81% of 2024 revenue, and the Middle East & Africa is growing at a 4.86% CAGR to 2030.

Global Rolling Stock Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization-driven metro expansion | +1.2% | Global, concentrated in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Government investments in high-speed rail corridors | +0.8% | Asia-Pacific, Europe, North America | Long term (≥ 4 years) |

| Decarbonization policies | +0.7% | Europe, North America, selective APAC markets | Medium term (2-4 years) |

| Infrastructure stimulus packages | +0.5% | Global, with emphasis on developed markets | Short term (≤ 2 years) |

| Lifecycle service contracts & mid-life modernizations | +0.4% | Global, led by Europe and North America | Medium term (2-4 years) |

| Hydrogen locomotive zero-emission | +0.3% | Europe, California, selective developed markets | Long term (≥ 4 years) |

Source: Mordor Intelligence

Urbanization-Driven Metro Expansion

Metropolitan agencies deepen rolling stock procurement to relieve overcrowded corridors, shown by Seoul’s GTX Line A debut in 2024 with 20 eight-car Hyundai Rotem trainsets operating at 180 km/h. Urban transit agencies already hold 20.11% of the 2024 demand and are the fastest-growing end-user group at 7.13% CAGR by 2030 as cities pivot to driverless networks. The USD 664 million Los Angeles Metro contract with Hyundai Rotem illustrates how global sporting events accelerate order cycles, aligning deliveries for the 2028 Games. Grade of Automation 4 systems raise line capacity by 30% through headways below 100 seconds, as documented by Berlin’s U-Bahn CBTC upgrade. Copenhagen’s plan to convert its S-bane network to driverless operations by 2033 extends the automation wave to regional commuter services.[1]Siemens Mobility, "Driverless Train Operations: Siemens Mobility Upgrades Signaling Entire S-Bane Network," press.siemens.com

Government Investments in High-Speed Rail Corridors

State-funded corridors reshape fleet specifications. Egypt’s 2,000 km network will require 41 Velaro and 94 Desiro trainsets inside an EUR 8.1 billion turnkey scope. JR East’s E10 Shinkansen, slated for 2030, trims emergency stop distance by 15% and introduces advanced seismic response. California selected Siemens’ American Pioneer 220 sets capable of 220 mph, marking North America's first Velaro Novo order. South Korea’s KTX-CheongRyong went into service in 2024 with fully localized production, demonstrating domestic industrial policy. A USD 642 billion GCC rail pipeline positions the Middle East for sustained procurement as projects shift from planning to execution.

Decarbonization Policies Accelerating Electric Locomotives

Zero-emission mandates keep electric propulsion at 61.73% share in 2024, rising at 5.63% CAGR through 2030 as diesel fleets retire. California’s hydrogen locomotive pilots with CPKC and CSX show alternative decarbonization paths, echoed by CRRC’s hydrogen units for Chilean mining shippers . Bayern intends to remove diesel from 462 km of lines by 2036, purchasing tilting battery trainsets and funding EUR 365 million of supporting infrastructure . Dublin’s DART+ battery-electric multiple units can cover 80 km beyond catenary and widen service reach . Hitachi battery retrofits on TransPennine Express reduced emissions and fuel cost by 30%, giving operators a transitional option before full electrification.[2]Hitachi Ltd., "Hitachi Rail Acquires Thales' Ground Transportation Systems for €1,660m," hitachi.com

Infrastructure Stimulus Packages Boosting Rail CAPEX

Public-sector stimulus accelerates replacement cycles. The U.S. Infrastructure Investment and Jobs Act finances Amtrak’s USD 7 billion Long Distance Fleet program targeting 40-year-old coaches. Mexico’s USD 7.8 billion Tren Maya and the USD 12 billion Brightline West corridor show how federal backing crowds in private rolling stock capital. Indian Railways’ USD 30 billion budget amplifies domestic manufacturing, with Integral Coach Factory aiming for 3,000 coaches including 600 Vande Bharat units in 2024-25. BNSF’s USD 3.8 billion 2025 program directs USD 2.84 billion to rail infrastructure and locomotives. The European Union’s proposed EUR 3 billion Rail Research Programme underwrites ERTMS, FRMCS, and Digital Automatic Coupling, sustaining technology-rich demand.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost and long procurement cycles | -0.6% | Global, acute in developing markets | Medium term (2-4 years) |

| Raw-material inflation & supply-chain disruptions | -0.4% | Global, concentrated in steel-dependent regions | Short term (≤ 2 years) |

| Regulatory uncertainty in cross-border certification | -0.3% | Europe, cross-border corridors globally | Medium term (2-4 years) |

| Grid-capacity limits for large-scale electrification | -0.2% | Global, acute in developing grid infrastructure | Long term (≥ 4 years) |

Source: Mordor Intelligence

High Capital Cost and Long Procurement Cycles

Procurement complexity slows delivery. Massachusetts Bay Transportation Authority renegotiated its CRRC contract amid inflation and tariffs that affected the USD 1.1-1.4 billion program. Indian Railways re-tendered Vande Bharat 4.0 after Alstom’s bid surpassed the Rs 1.40 billion per set target, lengthening timelines. Kapurthala Rail Coach Factory delivered none of its 32 planned Vande Bharat sets in FY 2022-23 due to capacity limits. Titagarh Rail Systems expects a 6-9-month slip in sleeper-variant prototyping, with the first unit now due March 2026. Amtrak’s Inspector General urges stronger risk management for its Long Distance Fleet Replacement to control cost and schedule.

Raw-Material Inflation & Supply-Chain Disruptions

Steel volatility pressures margins. European apparent consumption fell 3.1% in Q1 2024 following prior contractions tied to energy costs and conflict-related disruptions. Scrap scarcity complicates Electric Arc Furnace adoption, widening recycled-metal price spreads. U.S. metals tariffs push producers toward advance purchasing that locks up working capital. JR East delayed Chuo Line double-deck coaches until March 2025 because of semiconductor shortages. India’s import dependency for wheels spurs domestic capacity plans targeting 200,000 units annually by 2026.

Segment Analysis

By Type: Passenger Coaches Dominate Despite Metro Surge

Passenger coaches held 76.62% of 2024 revenue, anchoring intercity and commuter services within the rolling stock market. Metros and light rail, however, record a 12.81% CAGR, underscoring urban capacity demands that align with Grade of Automation investments. Locomotives holds a significant share as operators favor electric or hydrogen variants that meet net-zero goals. Freight wagons slice is supported by Greenbrier’s 7,000-unit Q4 2024 deliveries that keep backlogs at a decent value.

The metro boom illustrates how rolling stock market size gains are concentrated in driverless fleets ordered by Seoul, Los Angeles, and Copenhagen. Passenger coach upgrades such as Alstom’s EUR 4 billion S-Bahn Cologne contract show operators lock in 34-year maintenance terms to secure lifecycle support.[3]Alstom, "Alstom Wins €4 Billion Contract Supply and Maintenance 90 Commuter Trains S-Bahn Cologne Germany," alstom.com Locomotive suppliers leverage hydrogen pilots for Chile and North America, broadening the propulsion mix. Freight wagon demand rides commodity growth, with mining corridors in Guinea and iron ore routes in Australia booking new orders.

Note: Segment shares of all individual segments available upon report purchase

By Propulsion Type: Electric Systems Lead Decarbonization

Electric traction controlled 61.73% of 2024 revenue and expands at 5.63% CAGR, maintaining the largest rolling stock market share as grid-powered operations scale. Diesel remains at forefront but faces retirement; hydrogen fuel cells and battery-electric both are offering modular pathways toward net zero. Dual-mode locomotives provide a decent share, blending catenary and diesel for transitional corridors.

Battery-electric advances lift rolling stock market size through projects like Dublin’s DART+ and Bayern’s tilting battery sets. Hydrogen programs in California and Chile signal long-term potential, although infrastructure cost and fuel availability limit near-term uptake. The Federal Railroad Administration frames dual-mode and intermittent electrification as cost-effective steps, sustaining investment in hybrid fleets.

By Application: Passenger Rail Drives Growth

Passenger services generated 63.52% of revenue in 2024, outpacing freight with a 4.94% CAGR through 2030 as governments support high-speed lines. Freight maintained a decent share, supported by North American Class I modernizations and commodity-linked corridors in emerging markets.

Egypt, California, and India anchor new passenger demand, with India targeting 10 billion annual riders by 2030—up from 6.5 billion in 2024—thereby enlarging the rolling stock market size for long-distance fleets. Freight orders such as Wabtec’s USD 248 million Guinea locomotives tap mining growth, while UAE-Oman cross-border corridors strengthen Gulf logistics.

By End-User: Urban Transit Agencies Accelerate Adoption

National rail operators kept a 48.71% share in 2024, reflecting their scale in long-distance services. Though smaller, urban transit agencies log the highest 7.11% CAGR as city authorities automate networks. Private freight operators benefits from lease models that lift asset utilization.

Copenhagen’s S-bane automation and Deutsche Bahn’s 137 ICE 4 deliveries show how public players modernize fleets, while Trinity Industries’ 97.5% lease utilization underscores strong private-sector economics. Alstom’s USD 515 million Metrolink services contract reflects growing outsourcing in urban transit.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Autonomous Systems Gain Momentum

Conventional technology kept 93.46% share, yet autonomous and driver-assist platforms register an 11.55% CAGR as operators trial GoA4 networks. Berlin’s CBTC upgrade delivers 30% capacity gains, while Korea Railroad Research Institute’s 5 G-based program targets similar headway reductions.

Hyundai Rotem supplies autonomous LRVs for Taiwan, and Alstom plans GoA4 regional prototypes by 2025, confirming broader application beyond metros. Digital S-Bahn Hamburg integrates Automatic Train Operation with ETCS to equip more than 400 vehicles mid-decade, reinforcing rolling stock market share for technology vendors.

Geography Analysis

Asia-Pacific generated 53.81% of 2024 revenue, underpinned by CRRC’s dominating global share and India’s USD 30 billion modernization budget that widens domestic production. Japan’s forthcoming E10 Shinkansen and South Korea’s fully localized KTX-CheongRyong illustrate regional high-speed focus, while India’s plan for 250 km/h indigenous sets diversifies supply chains. Seoul’s GTX expansion and Taiwan’s autonomous LRVs confirm technological advancement across city networks.

Europe retained the second position in 2024 due to sustained ICE, TGV, and regional upgrade programs. Germany finalized 137 ICE 4 units valued at EUR 6 billion, while Berlin’s CBTC conversion unlocks 30% capacity. France’s EUR 850 million Proxima order, Cologne’s EUR 4 billion commuter fleet, Copenhagen’s automation, and Dublin’s battery-electric sets showcase a diverse procurement slate. Middle East and Africa records the fastest 4.86% CAGR to 2030, led by a USD 642 billion GCC rail pipeline and flagship programs in Saudi Arabia, Egypt, and the UAE-Oman corridor. Saudi Arabia alone earmarks USD 45 billion, including the Dream of the Desert luxury train, while Egypt’s Velaro order sets a regional high-speed benchmark. Sub-Saharan launches such as Nigeria’s Abuja metro revivals and DR Congo’s MetroKin highlight nascent urban demand.

North America’s slice stems from freight modernization and passenger corridor expansion, with projects such as Brightline West and Amtrak’s fleet renewal enlarging the rolling stock market. Wabtec’s USD 248 million Guinea order and CSX’s locomotive upgrades confirm ongoing freight capital investment.

Competitive Landscape

The rolling stock market is moderately concentrated, with players like CRRC, Alstom, and Siemens dominating the market. Hitachi Rail’s EUR 1.66 billion acquisition of Thales Ground Transportation Systems broadens its reach to 51 countries and nearly doubles engineering staff to 24,000. Wabtec’s USD 960 million Dellner Couplers and USD 110 million Fanox and Kompozitum purchases illustrate vertical integration into high-margin components.

Suppliers differentiate through automation, electrification, and digital service platforms that convert orders into recurring revenue. Alstom’s GoA4 developments and 34-year S-Bahn Cologne maintenance deal exemplify this shift. Emerging players appear in growth regions: Texmaco Rail’s Rs 615 crore Jindal Rail Infrastructure acquisition makes it India’s largest wagon producer. Titagarh Rail Systems secured Rs 240 billion Vande Bharat sleeper contracts.

White-space contests arise in hydrogen propulsion, battery-electric platforms, and analytics-driven maintenance, pitting traditional builders against technology specialists. Siemens, Hitachi, and Stadler emphasize modular hybrid lines, whereas start-ups provide predictive software that reduces unplanned downtime.

Rolling Stock Industry Leaders

-

CRRC Corporation Limited

-

Alstom SA

-

Siemens AG

-

Stadler Rail AG

-

Hitachi Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Wabtec announced the USD 960 million acquisition of Dellner Couplers, adding an installed base of 100,000 couplers and 12,500 gangways and projecting USD 250 million in revenue in 2025.

- February 2025: Siemens Mobility signed a EUR 50 million framework with Northrail for up to 50 Vectron locomotives plus an 8-year service package with fleet monitoring.

- January 2025: Alstom reached a CAD 500 million agreement with Metrolinx to overhaul 181 Bi-Level cars, sustaining 250 jobs at Thunder Bay until 2030.

- June 2024: Siemens Mobility expanded its Cornellà, Spain, factory by adding a gearbox line rated for 500 locomotive units yearly.

Global Rolling Stock Market Report Scope

Rolling stock is generally employed for the transportation of goods, like heavy machinery, construction materials, conventional fuels, agricultural products, and so on, and passengers. The rolling stock market is segmented by type, propulsion type, and geography. By type, the market is segmented into Locomotives, Metros, Passenger Coaches, and Other Types. By propulsion type, the market is segmented into Diesel, Electric, and Electro-diesel. The report also covers the market sizes and forecasts for the Rolling stock market in 17 countries across major regions. For each segment, market sizing and forecasts have been done based on value (USD Billion).

| By Type | Locomotives | Diesel Locomotives | |

| Electric Locomotives | |||

| Hybrid / Hydrogen Locomotives | |||

| Metros and Light Rail Vehicles | |||

| Passenger Coaches | |||

| Freight Wagons | |||

| By Propulsion Type | Diesel | ||

| Electric | |||

| Electro-diesel / Dual-mode | |||

| Hydrogen Fuel Cell | |||

| Battery-electric | |||

| By Application | Passenger Rail | ||

| Freight Rail | |||

| By End-user | National Rail Operators | ||

| Private Freight Operators | |||

| Urban Transit Agencies | |||

| By Technology | Conventional | ||

| Autonomous / Driver-Assist | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Turkey | |||

| South Africa | |||

| Egypt | |||

| Rest of Middle East and Africa | |||

| Locomotives | Diesel Locomotives |

| Electric Locomotives | |

| Hybrid / Hydrogen Locomotives | |

| Metros and Light Rail Vehicles | |

| Passenger Coaches | |

| Freight Wagons |

| Diesel |

| Electric |

| Electro-diesel / Dual-mode |

| Hydrogen Fuel Cell |

| Battery-electric |

| Passenger Rail |

| Freight Rail |

| National Rail Operators |

| Private Freight Operators |

| Urban Transit Agencies |

| Conventional |

| Autonomous / Driver-Assist |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

1. What is the current rolling stock market size?

The rolling stock market reached USD 33.97 billion in 2025 and is forecast to grow at a 3.71% CAGR through 2030.

2. Which segment is growing fastest in the rolling stock market?

Metros and light rail vehicles are expanding at a 12.81% CAGR, outpacing all other type segments.

3. How dominant are electric propulsion systems?

Electric traction commanded 61.73% of 2024 revenue and continues to rise at a 5.63% CAGR as decarbonization mandates phase out diesel fleets.

4. Which region holds the largest rolling stock market share?

Asia-Pacific led with 53.81% of 2024 revenue due to strong manufacturing capability and extensive rail expansion programs.

5. What is driving the adoption of autonomous rail technology?

Grade of Automation 4 deployments in metros, combined with CBTC and digital signaling, deliver up to 30% capacity gains and lower operating costs, encouraging operators to move beyond conventional systems.

6. How concentrated is the competitive landscape?

Together, three companies—CRRC, Alstom, and Siemens—control nearly 70% of global revenue, yet emerging regional manufacturers and technology suppliers continue gaining ground in specific niches.

Page last updated on: July 7, 2025