Refractories Market Size

| Study Period | 2019 - 2029 |

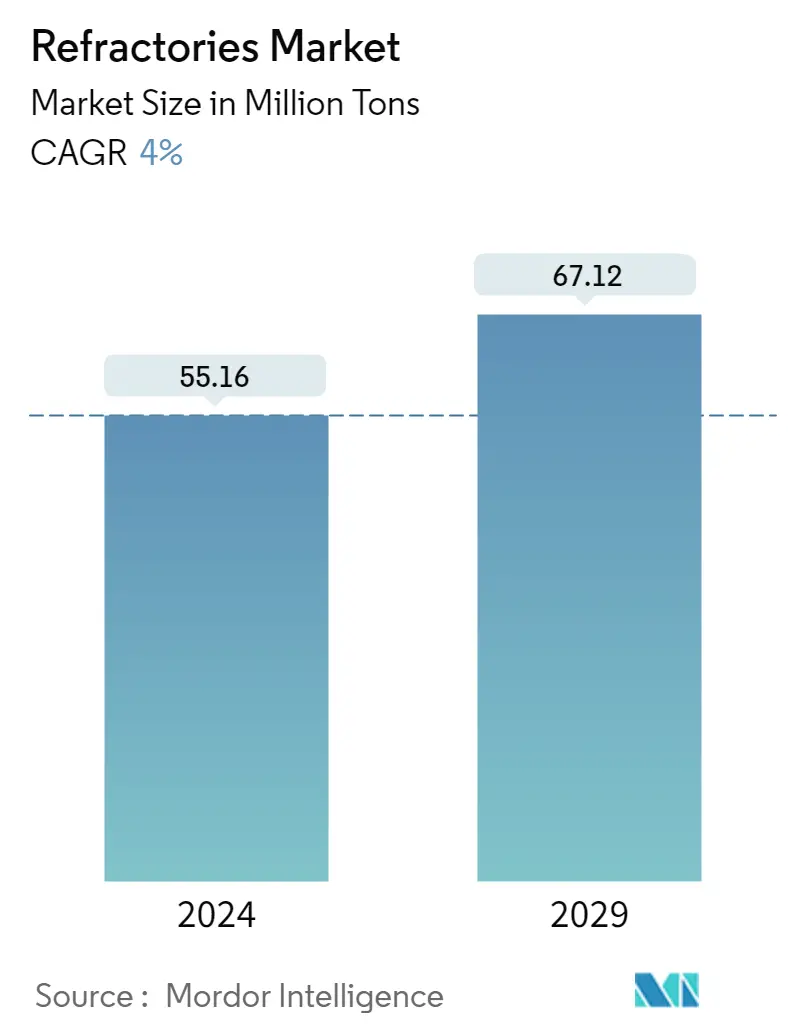

| Market Volume (2024) | 55.16 Million tons |

| Market Volume (2029) | 67.12 Million tons |

| CAGR (2024 - 2029) | 4.00 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Refractories Market Analysis

The Refractories Market size is estimated at 55.16 Million tons in 2024, and is expected to reach 67.12 Million tons by 2029, growing at a CAGR of 4% during the forecast period (2024-2029).

Due to COVID-19, numerous countries were in lockdown, significantly affecting the global economy, and economic and industrial activities were temporarily halted. The refractories market also witnessed a repercussion in production and demand from the end-user industries, such as iron and steel, cement, energy and chemicals, ceramics, etc. Although in the post-pandemic period, the end-user industries are growing because of the growing demand for products after economies open up.

- Over the medium term, the significant factors driving the market studied are the strong growth of iron and steel production in emerging countries and the increased output of non-ferrous materials. The refractories are used for internal lining applications in iron steel and non-ferrous productions.

- Moreover, high demand from the glass industry is the primary factor driving the growth.

- On the flip side, due to increasing environmental awareness, government agencies and environmental agencies worldwide are laying down guidelines regarding the usage and disposal of refractories. It is likely to hinder market growth.

- The growth potential of the Indian steel industry is expected to provide new opportunities for the market studied.

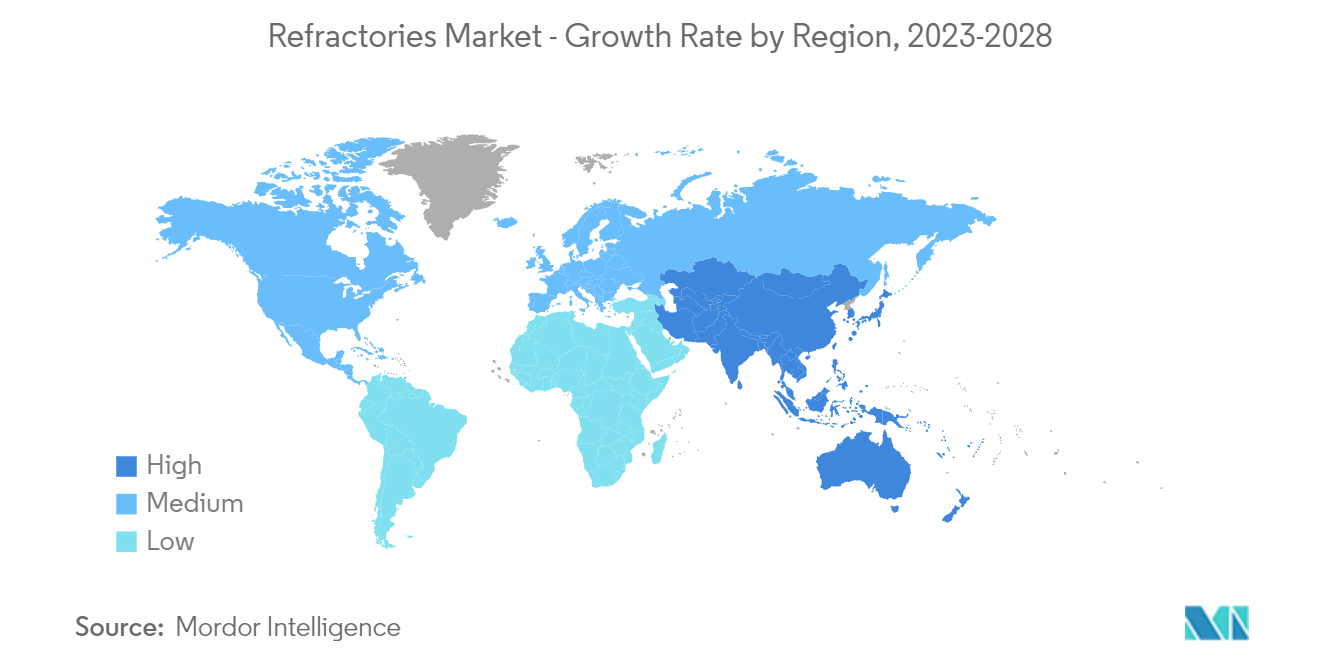

- The Asia-Pacific region will likely dominate the market and register the highest CAGR. Emerging countries like China, Russia, Mexico, and South Africa are investing heavily in large-scale infrastructure projects, which are expected to boost the iron and steel industry's growth significantly.

Refractories Market Trends

Increasing Demand from the Iron and Steel Industry

- The iron and steel industry is the primary end user of refractories, which accounts for around 70% of the market. These materials can withstand high temperatures, ranging from 260°C (500°F) to 1850°C (3400°F), without any significant change in their physical properties.

- The major refractory applications in the iron and steel industry include using internal furnace linings to make iron and steel, in furnaces for heating steel before further processing, in vessels for holding and transporting metal and slag, in the flues or stacks through which hot gases are conducted, and other applications.

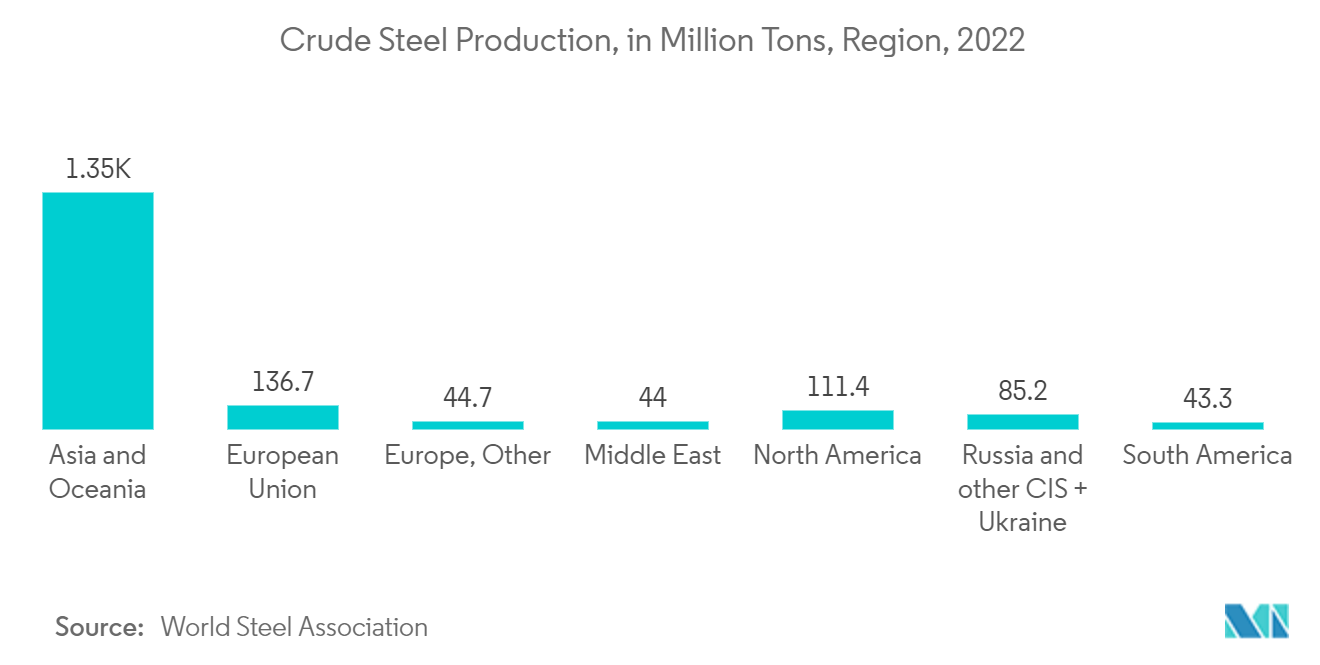

- According to the World Steel Association, the production of crude steel for 63 countries in the month of February 2023 was 142.4 million metric tons (Mt). It indicates the demand prospect prevailing worldwide, which is instrumental in driving steel production activities.

- The top 10 steel-producing countries in the month of February 2023 included China (80.1 Mt), India (10 Mt), Japan (6.9 Mt), the United States (6 Mt), Russia (5.6 Mt), and various others.

- In September 2022, Essar announced its plans to invest USD 4 billion in building and commissioning a four-mtpa steel complex in Saudi Arabia by 2025.

- In the European Union, a mild steel demand recovery continues while improving economic sentiment and investment conditions. However, uncertainties in the political landscape related to the refugee crisis and Brexit are some of the risks to the financial situation. The demand for steel in the region is anticipated to grow slowly over the forecast period.

- All the factors above are expected to drive the global market during the forecast period.

Asia-Pacific region to Dominate the Market

- In the Asia-Pacific region, China is the largest economy and one of the world's largest manufacturing and production industries. China dominates the refractories market in terms of consumption and production owing to the abundant supply of raw materials.

- China is the largest producer of steel in the world. As per the World Steel Association report, China produced around 80.1 Mt (million tons) in February 2023, which is up by 5.6% compared to February 2022. This massive demand for steel in the country projects market opportunities for refractories.

- In India, by FY 2030-31, crude steel actual production in the country is forecasted to reach 255 MT. In Union Budget 2022-23, the Indian government allocated USD 6.2 million to the Ministry of Steel.

- Furthermore, China, under its 14th Five-Year Plan (2021-2025), has set coal-power capacity targets to about 1,100 GW. Thus, the network operator State Grid and the China Electricity Council have targeted plans to develop hundreds of new coal-fired power stations in the country.

- As per the data of the Japan Iron and Steel Federation, the crude steel production in the country reached 89.2 million tons in 2022, compared to 96.3 million tons in 2021.

- Overall, refractory demand in the Asia-Pacific region is expected to grow significantly during the forecast period.

Refractories Industry Overview

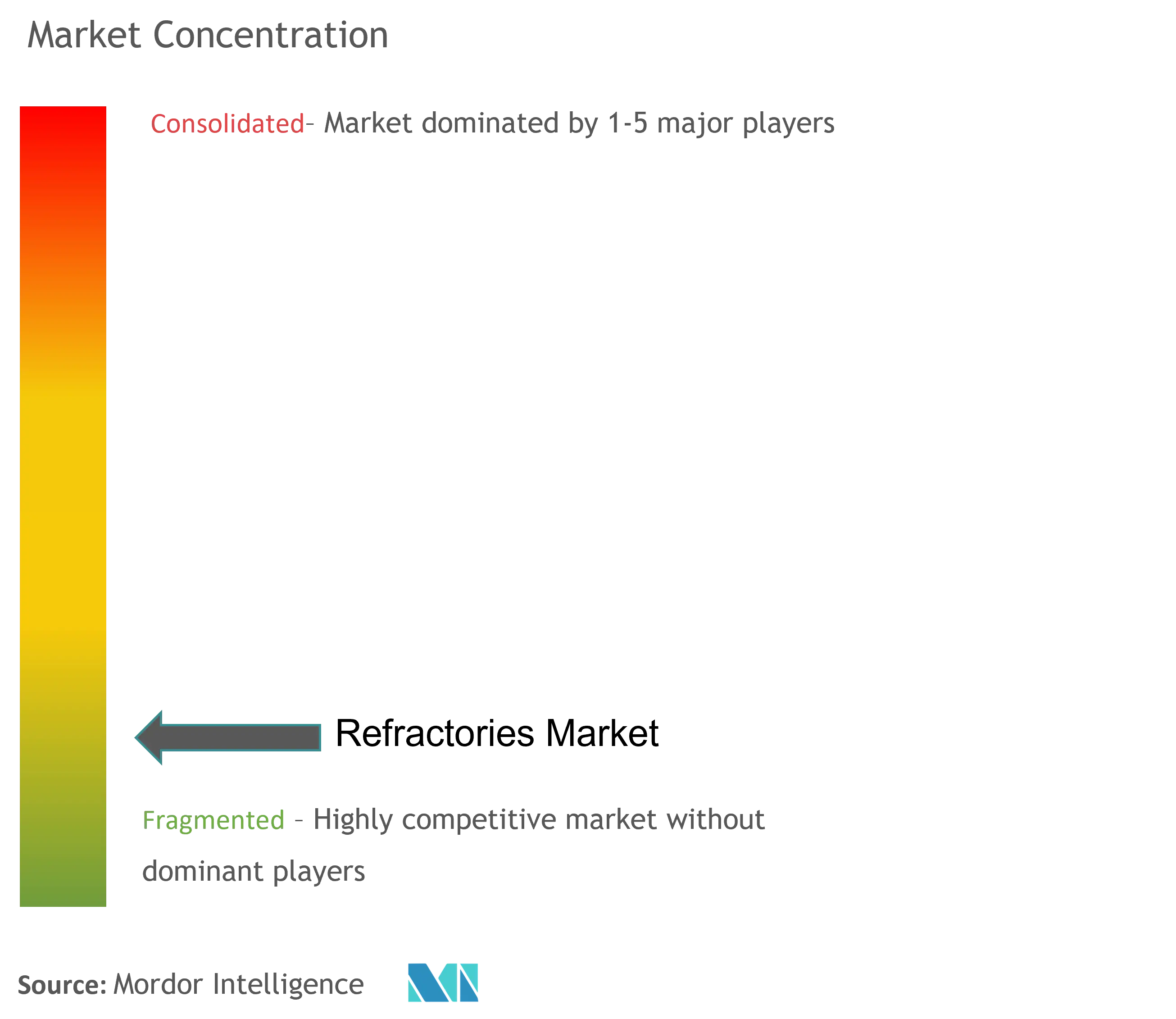

The refractories market stands to be fragmented in nature. The major players (not in any particular order) include RHI Magnesita GmbH, Chosun Refractories ENG Co., Ltd., Krosaki Harima Corporation, Shinagawa Refractories Co., Ltd., and Imerys.

Refractories Market Leaders

RHI Magnesita GmbH

Chosun Refractories ENG Co., Ltd

Krosaki Harima Corporation

Shinagawa Refractories Co., Ltd.

Imerys

*Disclaimer: Major Players sorted in no particular order

Refractories Market News

- January 2023: RHI Magnesita GmbH announced the completion of its acquisition of Dalmia Bharat Refractories Limited's (DBRL) Indian refractory business is expected to add almost 300,000 tons of capacity annually to the existing production footprint in India, enhancing the company's business in the studied market.

- December 2022: Shinagawa Refractories Co. Ltd (Shinagawa) acquired the Brazilian refractory business and alumina-based wear-resistant ceramics business from Compagnie de Saint-Gobain S.A. (Saint-Gobain) in the United States. This acquisition was expected to help the company to enhance its product portfolio in the coming years.

- April 2022: Saint-Gobain acquired Monofrax, based in New York, and a manufacturer of fused cast refractories. This strategic move was expected to strengthen the company's position in the American market.

Refractories Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Drivers

4.1.1 Continuous Usage of Refractories in the Iron and Steel Industry

4.1.2 Increase in the Production of Non-ferrous Metals

4.2 Restraints

4.2.1 Decreasing Production of Refractories in China

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

5.1 Product Type

5.1.1 Non-clay Refractory

5.1.1.1 Magnesite Brick (Dead Burned Magnesia, Fused Magnesia, and Caustic Calcined Magnesia)

5.1.1.2 Zirconia Brick

5.1.1.3 Silica Brick

5.1.1.4 Chromite Brick

5.1.1.5 Other Product Types (Carbides, Silicates)

5.1.2 Clay Refractory

5.1.2.1 High Alumina

5.1.2.2 Fireclay

5.1.2.3 Insulating

5.2 End-user Industry

5.2.1 Iron and Steel

5.2.2 Energy and Chemicals

5.2.3 Non-ferrous Metals

5.2.4 Cement

5.2.5 Ceramic

5.2.6 Glass

5.2.7 Other End-user Industries

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Chosun Refractories

6.4.2 Harbisonwalker International

6.4.3 IFGL Refractories Ltd

6.4.4 Imerys

6.4.5 Intocast AG

6.4.6 Krosaki Harima Corporation

6.4.7 Magnezit Group

6.4.8 Minerals Technologies Inc.

6.4.9 Morgan Advanced Materials

6.4.10 Puyang Refractories Group Co., Ltd

6.4.11 Refratechnik

6.4.12 RHI Magnesita GmbH

6.4.13 Saint-Gobain

6.4.14 Shinagawa Refractories Co. Ltd

6.4.15 Vesuvius

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growing Investments and Research on the Recycling of Refractories

Refractories Industry Segmentation

A refractory material is a material that, at high temperatures, is resistant to decomposition by heat, pressure, or chemical attack and retains strength and form. For their safe, low-maintenance, and cost-effective operations, refractories are used as a primary material for internal linings in large industrial equipment. The refractories market is segmented by product type, end-user industry, and geography (Asia-Pacific, North America, Europe, South America, and Africa). By product type, the market is segmented into non-clay refractories and clay refractories. By end-user industry, the market is segmented into iron and steel, energy and chemicals, non-ferrous metals, cement, ceramics, glass, and others. The report also covers the market size and forecasts for the refractories market in 15 countries across the central regions. For each segment, market sizing and forecasts have been done based on volume (kilo tons).

| Product Type | |||||||

| |||||||

|

| End-user Industry | |

| Iron and Steel | |

| Energy and Chemicals | |

| Non-ferrous Metals | |

| Cement | |

| Ceramic | |

| Glass | |

| Other End-user Industries |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Refractories Market Research FAQs

How big is the Refractories Market?

The Refractories Market size is expected to reach 55.16 million tons in 2024 and grow at a CAGR of 4% to reach 67.12 million tons by 2029.

What is the current Refractories Market size?

In 2024, the Refractories Market size is expected to reach 55.16 million tons.

Who are the key players in Refractories Market?

RHI Magnesita GmbH, Chosun Refractories ENG Co., Ltd, Krosaki Harima Corporation, Shinagawa Refractories Co., Ltd. and Imerys are the major companies operating in the Refractories Market.

Which is the fastest growing region in Refractories Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Refractories Market?

In 2024, the Asia Pacific accounts for the largest market share in Refractories Market.

What years does this Refractories Market cover, and what was the market size in 2023?

In 2023, the Refractories Market size was estimated at 53.04 million tons. The report covers the Refractories Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Refractories Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Refractories Industry Report

Statistics for the 2024 Refractories market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Refractories analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.