Market Overview

| Study Period | 2020 - 2031 |

|---|---|

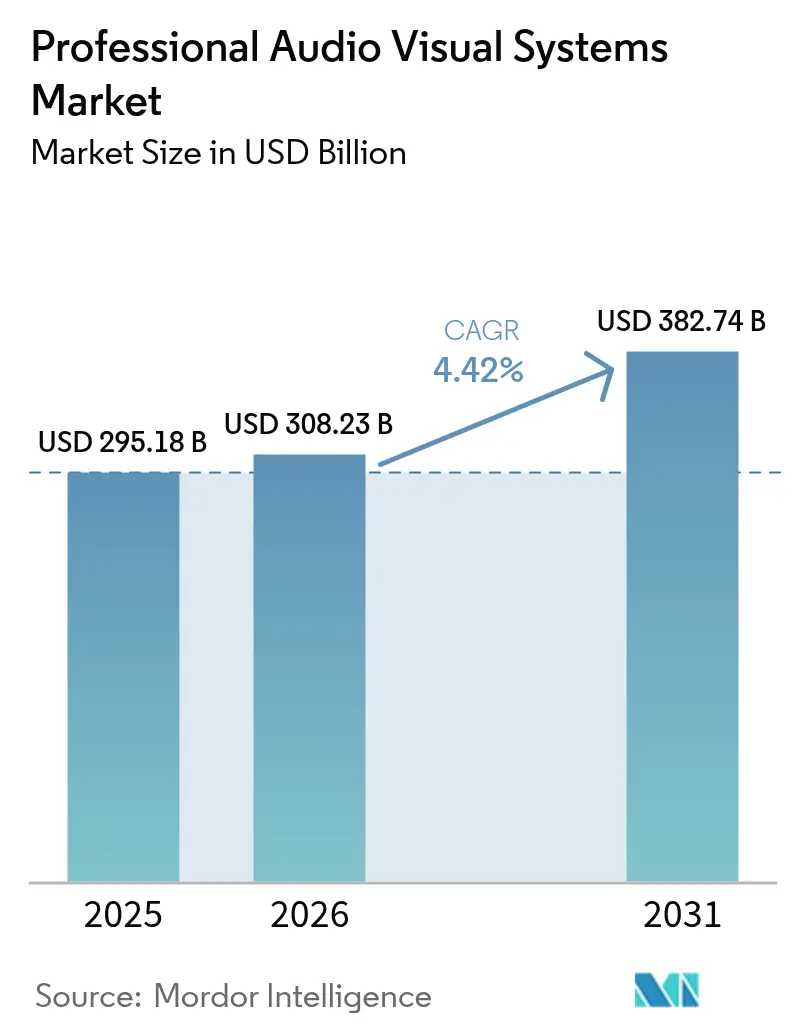

| Market Size (2026) | USD 308.23 Billion |

| Market Size (2031) | USD 382.74 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

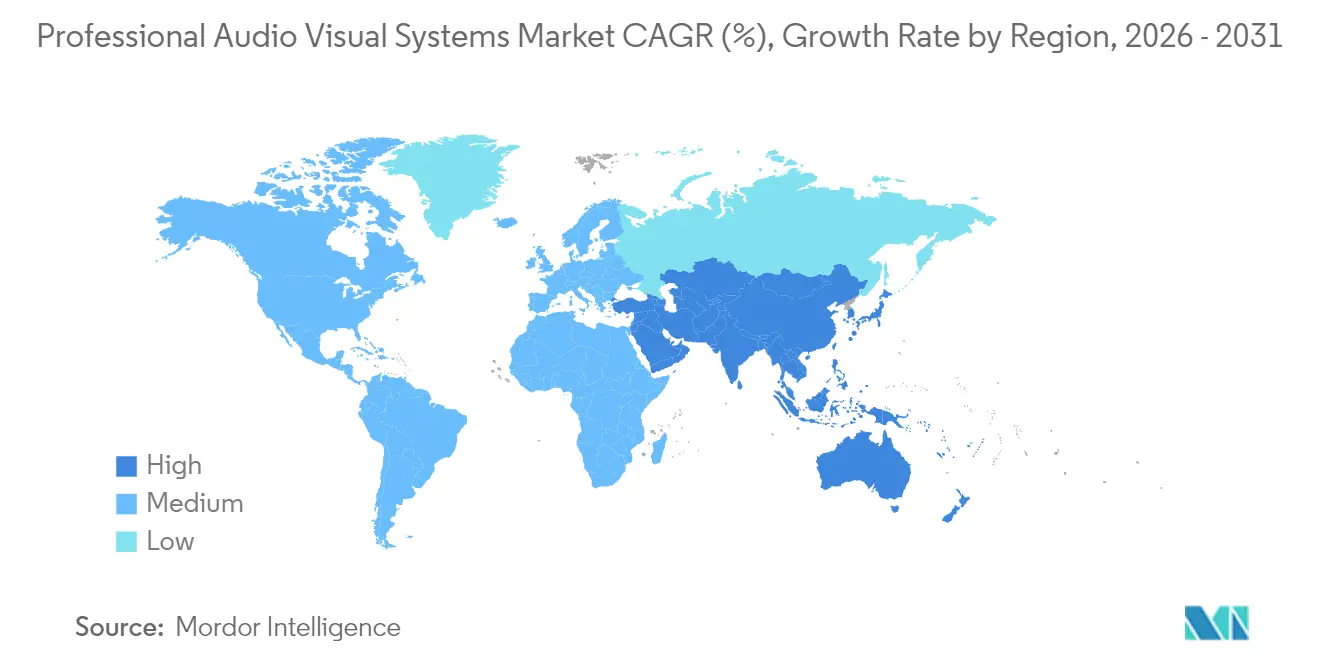

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Professional Audio Visual Systems Market Analysis by Mordor Intelligence

The professional audio visual system market size was valued at USD 295.18 billion in 2025 and estimated to grow from USD 308.23 billion in 2026 to reach USD 382.74 billion by 2031, at a CAGR of 4.42% during the forecast period (2026-2031). Hybrid work requirements, investment in digital signage, and the migration of AV processing to cloud and IP networks drive demand resilience. Spending momentum is visible in enterprise collaboration suites, large-format LED displays, and AI-enabled audio that supports inclusive meetings. Vendor competition is intensifying as software-centric newcomers challenge traditional integrators with subscription models and remote device management. Supply-chain pressures related to semiconductors remain a headwind, yet regulatory mandates on accessibility and energy efficiency are opening new revenue avenues for compliance-ready platforms.

Key Report Takeaways

- By geography, Asia-Pacific led with 29.55% professional audio visual system market share in 2025, while the region is also forecast to post a 5.78% CAGR to 2031.

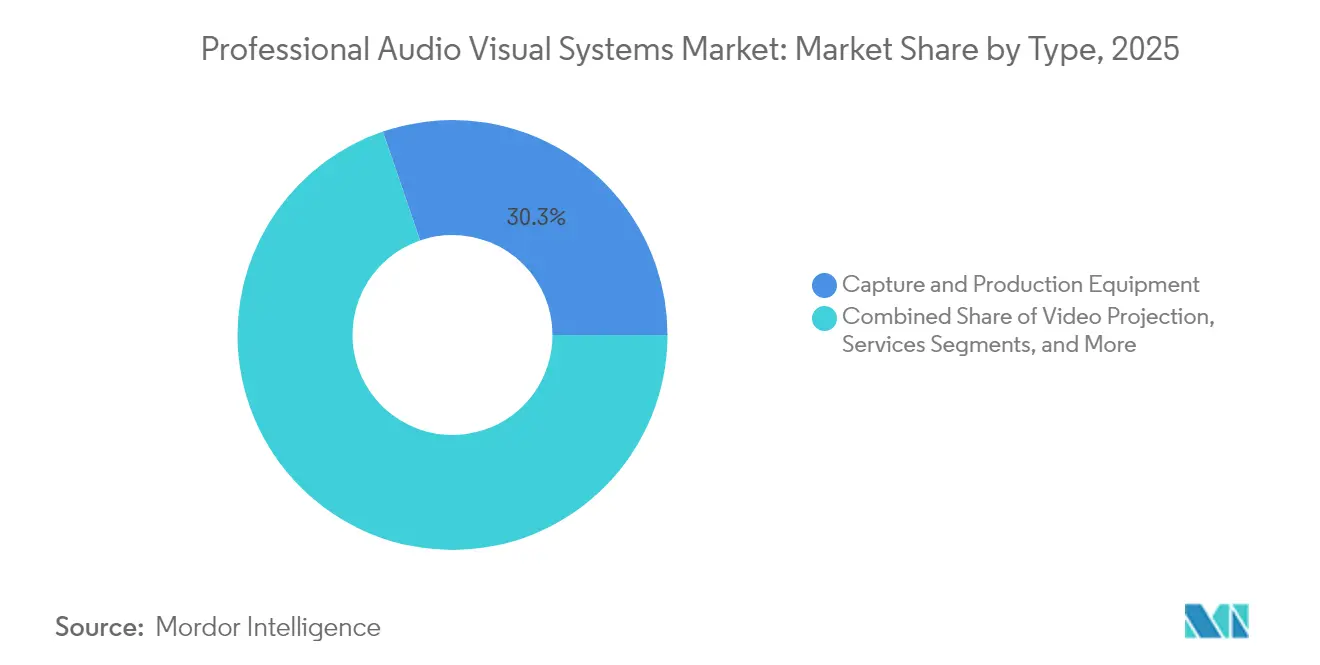

- By type, Capture and Production Equipment held a 30.25% revenue share in 2025; Streaming Media, Storage, and Distribution is projected to advance at a 5.33% CAGR through 2031.

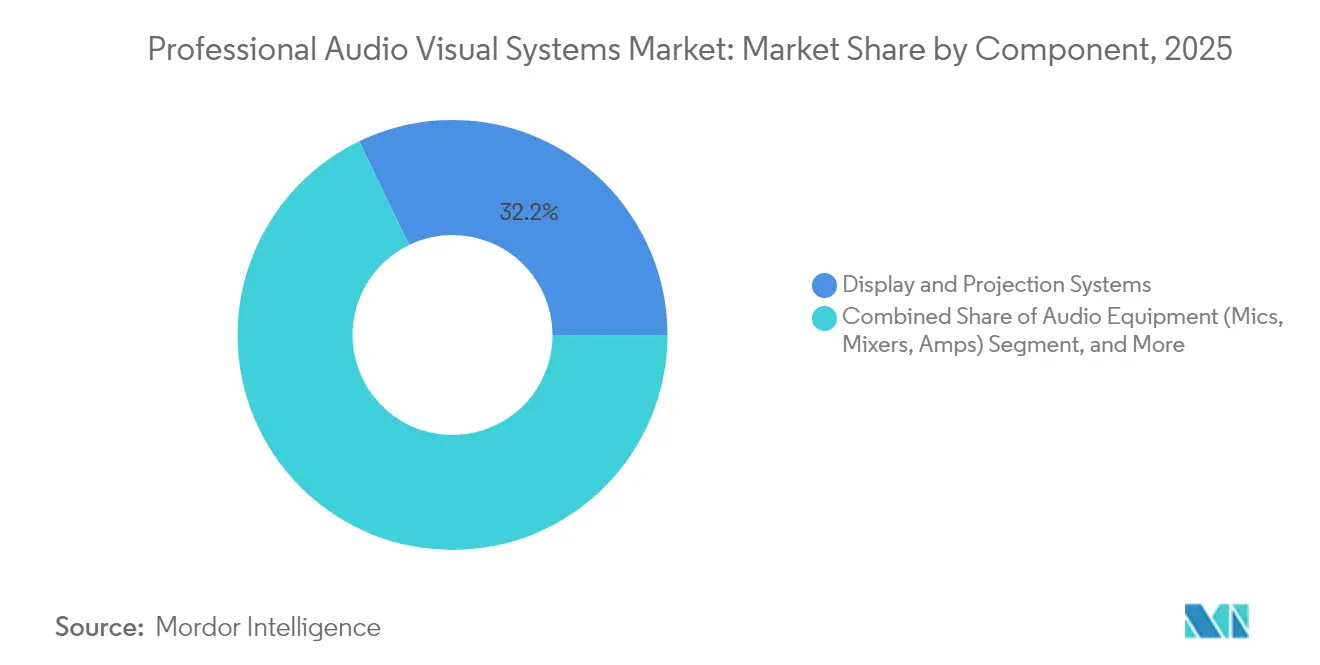

- By component, Display and Projection Systems contributed 32.15% of 2025 revenue; Audio Equipment is set to rise at a 5.03% CAGR during the forecast period.

- By end-user vertical, Corporate accounted for 32.62% of spending in 2025, while Retail is poised for the fastest 4.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Professional Audio Visual Systems Market Trends and Insights

Driver Imapct Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Hybrid work and learning surge | +1.2% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Experiential retail and public-venue LED rollouts | +0.8% | Core in Asia-Pacific, follow-on in North America | Medium term (2-4 years) |

| Live and hybrid events rebound post-pandemic | +0.7% | Global, metro clusters | Short term (≤ 2 years) |

| Migration to AV-over-IP architectures | +0.9% | North America and Europe lead, Asia-Pacific follows | Long term (≥ 4 years) |

| AI-driven real-time accessibility solutions | +0.5% | Global, regulatory driven in developed markets | Medium term (2-4 years) |

| Decarbonization mandates for energy-efficient AV | +0.4% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid Work and Learning Surge

Corporate spending shifted from isolated conference-room upgrades to enterprise-wide ecosystems that deliver equitable experiences for on-site and remote staff. Investments span spatial audio arrays, multi-camera tracking, and automated content framing that integrate with leading collaboration platforms.[1]Source: Extron, “Extron and Microsoft Teams,” extron.com Education is mirroring this demand with lecture capture, campus streaming, and device management that support blended classrooms. The professional audio visual system market benefits because enterprises prefer certified, fully managed solutions that plug into existing IT policies. Rapid refresh cycles are fueled by employee experience benchmarks, leading to multiyear procurement roadmaps. As a result, platform interoperability and cloud dashboards have emerged as critical vendor differentiators.

Experiential Retail and Public-Venue LED Rollouts

Retail chains are turning stores into immersive media venues where fine-pitch LEDs deliver branded storytelling, wayfinding, and real-time promotions. Scheels’ USD 11 million national signage rollout underscores capital intensity and scale.[2]Source: Chain Store Age, “Scheels in USD 11 Million Digital Signage Rollout,” chainstoreage.com Public buildings and transport hubs are installing similar displays to manage passenger flow and safety messaging. Central content management lets operators synchronize campaigns across regions while tailoring local language and offers. The professional audio visual system market is bolstered because display hardware now ships with embedded analytics that feed retailers’ CRM tools. Rising foot-traffic expectations keep LED demand elevated despite cyclical retail spending.

Live and Hybrid Events Rebound Post-Pandemic

Trade shows, concerts, and corporate town halls now serve simultaneous in-person and virtual audiences, requiring broadcast-grade cameras, mixing consoles, and low-latency streaming encoders. Attendance at NAB 2025 surpassed 55,000, signaling renewed exhibitor confidence.[3]Source: AV Network, “Pro AV 2025: What’s Trendy?” avnetwork.com Permanent installs replace rental gear as venues hedge against future disruptions. Event organizers prioritize flexible infrastructures that reconfigure between full-capacity shows and small hybrid seminars. Consequently, the professional audio visual system market sees sustained orders for scalable production switchers and cloud content delivery.

Migration to AV-over-IP Architectures

Enterprises are moving from point-to-point cabling toward Ethernet-based audio and video transport that rides on existing switches.[4]Source: AVIXA, “Guide to AV over IP,” avixa.orgStandards such as IPMX and Dante accelerate multivendor interoperability, reducing lock-in and enabling phased upgrades. Benefits include dynamic routing, remote monitoring, and simplified adds-moves-changes that cut the total cost of ownership over system life. The switch favors suppliers with network engineering expertise and secure firmware roadmaps. Long term, software licenses and analytics subscriptions attached to AV-over-IP endpoints are expected to outpace pure hardware margins across the professional audio visual system market.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High TCO and compliance costs | -0.8% | Global, intense in regulated industries | Medium term (2-4 years) |

| Semiconductor and display supply-chain volatility | -0.6% | Global, production centered in Asia-Pacific | Short term (≤ 2 years) |

| Cyber-insurance premiums on networked AV | -0.3% | North America and Europe, expanding worldwide | Medium term (2-4 years) |

| Skilled-labor shortages and wage inflation | -0.7% | Global, severe in developed economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High TCO and Compliance Costs

Accessibility, cybersecurity, and energy mandates have transformed procurement math. The FCC rules, effective January 2027, require captioning, sign-language support, and accessible user interfaces within video-conferencing platforms. Parallel energy standards push manufacturers to redesign enclosures and power supplies with higher-efficiency components. Compliance adds testing, certification, and frequent software updates, doubling lifecycle spending for complex deployments. Organizations underestimate ongoing training, monitoring, and audit documentation, leading to budget overruns that temper near-term orders in the professional audio visual system market.

Skilled-Labor Shortages and Wage Inflation

Installation and service teams must now blend AV design, network engineering, and cybersecurity. The talent pool has not kept pace; average U.S. AV technician wages climbed to USD 59,260 in 2024, outpacing broader occupational averages. Project timelines extend while integrators search for Dante-certified programmers and IT-savvy field engineers. Firms invest in internal academies and vendor-sponsored certifications, but ramp-up periods stretch delivery schedules. Persistent scarcity restricts rollout velocity, slowing revenue recognition across the professional audio visual system market despite healthy demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Content Capture Dominance Meets Streaming Momentum

The professional audio visual system market recorded Capture and Production Equipment at a leading 30.25% share in 2025, underscoring the premium placed on high-quality source content. Camera systems, PTZ controllers, and production switchers move down-market as corporate and educational studios replicate broadcast workflows. Bundled subscription models that wrap hardware, software, and remote support increase annual recurring revenue for vendors. Streaming Media, Storage, and Distribution, the fastest-growing slice at a 5.33% CAGR, reflects demand for scalable cloud encoders and on-demand content libraries. Edge caching reduces latency for globally dispersed viewers, turning media servers into strategic nodes in the professional audio visual system market size discussions.

Traditional Video Projection retains relevance for auditoriums and houses of worship but yields share to direct-view LED in high-brightness settings. Services, including design, monitoring, and break-fix contracts, climb as customers outsource lifecycle management. Emerging types such as holographic displays and spatial computing remain niche yet capture innovation budgets for premium venues. Every sub-segment illustrates a shift where value creation migrates from isolated hardware to integrated ecosystems that monetize analytics and content workflows.

By Component: Displays Lead While Intelligent Audio Accelerates

Display and Projection Systems commanded 32.15% of revenue in 2025 as enterprises replaced lamp-based projectors with fine-pitch LED tiles and interactive flat panels. The professional audio visual system market size for this component is forecast to keep pace with venue expansions, but margin pressure grows due to commoditization. In response, manufacturers bundle calibration software and energy dashboards. Audio Equipment displays the strongest 5.03% CAGR because intelligible speech is decisive for meeting equity. Advances in beamforming microphones, spatial audio processors, and AI noise suppression reshape acoustic design norms.

Control and Processing units form the digital nervous system, orchestrating sources, displays, lighting, and building management. Open APIs allow integrators to embed AV data into enterprise dashboards that track room utilization and energy consumption. Storage and Distribution Hardware evolves toward hyper-converged nodes that perform decoding, recording, and analytics at the edge. Component convergence means that future professional audio visual system market share milestones will rely less on unit shipments and more on software attach rates.

By End-User Vertical: Corporate Scale Faces Retail Agility

Corporate buyers retained a 32.62% revenue contribution in 2025 as hybrid work shifted from pilot to permanent. Multizone audio, wide-angle cameras, and occupancy sensors transform meeting equity into a procurement baseline. Finance and legal sectors demand stringent encryption and failover architectures, nudging average deal sizes upward. In parallel, Retail delivers the quickest 4.71% CAGR thanks to dynamic pricing labels, smart shelves, and shopper analytics that improve basket conversion.

Venues and Events allocate capital toward permanent 4K switchers and cloud streaming to hedge against travel disruptions. Education invests in lecture-capture suites, while Healthcare purchases telemedicine carts integrated with EMR systems. Government mandates on emergency communications stimulate municipal spending on outdoor LED and mass-notification audio horns. Segment diversification safeguards the professional audio visual system market against single-industry slowdowns while rewarding integrators that master domain-specific compliance.

Geography Analysis

Asia-Pacific holds the largest 29.55% share and a leading 5.78% CAGR, propelled by mega-projects in transportation, hospitality, and smart cities. National digitization policies funnel funds into campus networks and immersive classrooms in China, India, and Indonesia. Local manufacturing clusters compress lead times and cost structures, allowing rapid adoption of next-generation LED and AI processing. Japan and South Korea supplement volume with research and development breakthroughs in micro-LED packaging and voice AI, enhancing export competitiveness. Mature integrators forge joint ventures to navigate regional procurement and language diversity, a tactic that expands the professional audio visual system market footprint.

North America posts steady upgrades anchored by accessibility mandates and hybrid work normalization. The FCC captioning rule multiplies demand for AI transcription engines and adaptive UI elements. Enterprises revisit refresh cycles every three to five years to maintain parity between in-office and remote experiences. Canada boosts market momentum through investments in broadcast studios and distance-learning infrastructure across dispersed territories. Mexico’s maquiladora centers adopt AV-over-IP to coordinate cross-border supply chains, keeping the region integral to the professional audio visual system market.

Europe advances on the back of sustainability legislation requiring lower energy consumption and circular-economy design. Germany and France prioritize passive cooling enclosures and firmware that schedules low-power modes. The United Kingdom accelerates the adoption of AI analytics in transport hubs to manage passenger density. Eastern European countries allocate recovery funds to upgrade civic theatres and regional universities. Pan-European data-privacy laws elevate secure cloud control as a competitive edge among vendors, shaping procurement policies across the professional audio visual system market.

Competitive Landscape

Competition is moderate and trending toward consolidation. Acuity Brands finalized a USD 1.215 billion acquisition of QSC in January 2025, aiming to fuse lighting, controls, and the Q-SYS cloud platform into a unified smart-building offering. Scale allows cost leverage in silicon sourcing and accelerates roadmap execution. Large integrators such as AVI-SPL and Diversified broaden global reach through regional takeovers, expanding managed-service annuities, and strengthening relationships with multinational clients.

Differentiation is shifting from proprietary hardware toward software extensibility, cybersecurity compliance, and AI-driven diagnostics. Vendors embed machine-learning algorithms that predict amplifier failures or microphone misuse, cutting downtime and service calls. Suppliers able to prove low total emissions during product life cycles gain traction in Europe and parts of Asia-Pacific as sustainability reporting tightens. The professional audio visual system market favors brand portfolios that span capture, processing, display, and analytics, enabling single-vendor fulfillment for complex bids.

Niche disruptors exploit cloud-native architectures and subscription pricing that replace capex with opex. Their platforms integrate APIs for facility management and IoT sensors, converting AV endpoints into data storytellers. Established manufacturers respond with open SDKs and marketplace ecosystems, signaling a shift toward collaborative innovation. Over the medium term, software revenue share is expected to rise faster than hardware, altering valuation metrics for publicly listed firms in the professional audio visual system industry.

Professional Audio Visual Systems Industry Leaders

AVI-SPL Inc.

Diversified

AVI Systems Inc.

Solotech Inc.

Kinly BV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Acuity Brands completed its USD 1.215 billion purchase of QSC, bringing cloud-manageable audio, video, and control products into its Intelligent Spaces Group and expanding data-driven building services.

- December 2024: AVI Systems acquired CCS Southeast, enlarging federal-agency support capabilities and lifting headcount beyond 1,200 across 40 sites.

- December 2024: VusionGroup partnered with The Fresh Market to roll out Vusion 360 digital shelf labels in 166 stores by end-2025, combining multicolor e-ink, AI inventory analysis, and data dashboards.

- October 2024: Extron introduced ShareLink Pro 2500, the first 4K dual-screen wireless presenter supporting simultaneous display from four devices and USB pickup for virtual meetings.

Global Professional Audio Visual Systems Market Report Scope

A professional audio-visual (AV) system is a sophisticated interaction system installed for commercial sharing, advertising, and marketing. It is used in private and public complexes for electronic displays to deliver videos, web content, graphics, and texts. Lighting and sound devices, digital signage, video conferencing systems, companion whiteboard recording equipment, and projector systems are audio-visual systems. These components help improve overall user communication and connectivity and are used in classrooms, presentations, and on-site product demonstrations.

The professional audio-visual systems market is segmented by type (capture and production equipment, video projection, streaming media, storage and distribution, services, and other types), end-user vertical (corporate, venues and events, retail, media, and entertainment, and other end-user verticals), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

By Type

| Capture and Production Equipment |

| Video Projection |

| Streaming Media, Storage and Distribution |

| Services |

| Other Types |

By Component

| Audio Equipment (mics, mixers, amps) |

| Display and Projection Systems |

| Control and Processing |

| Storage and Distribution Hardware |

By End-user Vertical

| Corporate |

| Venues and Events |

| Retail |

| Media and Entertainment |

| Education |

| Government |

| Healthcare |

| Other End-user Verticals |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type | Capture and Production Equipment | ||

| Video Projection | |||

| Streaming Media, Storage and Distribution | |||

| Services | |||

| Other Types | |||

| By Component | Audio Equipment (mics, mixers, amps) | ||

| Display and Projection Systems | |||

| Control and Processing | |||

| Storage and Distribution Hardware | |||

| By End-user Vertical | Corporate | ||

| Venues and Events | |||

| Retail | |||

| Media and Entertainment | |||

| Education | |||

| Government | |||

| Healthcare | |||

| Other End-user Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the professional audio visual system market in 2026?

The professional audio visual system market size is USD 308.23 billion in 2026.

What is the expected growth rate through 2031?

Aggregate revenue is projected to advance at a 4.42% CAGR, reaching USD 382.74 billion by 2031.

Which region leads spending on professional AV solutions?

Asia-Pacific holds the highest spending share at 29.55% and also records the fastest 5.78% CAGR.

Which product type commands the most revenue?

Capture and Production Equipment leads with 30.25% revenue share, reflecting the boom in content creation.

Page last updated on: