Robotic Waste Sorting System Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

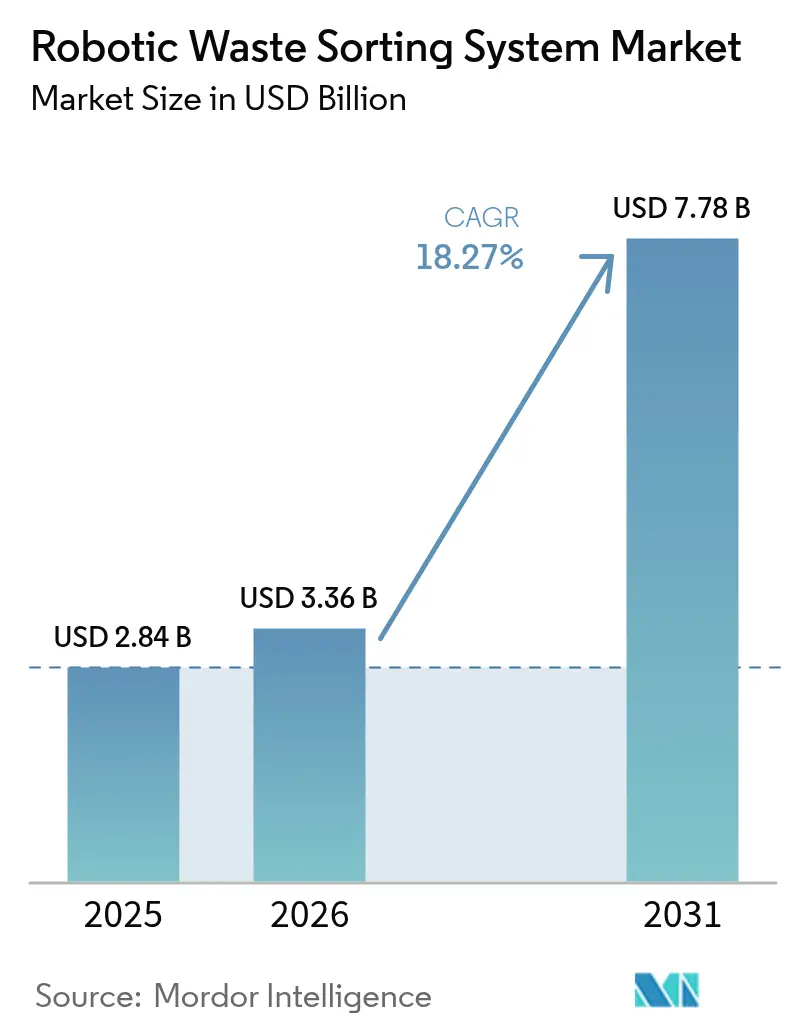

| Market Size (2026) | USD 3.36 Billion |

| Market Size (2031) | USD 7.78 Billion |

| Growth Rate (2026 - 2031) | 18.27% CAGR |

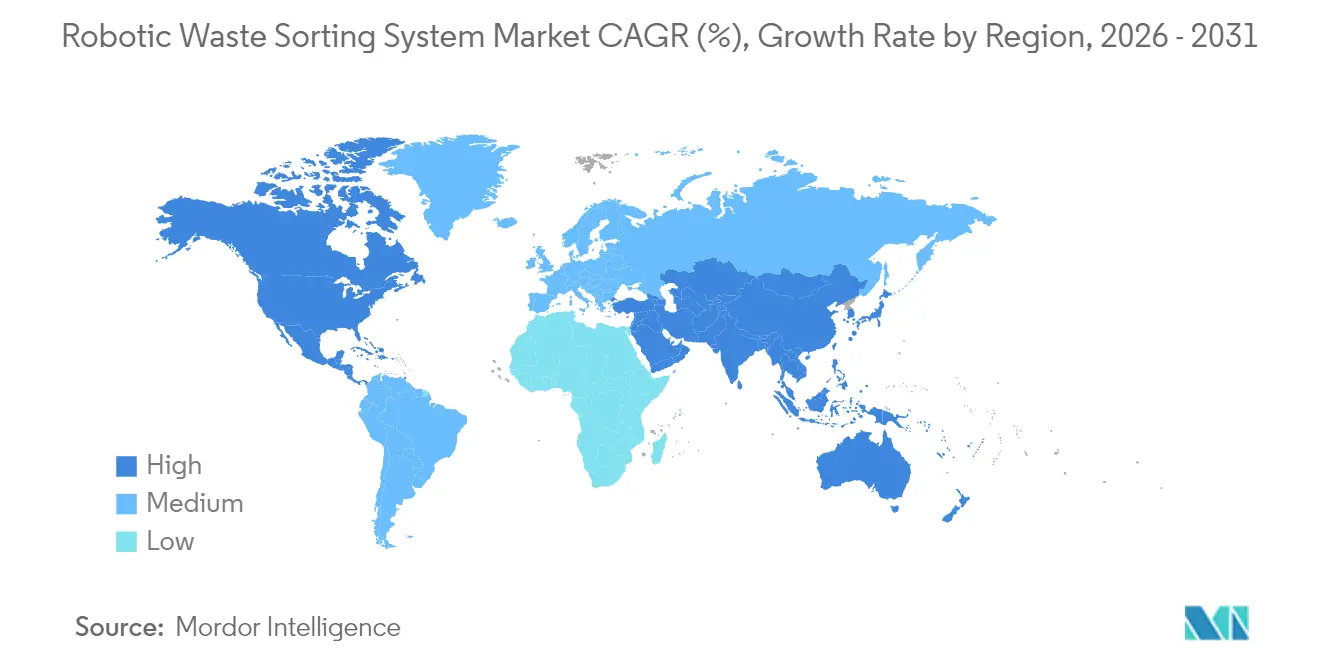

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

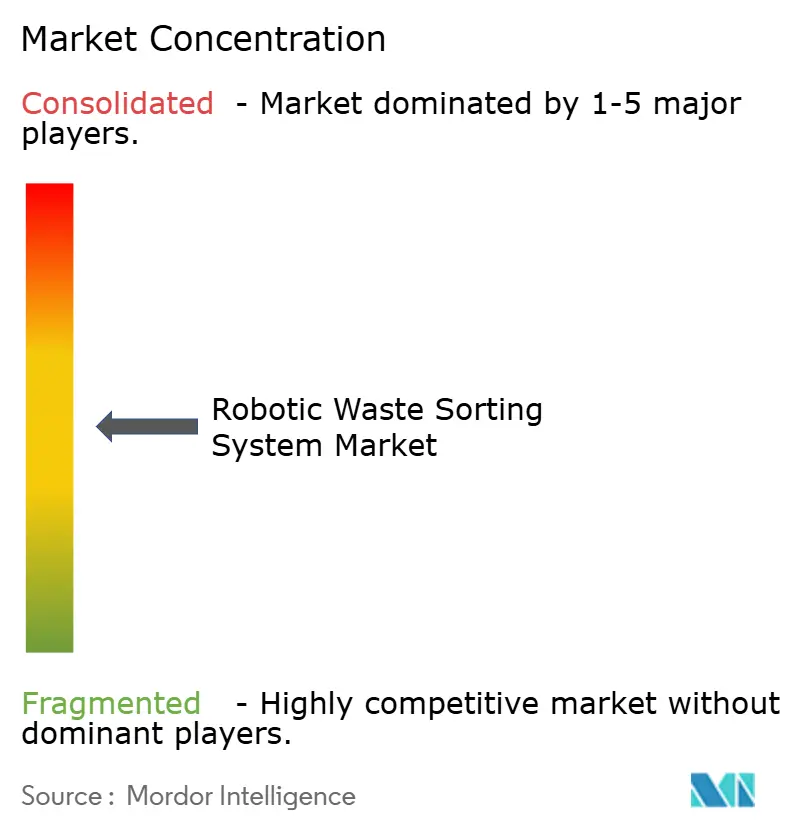

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotic Waste Sorting System Market Analysis by Mordor Intelligence

The robotic waste sorting system market size is expected to grow from USD 2.84 billion in 2025 to USD 3.36 billion in 2026 and is forecast to reach USD 7.78 billion by 2031 at 18.27% CAGR over 2026-2031. Growth momentum in the robotic waste sorting system market is driven by tightening landfill-diversion rules, producer responsibility mandates, and sustained investment in artificial-intelligence hardware.[1] European Parliament, “Packaging and Packaging Waste,” europarl.europa.eu Automated sorting has become a strategic response to labor scarcity at Material Recovery Facilities (MRFs) and to China’s restrictions on low-grade imports, both of which have raised the value of high-purity recyclables. Rapid improvements in multi-sensor fusion now allow robots to recognize more than 500 waste categories with 99% accuracy, lifting recovery rates and lowering residual disposal fees. Service-based leasing is gaining traction, easing capital constraints, while cybersecurity spending is rising as interconnected fleets expose facilities to industrial control threats. As a result, the robotic waste sorting system market continues to shift from pilot projects to core infrastructure investment strategies across advanced economies.

Key Report Takeaways

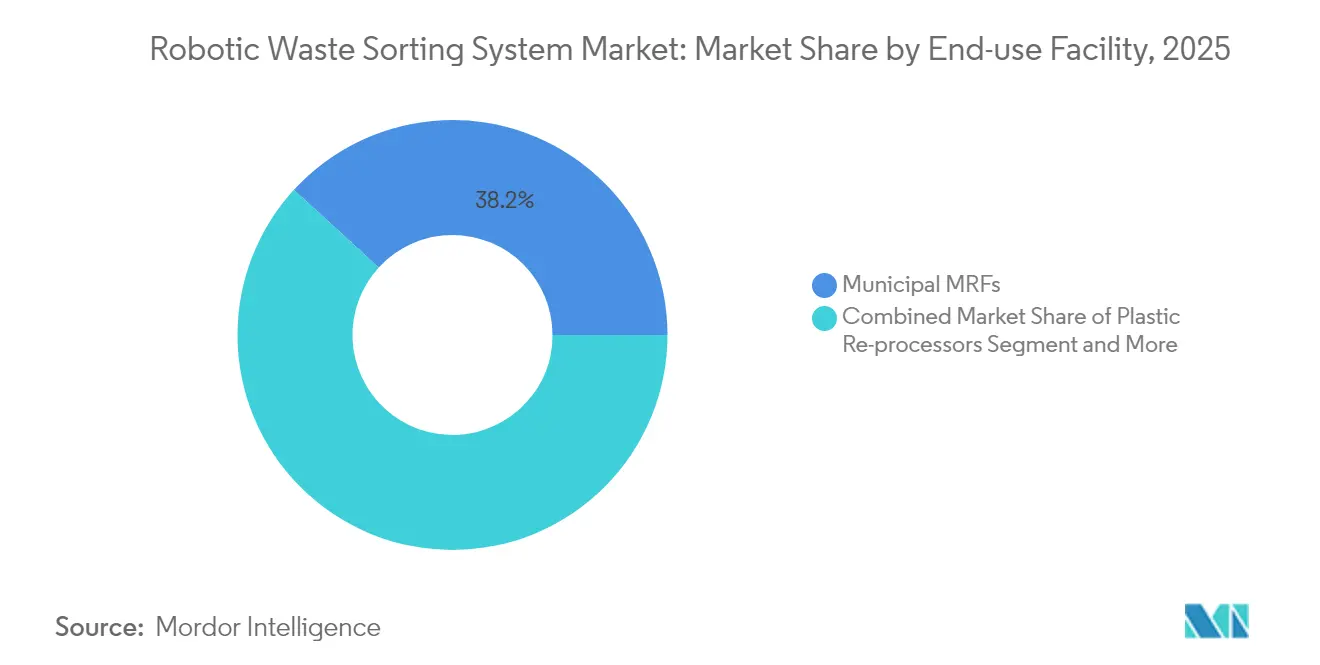

- By end-use facility, Municipal MRFs led with 38.20% of the robotic waste sorting system market share in 2025, while Plastic Re-processors are forecast to expand at a 20.35% CAGR through 2031.

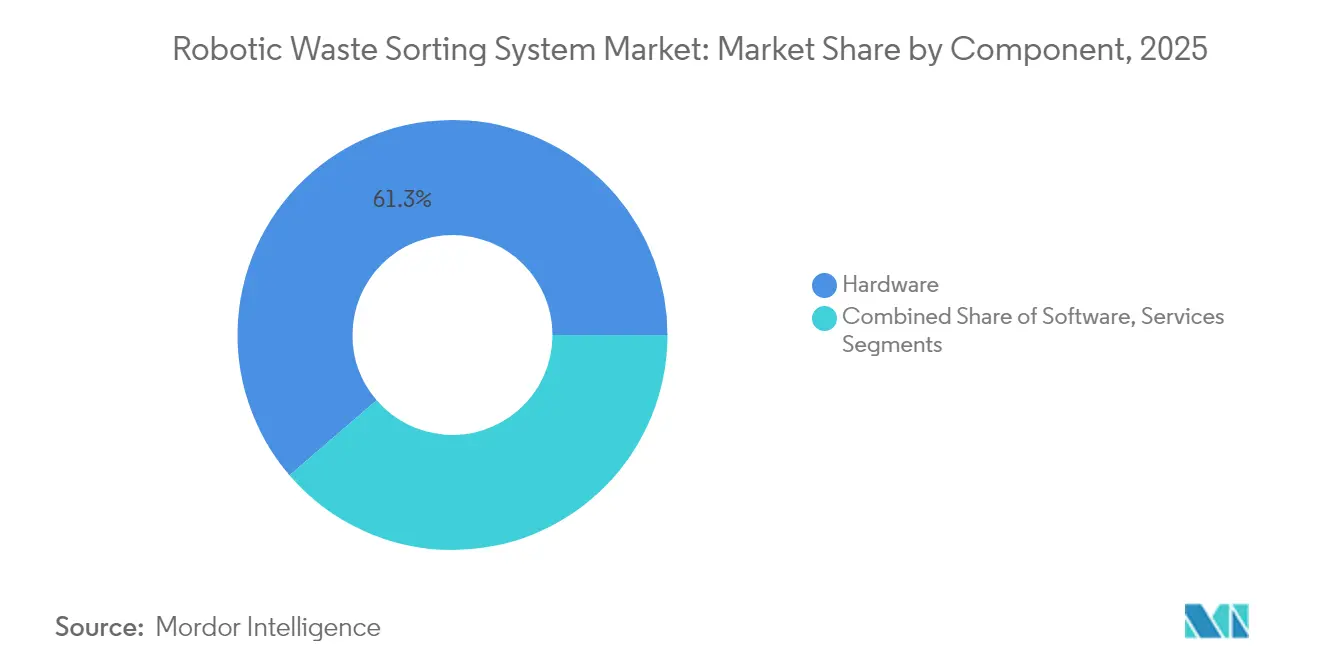

- By component, hardware accounted for 61.30% of the robotic waste sorting system market size in 2025; software is growing at 20.18% CAGR as AI capabilities scale.

- By sorting technology, NIR / hyperspectral optical systems held a 43.40% share of the robotic waste sorting system market size in 2025, whereas AI vision-only solutions are poised for a 19.47% CAGR to 2031.

- By geography, North America represented 32.70% of global revenue in 2025, but Asia-Pacific is the fastest-growing region at an 18.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Robotic Waste Sorting System Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter landfill-diversion and EPR regulations | +4.2% | EU, Asia-Pacific | Medium term (2–4 years) |

| Ban on low-grade waste imports | +3.8% | Global, spillover to Southeast Asia | Short term (≤ 2 years) |

| Labor shortages and rising MRF operating costs | +3.1% | North America, EU | Short term (≤ 2 years) |

| Surge in recycled-content packaging mandates | +2.9% | EU, Global brands | Medium term (2–4 years) |

| Demand for AI-enabled closed-loop data | +2.2% | North America, APAC tech hubs | Long term (≥ 4 years) |

| OEM service-based leasing models | +1.8% | Developed markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Stricter Landfill Diversion and EPR Regulations

Extended Producer Responsibility rules shift cost burdens from municipalities to brand owners, and the EU’s 2024 packaging measure requires all packaging to be recyclable and to hit specific recycled-content thresholds by 2030 and 2040, accelerating automation adoption. [2]OECD, “Extended Producer Responsibility and Economic Instruments,” oecd.org Municipalities and producers now deploy robots to secure higher material purity and avoid EPR penalties. The OECD notes that variable EPR fees reward companies that design recyclable products, which further sharpens demand for precision sortation. Facilities deploying robotic systems report recovery-rate jumps of 20 percentage points within 12 months of commissioning. These returns strengthen the robotic waste sorting system market as new regional mandates replicate the EU model.

Ban on Low-Grade Waste Imports by China and Others

China’s National Sword policy requires sub-0.5% contamination, forcing Western MRFs to upgrade equipment to regain export revenue. Robots provide the accuracy needed to meet the new quality bar, and payback periods have fallen to under 24 months in high-volume plants. Similar bans in Malaysia, Thailand, and Vietnam magnify the driver. Consequently, the robotic waste sorting system market has realigned toward domestic capacity investment, with North American operators adding AI sorters at mixed-plastic lines to recapture commodity margins lost after 2018.

Labor Shortages and Rising MRF Operating Costs

Turnover rates above 100% led managers to automate the most hazardous jobs. Human sorters average 40 picks per minute, whereas robots achieve 80 picks with 99% uptime, doubling throughput and reducing overtime costs. Decision-makers see a direct link between automation and operating-cost avoidance, which underpins capital budgeting for new installations and reinforces expansion of the robotic waste sorting system market.

Surge in Recycled-Content Packaging Mandates

Consumer-goods groups have pledged to use 25–50% recycled plastic by 2030, creating premiums for food-grade pellets. Robots fitted with hyperspectral sensors detect polymer types with 99% accuracy, enabling facilities to supply these premium streams at higher margins. Plastic re-processors therefore record the highest forward orderbooks for automated lines, sustaining double-digit growth in the robotic waste sorting system market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and payback uncertainty | -2.8% | Emerging markets | Short term (≤ 2 years) |

| Cyber-security exposure of IIoT robots | -1.9% | Global critical infrastructure | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capex and Payback Uncertainty

Complete robotic lines cost USD 2–5 million, equal to 8–12 months of revenue for a 100,000-tonne MRF. Commodity-price swings elongate payback, delaying investment in emerging markets. Leasing and Robotics-as-a-Service (RaaS) are mitigating this restraint by shifting spending from capex to opex, yet access to dollar-denominated leases remains limited outside developed economies. The robotic waste sorting system industry therefore advances unevenly across regions with different capital-access profiles.

Cyber-Security Exposure of IIoT Robots

Cloud-connected robots widen the attack surface for critical waste infrastructure. Recent studies highlight gaps in user-friendly end-point protections, prompting operators to integrate ISA/IEC 62443 standards and layered network segmentation. [3]EURASIP Journal on Information Security, “Securing Cyber-Physical Robotic Budget allocations for cyber-hardening now form part of total-cost-of-ownership models, adding 3–5 percentage points to lifecycle cost and tempering rollout speed within the robotic waste sorting system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-use Facility: Municipal MRFs Anchor Demand

Municipal MRFs managed 38.20% of the robotic waste sorting system market in 2025, reflecting the largest installed base and the highest mix-waste volumes. As these plants target contamination thresholds below 1%, managers install AI robots on residual lines to boost purity and reduce landfill levies. The robotic waste sorting system market size for Municipal MRFs is projected to grow at a steady 14.62% CAGR through 2031, supported by state-level funding programs in the United States and provincial grants in Canada.

Plastic Re-processors, while smaller in absolute terms, are accelerating at 20.35% CAGR. The segment captures demand from consumer-packaged-goods brands pursuing closed-loop strategies. Robots specialize in polymer separation, extracting color-sorted PET and HDPE that command price premiums of up to 30% over mixed-bale equivalents. As a result, Plastic Re-processors are expected to hold a 23.10% robotic waste sorting system market share by 2031, narrowing the gap with Municipal MRFs.

By Waste Type Sorted: Plastics Dominate Complexity

Plastics accounted for 38.60% of revenue in 2025 and continue to exhibit the fastest uptake. AI systems now identify multilayer films and colored PET with near-laboratory precision. In value-chain terms, each percentage-point reduction in plastic bale contamination lifts resale prices by USD 25 per tonne, supporting investment cases. Paper and cardboard remain a stable category as optical scanners adjust for ink and residue. Metals enjoy robust capture using eddy currents, yet robots add value by isolating high-grade aluminum alloys. Glass sorting gains from AI color-detection models that lift recovery from 70% to 85% in Scandinavian plants.

The robotic waste sorting system market size for plastics alone is projected to exceed USD 3.01 billion by 2031, equal to 38.60% of global value. Robots’ ability to sort complex resins positions the segment for sustained double-digit expansion.

By Component: Software Captures Value Pools

Hardware still represented 61.30% of revenue in 2025; however, software is the value-creation engine. Fourth-generation recognition platforms like ZenBrain now account for 35% of total bill-of-materials in new orders, up from 20% in 2022. Predictive-maintenance algorithms reduce unplanned downtime by 40%, while continuous learning extends system life, mitigating obsolescence risk.

The robotic waste sorting system market sees software revenue growing at 20.18% CAGR to 2031, outpacing hardware expansion. Services, including RaaS contracts, are forecast to reach USD 1.12 billion annual revenue by 2031, reflecting a strategic pivot toward outcome-based pricing.

By Sorting Technology: AI Vision Challenges Hyperspectral

NIR / hyperspectral optical platforms held 43.40% share, underpinned by a three-decade performance record in polymer identification. Yet AI vision-only is growing at highest CAGR of 19.47% by 2031, while these solutions gain ground where flexibility trumps chemical specificity. These systems process 200 items per frame and can be retrofitted to legacy conveyors at half the cost of full optical rigs.

Hybrid multi-sensor configurations remain the premium solution for construction or e-waste, but procurement teams increasingly deploy pure vision systems on fiber and rigid-plastic lines, accelerating democratization of the robotic waste sorting system market.

Geography Analysis

North America accounted for 32.70% of global revenue in 2025, with early robot adopters scaling fleets to offset labor churn and to hit recycling-rate mandates in California, Oregon, and Colorado. Waste Management alone invested USD 1.4 billion in AI-enabled facilities between 2024 and early 2025. The region hosts over 400 AMP Robotics units, and robotic waste sorting system market size in the United States is projected to exceed USD 2.34 billion by 2031.

Asia-Pacific is the fastest-growing region at 18.15% CAGR. China’s domestic policy pivot from importer to recycler triggered a surge in capacity adds, including ZenRobotics construction-waste lines in Shanghai. Japan’s municipal plants deploy AI glass sorters that lift recovery rates for amber and flint cullet, supporting the country’s bottle-to-bottle targets. South Korea’s ATron robots demonstrate 99.3% precision and showcase export potential across ASEAN. Consequently, Asia-Pacific’s share of the robotic waste sorting system market is forecast to rise from 27.40% in 2025 to 33.20% in 2031.

Europe benefits from mature EPR regulations that fund capital investment. Denmark’s autonomous construction-waste plant achieves 98% purity for recycled aggregates, setting new circular-economy benchmarks. Spain’s first AI sorting initiative under Urbaser signals wider Iberian adoption. Although growth is steadier than in Asia-Pacific, the region remains a technology test bed, sustaining a high concentration of pilot projects and patents that inform global standards for the robotic waste sorting system market.

Competitive Landscape

The market is moderately fragmented with top players holding a combined 45% revenue share. AMP Robotics, ZenRobotics (Terex), and TOMRA Systems remain technology leaders, each differentiating by proprietary AI stacks and sensor portfolios. Terex’s 2022 acquisition of ZenRobotics integrated heavy-equipment capabilities with robotic intelligence, enabling cross-selling into metals and demolition segments. TOMRA leverages its installed sensor base to upsell AI modules, while AMP expands its cloud-analytics platform, monetizing performance data for process optimization.

Emerging innovators such as Everest Labs and Greyparrot focus on retrofit vision platforms that lower barriers for mid-tier MRFs. These firms use capital-light business models and RaaS contracts to capture greenfield projects in Latin America and the Middle East. MandA activity is expected to intensify as incumbents seek AI capabilities and regional coverage, driving gradual consolidation within the robotic waste sorting system market. Patent filings around multi-sensor fusion and chemical-composition detection have more than doubled since 2022, underscoring competitive intensity.

Robotic Waste Sorting System Industry Leaders

Machinex Industries Inc

AMP Robotics Corporation

ZenRobotics Ltd

Sadako Technologies

Bulk Handling Systems (BHS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Recology King County installed Glacier AI robots to reduce contamination at its Washington MRF, aligning with a zero-landfill strategic objective and showcasing data-driven process control.

- May 2025: Fukuoka Institute of Technology partnered with Temasek Polytechnic and Hanoi University to debut a Robot Compost system for EXPO 2025 Osaka, representing a collaboration framework for cross-border R&D commercialization.

- January 2025: AETECH commercialized its ATron robot in Korea, reaching 13 domestic installations and signaling market readiness for high-accuracy, mid-cost systems aimed at secondary cities.

- January 2025: Danish Technological Institute joined Refind Technologies to automate battery extraction from e-waste, extending robotic applications into hazardous-waste niches and strengthening circular-economy compliance.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the robotic waste sorting system market as the revenue generated from newly installed, fixed or mobile robotic units that identify, pick, and separate solid-waste streams inside material-recovery facilities, plastic re-processors, e-waste recyclers, construction and demolition sorting lines, and industrial recycling plants. These systems combine vision sensors, AI software, and gripping hardware, and the market size is expressed in constant 2025 US dollars, covering hardware, embedded software, and first-year services only.

Scope Exclusion: We do not count revenue from optical sorters without robotic pick arms, multiyear maintenance contracts, or autonomous waste collection vehicles.

Segmentation Overview

- By End-use Facility

- Municipal MRFs

- Industrial and Commercial Recycling Plants

- Construction and Demolition Facilities

- Plastic Re-processors

- E-waste Recyclers

- By Waste Type Sorted

- Plastics

- Paper and Cardboard

- Metals

- Glass

- Organic and Food Waste

- Mixed CandD Debris

- By Component

- Hardware

- Software

- Services (Installation, OandM, Leasing)

- By Sorting Technology

- AI Vision-only

- NIR / Hyperspectral Optical

- 3-D Laser and X-ray

- Hybrid Multi-Sensor

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- APAC

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- ASEAN-6

- Rest of APAC

- Middle East and Africa

- Middle East

- GCC (Saudi Arabia, UAE, Qatar)

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with plant managers in North America, Europe, and Asia, system integrators, sensor suppliers, and municipal procurement officers. Their insights confirmed labor cost pressures, achievable sort speed, and price dispersion, which let us fine-tune unit counts and utilization assumptions.

Desk Research

Mordor analysts reviewed open datasets such as Eurostat waste accounts, the US EPA Advancing Recycling Dashboard, China Solid Waste Center export filings, and Questel patent libraries to calibrate installed base and technology diffusion. Trade publications from ISWA, Plastics Europe, and the Bureau of International Recycling, together with company 10-Ks and press releases, helped us map new facility additions, throughput, and average selling prices. We also tapped paid intelligence from D&B Hoovers for revenue splits and Dow Jones Factiva for deal flow that signals capacity expansion. These sources shaped the historical skeleton we later validated. The list is illustrative; many other channels informed data collection and checks.

Market-Sizing & Forecasting

A top-down build began with municipal and commercial waste volumes by region, converted to addressable tons after recovery rate filters, then translated into robot demand through observed robot per ton ratios. Bottom-up cross-checks rolled up shipments reported by leading suppliers and weighted ASPs to validate totals. Key drivers in the model include waste generation per capita, recycling mandates, average plant throughput, capital cost trends, software subscription uptake, and sensor price learning curves. Five-year forecasts rely on multivariate regression combined with scenario analysis, with variable coefficients reviewed by our interview panel.

Data Validation & Update Cycle

Outputs pass variance checks against historical adoption curves and independent waste processing benchmarks before senior review. We refresh the model each year, and interim recalculations are triggered when a material event such as a nationwide landfill ban or a major funding round changes adoption economics.

Why Mordor's Waste Sorting Robots Baseline Commands Reliability

Published estimates often diverge because firms pick different waste streams, pricing envelopes, and refresh timings.

Closest published year used where a 2025 value is not available.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.84 B | Mordor Intelligence | |

| USD 2.70 B (2023) | Global Consultancy A | Includes retrofit services and rental fees |

| USD 2.00 B (2023) | Industry Association B | Excludes industrial recycling plants and applies lower ASPs |

| USD 2.17 B (2023) | Regional Analyst C | Uses conservative robot per ton ratios and 2022 exchange rates |

The comparison shows that Mordor's disciplined scope selection and yearly refresh give decision makers a balanced, transparent baseline traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the robotic waste sorting system market?

The global robotic waste sorting system market size is USD 3.36 billion in 2026 and is forecast to reach USD 7.78 billion by 2031.

Which end-use facility segment leads the market?

Municipal MRFs hold the largest share at 38.20% in 2025 due to urban waste volumes and stringent recycling targets.

Why is Asia-Pacific the fastest-growing region?

China’s domestic recycling build-out, Japan’s precision-sorting initiatives, and South Korea’s AI robot deployments drive an 18.15% CAGR through 2031.

How do Robotics-as-a-Service models affect adoption?

RaaS shifts spending from capital budgets to operating budgets, shortening payback cycles and enabling smaller facilities to adopt automation.

What cybersecurity standards apply to waste-sorting robots?

Operators increasingly adopt ISA/IEC 62443 frameworks to manage cyber-risks associated with cloud-connected industrial robots.

Page last updated on: