Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

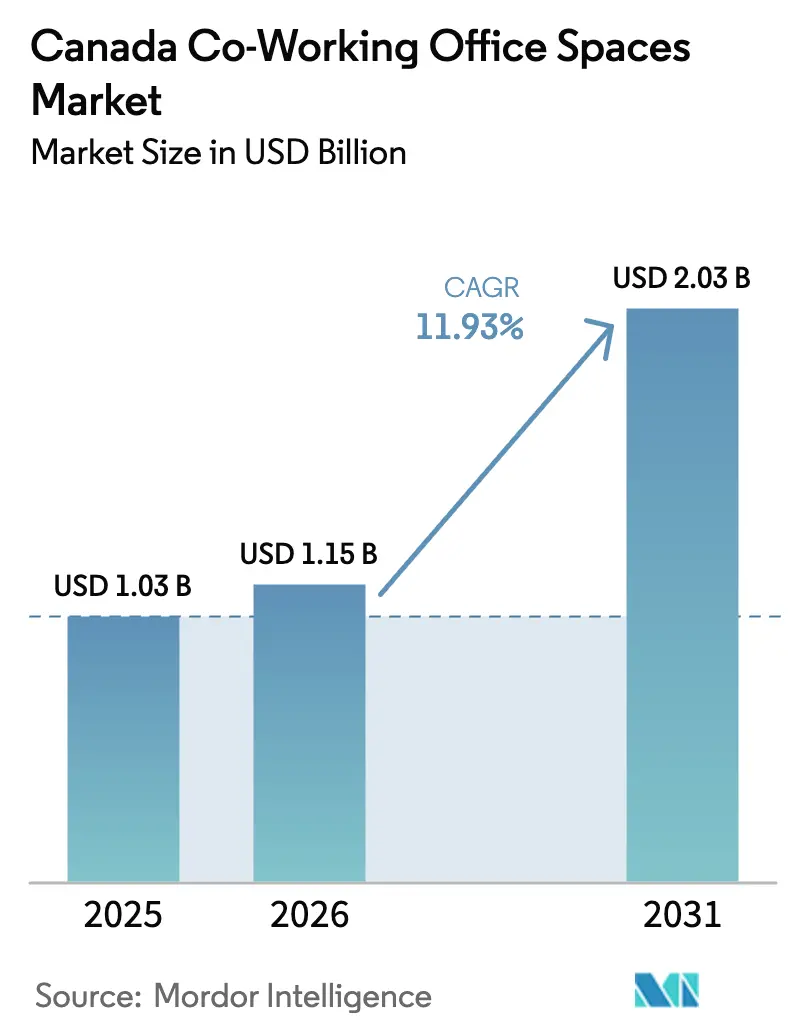

| Base Year Market Size (2025) | USD 1.03 Billion |

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 2.03 Billion |

| Growth Rate (2026 - 2031) | 11.93% CAGR |

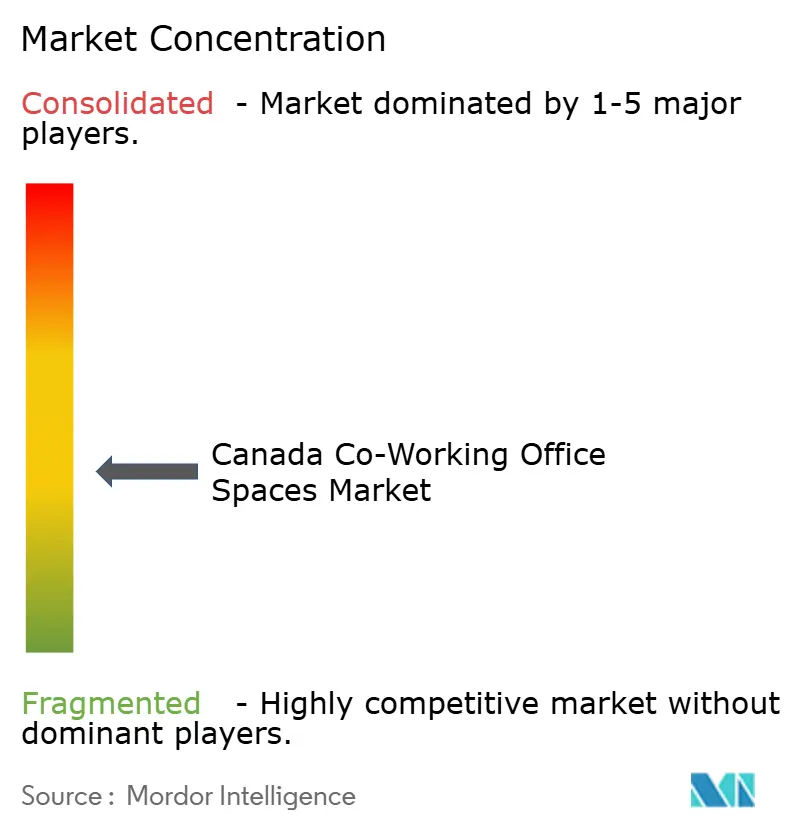

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Coworking Office Spaces Market Analysis by Mordor Intelligence

Canada Coworking Office Spaces Market size in 2026 is estimated at USD 1.15 billion, growing from 2025 value of USD 1.03 billion with 2031 projections showing USD 2.03 billion, growing at 11.93% CAGR over 2026-2031. Steady hybrid work adoption, rising suburban demand, and government innovation funding keep the growth runway open. Domestic operators gain ground as global incumbents retrench, while asset-light partnership models lower capital risk and speed expansion. Operators that blend technology, ESG credentials, and wellness programs enjoy stronger pricing power. Downtown vacancy softness creates favorable leasing terms, yet high rents in prime towers still weigh on margins.

Key Report Takeaways

- By sector, information technology captured 39.85% of the Canada Coworking Office Spaces Market share in 2025; business consulting and professional services are poised for a 13.32% CAGR through 2031.

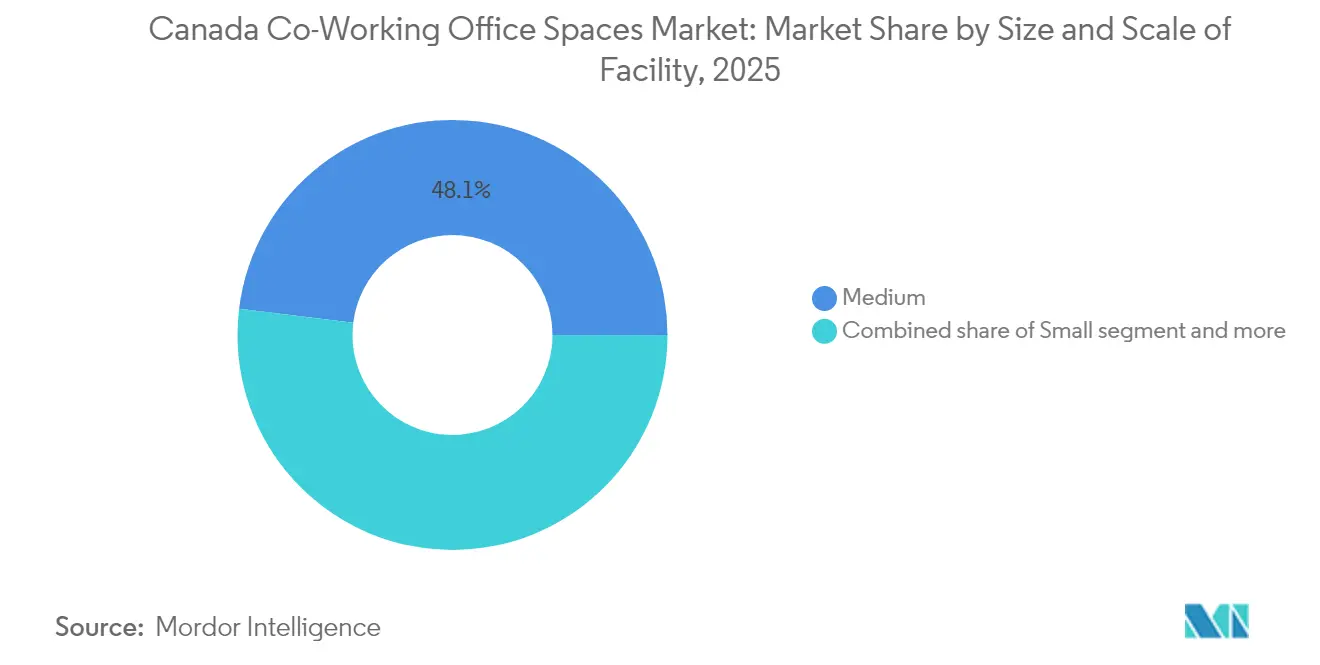

- By facility size, medium locations commanded 48.05% of the Canada Coworking Office Spaces Market size in 2025, whereas small facilities are forecast to climb at a 13.08% CAGR over 2026-2031.

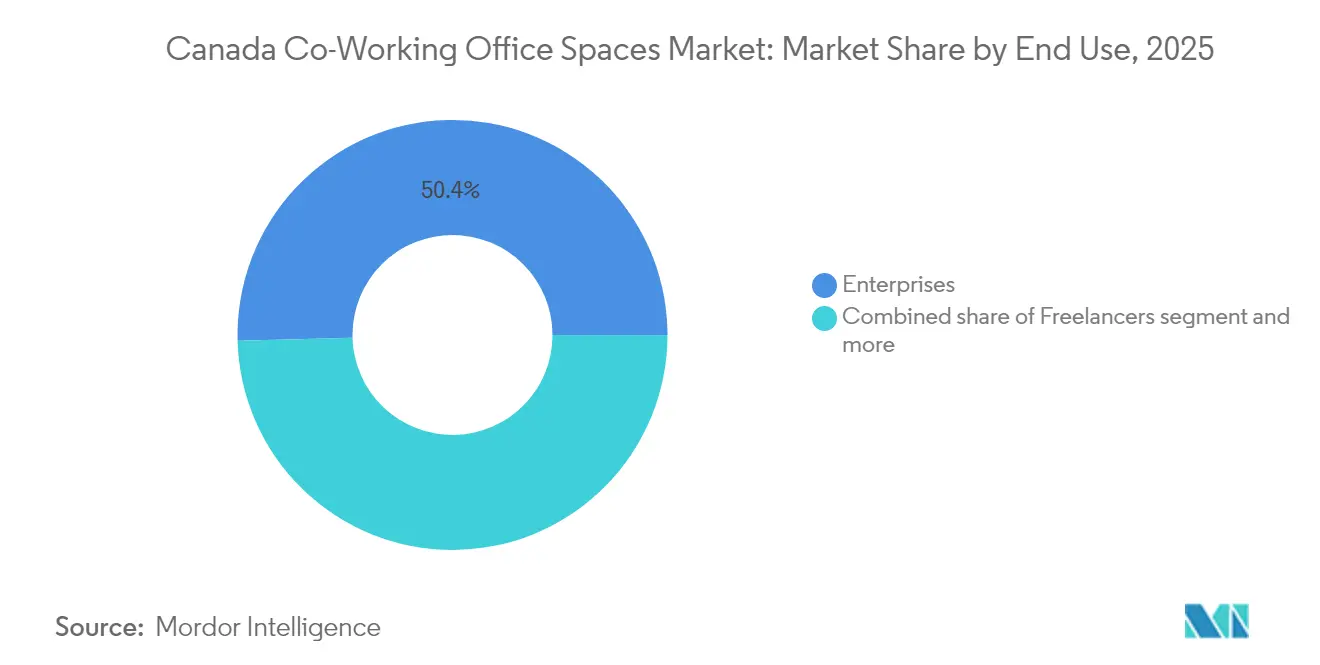

- By end use, enterprises controlled 50.42% revenue share in 2025; the start-ups and others segment is projected to expand at a 13.55% CAGR during the same horizon.

- By province, Ontario led with 47.15% revenue share in 2025, while Alberta is on track for the fastest 13.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Coworking Office Spaces Market Trends and Insights

Drivers Impact Analysis*

| Drivers | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of hybrid and remote work practices | +3.1% | National with Toronto, Vancouver, Montreal focus | Medium term (2-4 years) |

| Preference for suburban centers | +2.2% | GTA, Metro Vancouver, Montreal suburbs | Medium term (2-4 years) |

| Adoption by start-ups, SMEs, and global tech firms | +2.5% | Ontario, Quebec, British Columbia | Short term (≤ 2 years) |

| Government innovation programs and incubators | +1.8% | National innovation hubs | Long term (≥ 4 years) |

| Demand for wellness and sustainability credentials | +1.2% | ESG-mandated urban cores | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Hybrid and Remote Work Practices

Hybrid work is now part of normal business life across Canada. Teleworkers save over an hour daily on commuting and consistently report higher work-life balance, which keeps employers open to flexible models. Federal policy that sets a three-day on-site baseline anchors these arrangements in the public sector and signals acceptance across the broader economy. Work-from-home prevalence stabilized at 18.7% in May 2024, far above the pre-pandemic 7.1% level, showing that the trend has settled rather than reversed. Longer occasional commute distances encourage workers to use well-positioned co-working sites instead of traditional headquarters. Sustained occupier interest therefore lifts demand across the Canada Coworking Office Spaces Market[1]Mona Fortier, “Implementation of a Common Hybrid Work Model,” Treasury Board of Canada Secretariat, tbs.gc.ca.

Government Innovation Programs and Incubators

Federal and provincial agencies deploy billions of dollars to stimulate advanced technologies, and that capital needs a flexible physical home. A USD 200 million artificial-intelligence initiative and a USD 100 million AI Assist program both specify collaboration spaces as critical infrastructure. Ontario’s Grid Modernization Centre, supported by USD 10 million of federal money, provides lab-style space for 120 clean-tech ventures and sets an example for sector-specific co-working hubs. The Business Development Bank of Canada oversees CAD 7 billion (USD 5.25 billion) in venture funds that support early-stage tenants. Public commitments to women- and Indigenous-led businesses amplify inclusive workspace demand. Together, these schemes inject long-cycle growth into the Canada Co-Working Office Spaces industry[2]François-Philippe Champagne, “Departmental Plan 2024-25,” Innovation, Science and Economic Development Canada, ic.gc.ca.

Preference for Suburban Centers

Commuting pain points send more tenants to suburban locations. WeWork’s tie-up with Vast Coworking unlocks 75 suburban sites across North America, including Richmond Hill, to meet that shift. IWG reports that 80% of recent global openings sit outside downtown cores, mirroring Canadian patterns where many residents moved to lower-density areas during the pandemic. Almost 1 in 10 Canadians still face hour-plus commutes, so closer neighborhood options present a valued alternative. Asset-light deals allow operators to retrofit underused retail or Class B assets quickly. This suburban wave supports new revenue streams for the Canada Coworking Office Spaces Market[3]Cathy S. Rozel Farnworth et al., “Flexible Work and Urban Mobility Post-COVID-19,” Journal of Urban Economics, sciencedirect.com.

Demand for Wellness and Sustainability Credentials

Corporate ESG targets reshape space expectations. Tenants seek WELL-rated air systems, biophilic design, and verified carbon reductions. Allied REIT boosted its certified portfolio to 41%, demonstrating landlord willingness to invest where demand exists. National Bank Place aims for LEED v4 Gold and WELL v2 Silver, setting benchmarks that ripple through leasing decisions. Operators that deliver green fit-outs, quiet zones, and mental-health amenities can charge premiums and secure longer memberships. Health-first positioning thus adds an incremental lift to the Canada Coworking Office Spaces Market growth.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High real estate costs in prime cores | -2.3% | Toronto, Vancouver, Montreal CBDs | Short term (≤ 2 years) |

| Economic slowdown risk for start-ups and SMEs | -1.8% | Venture-backed clusters | Short term (≤ 2 years) |

| Concentration in a few metros | -1.4% | Secondary cities nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Real Estate Costs in Prime Cores are Impacting Operator Profitability

Prime city towers still charge top rents even as vacancy tops 18% in downtown Toronto. Operators that rely on showcase addresses, therefore, face tighter margins. Trophy buildings enjoy the lowest vacancy in four years, forcing a hard trade-off between prestige and profit. New supply is thin with only 4.2 million square feet under construction nationwide, so rent relief is unlikely. Cap-ex-heavy projects like Montreal’s USD 1.1 billion National Bank Place highlight barriers that mid-size operators cannot cross. Cost pressure may slow flagship expansion within the Canada Coworking Office Spaces Market.

Market Concentration in a Few Large Metros is Leaving Secondary Cities Underserved

Toronto, Vancouver, and Montreal collect 88% of venture investment, steering most co-working demand to those hubs. Secondary cities lack the density of knowledge workers needed to keep centers at break-even occupancy. Mortgage stress in large urban pockets further chills risk appetite for expansion outside proven areas. Even government-backed innovation centers in towns like Kingston or Thunder Bay cannot always sustain a private operator’s rent roll. The uneven geography limits full national penetration of the Canada Coworking Office Spaces Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size & Scale of Facility: Balanced formats sustain leadership

The medium format led the Canada Coworking Office Spaces Market size in 2025 with 48.05%, as these footprints balance amenities and cost efficiency. Operators can host both project teams and freelancers without major cap-ex. Large sites cater to enterprise clients, but higher fit-out spends and downtown rents limit new openings. In suburban zones, small facilities win share because landlords accept flexible terms and demand thresholds are lower. That formula yields the top 13.08% CAGR forecast for small sites through 2031. IWG’s global model, which places 80% of new openings in neighborhood settings, shows the scalability of smaller footprints within the Canada Coworking Office Spaces Market.

Medium locations remain essential for corporate hybrid programs that rotate staff in staggered patterns. Meeting suites, podcast rooms, and wellness corners fit within 20,000-40,000 sq ft and draw premium day-pass rates. Operators refine smart-building tech to track utilization and right-size services. Small facilities continue to spread toward transit-adjacent suburbs where rent is 30% below downtown averages. This twin-track strategy keeps operator portfolios diverse and cushions cyclical swings.

By Sector: Technology leads while services accelerate

Information technology held a 39.85% share of the Canada Coworking Office Spaces Market in 2025. Start-ups, SaaS vendors, and AI labs value plug-and-play infrastructure, so they rarely lease traditional space at early stages. Government AI grants deepen that pipeline and sustain the segment’s anchor role. Professional services, led by consulting and legal firms, are the fastest climbers at 13.32% CAGR as client proximity outweighs fixed leases. Hybrid engagements require on-demand rooms, driving these firms to membership plans.

Tech remains the innovation magnet that shapes amenity packages, including fiber redundancy and event stages. However, management consultancies and design agencies now occupy entire suites, preferring flexible expansions over five-year contracts. Fintech, life sciences, and clean energy ventures fill out the tenant mix, proving that the Canada Co-Working Office Spaces industry is extending beyond its original tech roots.

By End Use: Enterprises dominate yet start-ups surge

Enterprises accounted for 50.42% of 2025 revenue, reflecting the mainstreaming of co-working for satellite hubs and project squads. Fortune 500 firms sign multi-year deals that underpin cash flow, pushing operators to raise corporate-grade service levels. Start-ups and other small businesses are set for the strongest 13.55% CAGR, aided by accelerator networks and inclusive funding. Freelancers provide baseline demand, keeping occupancy steady even when larger clients churn.

Corporate clients seek sustainability reporting, data security, and campus-like facilities. Operators who certify to WELL or LEED win RFPs. Start-ups remain price sensitive but value community programs and investor meet-ups. The two groups together boost utilization across weekdays and evenings, reinforcing revenue density for the Canada Coworking Office Spaces Market.

Geography Analysis

Ontario anchors the Canada Coworking Office Spaces Market with a 47.15% share thanks to Toronto’s role as a financial and tech powerhouse. Net absorption surpassed 650,000 sq ft in Q3 2024, underscoring demand rebound. Snowflake, BMO, and multiple AI labs chose the region, validating its talent pool. Yet an 18.1% downtown vacancy rate grants operators favorable lease terms for a strategic site. Government-backed Regional Innovation Centers in 17 Ontario cities widen the addressable base beyond the GT.

Alberta is the speed leader with 13.78% CAGR as Calgary’s diversification agenda gains traction. A USD 52.5 million downtown renewal fund entices landlords to convert underused floors into co-working layouts. Energy-to-tech transition projects in Edmonton further spark demand. Quebec leverages Montreal’s bilingual workforce and large-scale builds like National Bank Place to attract enterprises seeking modern, sustainable space. British Columbia benefits from Vancouver’s Pacific trade orientation and a growing number of suburban locations, such as Richmond Hill, that capture hybrid commuters.

Other provinces still trail due to thinner start-up density. However, digital infrastructure grants and remote-first hiring could shift talent west and east over time. Operators that form landlord alliances or public-private partnerships may bridge the gap and bring the Canada Coworking Office Spaces Market to underserved regions.

Competitive Landscape

The market is moderately fragmented. IWG reported record 2023 revenue of GBP 3.3 billion (USD 4.2 billion) through asset-light partnerships with landlords, a model that lowers upfront risk. WeWork shed USD 4 billion in debt during its restructuring and trimmed Canadian sites to core assets, letting local brands like Workhaus expand into vacated floors. Regional players differentiate through curated communities, bilingual staff, or sector-specific labs.

Technology usage is now a key battleground. Workplace K runs occupancy sensors and in-app desk booking that raise utilization and user satisfaction. ESG leadership also matters: operators in LEED-certified buildings capture ESG-minded corporates willing to pay premiums. Suburban growth is the newest arena; nearly half of North American locations now sit outside downtowns, and Canadian operators mirror that pattern. The top five providers together control about 35% of the national supply, leaving room for nimble entrants.

M&A could accelerate as global groups scout for prime portfolios in secondary markets. Joint ventures with developers give operators preferred access to mixed-use sites. As long as landlords face elevated vacancy, revenue-share or management agreements will remain popular growth routes across the Canada Coworking Office Spaces Market.

Canada Coworking Office Spaces Industry Leaders

International Workplace Group plc

WeWork

Staples Studio

Workhaus

IQ Offices

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: YOO and IWG formed a global partnership to launch club-style workplaces that merge premium design with flexible terms across five continents.

- October 2024: WeWork partnered with Vast Coworking Group to access 75 suburban sites, including Richmond Hill, boosting its Coworking Partner Network.

- September 2024: BMO introduced BMO Academy in downtown Toronto, a 500-seat hybrid learning and event hub geared toward blended work models.

- September 2024: National Bank opened National Bank Place in Montreal, the city’s largest office project in three decades, aiming for LEED v4 Gold and WELL v2 Silver ratings.

Canada Coworking Office Spaces Market Report Scope

Co-working spaces refer to working arrangements in which people from different teams and companies come together to work in a single shared space. A co-working space is characterized by shared facilities, services, and tools. Sharing infrastructure in this way helps spread the cost of running an office across members.

The Canada Co-working Office Space Market is segmented by end user (personal user, small-scale company, large-scale company, and other end users), by type (flexible managed office and serviced office), by application (information technology (IT) and information technology (ITES), legal services, BFSI (banking, financial services, and insurance), consulting, and other services), and by geography (Vancouver, Calgary, Ottawa, Toronto, and Rest of Canada). The report offers the market size and forecast in value (USD) for all the above segments.

By Size & Scale of Facility

| Small |

| Medium |

| Large |

By Sector

| Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) |

| Business Consulting & Professional Service |

| Other Services (Retail, Lifesciences, Energy, Legal Services) |

By End Use

| Freelancers |

| Enterprises |

| Start Ups and Others |

By Province

| Ontario |

| Quebec |

| British Columbia |

| Alberta |

| Rest of Canada |

| By Size & Scale of Facility | Small |

| Medium | |

| Large | |

| By Sector | Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) | |

| Business Consulting & Professional Service | |

| Other Services (Retail, Lifesciences, Energy, Legal Services) | |

| By End Use | Freelancers |

| Enterprises | |

| Start Ups and Others | |

| By Province | Ontario |

| Quebec | |

| British Columbia | |

| Alberta | |

| Rest of Canada |

Key Questions Answered in the Report

How large is the Canada Coworking Office Spaces Market in 2026?

It is valued at USD 1.15 billion with a 11.93% CAGR outlook to 2031.

Which province generates the highest demand?

Ontario leads with 47.15% revenue share thanks to Toronto’s finance and tech mix.

What segment grows fastest by facility size?

Small facilities are projected to rise at a 13.08% CAGR through 2031.

Why are suburban co-working centers expanding?

Hybrid workers want shorter commutes, and landlords offer favorable terms outside downtown cores.

Page last updated on: