Production Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.03 Billion |

| Market Size (2031) | USD 10.63 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

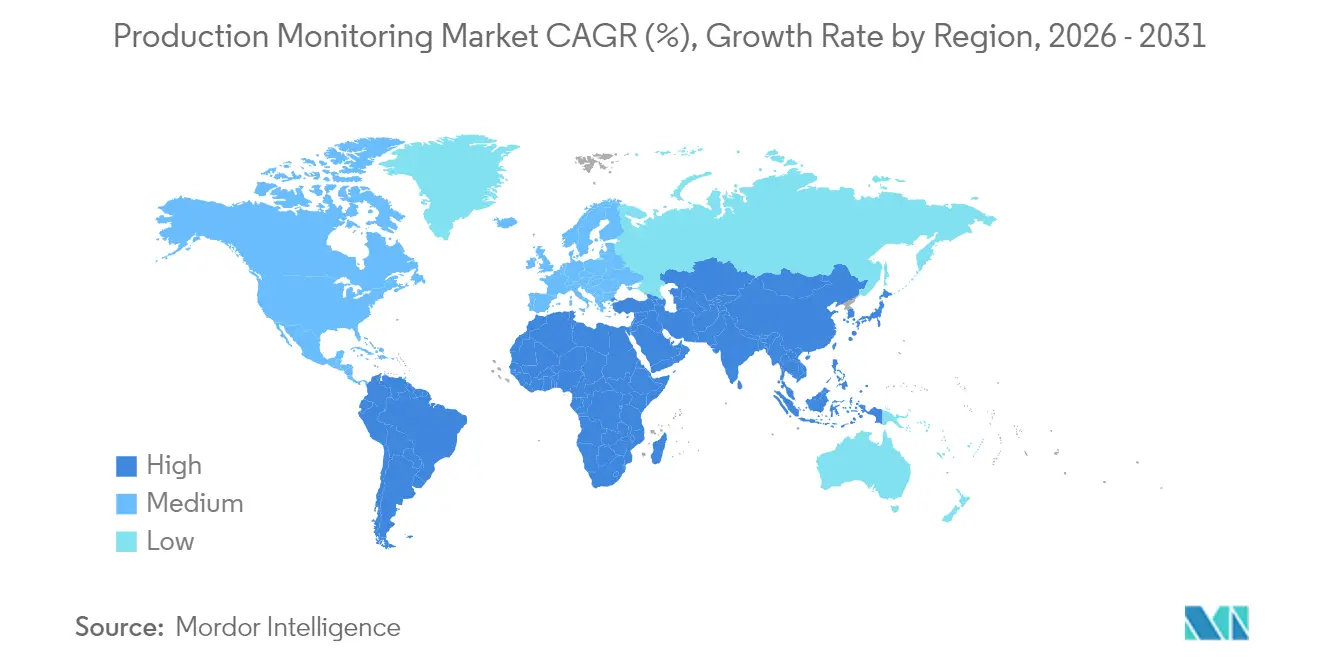

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

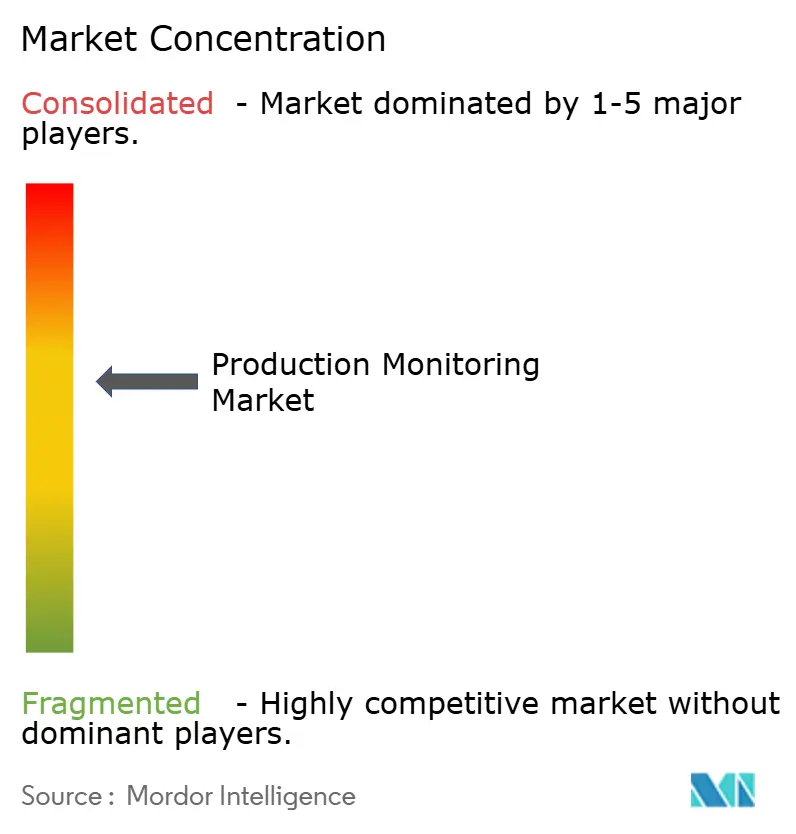

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Production Monitoring Market Analysis by Mordor Intelligence

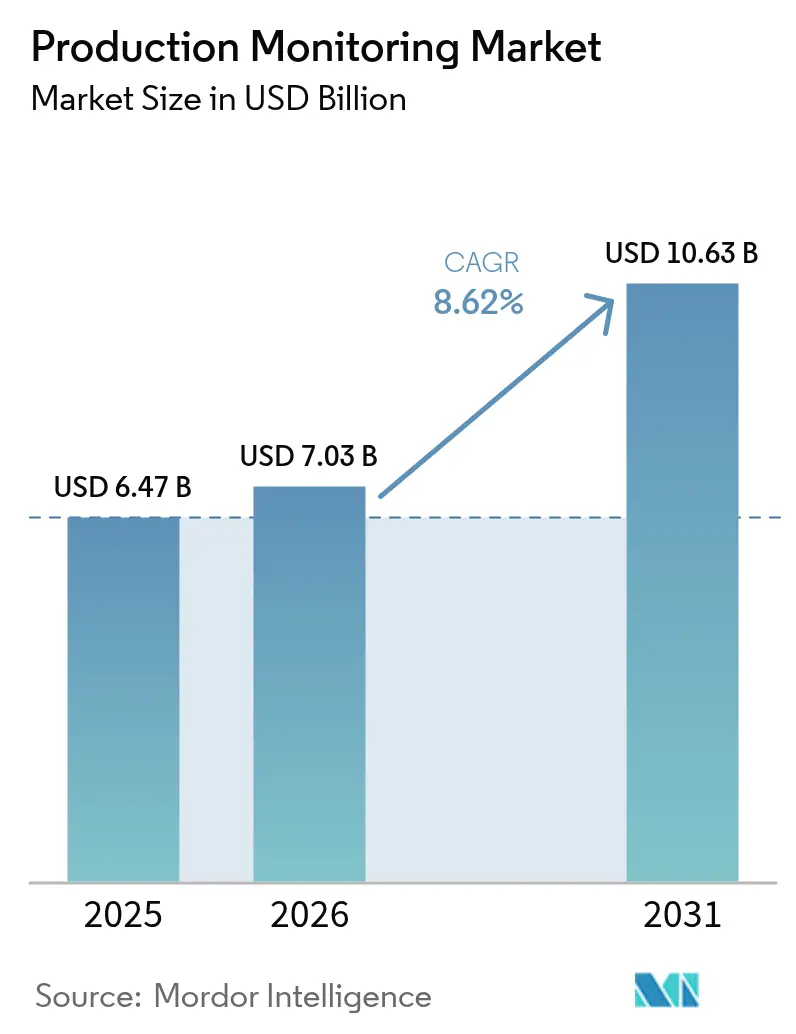

The Production monitoring market size was valued at USD 6.47 billion in 2025 and estimated to grow from USD 7.03 billion in 2026 to reach USD 10.63 billion by 2031, at a CAGR of 8.62% during the forecast period (2026-2031). The Production monitoring market is expanding because manufacturers are aligning Industry 4.0 roadmaps with corporate productivity goals, rolling out IIoT architectures, and prioritizing predictive maintenance over reactive repairs. Cloud-first deployments continue to attract investment because they scale analytics and lower upfront hardware costs, while edge-AI installations give plant managers instant insights at the machine level. Automotive and high-compliance verticals such as pharmaceuticals remain early adopters, but food, energy, and discrete electronics plants are fast closing the gap as regulatory reporting and traceability mandates tighten. Competitive intensity is rising as incumbent automation vendors pivot from hardware bundles to software-centric service models and specialized AI companies enter with anomaly-detection algorithms that reduce downtime.

Key Report Takeaways

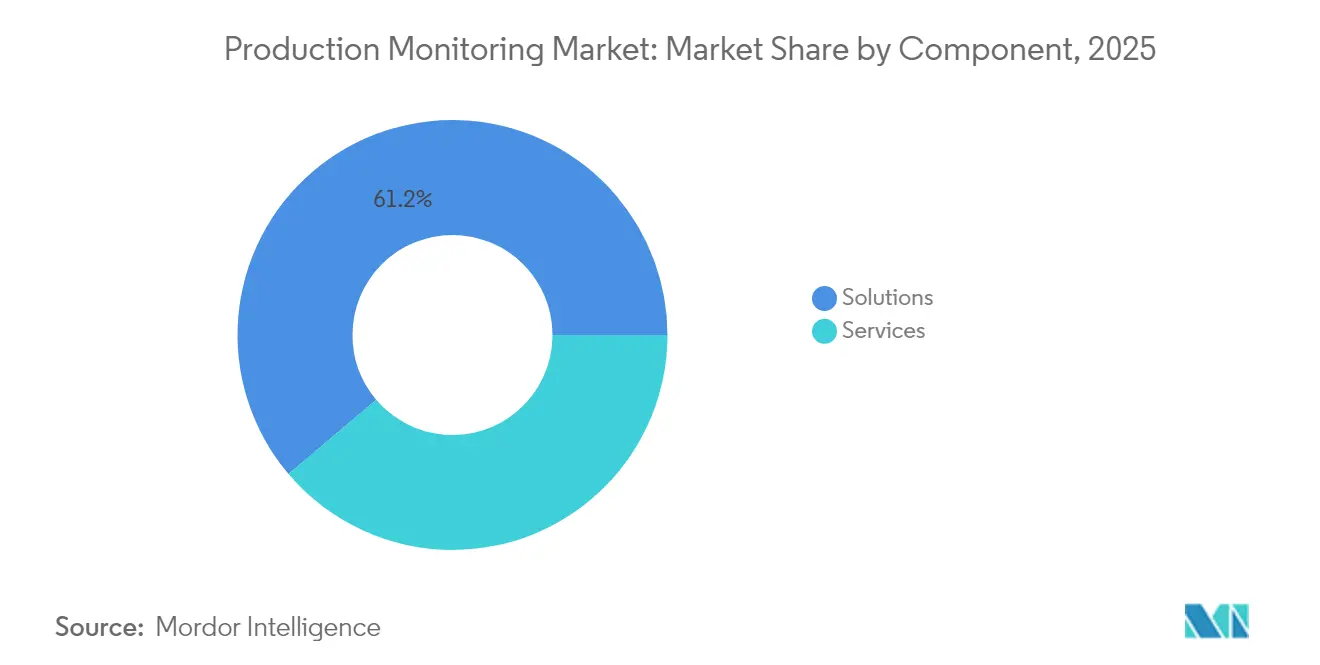

- By component, Solutions held 61.20% of the Production monitoring market share in 2025; Services is projected to compound at a 9.62% CAGR to 2031.

- By deployment, cloud models accounted for 57.40% of the Production monitoring market size in 2025 and are expanding at a 9.31% CAGR through 2031.

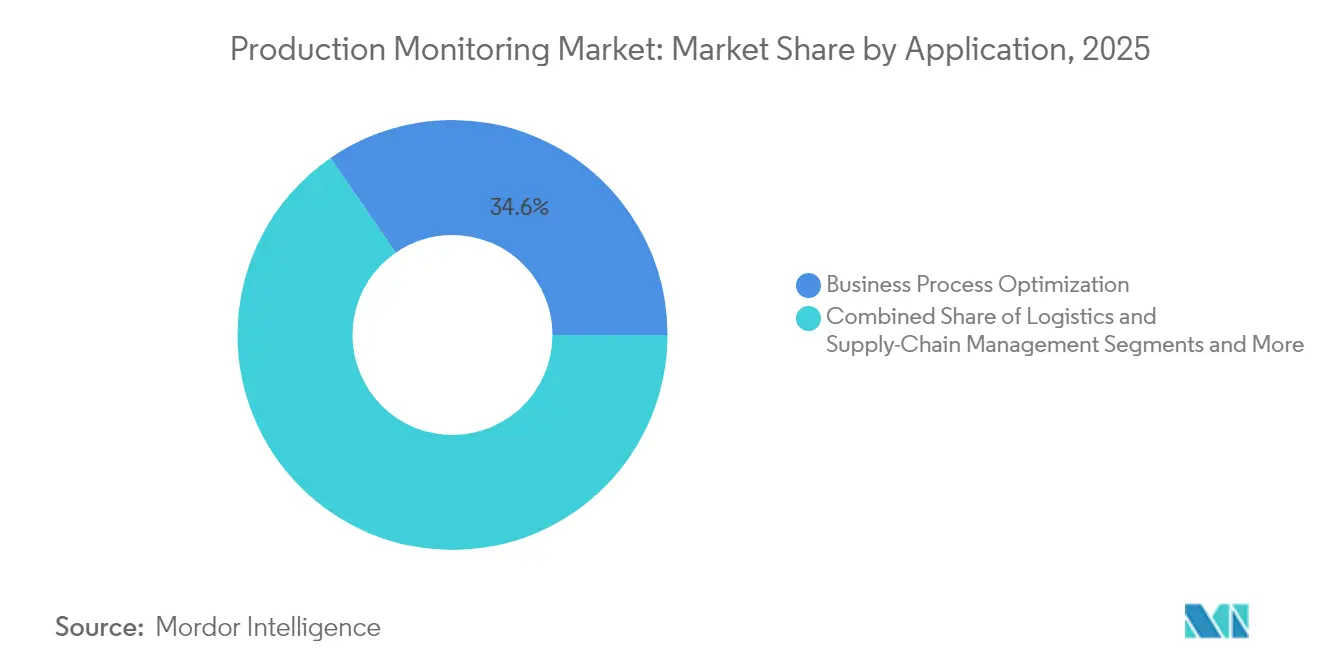

- By application, business process optimization accounted for 34.60% of the Production monitoring market size in 2025; edge-AI anomaly detection leads growth at 9.01% CAGR to 2031.

- By end user, the automotive sector led with a 21.70% Production monitoring market share in 2025, while healthcare and life sciences is advancing at a 9.78% CAGR to 2031.

- By geography, Asia-Pacific commanded 33.70% of the Production monitoring market in 2025; the Middle East and Africa region is forecast to grow at a 10.34% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Production Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for centralized monitoring and predictive maintenance | +2.8% | Global, early gains in Asia-Pacific hubs | Medium term (2-4 years) |

| Adoption of IIoT platforms for real-time visibility | +2.1% | North America & EU leading, Asia-Pacific rapid uptake | Short term (≤ 2 years) |

| Expansion of Industry 4.0 smart-factory initiatives | +1.9% | Asia-Pacific core, spill-over to Middle East & Africa | Medium term (2-4 years) |

| Edge-AI deployment for anomaly detection | +1.6% | Global, concentrated in automotive and oil & gas | Long term (≥ 4 years) |

| Regulatory push for energy-efficiency disclosures | +1.2% | EU and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growth of green-production certification tracking | +0.8% | Global, emphasis on developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for Centralized Monitoring and Predictive Maintenance

Manufacturers are consolidating asset data across plants to create single sources of truth that feed AI maintenance models. Zebra Technologies reported that only 16% of producers had real-time shop-floor visibility in 2024, exposing a sizeable performance gap. Automotive groups adopting predictive analytics reduced unplanned breakdowns by up to 70% and unlocked USD 100 million in lifetime equipment value by optimizing edge infrastructure. Production managers therefore view predictive maintenance as a profit lever, not merely a cost-avoidance tool, elevating demand for platforms that integrate vibration, temperature, and pressure data into actionable health scores.

Adoption of IIoT Platforms for Real-Time Visibility

IIoT suites now orchestrate machines, workers, and logistics streams in a single digital fabric. A 5G rollout at Midea Thailand delivered 15–20% productivity gains by unifying robotics and AI inspection flows. Sensor modules such as TDK’s i3 Micro integrate multi-modal data in a postage-stamp form factor, enabling brownfield sites to join data lakes without heavy retrofits. Tier-two suppliers benefit because cloud edge gateways compress deployment costs, lowering barriers to entry in the Production monitoring market.

Expansion of Industry 4.0 Smart-Factory Initiatives

Smart-factory programmes have moved beyond pilots into strategic portfolio investments. Siemens’ MACHINUM platform links machine-tool controls with adaptive feed-rate algorithms that trim downtime and energy waste. Precision manufacturers in Japan improved machine utilisation by 20% and cut scrap by 25% after linking IoT devices to digital twins, demonstrating tangible ROI that encourages further adoption. [1]Manufacturing Tomorrow, "IoT in Manufacturing: Advanced Precision as a Promising Trend for 2025," manufacturingtomorrow.com

Edge-AI Deployment for Anomaly Detection

Edge-AI pushes inferencing to microcontrollers embedded on the line, reducing latency and bandwidth needs. STMicroelectronics and SMRI used on-chip models to predict bearing failures before catastrophic damage, safeguarding uptime while keeping data on-premise for security. [2]STMicroelectronics, "AI Solution for Failure Prediction," st.comRockwell Automation’s GuardianAI updates existing drives with analytics overlays, proving that performance lifts are attainable without bolt-on sensors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security and privacy concerns | −1.8% | Global, heightened in EU & North America | Short term (≤ 2 years) |

| High upfront integration costs | −1.5% | Global, impacting SMEs in developing markets | Medium term (2-4 years) |

| OT-protocol heterogeneity in legacy assets | −1.2% | Global, established plants | Long term (≥ 4 years) |

| Shortage of OT-cybersecurity talent | −0.9% | Global, acute in Asia-Pacific & MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Security and Privacy Concerns

Connected factories widen the attack surface. The 2024 VOID Report showed that automated systems can amplify incidents when mis-configured, forcing operators to intervene manually.[3]VOID Community, "2024 VOID Report VOID Community," thevoid.communityEU manufacturers must now comply with stringent data-governance rules, driving interest in blockchain-based traceability that preserves transparency while hardening privacy.

High Upfront Integration Costs

Full-scale roll-outs strain capital budgets, especially for SMEs that still rely on analogue controls. Cloud subscriptions alleviate hardware expenditures, yet integration services remain essential to harmonise proprietary protocols. Siemens’ Simatic Automation Workstation displaces hardware PLCs with software images, creating a migration path that spreads spend over time. Financing bottlenecks persist in emerging markets where energy costs and credit access deter quick payback cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum Amid OT-IT Complexity

Solutions captured 61.20% of the Production monitoring market in 2025, reflecting entrenched hardware and platform sales. Services, however, will expand faster at 9.62% CAGR to 2031 as organisations confront protocol heterogeneity and workforce skill gaps. Emerson’s DeltaV update illustrates why: the feature pack lets utilities migrate from third-party controls while retaining legacy I/O, yet successful adoption hinges on specialist integrators who re-map tags and validate safety logic. Managed analytics and continuous optimisation contracts therefore secure recurring revenue streams for vendors and enable plant teams to scale expertise without large hiring drives.

At the same time, advisory partners now bundle change-management playbooks with technical deployments. Clients realise that organisational workflows must evolve to exploit AI insights, not simply display dashboards. This services-first mind-set reinforces a virtuous circle where solution providers embed deeper in customer operations, enlarging lifetime value in the Production monitoring market.

By Deployment: Cloud Extends Lead While Hybrid Models Balance Control

Cloud options held 57.40% of the Production monitoring market in 2025, advancing at a 9.31% CAGR as manufacturers favour elastic compute and rapid model updates. Microsoft showcases how cloud analytics decodes energy patterns to lower carbon footprints and sharpen regulatory reporting microsoft.com. Yet data-sovereignty and latency‐critical tasks keep on-premise estates relevant, especially in defense and utilities where command-and-control must function under air-gapped conditions. Hybrid frameworks emerge as the governance compromise: sensitive control loops stay local, while AI-heavy workloads offload to hyperscale resources. Emerson’s Ovation 4.0 wraps generative AI inside such an architecture, giving operators cloud-grade insights without sacrificing cybersecurity standards.

Enterprises also exploit pay-as-you-go OPEX models to prototype niche use cases, then scale proven blueprints across plants. That agility accelerates digital-transformation timelines and cements cloud’s role as the default innovation sandbox for the Production monitoring market.

By Application: Process Optimization Anchors Spend; Edge Anomaly Detection Scales Fast

Business process optimisation commanded 34.60% of the Production monitoring market size in 2025, underlining management’s focus on throughput and inventory turns. Real-time dashboards link takt-time deviations to scheduling engines, exposing bottlenecks that planners can rectify before they snowball into backlogs. Emergency and incident management solutions win board-level attention after high-profile industrial fires. The US Homeland Security roadmap identified 13 AI technologies primed to modernise crisis response, positioning production-monitoring vendors for cross-domain expansion.

Edge-AI anomaly detection represents the fastest-rising application at 9.01% CAGR. Early adopters see immediate ROI by catching bearing wear or motor imbalance during micro-second windows that traditional SCADA polling misses. Logistics-tracking modules round out demand because pandemic disruptions proved that visibility gaps directly threaten service levels. Half of food-and-beverage companies plan to fit supply-chain tracking systems by 2025, inserting new endpoints into the Production monitoring market.

By End User: Automotive Sets the Pace; Healthcare Outpaces Growth

Automotive plants accounted for 21.70% Production monitoring market share in 2025. EV production lines deploy AI vision to validate battery welds and barcode systems to authenticate components, reducing recall. Predictive maintenance platforms trim downtime on paint lines where every minute lost equates to high scrap costs.

Healthcare and life sciences exhibit the steepest trajectory at 9.78% CAGR. Stringent validation rules demand traceable batch histories that production-monitoring suites generate automatically. Digital pill tracking and real-time environmental monitoring support compliance as Healthcare 4.0 moves from concept to standard practice mdpi.com. Oil and gas operators apply autonomous distillation controls, while chemical, power, food, and aerospace users adopt digital twins to hedge against volatility and regulatory audits. These vertical expansions reinforce the addressable base for the Production monitoring market.

Geography Analysis

Asia-Pacific held 33.70% of the Production monitoring market in 2025. China scales Industry 4.0 statewide, and India’s incentive programmes underwrite smart-factory deployments despite infrastructure gaps. LG Electronics’ vision for multi-trillion KRW enterprise value by 2030 exemplifies corporate ambition to embed AI across assembly cells. ASEAN plants leverage 5G private networks to automate material flow, gaining double-digit yield lifts.

The Middle East and Africa lead growth prospects at 10.34% CAGR. Saudi Arabia’s SAR 90 billion (USD 24 billion) manufacturing push includes smart food-processing clusters that rely on continuous monitoring to certify output quality. South Africa’s digitalisation events promote transparent and flexible production, but power constraints and financing hurdles moderate rollout speed.

North America and Europe remain technology bellwethers. The EU Corporate Sustainability Reporting Directive obliges automated energy metering, prompting investments in carbon-tracking dashboards. North American executives prioritise workforce reskilling; 73% plan upskilling programmes to turn data into decisions. These dynamics ensure a steady baseline of demand even as emerging economies surge.

Competitive Landscape

The Production monitoring market shows moderate concentration. Global automation majors retain scale advantages through installed bases and lifecycle services, yet software-native entrants capture share in AI niches. Siemens pivots toward platform economics with MACHINUM and the software-only Simatic Workstation, cutting hardware lock-in and accelerating changeovers. Emerson layers generative AI onto Ovation 4.0, using data federation to differentiate in power and water markets.

Strategic alliances proliferate as vendors partner with hyperscalers to embed analytics at the edge while leveraging cloud compute for model training. M&A deals target data-ops and cybersecurity startups to patch capability gaps. White-space remains in emergency-management overlays where incumbents lack domain depth, inviting specialists to stake positions. Price competition shifts from hardware margins to value-based service contracts, reshaping profitability drivers across the Production monitoring market.

Production Monitoring Industry Leaders

-

Capgemini SE

-

Siemens AG

-

Emerson Electric Co.

-

Rockwell Automation Inc.

-

New Relic Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: bioMérieux identified AI and blockchain as near-term levers for food-safety assurance, validating investment themes in traceability platforms.

- March 2025: Oktogrid’s analysis of the Heathrow transformer fire underlined the ROI of high-frequency partial-discharge monitoring and will likely spur utility adoption of continuous monitoring.

- February 2025: An industrial fire at SPS Technologies highlighted demand for integrated incident-management layers that link sensor alerts with evacuation protocols.

- January 2025: TDK introduced the i3 Micro Module, embedding multi-sensor and edge-AI capabilities to predict industrial anomalies, expanding its value proposition from component supplier to predictive-maintenance enabler.

Global Production Monitoring Market Report Scope

The production monitoring records the overall performance of the production line in real-time through software and service offerings deployed through the cloud or on-premise, providing the monitoring of production to end users, such as oil and gas, chemical, and automotive.

| Solutions |

| Services |

| Cloud |

| On-Premise |

| Business Process Optimization |

| Logistics and Supply-Chain Management |

| Emergency and Incident Management |

| Automation and Control Management |

| Oil and Gas |

| Chemical |

| Automotive |

| Energy and Power |

| Food and Beverage |

| Aerospace and Defense |

| Healthcare and Life Sciences |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN-5 | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment | Cloud | ||

| On-Premise | |||

| By Application | Business Process Optimization | ||

| Logistics and Supply-Chain Management | |||

| Emergency and Incident Management | |||

| Automation and Control Management | |||

| By End User | Oil and Gas | ||

| Chemical | |||

| Automotive | |||

| Energy and Power | |||

| Food and Beverage | |||

| Aerospace and Defense | |||

| Healthcare and Life Sciences | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN-5 | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Production monitoring market?

The Production monitoring market size reached USD 7.03 billion in 2026 and is forecast to hit USD 10.63 billion by 2031.

Which deployment model is growing fastest?

Cloud deployments lead growth, expanding at a 9.31% CAGR as manufacturers seek scalable analytics capabilities.

Which industry vertical adopts production monitoring most actively?

Automotive plants hold the largest share at 21.70%, although healthcare and life sciences deliver the highest CAGR at 9.78% through 2031.

Why are services growing faster than solutions?

Services address OT-IT integration complexity, data-quality governance, and continuous AI model tuning, driving a 9.62% CAGR.

Which region shows the highest growth potential?

The Middle East and Africa region is projected to expand at a 10.34% CAGR thanks to large-scale industrial diversification programmes.

How is edge-AI reshaping production monitoring?

Edge-AI enables real-time anomaly detection on the shop floor, reducing unscheduled downtime by up to 70% for early adopters.

Page last updated on: