Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

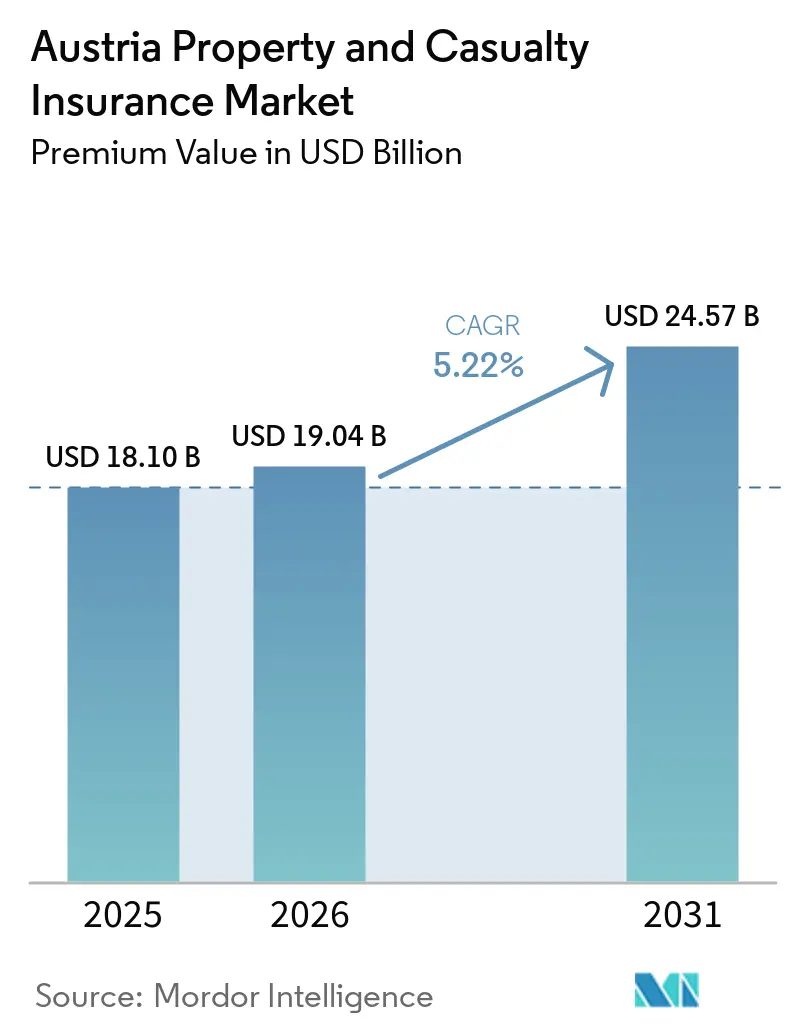

| Base Year Market Size (2025) | USD 18.10 Billion |

| Market Size (2026) | USD 19.04 Billion |

| Market Size (2031) | USD 24.57 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

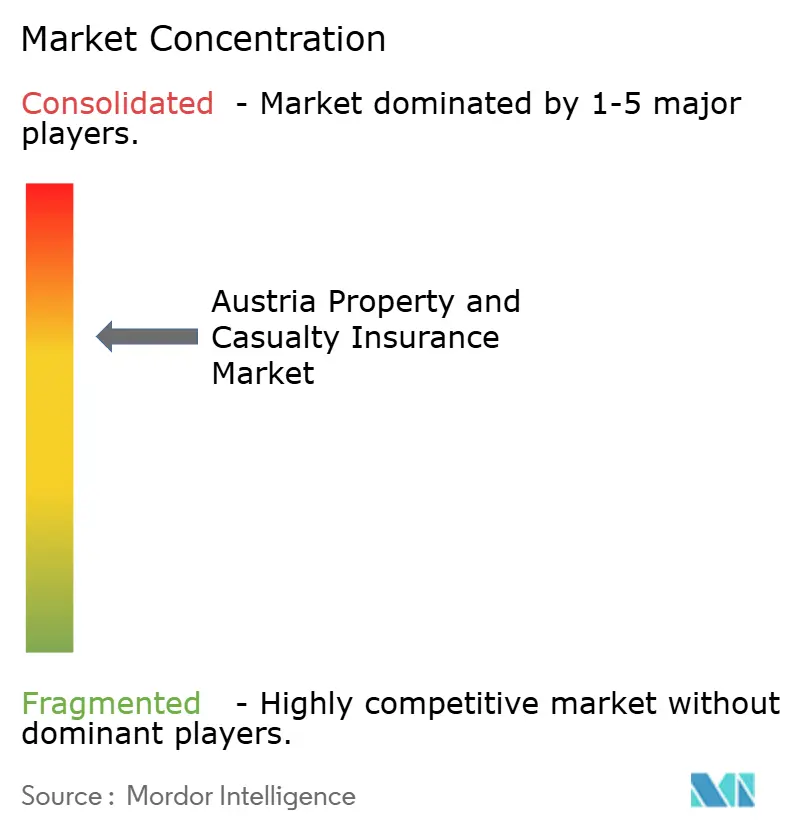

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Property and Casualty Insurance Market Analysis by Mordor Intelligence

The Austria Property And Casualty Insurance Market size in terms of premium value is expected to grow from USD 18.10 billion in 2025 to USD 19.04 billion in 2026 and is forecast to reach USD 24.57 billion by 2031 at 5.22% CAGR over 2026-2031.

However, the growth rate defies the Austrian National Bank’s forecast of –0.1% real GDP growth and 2.9% inflation in 2025. Three structural forces propel growth. First, reconstruction after the September 2024 Central European floods produced EUR 550–650 million (USD 594–702 million) in domestic losses and pushed the federal disaster fund to EUR 1 billion (USD 1.08 billion). Second, motor insurers are repricing as cost-inflation collides with a EUR 35 (USD 38) annual tax on newly registered cars, while battery-electric vehicles remain exempt. Third, digital and bancassurance channels are ramping at double-digit rates, mirroring wider European adoption. Heightened climate risk, EU sustainability mandates, and the Digital Operational Resilience Act are pressuring players to innovate, even as low reinvestment yields and aggregator-led price competition weigh on margins. Therefore, the Austria property and casualty insurance market balances macro headwinds with product and channel tailwinds.

Key Report Takeaways

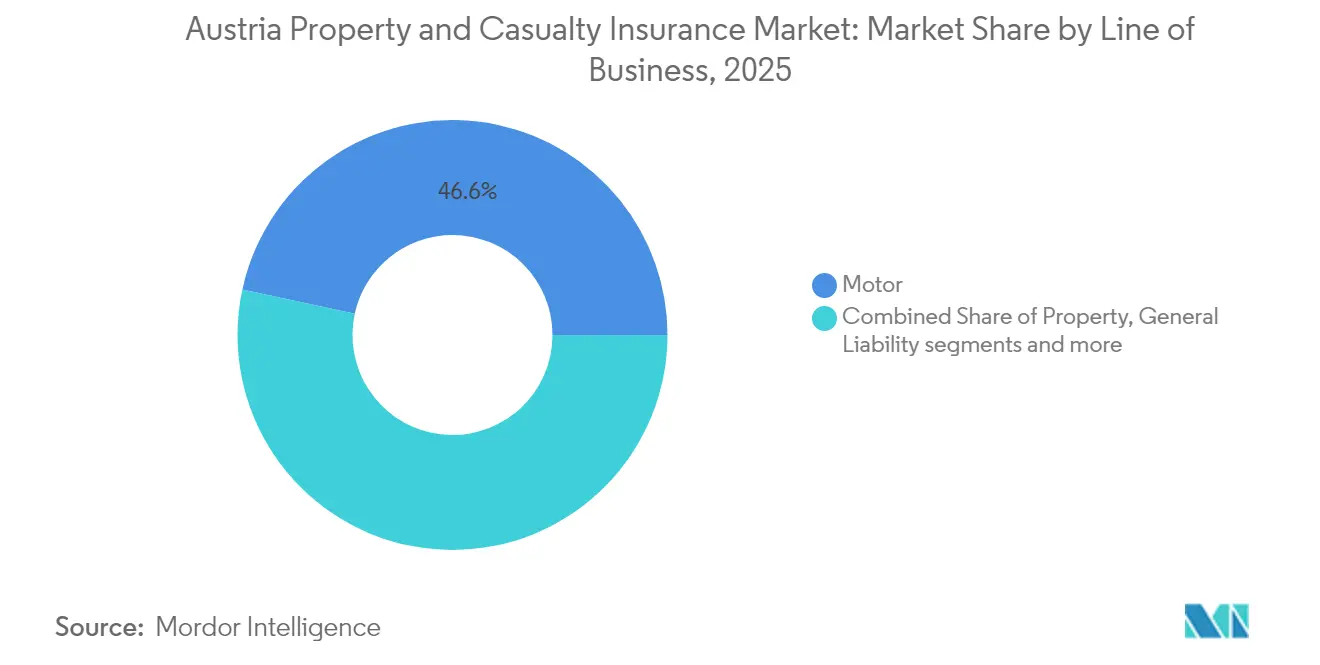

- By line of business, motor retained leadership with 46.60% of the Austria property and casualty insurance market share in 2025, while commercial property is projected to expand at a 6.63% CAGR to 2031.

- By customer type, individual policyholders held 62.40% revenue share in 2025; small and medium enterprises are advancing at a 6.11% CAGR through 2031.

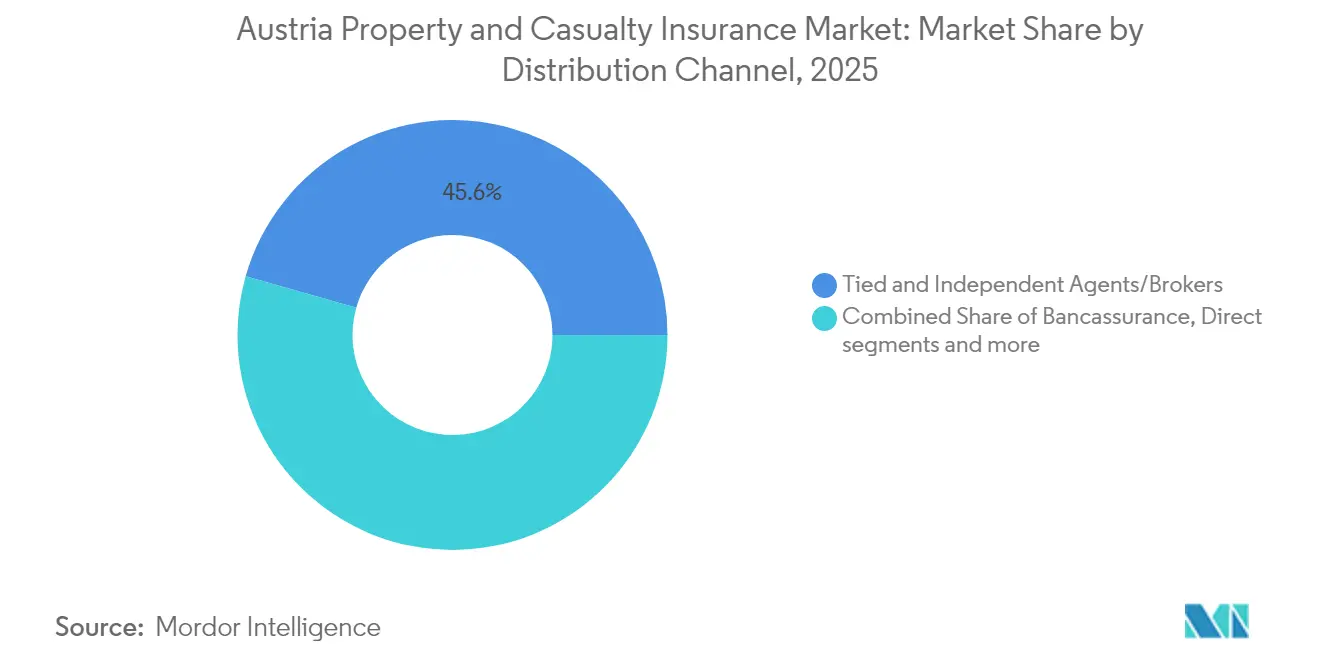

- By distribution channel, agents and brokers accounted for 45.60% of the 2025 premium; digital and online aggregators are scaling at an 11.05% CAGR to 2031.

- By region, Vienna commanded 31.85% of the Austria property and casualty insurance market size in 2025, while Vorarlberg is growing at a market-leading 7.25% CAGR.

- Vienna Insurance Group and UNIQA together controlled more than half of the direct premium in 2024, underscoring a moderately concentrated competitive landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Austria Property and Casualty Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened NatCat exposure raises property cover demand | +1.2% | Nationwide, focused on Lower Austria & Vienna | Short term (≤ 2 years) |

| Inflation-driven motor repair costs push premium growth | +0.9% | Nationwide, urban focus | Medium term (2–4 years) |

| Digital & bancassurance channels widen market reach | +0.7% | Nationwide, gains in Vienna, Salzburg, Tyrol | Medium term (2–4 years) |

| EU “Green Deal” renovation wave lifts property lines | +0.8% | Nationwide, emphasis on Vienna, Upper Austria, Styria | Long term (≥ 4 years) |

| Corporate-sustainability rules boost liability demand | +0.5% | Nationwide, corporate clusters in Vienna, Upper Austria | Long term (≥ 4 years) |

| E-mobility surge creates EV-specific insurance niches | +0.4% | Nationwide, early adoption in Vienna, Salzburg, Vorarlberg | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Heightened NatCat Exposure Raises Property Cover Demand

The 2024 flood catastrophe exposed vulnerabilities, with nearly 5,000 emergency responses in Lower Austria and rainfall intensity up 15% over four decades according to a recent Nature study[1]Nature Editorial Team, “Rising Extremes in Central Europe,” nature.com . The disaster fund increase to EUR 1 billion (USD 1.08 billion) confirms official acceptance that post-event compensation is insufficient. Insurers are recalibrating risk-based pricing, lobbying for compulsory natural catastrophe schemes, and introducing parametric flood solutions. The Austrian Institute of Economic Research argues that mandatory cover would spread risk more equitably and deepen the Austria property and casualty insurance market.

Inflation-Driven Motor Repair Costs Push Premium Growth

Modern vehicles embed expensive sensors and driver-assistance systems that elevate claim severity. The Austrian Automobile Club notes a EUR 35 (USD 38) annual tax on new registrations from 2025, while the inflation outlook pushes parts costs higher. UNIQA’s 2024 report shows motor premiums growing faster than exposure, illustrating pricing power despite cost pressure[2]UNIQA Group, “Annual Report 2024,” uniqagroup.com . Electric-vehicle uptake introduces battery-replacement risk that can exceed EUR 10,000 (USD 10,800), prompting insurers to launch BEV-specific wordings.

Digital & Bancassurance Channels Widen Market Reach

EIOPA finds that online channels already capture 20% of new European motor policies, and Austria is trending similarly [3]European Insurance and Occupational Pensions Authority, “Digitalisation Market Report 2024,” eiopa.europa.eu. Erste Group’s loan recovery fuels cross-sell potential, while UNIQA’s FRISS analytics cut USD 21 million in fraud losses and improve claims turnaround. Digital Operational Resilience Act compliance is catalyzing end-to-end process upgrades, enabling straight-through underwriting that enhances customer experience and lowers cost ratios.

EU “Green Deal” Building-Renovation Wave Lifts Property Lines

Directive 2024/1275 sets zero-emission targets by 2050, while Austria’s housing law allocates EUR 1 billion (USD 1.08 billion) in subsidies for 2024-2026 with photovoltaic integration[4]Austrian Parliament, “Housing Subsidy Act 2024,” parlament.gv.at. Renovations raise sums insured and create demand for coverage of heat pumps, rooftop solar, and digital monitoring systems. Liability exposure for energy-performance assessors drives professional indemnity demand, widening the Austria property and casualty insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent low reinvestment yields squeeze underwriting margins | –0.8% | Nationwide | Medium term (2–4 years) |

| Intensifying price competition via online aggregators | –0.6% | Nationwide, urban centers | Short term (≤ 2 years) |

| Stricter Solvency II and IFRS 17 capital requirements | –0.4% | Nationwide | Medium term (2–4 years) |

| Social-inflation litigation elevates claims severity | –0.3% | Nationwide, especially Vienna | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Low Reinvestment Yields Squeeze Underwriting Margins

Even as the European Central Bank tightens its monetary policy, insurers find their portfolio reinvestment rates stuck below 2%. This limitation on investment income tightens underwriting margins, particularly in years marked by significant natural catastrophe (NatCat) losses. A case in point is UNIQA, which reported a 2024 combined ratio of 93.6%, leaving scant room for fluctuations. In a bid to counteract the pressure on yields, insurers are increasingly gravitating towards alternative assets, such as infrastructure debt and green bonds. Yet, these alternatives come with heightened credit risks and impose extra capital charges under Solvency II, further straining the financial landscape.

Intensifying Price Competition Via Online Aggregators

Aggregator platforms are reshaping high-volume sectors, such as motor and household insurance, where price now reigns supreme in consumer choices. This shift exerts heightened margin pressures on insurers, propelling them into a relentless downward spiral. In 2023, the Austrian Federal Competition Authority underscored its commitment to pro-competition policies by levying fines totaling €51.2 million (USD 55.3 million). Consequently, smaller intermediaries grapple with an escalating threat of disintermediation, catalyzing a swift consolidation across distribution channels and diminishing the clout of traditional agents in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Line of Business: Commercial Property Surges As Motor Retains Scale

Commercial property premiums are tracking a 6.63% CAGR, lifted by EU renovation finance, while motor retains 46.60% of the Austria property and casualty insurance market share. Inflation-linked tariff reviews buttress motor revenue, whereas construction activity, flood awareness, and photovoltaic installations sustain property demand. Solar installations require cover for inverter failure and fire risk, expanding ancillary endorsements. Accident and health non-life lines grow steadily as aging demographics raise personal accident add-ons. Marine, aviation, and transport covers benefit from Austria’s logistics hub status.

Commercial property’s share of the Austria property and casualty insurance market size is projected to reach 12.88% by 2031. Renovation passports mandated by Directive 2024/1275 introduce professional indemnity exposure, and insurers offer combined contractor all-risks and delay-in-start-up solutions. Parametric triggers for rainfall and river level are bundled with traditional indemnity to shorten claims cycle times.

By Customer Type: SME Momentum Narrows Gap With Individuals

Individual policyholders still drive 62.40% of the 2025 premium, anchored by mandatory MTPL, household, and private liability lines. SME premium, however, is expanding at 6.11% CAGR, supported by EU digital and green investment that demands cyber and environmental liability cover. Large corporations face higher disclosure risk, prompting limits increases on environmental impairment liability, while the public sector leverages the EUR 1 billion (USD 1.08 billion) disaster fund to co-insure municipal infrastructure.

UNIQA’s SME-focused digital portal cuts quotation time to minutes, demonstrating that digital service quality can trump price alone. Bancassurance partners use transaction data to pre-fill proposals, boosting conversion rates in both SME and retail segments.

By Distribution Channel: Digital Velocity Outpaces Legacy Reach

Agents and brokers write 45.60% of premium, but online aggregators grow at 11.05% CAGR and are forecast to surpass 15% share by 2031. Bancassurance benefits from Erste Group’s mortgage rebound; loan onboarding funnels property policy offers with embedded climate-risk scoring. Direct writer call centers remain essential for complex commercial risks, but integrate video-adjusting for faster claims assessment.

The Austria property and casualty insurance market relies increasingly on API-enabled exchanges that support real-time quotation. VIG’s broker cockpit integrates policy lifecycle tasks, enhancing agent productivity and reinforcing its leading position. Aggregator pressure forces carriers to sharpen underwriting segmentation and refine risk-based pricing.

Geography Analysis

Vienna dominates the Austria property and casualty insurance market. Its role as a regulatory and corporate hub anchors demand across property, liability, and specialty lines. Dense urban infrastructure results in high insured values, and the city hosts a cluster of InsurTech start-ups offering embedded and parametric products. Regulatory proximity accelerates pilot approvals for new wordings.

Vorarlberg writes the lowest in premiums yet grows fastest. Cross-border commuters buy combined Austria-Swiss liability covers, while SMEs seek multi-jurisdictional cyber protection. Tailored usage-based fleet covers price kilometers driven in both euro and Swiss franc revenue zones.

Upper Austria and Styria contribute a significant share in premiums, with heavy industry upgrading to meet decarbonization targets. Insurers design wrap-around covers combining construction all-risks, delay-in-start-up, and performance guarantees for heat-pump and solar installations, reinforcing the Austria property and casualty insurance market.

Tyrol and Salzburg contribute moderately to the premium share, focused on hospitality, ski-resort liability, and Alpine rescue. Seasonal volatility prompts parametric snow-deficit triggers. Carinthia and Burgenland write USD 1.00 billion, with rural broadband and green building grants supporting targeted insurance demand. The EUR 1 billion (USD 1.08 billion) disaster fund equalizes provincial NatCat exposure.

Competitive Landscape

The Austria property and casualty insurance market is moderately concentrated. Vienna Insurance Group (VIG) and UNIQA hold more than half of the premium, while Allianz, Generali, and Zurich are further, putting the top five shares near three-fourths of the market.

Generali’s active presence in property and casualty insurance lines enables it to cross-subsidize Austrian innovation. Allianz pilots telematics-based pay-how-you-drive tariffs, while Zurich focuses on multinational program issuance aligned with EU disclosure rules. Regional mutuals such as Oberösterreichische Versicherung rely on local claims servicing, but aggregator pressure challenges their rate adequacy.

Technology is the competitive frontier. UNIQA’s FRISS deployment saved USD 21 million in fraud over two years and won a Celent award. VIG’s broker cockpit integrates first-notice-of-loss, policy issuance, and analytics, increasing agent sales productivity. Smaller carriers without digital budgets partner with InsurTechs for white-label products. KPMG warns that the Sanktionengesetz 2024 will raise compliance overhead, likely accelerating mergers.

White-space opportunities include battery warranty covers, parametric flood protection, and ESG-linked performance guarantees. The Austria property and casualty insurance industry is thus innovating within a concentrated but dynamic landscape.

Austria Property and Casualty Insurance Industry Leaders

Vienna Insurance Group (Wiener Städtische)

UNIQA Insurance Group

Allianz Österreich

Generali Versicherung

Zurich Österreich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: UNIQA joined the Eurapco Alliance, linking carriers that write EUR 48.5 billion (USD 52.4 billion) annually.

- February 2025: Austria enacted the Sanktionengesetz 2024, extending sanctions checks to insurers from January 2026

- December 2024: Government housing program earmarked EUR 1 billion (USD 1.08 billion) for affordable construction and renovation

- May 2024: EU adopted Directive 2024/1275 mandating zero-emission buildings by 2050. The EU “Green Deal” building-renovation wave is expected to lift Property lines

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Austria's property & casualty (P&C) insurance market as all gross written premiums from non-life covers that protect physical assets, motor vehicles, liability exposures, and accident & supplemental health risks written by licensed insurers in the country. The baseline therefore pools motor, property, general liability, accident-health (non-life), marine, aviation, and transport as reported to the Financial Market Authority (FMA).

Scope exclusion: reinsurance cessions, life, pension, and purely health-fund products are left outside the model.

Segmentation Overview

- By Line of Business

- Motor

- MTPL

- Casco

- Property- Residential

- Property- Commercial & Industrial

- General Liability

- Accident & Health (non-life)

- Marine, Aviation & Transport

- Motor

- By Customer Type

- Individuals / Personal Lines

- Small & Medium Enterprises

- Large Corporates

- Public Sector

- By Distribution Channel

- Tied & Independent Agents / Brokers

- Bancassurance

- Direct (Branch & Call-centre)

- Digital / Online Aggregators

- Affinity & Partnership Programmes

- By Region

- Vienna

- Lower Austria

- Upper Austria

- Styria

- Tyrol

- Salzburg

- Carinthia

- Vorarlberg

- Burgenland

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with underwriting managers, broker federations, and actuarial consultants across Vienna, Graz, and Innsbruck, followed by buyer surveys among SME fleet owners and household policyholders. These dialogues clarified tariff movements, digital uptake rates, and catastrophe loss assumptions that secondary data alone could not capture.

Desk Research

We collected foundational data from FMA annual reports, Statistics Austria premium series, the Austrian Insurance Association, Eurostat macro releases, and peer-reviewed climate-risk journals. Company filings, Vienna Stock Exchange disclosures, and reputable business media enriched competitive insights. To size channel flows and claims inflation, our analysts also extracted headline ratios from D&B Hoovers, Dow Jones Factiva, and Questel patent analytics for insurtech activity. The sources cited illustrate the breadth; many additional public records were consulted for corroboration.

Market-Sizing & Forecasting

A top-down build starts with FMA gross premiums, which are then split by line, channel, and region using penetration-rate patterns from household dwelling stock, registered vehicle counts, SME census data, claims frequency, and NatCat loss ratios. Select bottom-up checks, median motor premium × vehicle parc or landlord cover × rental stock, validate segment totals before adjustments. Key model drivers include new-car registrations, construction output index, consumer CPI for vehicle repair, insured NatCat loss trend, digital policy issuance, and GDP at current prices. Five-year forecasts combine ARIMA projections for macro indicators with expert-benchmarked scenario analysis for climate events.

Data Validation & Update Cycle

Outputs move through variance checks against independent premium pools, peer ranges, and prior-year loss ratios. Senior reviewers query anomalies, and figures are refreshed each year, with interim updates triggered by material events (e.g. flood losses or regulatory shifts) before final client release.

Why Mordor's Austria Property & Casualty Insurance Baseline Earns Decision-Makers' Trust

Published estimates often diverge. Differences usually spring from what risks are counted, whether accident-health sits inside P&C, and if numbers are stated in net or gross terms.

Key gap drivers here are scope breadth, currency conversion year, and update cadence. Several external studies focus only on motor and property, exclude accident-health, and freeze exchange rates at 2023 levels, whereas our team reports the full non-life basket in 2025 euros converted to constant-year dollars.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.10 bn (2025) | Mordor Intelligence | - |

| USD 5.60 bn (2024) | Global Consultancy A | Narrow scope omits accident-health; no inflation adjustment. |

| USD 5.37 bn (2024) | Industry Journal B | Uses net premiums; excludes brokered affinity covers; older exchange rate. |

The comparison shows that when full-scope premiums, fresh macrodeflators, and blended validation are applied, Mordor's balanced baseline stands as the most dependable starting point for strategy, pricing, and capital-allocation decisions.

Key Questions Answered in the Report

What is the current value of the Austria property and casualty insurance market?

The Austria property and casualty insurance market stands at USD 19.04 billion in 2026 and is projected to reach USD 24.57 billion by 2031, growing at a 5.22% CAGR.

Which line of business is expanding fastest?

Commercial property is growing at a 6.63% CAGR, driven by EU renovation mandates and heightened flood awareness.

How significant are digital channels?

Agents and brokers currently write 45.60% of premium, but online aggregators are growing at 11.05% CAGR and are expected to pass 15% share by 2031

Why are motor premiums increasing?

Inflation-driven repair costs, a EUR 35 (USD 38) tax on new cars, and expensive electronic parts are pushing premiums upward, while BEVs remain tax-exempt.

Page last updated on: