Resistance Bands Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

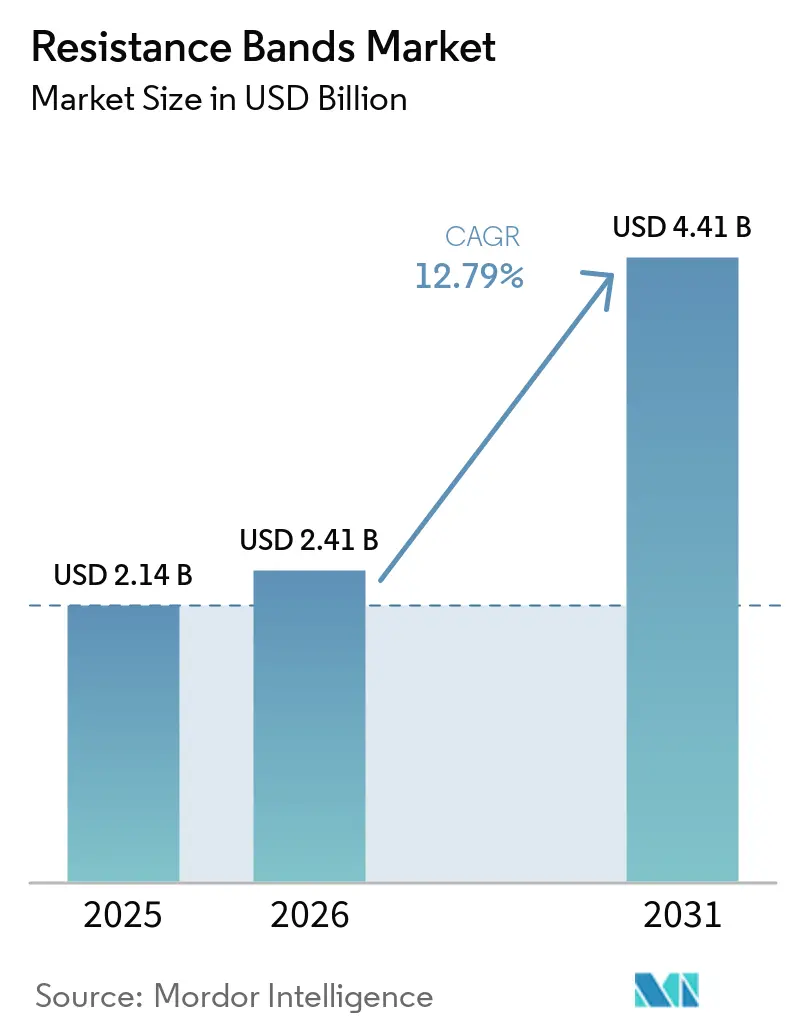

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 4.41 Billion |

| Growth Rate (2026 - 2031) | 12.79% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Resistance Bands Market Analysis by Mordor Intelligence

The Resistance Bands Market size is expected to grow from USD 2.14 billion in 2025 to USD 2.41 billion in 2026 and is forecast to reach USD 4.41 billion by 2031 at 12.79% CAGR over 2026-2031.

The market is being lifted by steady demand for compact strength tools that fit home, studio, and clinical settings without large equipment costs. Clinical rehabilitation is becoming a stronger part of the resistance bands market as elastic resistance training gains support from peer reviewed studies and established therapy suppliers expand their reach across hospitals and clinics. The resistance bands market also benefits from digital training ecosystems because bands can be paired with guided exercise content, app trials, and rehabilitation programs that increase repeat purchasing and brand stickiness. Product economics remain favorable because bands are portable, easy to store, and suitable for progressive resistance across many user groups, from beginners to older adults and post injury users. Even so, the resistance bands market faces pressure from counterfeit supply, input cost volatility, and the lack of standardized resistance ratings, which makes trusted brand positioning and clinical channel credibility more important than simple price competition.

Key Report Takeaways

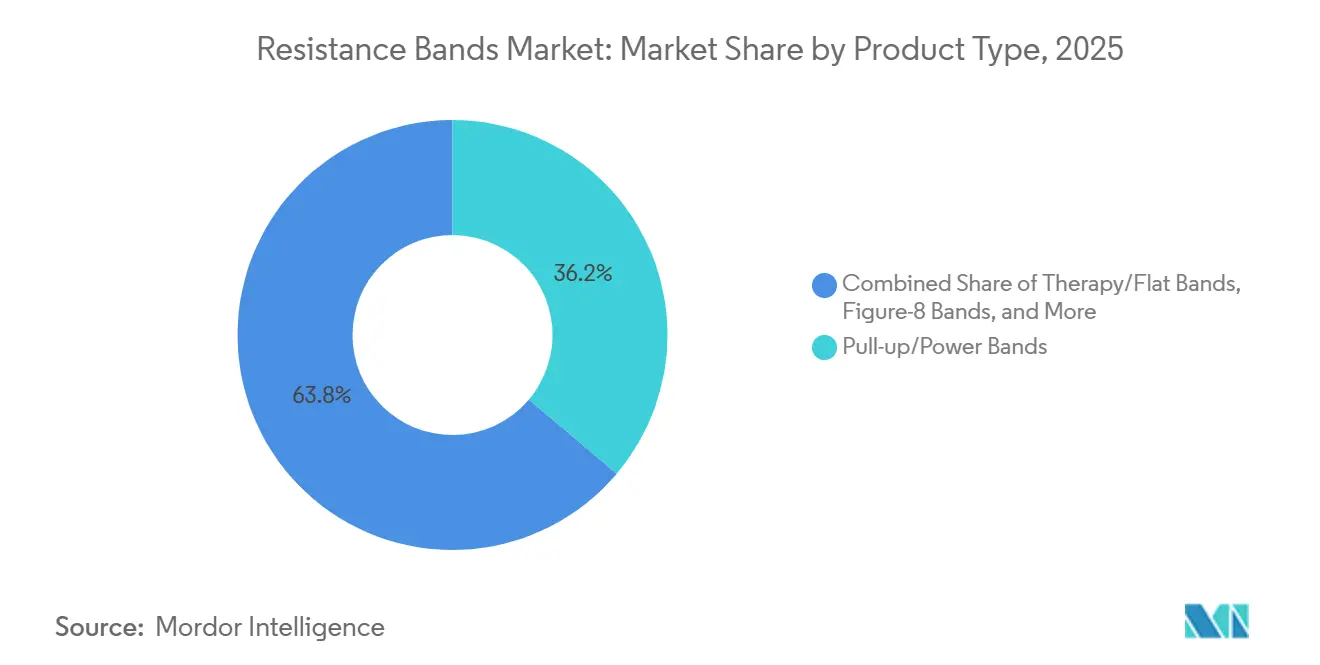

- By product type, Pull-up/Power Bands led with 36.15% revenue share in 2025, while Therapy/Flat Bands are forecast to expand at a 13.98% CAGR through 2031.

- By resistance level, Medium bands held 38.19% share in 2025, while Heavy bands are projected to grow at a 13.52% CAGR through 2031.

- By material, Latex accounted for 51.3% of revenue in 2025, while TPE is expected to record the fastest growth at a 13.25% CAGR through 2031.

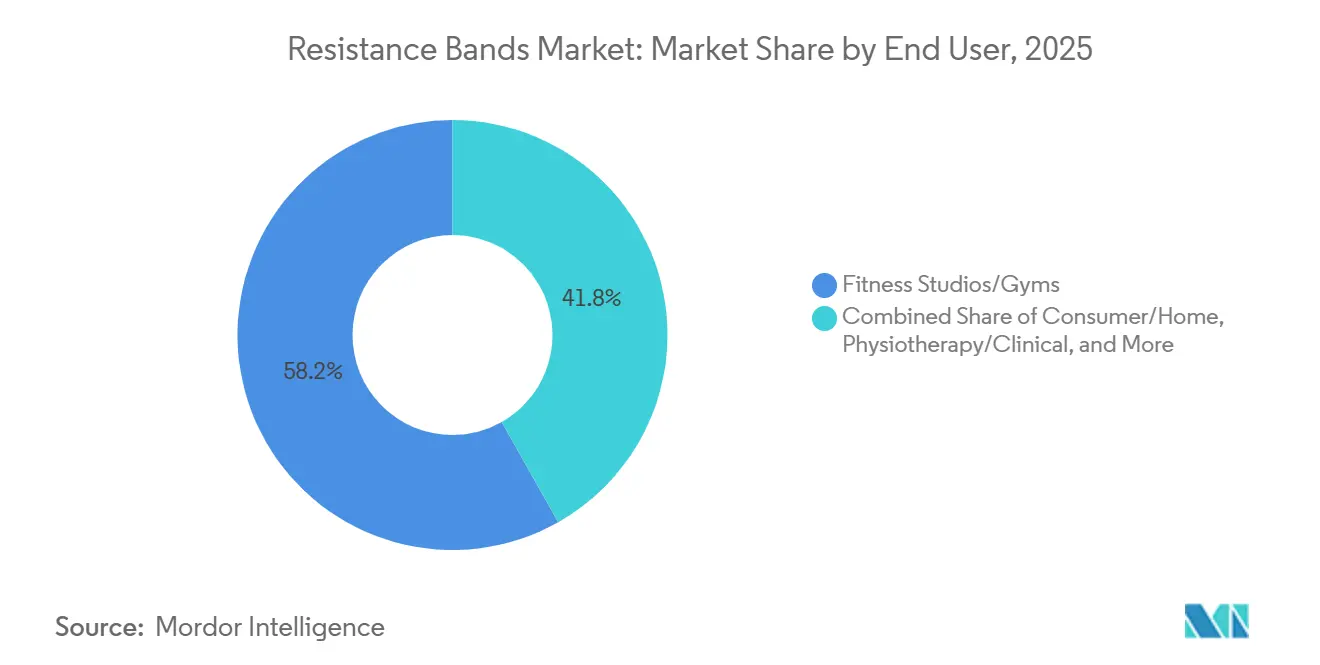

- By end user, Fitness Studios/Gyms held 58.19% of the resistance bands market share in 2025, while Consumer/Home is advancing at a 13.41% CAGR through 2031.

- By distribution, Offline channels captured 64.3% of revenue in 2025, while Online Marketplaces are projected to expand at a 13.92% CAGR through 2031.

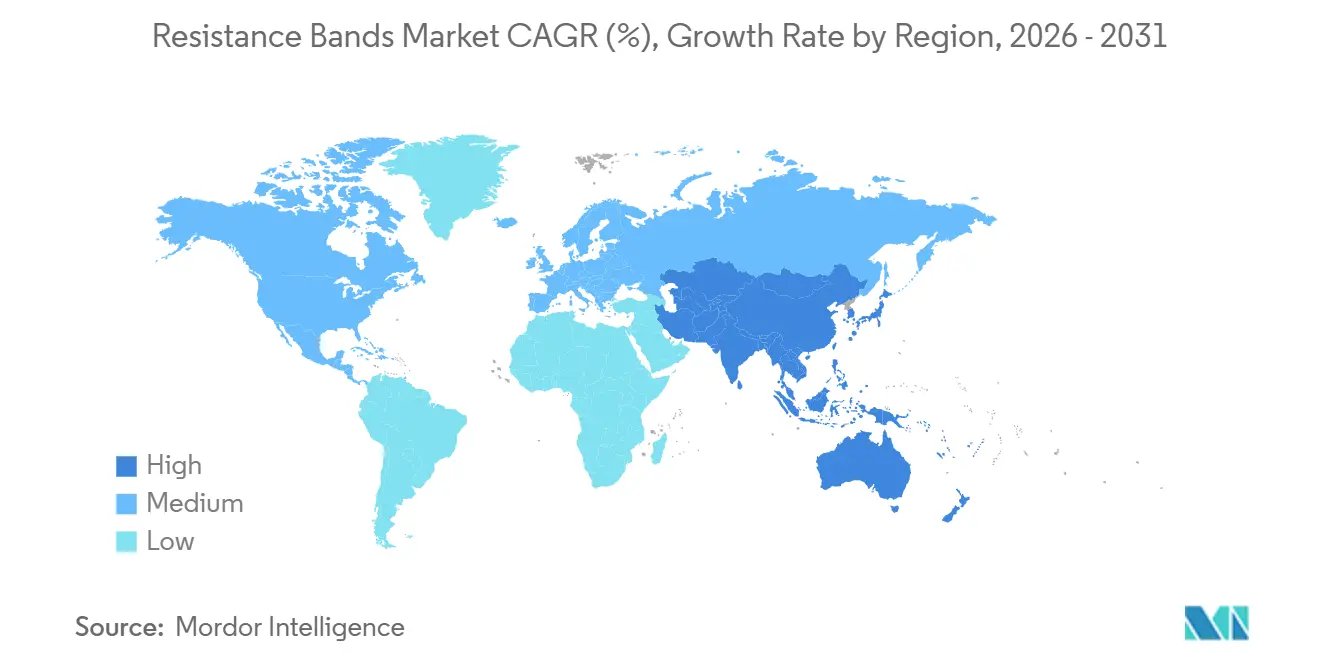

- By geography, North America held the largest regional share at 37.16% in 2025, while Asia-Pacific remains the fastest-growing region through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Resistance Bands Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Home Fitness And Hybrid Workout Adoption | +3.2% | Global | Medium term (2-4 years) |

| Expanded Use In Physiotherapy And Rehabilitation Pathways | +2.8% | Global, strong in North America, Europe, East Asia | Long term (≥ 4 years) |

| E-Commerce And DTC Penetration In Fitness Accessories | +2.1% | Global, leading in APAC and North America | Short term (≤ 2 years) |

| Low-Cost Portable Strength Training For Space-Constrained Users | +1.9% | Global, especially South Asia, Southeast Asia, urban Europe | Medium term (2-4 years) |

| Calisthenics And Pull-Up Assistance Fueling Loop Band Demand | +1.4% | Global, strong in North America, Europe, South Korea | Short term (≤ 2 years) |

| Shift To Latex-Free Sustainable Materials Opens Institutional Channels | +0.9% | Europe, North America, APAC premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Home Fitness and Hybrid Workout Adoption

Home and hybrid exercise patterns continue to support the resistance bands market because bands fit small spaces, require little setup, and support many exercise formats. The product works well in starter home gyms because a full set can cover mobility, strength, and recovery without the cost or footprint of larger equipment. This creates a durable entry point in the resistance bands market, where first time buyers can later move into higher resistance tiers, bundled accessories, and guided programming. Commercial suppliers are also designing studio systems that use bands in compact training layouts, which keeps band usage visible even when consumers move between home and facility based routines. Brands with digital content have an advantage because they connect the hardware to exercise plans, rehabilitation sequences, and habit building tools that encourage repeat engagement. That combination of convenience, portability, and digital support keeps home driven demand broad rather than temporary in the resistance bands market.

Expanded Use in Physiotherapy and Rehabilitation Pathways

The market is gaining durable support from physiotherapy and rehabilitation because elastic resistance is now used as a primary treatment tool in many recovery settings. A 16 week study published in Healthcare in May 2025 found that eccentric elastic band training in sedentary adults aged 60 and older increased BDNF by 5.4% and reduced oxidative stress markers by 29% to 44%, while more than 50% of participants achieved clinically meaningful improvement across 11 of 14 health variables. A November 2025 meta analysis in Frontiers in Sports and Active Living also reported significant gains in lower limb strength and balance in older adults, with stronger outcomes in programs lasting at least 12 weeks. These findings matter commercially because stronger clinical validation supports formulary inclusion and long duration supply relationships with therapy providers. Performance Health stated in 2024 that it had reach across 1,200 hospitals and 1,700 clinics globally, which shows how large the institutional channel already is for established suppliers. As rehabilitation volumes rise with aging populations, this clinical pathway should keep expanding the resistance bands market beyond consumer fitness alone.

E-Commerce and DTC Penetration in Fitness Accessories

Digital retail continues to widen access in the resistance bands market because bands are simple to ship, easy to compare, and well suited to repeat online purchases. Direct selling is especially valuable because it lets brands connect a physical product to app access, exercise libraries, and branded rehabilitation plans. TRX illustrates this approach by pairing its exercise bands with a 30 day app trial, HSA and FSA eligibility, and rehabilitation focused programming. This model gives branded suppliers a better chance to defend pricing because the buyer is paying for a training relationship rather than a strip of elastic material. The online channel also helps the resistance bands market reach users in cities where living space is tight and in regions where fitness retail remains underdeveloped. At the same time, success online depends on review quality, listing integrity, and protection against counterfeit adjacency, so digital growth rewards brands that manage content and channel discipline carefully.

Calisthenics and Pull-Up Assistance Fueling Loop Band Demand

The resistance bands market is also benefiting from the spread of calisthenics because loop formats are central to assisted pull up progressions and bodyweight strength training. The Calisthenics Association notes that first pull up training programs often require 3 to 5 loop bands at different resistance levels, which creates a multi unit purchase pattern rather than a single item sale[1]Calisthenics Association, “How to Do Your First Pull-Up: 8-Week Training Plan,” Calisthenics Association, calisthenicsassociation.org. That purchasing pattern supports revenue concentration in Pull-up/Power Bands, which already held the largest product type share in 2025. The category also fits both beginner and advanced use cases because the same format can assist pull ups, add accommodating resistance, or support mobility drills. This makes loop products a stable volume driver in the resistance bands market even when consumer preferences shift across training styles. As more coaches and digital fitness creators use band assisted progressions, demand for loop based products should stay closely linked to participation growth in bodyweight training communities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commoditization And Counterfeit Products Eroding Margins And Trust | -1.8% | Global, most acute in APAC and online channels | Medium term (2-4 years) |

| Substitution From Free Weights And Connected Fitness Systems | -1.4% | North America, Europe premium segments | Long term (≥ 4 years) |

| Non-Standardized Resistance Ratings Complicate B2B Procurement | -0.7% | Global, especially institutional channels | Medium term (2-4 years) |

| Latex Supply Tariff Volatility Impacting Input Costs | -1.2% | Global, most acute in North America post-2025 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Commoditization and Counterfeit Products Eroding Margins and Trust

The resistance bands market remains exposed to heavy price pressure because product design is easy to copy and many listings look interchangeable on marketplace platforms. This weakens brand differentiation in the lowest price tiers and makes it harder for suppliers to defend margins with appearance or packaging alone. In response, stronger brands are using training ecosystems, clinical endorsements, and community based programming to build trust that low cost sellers cannot match. TRX has certified more than 300,000 trainers across more than 30 countries, which helps keep its products embedded in commercial and rehabilitation use rather than treated as generic accessories. Rogue Fitness also protects its premium position by tying bands into broader strength packages and athlete centered ecosystems instead of selling them as isolated low priced items[2]Rogue Fitness, “Rogue Fitness – Strength & Conditioning Equipment,” Rogue Fitness, roguefitness.com. Even with those defenses, counterfeit and white label supply still create trust issues that limit pricing power across large parts of the resistance bands market.

Latex Supply and Tariff Volatility Impacting Input Costs

Input cost risk is another clear restraint for the resistance bands market because natural latex remains a large part of production cost for many products. The supply chain is exposed to both raw material concentration in Southeast Asia and trade policy shifts that raise landed costs for finished goods. Teeter reported that the 2025 tariff regime imposed levies of up to 42% on Chinese fitness equipment imports and drove wholesale price increases of 12% to 18% across the sector. York Barbell also cited the National Sporting Goods Association in pointing to tariff driven pressure across home gym equipment categories in 2025. For the resistance bands market, this matters most in clinical and branded channels where material consistency, allergen documentation, and quality assurance cannot easily be compromised. Diversifying production can reduce concentration risk, but the shift often adds complexity and does not remove cost pressure quickly, which leaves margins exposed in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rehabilitation Demand Reshapes the Category Mix

Therapy/Flat Bands are the fastest-growing product type in the resistance bands market, with a 13.98% CAGR projected through 2026 to 2031. Pull-up/Power Bands held 36.15% of the resistance bands market share in 2025, which confirms that assisted calisthenics and strength training still anchor category volume. The product mix is now splitting more clearly between fitness led use and clinically led use, rather than moving in one broad direction. Therapy and flat formats are benefiting from stronger evidence in balance, mobility, and older adult rehabilitation programs. A 2025 randomized controlled trial in Frontiers in Bioengineering and Biotechnology found that a 12 week elastic band program in older women with fall histories improved static balance by 14.2% to 16.2% and reduced Timed Up and Go results by 16.9%, while fear of falling fell by 42.1% when vibration training was added. Those results make therapy formats more relevant in hospital, clinic, and elder care purchasing discussions. This is changing the category from a mostly consumer accessory group into a more segmented set of use cases with clearer clinical value. As that shift continues, the resistance bands market should see stronger pricing and repeat ordering in medically aligned product lines.

Loop and mini bands remain important in the resistance bands market because they fit mobility drills, glute activation routines, and warm up protocols used by studios and trainers. Their role is stable because they solve a very specific use case with little friction for consumers or coaches. Tube and handled bands still matter in home use because the handles make exercises easier for beginners and older users to perform with confidence. Across the resistance bands industry, the commercial value is shifting away from broad SKU expansion and toward sharper specialization by training or treatment need. That favors suppliers that can match a product format to a well defined exercise pathway rather than simply adding more similar items to their catalog. In practical terms, the resistance bands market is rewarding companies that sell a solution for pull up progression, shoulder rehab, or fall reduction, instead of a generic band assortment. This also means premium pricing is more achievable in targeted niches than in the mass consumer shelf where visual differentiation is weak.

By Resistance Level: Medium Anchors Volume While Heavy Tiers Scale

Medium resistance held a 38.19% share in 2025, making it the largest resistance tier in the resistance bands market. That position reflects how broadly medium bands fit therapy routines, beginner fitness progression, and everyday strength work. The tier is also well aligned with color coded resistance systems that clinical buyers already understand, which helps standardize reordering. Germany offers a useful example because TheraBand’s progressive system is distributed through specialist channels that range from clinical suppliers to pharmacy platforms. Bulk roll formats further support volume concentration in this tier because institutions buy long rolls for repeated in facility use rather than single consumer units. This makes medium resistance especially important in the resistance bands market where clinical revenue and consumer revenue overlap. It is the default choice for a wide training population, which gives it better turnover and more predictable replenishment demand than either lighter or very heavy tiers. The result is a segment that anchors volume, even as other resistance levels expand more quickly.

Heavy resistance is the fastest-growing tier, with a 13.52% CAGR projected through 2031. Demand is rising because advanced users want progressive overload options without moving fully into larger equipment categories. Heavy bands are also useful in powerlifting assistance and post injury sports conditioning, where higher tension is necessary for return to performance work. Light bands continue to serve geriatric and post operative users, and extra heavy tiers remain relevant for specialist strength athletes. The important change is not that one tier replaces another, but that buyers increasingly purchase sets across several resistance levels at the same time. This bundled behavior improves average order value and supports better cross sell opportunities for the resistance bands market. It also fits rehabilitation logic, since many programs require progression from one level to the next rather than staying at one tension point. In the resistance bands market, that pattern should keep lifting the value of multi pack offerings for both direct selling brands and institutional distributors. Suppliers that present resistance progression clearly are likely to convert more efficiently than those that rely on vague strength descriptors.

By Material: Latex Dominates, But TPE Gains Structural Ground

Latex retained 51.3% share in 2025, so it remained the leading material base in the resistance bands market. TPE is the fastest-growing material segment, with a 13.25% CAGR projected through 2031. Latex continues to hold scale because it benefits from established processing systems, familiar stretch characteristics, and years of embedded use in therapy protocols. That installed base matters because clinicians often prefer materials with known performance under repeated use. Performance Health has maintained broad clinical reach for TheraBand products, which reinforces the staying power of latex centered solutions in treatment settings. Even so, the resistance bands market is shifting because allergen concerns and procurement requirements make latex free products easier to approve in some institutions. TPE gains are therefore structural rather than cosmetic, since they come from compliance and risk management as much as from user preference. This should keep TPE on a strong growth path even if latex remains the larger revenue base for several years.

Factory economics still favor latex in many consumer formats, but institutional logic is moving in a different direction. TPE products offer allergen free positioning and better resistance to heat and UV exposure, which supports longer usable life in some environments. Fabric and composite products remain the smallest segment, but they are carving out a premium niche in glute activation and comfort led training routines. Certification can also support that niche. Blackroll’s latex free textile composite band carries OEKO TEX Standard 100 certification, which shows how materials compliance can become a selling point and a procurement qualifier at the same time. The resistance bands market is therefore moving toward a two track materials structure, with latex holding its established role in clinical and performance settings, and TPE or fabric formats capturing faster growth in retail and allergen sensitive use. This is one of the clearer examples where the resistance bands market is being shaped by channel requirements rather than pure end user taste. Over time, material choice should reflect the intended buying environment as much as the exercise type.

By End User: Institutional Concentration Meets Consumer-Side Acceleration

Fitness Studios/Gyms held 58.19% of the resistance bands market size in 2025, which shows that commercial buying scale still outweighs household purchases in revenue terms. Large facility orders create much more value than individual consumer baskets, even when unit prices are lower on a per item basis. Commercial operators also use bands across multiple classes, functional zones, mobility stations, and trainer led programs, which raises replacement frequency. TRX’s studio line expansion in 2025 reflected this demand by designing space efficient commercial systems that integrate band based training into facility layouts. That helps explain why the resistance bands market still leans heavily toward institutional revenue even as home training remains visible. Commercial users also prefer branded solutions that can support coaching consistency and safety expectations. This strengthens established suppliers that combine equipment with training frameworks. As a result, the resistance bands market retains a concentrated demand center in facilities even within a fragmented supplier landscape.

Consumer/Home is the fastest-growing end-user category, with a 13.41% CAGR projected through 2031. Growth is being supported by hybrid routines and by the ease of pairing bands with guided digital programs that reduce the need for in person instruction. The consumer channel also benefits from lower trial risk because bands are affordable compared with larger home strength equipment. Physiotherapy and clinical buyers remain highly attractive because they often pay higher prices and place repeat orders under structured procurement cycles. Schools, military programs, and corporate wellness settings still look underpenetrated, but they could become important as compliance friendly and allergen free products widen access. In the Resistance bands industry, this creates a split where gyms anchor current scale, homes deliver the fastest expansion, and clinical use offers the strongest margin profile. The resistance bands market will likely reward suppliers that can serve at least 2 of these channels without confusing the brand message. Those that stay strong in only one channel may face more pressure from either commodity retail sellers or specialist therapy suppliers.

By Distribution: Offline Maintains Scale While Online Channels Accelerate

Offline distribution held 64.3% share in 2025, so physical and specialist procurement routes still dominated the resistance bands market. This leadership is less about walk in consumer shopping and more about how clinics, hospitals, and institutional buyers purchase products. Therapy oriented demand often moves through medical distributors, pharmacy channels, and specialist rehabilitation suppliers rather than broad marketplace listings. TheraBand’s presence across pharmacy and specialist distribution channels in Europe shows how this system remains important for clinically trusted brands[3]ARTZT GmbH, “High Resistance Band Kaufen | TheraBand,” ARTZT GmbH, artzt.eu. Offline therefore retains real scale in the resistance bands market because it is tied to compliance, procurement workflows, and professional recommendation patterns. It also supports product education and repeat ordering in therapy settings where users want established grading systems. That gives offline channels resilience even while consumer discovery shifts online. For many suppliers, maintaining this institutional base is essential to balance the volatility of retail pricing.

Online Marketplaces are the fastest-growing channel, with a 13.92% CAGR projected through 2031. Digital channels are becoming more important because they reduce geographic barriers and let brands reach consumers directly with content, bundles, and subscription offers. The strongest branded strategies use selective marketplace exposure while building owned storefronts that preserve pricing and customer data. REP Fitness showed this direction in 2025 when it announced a direct to consumer launch in the United Kingdom with a dedicated fulfillment facility. The online channel is therefore not just a convenience layer in the resistance bands market. It is also a route to stronger lifetime value when brands control the consumer relationship and attach training services to the sale. Still, online growth comes with more exposure to counterfeits and review driven ranking swings, which means brand protection has become part of channel execution. In the resistance bands market, the best results will likely come from suppliers that combine institutional offline strength with disciplined direct online expansion.

Geography Analysis

North America held 37.16% of the resistance bands market size in 2025, making it the largest regional contributor. The region benefits from a mature blend of hospital and therapy distribution, sports retail, and direct to consumer fitness brands. Performance Health’s TheraBand business has scale across hospitals, clinics, and international partners, which shows how deeply clinical distribution supports regional demand. TRX also expanded its rehabilitation toolkit in 2025 with products and content aimed at physical therapy use, which strengthens North America’s premium channel depth. This makes the resistance bands market in North America less dependent on impulse consumer purchasing than many accessory categories. It also means brands with trusted therapy and training ecosystems can scale faster than sellers competing only on price. Tariff pressure remains a real constraint in the region because higher import levies have raised wholesale costs for fitness equipment categories.

Europe remains the second largest regional block in the resistance bands market, with Germany and the United Kingdom acting as key demand centers. Germany stands out because product grading, specialist distribution, and pharmacy availability support a highly structured therapy environment. That environment favors certified and standardized products over unverified low cost imports. Europe also shows stronger traction for material certification, which supports growth in latex free and textile composite formats. For the resistance bands market, this means the region remains important not only for volume, but also for premium positioning and compliance led purchasing behavior.

Asia-Pacific is the fastest-growing region in the resistance bands market through 2031. Growth is supported by aging demographics in China, rising urban fitness participation in India, and strong strength training adoption in South Korea. The region also benefits from advanced digital commerce behavior, which helps bands reach consumers quickly across densely populated urban centers. At the same time, price competition is more intense, which means branded suppliers need stronger localization and channel control to defend margins. The resistance bands market share pattern is therefore still led by North America today, while Asia-Pacific sets the pace for future expansion because it combines rehabilitation demand, consumer fitness growth, and broad digital reach. Smaller regions such as the Middle East, Africa, and South America remain less significant in size, but they are expanding as premium fitness infrastructure and direct online access improve. That leaves the resistance bands market with a clear geographic balance, where established value sits in North America and Europe, while the strongest forward momentum builds in Asia-Pacific.

Competitive Landscape

The resistance bands market is fragmented at the manufacturing level, with several hundred OEM and ODM producers supplying both private label and branded sellers. This fragmentation is strongest in basic online listings where product differentiation is limited and price visibility is high. A smaller group of branded companies holds stronger positions through clinical trust, digital content, and specialized training use cases. Performance Health, TRX, Rogue Fitness, Serious Steel Fitness, Meglio, and WODFitters are among the names with clearer brand identity in the resistance bands market. Performance Health benefits from entrenched therapy relationships and broad clinical reach, which gives it an advantage in institutional channels. TRX has another kind of strength because its trainer network and app based programming connect the product to ongoing exercise behavior rather than one time hardware use. This gives the resistance bands market a layered structure, where low end supply is crowded, but premium relevance still depends on ecosystem control.

Several strategic moves show how branded players are trying to escape commodity pressure in the resistance bands market. TRX launched new physical therapy and rehabilitation tools in February 2025, including Bandit handle attachments and Rehab to Resilience content, which deepened its role in therapy oriented applications. TRX also announced a global partnership with BlazePod in October 2025 to connect functional strength with cognitive training across commercial, sports, and rehabilitation settings. Performance Health expanded its clinical capability set through a partnership with LiveBand BFR in April 2025, which added blood flow restriction technology to its professional offering. Rogue Fitness has continued to tie bands into broader strength packages and mobility kits, which helps preserve premium pricing by selling a system rather than a standalone elastic product. These moves suggest the next stage of competition in the resistance bands market will center more on program ownership, channel credibility, and training ecosystems than on simple product innovation.

White space remains in institutional procurement and in sensor enabled smart formats, but the near term battle is more basic. Brands need clearer resistance communication, better quality assurance, and stronger proof of use case relevance. That matters because non standardized resistance ratings still slow B2B purchasing and make comparisons harder for professional buyers. Niche specialists have shown that vertical focus works. Serious Steel Fitness is tied closely to pull up progression use cases, while therapy aligned products continue to gain support from peer reviewed evidence in older adult balance and mobility work. In the resistance bands market, that means specialized credibility may be a stronger moat than having the widest assortment. The companies most likely to lead are those that can combine trusted product quality, channel discipline, and training or rehabilitation content in a way that generic suppliers cannot copy easily.

Resistance Bands Industry Leaders

Performance Health (TheraBand)

Black Mountain Products

ProsourceFit

Bodylastics USA Inc.

TRX (Fitness Anywhere LLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: BooyaFit introduced the Booya Band, a user-friendly clip-on resistance band designed to make life easier for fitness professionals, Pilates instructors, and physical therapists during client sessions and classes.

- March 2026: TRX launched the YBell Elite at the Health & Fitness Association (HFA) Show in San Diego, a premium 4-in-1 functional training tool targeting high-performance commercial gym environments, with confirmed adoption at Orangetheory Fitness, Anytime Fitness, F45 Training, and a planned Decathlon Europe rollout. The launch signals TRX's deliberate strategy to deepen commercial gym penetration through multi-functional training ecosystems rather than standalone hardware.

Global Resistance Bands Market Report Scope

As per the scope of the report, resistance bands are elastic bands used for strength training, physical therapy, and exercise. They provide resistance when stretched, helping to build muscle strength, improve flexibility, and enhance workout versatility.

The resistance bands market is segmented by product type, resistance level, material, end user, distribution channel, and geography. By product type, the market includes loop/mini bands, tube/handled bands, therapy/flat bands, pull-up/power bands, and figure-8 bands. By resistance level, it is categorized into light, medium, heavy, and extra heavy. Based on material, the segmentation includes latex, TPE (thermoplastic elastomer), and fabric/composite. By end user, the market is divided into consumer/home, fitness studios/gyms, physiotherapy/clinical, and institutional (schools, military, corporate wellness). By distribution channel, it is segmented into online marketplaces and offline. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Loop/Mini Bands |

| Tube/Handled Bands |

| Therapy/Flat Bands |

| Pull-up/Power Bands |

| Figure-8 Bands |

| Light |

| Medium |

| Heavy |

| Extra Heavy |

| Latex |

| TPE (Thermoplastic Elastomer) |

| Fabric/Composite |

| Consumer/Home |

| Fitness Studios/Gyms |

| Physiotherapy/Clinical |

| Institutional (schools, military, corporate wellness) |

| Online Marketplaces |

| Offline |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Loop/Mini Bands | |

| Tube/Handled Bands | ||

| Therapy/Flat Bands | ||

| Pull-up/Power Bands | ||

| Figure-8 Bands | ||

| By Resistance Level | Light | |

| Medium | ||

| Heavy | ||

| Extra Heavy | ||

| By Material | Latex | |

| TPE (Thermoplastic Elastomer) | ||

| Fabric/Composite | ||

| By End User | Consumer/Home | |

| Fitness Studios/Gyms | ||

| Physiotherapy/Clinical | ||

| Institutional (schools, military, corporate wellness) | ||

| By Distribution | Online Marketplaces | |

| Offline | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in resistance bands demand through 2031?

Growth is being supported by home and hybrid workouts, stronger clinical use in rehabilitation, and wider digital selling models. The category is forecast to rise from USD 2.41 billion in 2026 to USD 4.41 billion by 2031 at a 12.79% CAGR.

Which product type leads sales and which one is growing the fastest?

Pull-up/Power Bands led with 36.15% revenue share in 2025, while Therapy/Flat Bands are projected to post the fastest growth at a 13.98% CAGR through 2031.

Why are therapy and rehabilitation applications becoming more important?

Peer reviewed studies published in 2025 showed measurable gains in balance, mobility, strength, and health markers in older adults using elastic resistance programs, which supports broader clinical adoption.

Which end-user group generates the most revenue today?

Fitness Studios/Gyms generated the largest share at 58.19% in 2025 because commercial facilities buy at scale and use bands across several training zones and class formats.

What are the main risks for branded suppliers?

The biggest risks are counterfeit and commodity competition, tariff and latex cost volatility, and the lack of standardized resistance ratings for institutional buyers.

Which region is expected to expand the fastest?

Asia-Pacific is the fastest-growing region through 2031, while North America remained the largest regional market with a 37.16% share in 2025.

Page last updated on: