Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 5.63 Trillion |

| Market Size (2031) | USD 10.95 Trillion |

| Growth Rate (2026 - 2031) | 14.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Asset Management Market Analysis by Mordor Intelligence

The Japan asset management market reached USD 5.63 trillion in 2026, and it is projected to reach USD 10.95 trillion by 2031 at a 14.22% CAGR, reflecting a strong expansion in market size during the forecast period. The Japan asset management market is experiencing robust growth, driven by a gradual shift in household portfolios toward professionally managed investment vehicles. Investors are increasingly favoring investment trusts, reflecting a broader move away from traditional savings and cash holdings. Regulatory changes are also shaping the market, as pension reforms and disclosure requirements encourage greater transparency and the adoption of fee-based advisory models. The Financial Services Agency’s push for fiduciary standards is strengthening trust between advisors and clients, further supporting inflows into managed products. Rising interest rates are altering the risk-reward dynamics across different asset classes, prompting both retail and institutional investors to diversify their holdings. Meanwhile, the expansion of ESG and transition-bond strategies is creating new opportunities for specialized investment approaches. This growing focus on sustainability is widening the investable universe and attracting capital into socially responsible assets. Product innovation is accelerating, particularly in alternatives, indexed solutions, and tokenized instruments that cater to evolving investor preferences.

Key Report Takeaways

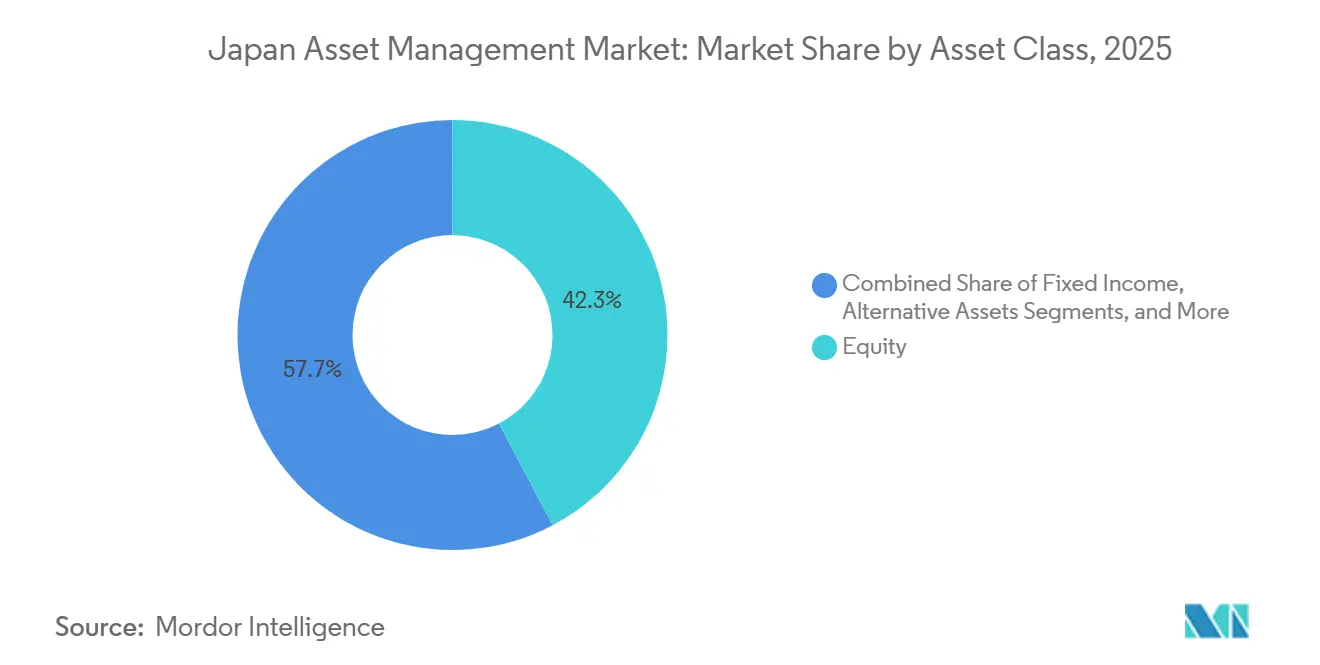

- By asset class, equity assets led with 42.29% of the Japan asset management market share in 2025, while alternative assets are forecast to expand at a 16.34% CAGR through 2031.

- By firm type, banks held 45.61% of the Japanese asset management market share in 2025, while wealth advisory firms and registered investment advisors are projected to grow at a 15.81% CAGR.

- By mode of advisory, human advisory accounted for 91.18% of the Japanese asset management market share in 2025, while robo-advisory is scaling at a 20.18% CAGR.

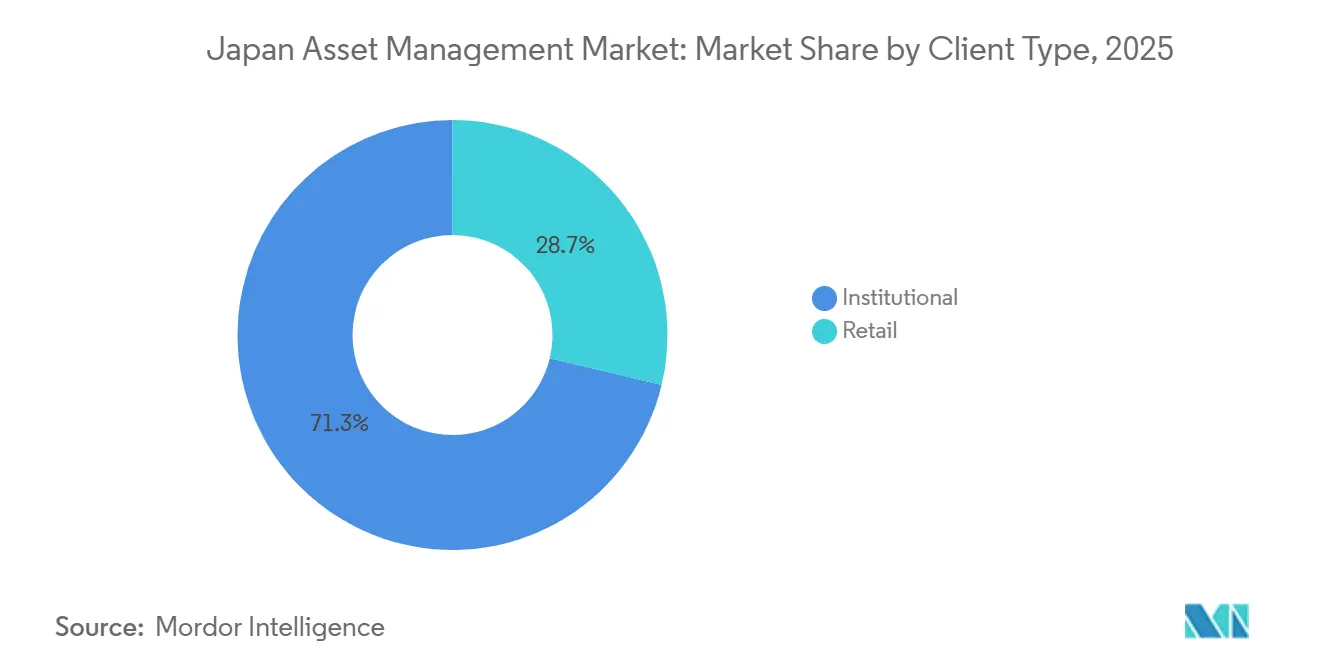

- By client type, institutional mandates accounted for 71.27% of the Japan asset management market share in 2025, while retail is advancing at a 17.42% CAGR supported by the revised NISA framework.

- By management source, onshore-managed assets represented 85.56% of the Japan asset management market share in 2025, while offshore-delegated mandates are projected to grow at a 16.85% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Asset Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating shift from bank deposits to investment funds | +3.2% | National, with early gains in Tokyo, Osaka, and Nagoya metropolitan areas | Medium term (2-4 years) |

| Mandatory corporate pension reform boosting AUM inflows | +2.8% | National, concentrated in corporate headquarters regions (Tokyo, Osaka) | Long term (≥ 4 years) |

| Robo-advisory adoption among mass-affluent investors | +1.9% | National, the strongest uptake in urban prefectures (Tokyo, Kanagawa, Osaka) | Short term (≤ 2 years) |

| GPIF's alternative-asset appetite is setting industry benchmarks | +2.5% | National impact, spillover to prefectural and municipal pension systems | Long term (≥ 4 years) |

| Tokenized securities pilots opening new investable asset pools | +1.4% | Tokyo-Osaka financial corridor, expanding to regional financial centers | Medium term (2-4 years) |

| ESG transition bonds fueling specialized fund launches | +2.4% | National, with higher activity in industrial prefectures (Aichi, Hyogo, Fukuoka) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift from Bank Deposits to Investment Funds

Japanese households are gradually reallocating their financial assets from traditional bank deposits to investment funds, with investment trusts reaching a growing share of total household assets. In FY2024, household allocation to investment trusts rose to 6.0% of total financial assets, marking a significant inflection in deposit substitution and establishing a higher baseline for recurring mutual fund inflows. This trend reflects increasing familiarity with market-based instruments and represents a structural shift in saving behavior, supporting more consistent inflows into professionally managed products[1]Bank of Japan, “Flow of Funds Accounts: Household Sector Financial Assets,” Bank of Japan, boj.or.jp. . The behavioral shift toward investment funds is driven by generational turnover and growing acceptance of equity exposure among younger investors. Regulatory changes, including a more flexible tax-advantaged investment framework, have further encouraged households to channel savings into equity-focused products, particularly foreign equities. In response, regional banks are transforming branches into advisory hubs to capture this changing investor demand, shifting staff from traditional teller roles to wealth and investment advisory services.

Mandatory Corporate Pension Reform Boosting AUM Inflows

Recent corporate pension reforms have strengthened asset inflows into the Japan asset management market by making defined-contribution plans more flexible and accessible. Changes such as the removal of strict employer-matching requirements, higher contribution limits, and extended eligibility have expanded the potential contribution base, enabling managers to plan for sustained inflows. These reforms have prompted many companies, particularly in manufacturing regions, to transition away from defined-benefit plans, increasing demand for professionally managed retirement products. Life-cycle and low-volatility strategies are seeing strong adoption within workplace plans, reflecting investor preference for products that balance growth with risk management. Digital reporting platforms have further reduced administrative burdens for plan sponsors, accelerating the shift to defined-contribution formats and reinforcing stable, long-term channels for asset accumulation.

Robo-Advisory Adoption Among Mass-Affluent Investors

Robo advisory platforms in Japan have rapidly gained traction among mass affluent investors and now manage approximately Yen 3 trillion (USD 19 billion) in assets. These services are attractive due to low minimums, automated diversification, and digital accessibility, helping broaden participation beyond traditional advisory channels. A major milestone was the acquisition of WealthNavi by MUFG for Yen 30 billion (USD 190 million), which signals mainstream validation and creates cross-sell opportunities into the MUFG Group’s large retail base[2]Reuters, “Japan’s MUFG to spend over $660 million to buy robo‑adviser WealthNavi,” Reuters. Adoption skews toward younger investors, with over half of users aged 30–44, indicating that digital advice is filling an accessibility gap for this cohort. Robo advisors are also gaining momentum in retirement channels such as iDeCo, where average fees have been reduced from 0.68% to 0.31%, enhancing cost competitiveness[3]SBI Group, “SBI Group Investor Presentation,” SBI Group. The combination of scale, demographic reach, and expanded retirement integrations highlights the strategic role of automated investment solutions in Japan’s evolving wealth management landscape. Overall, robo advisory adoption reflects a structural shift toward low-cost, technology-enabled wealth management for the mass affluent segment.

GPIF’s Alternative-Asset Appetite Setting Industry Benchmarks

The Government Pension Investment Fund (GPIF) is increasingly emphasizing alternative assets such as infrastructure, private equity, and real assets to enhance returns beyond traditional fixed-income and public equity markets. This shift reflects challenges in domestic returns, as low government bond yields and mature equity valuations limit the ability to meet long-term pension obligations. GPIF’s commitment to expanding alternative allocations is shaping expectations across corporate and prefectural pension systems, encouraging alignment with public benchmarks. Domestic asset managers are responding by building in-house expertise and launching dedicated funds in areas like renewable energy and infrastructure. At the same time, foreign managers are scaling operations in Japan, targeting private credit and other alternative strategies to meet rising demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent negative/near-zero interest-rate policy compressing yields | -1.8% | National, acute pressure on regional financial institutions outside Tokyo-Osaka | Short term (≤ 2 years) |

| The shrinking working-age population is limiting long-term contribution growth | -2.3% | National, most severe in rural prefectures (Akita, Shimane, Kochi) | Long term (≥ 4 years) |

| Regulatory compliance and risk-profiling requirements are increasing operational costs | -1.2% | National, affecting all retail and corporate channels | Short to medium term (1–3 years) |

| Market concentration and competition from robo-advisors are reducing margins for traditional managers | -0.9% | Primarily urban financial centers (Tokyo, Osaka, Nagoya) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Persistent Negative or Near-Zero Interest-Rate Policy Compressing Yields

Despite the Bank of Japan exiting negative rates and gradually raising policy rates, real interest rates remain negative when adjusted for inflation, suppressing the yield foundation for balanced and target-date portfolios. Low 10-year JGB yields complicate fixed-income allocation decisions, while regional banks with large government bond holdings face compressed net-interest margins, limiting their ability to invest in advisory capacity or expand fee-based AUM. Low yields also depress revenue from money-market and short-duration bond funds, narrowing the overall revenue mix unless clients shift toward higher-fee products. Although the BOJ’s balance-sheet normalization plan may gradually restore price discovery in equities, policymakers are proceeding cautiously to avoid disruptive effects on currency and exports, leaving yield pressures largely intact. Collectively, these conditions constrain portfolio performance, limit revenue growth, and pose ongoing challenges for asset managers in Japan.

Shrinking Working-Age Population Limiting Long-Term Contribution Growth

Japan’s declining working-age population is reducing the base of contributors to corporate pensions and individual retirement schemes, creating long-term pressures on asset inflows. The demographic decline is most pronounced in rural prefectures, where working-age shares are low, turning some prefectural pension systems into net withdrawers and increasing the payout burden relative to contributions. Even with higher contribution ceilings, inflows increasingly depend on retention and asset growth rather than new entrants. Rising dependency ratios indicate a growing share of assets will be drawn down to meet retirement needs, placing additional strain on pension systems. While managers are targeting engagement strategies for women returning to work and foreign labor, lower income levels in these groups limit near-term contribution capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Alternatives Surge While Equity Dominance Persists

Equity assets commanded 42.29% of the Japan asset management market size in 2025, and this was led by TOPIX-linked passive mandates and focused themes spanning semiconductors, robotics, and healthcare. Alternative assets are forecasted to expand at a 16.34% CAGR through 2031 from a modest base, propelled by the GPIF’s alternatives database and broader policy alignment that encourages longer-duration exposures in institutional portfolios. Fixed-income growth remains limited as persistently low yields push investors toward credit risk or external diversification to meet policy benchmarks. Managers are increasingly pivoting toward infrastructure debt, private credit, and secondary markets, as seen in strategic acquisitions of overseas alternatives platforms. Tokenized assets and innovative REIT structures are also providing new channels for investors to access illiquid or hybrid assets with greater flexibility and secondary-market liquidity.

The shift in asset-class allocation is reinforced by domestic capacity-building in alternatives and selective use of offshore expertise where local execution remains thin. Public equity strategies continue to evolve, with stronger governance emphasis and stewardship practices sustaining investor interest even as passive inflows normalize under central bank policy. Multi-asset and balanced solutions are expanding, catering to defined-contribution participants who seek smoother return profiles. Institutional and retail allocators are increasingly blending listed equities, higher-quality bonds, and alternatives to achieve diversification while managing liquidity exposure. Overall, the asset mix evolution reflects a market balancing traditional equity dominance with a strategic push toward higher-yielding, long-duration alternative investments.

By Firm Type: Wealth Advisors Disrupt Bank Hegemony

Banks held 45.61% of the Japan asset management market share in 2025 due to custody, broad cross-sell, and national branch density that supports multi-channel distribution. Wealth advisory firms and registered investment advisors are projected to grow at a 15.81% CAGR as the FSA’s fiduciary framework pushes product distribution toward fee-based advisory accounts that minimize conflicts and emphasize ongoing service. Broker-dealers are adapting by creating wrap-account platforms for high-net-worth clients and by emphasizing fee-led relationships instead of transaction-led revenue. Regional banks are rotating staffing toward advisory roles to stabilize income mix as net-interest margins remain below 0.95% under a shallow rate curve. Trust banks and insurance-linked managers continue to grow within specialized mandates, especially in DC, where their expertise aligns with sponsor needs and reporting obligations.

The direction of travel is toward higher professionalization and formal planning standards, supported by the FSA’s adoption of ISO 22222 in late 2024, which encourages consistent advice processes that clients can evaluate across providers. Advisor migration from product-push environments to fee-based models has quickened following the June 2025 trailer-fee disclosure rule, which has improved transparency and accelerated the move to clean-fee share classes and ETFs in the Japan asset management market. As firms codify fiduciary duty and invest in advice technology, the economics of human advisory services become more scalable through hybrid models that pair planners with digital tools to serve more households effectively. Competitive differentiation now rests on advice quality, platform breadth, risk tooling, and service standards rather than shelf depth alone. Firms that can balance compliance automation with client-facing personalization are best positioned to gain share over the next planning cycle.

By Mode of Advisory: Robo Platforms Scale Despite Compliance Friction

Human advisory accounted for 91.18% of assets in 2025, reflecting high trust in advisor relationships and the value clients place on behavioral support during market episodes. Robo-advisory is scaling at a 20.18% CAGR, after MUFG’s acquisition of WealthNavi signaled megabank endorsement and unlocked cross-sell synergies. Younger investors dominate the user base, while corporate DC channels have become a new on-ramp through auto-rebalancing solutions, which lower all-in costs and raise digital engagement in the Japan asset management market. Suitability and periodic risk profiling rules add operating costs for robo platforms, which encourages innovation in supervised AI-based methods to maintain compliance at scale. As hybrid advice grows, platforms that join automated rebalancing with human check-ins can address both cost control and client confidence.

The median investor outcome in digital channels improves when the platform offers tax-loss harvesting inside NISA wrappers, automatic glidepaths, and transparent fee disclosure presented in plain language. Human advisors continue to play a central role for complex households that face estate planning, cross-border considerations, or concentrated risk, which keeps the core of the channel resilient even as digital share rises. Over time, a steady shift toward digital advice should reduce distribution frictions and expand reach beyond metropolitan centers, improving participation in the Japan asset management market. Managers that invest in modern client interfaces, consolidated reporting, and low-cost diversified building blocks are set to capture this demand. A measured approach to risk profiling and disclosure can build trust and reduce churn through better alignment between portfolio design and client tolerance.

By Client Type: Retail Gains Narrow Institutional Gap

Institutional mandates accounted for 71.27% of assets in 2025, driven by GPIF’s scale, large corporate plans, and prefectural systems that distribute mandates across passive core and specialist active or alternatives sleeves. Retail is expanding at a 17.42% CAGR, spurred by the revised NISA that removed contribution caps. Retail flows have leaned toward foreign-equity index funds, which reflect a desire to diversify currency and earnings exposure beyond domestic benchmarks. Pension reforms that increase DC ceilings and extend eligibility encourage sustained workplace saving, which supports both institutional and retail channels in the Japan asset management market. Institutions are rationalizing mandates and rotating toward alternatives, a trend that aligns with the need for sources of return that are less tied to low domestic yields.

Retail momentum benefits from branch-to-advisory conversions and fee transparency that tilt investors toward low-cost vehicles and advisory structures that clarify value delivered for fees paid. Institutional growth remains steady as governance practices refresh, and as allocators diversify their active risk budget into specialized non-correlated strategies that complement core index holdings. The Japan asset management industry is responding with simplified defaults, lifecycle designs, and modular alternative sleeves tailored for plans with varying operational capacity. Retail and institutional preferences are converging on clarity, cost control, and risk tools, which help both channels adopt similar building blocks with different implementation approaches. This channel blend strengthens the Japan asset management market by broadening the base of long-term wealth accumulators.

By Management Source: Onshore Dominance Faces Offshore Specialization

Onshore-managed assets represented 85.56% in 2025, which reflects home bias, regulatory familiarity, and advantages in navigating domestic approval and reporting processes that favor local stewardship. Offshore-delegated mandates are projected to grow at a 16.85% CAGR as allocators outsource specific exposures to specialists, especially for emerging markets, energy transition infrastructure, and private markets. GPIF’s alternatives database explicitly incorporates offshore managers to close capability gaps in areas like data centers, renewable transmission, and secondaries, which helps diversify return drivers in the Japan asset management market. Foreign entrants are expanding their presence to serve regional banks and pensions seeking alternative sleeves, while new domestic capabilities arise through acquisitions that internalize global platforms. The FSA’s integration of crypto-assets into the Financial Instruments and Exchange Act from January 2026 enables onshore fund managers to deliver exposures that previously required offshore solutions.

Compliance and governance posture remain important differentiators, as adoption of international standards like ISO 37001 bolsters institutional comfort with onshore managers competing for large mandates. The Japan asset management market is balancing the benefits of local control with the specialized returns offered by global partners in targeted asset classes. As domestic teams gain experience and broaden networks, the gap between onshore and offshore execution quality narrows. This allows allocators to decide by total cost, operational resilience, and integration needs rather than by necessity. A pragmatic split of core onshore oversight and selective offshore delegation supports robust portfolio construction for long-horizon investors.

Geography Analysis

Tokyo hosts the majority of asset managers, regulators, and service providers, creating network benefits that reinforce its standing as the nation’s financial epicenter. Osaka ranks as a secondary hub, leveraging historical bank and insurance headquarters to serve western prefectures. Outside these metros, regional banks and credit unions dominate savings pools but lack product breadth, offering entry points for managers willing to extend digital advisory and remote service models.

Government strategy to position the country as a premier international asset management center catalyzes infrastructure upgrades—English documentation, streamlined licensing, and favorable tax treatment—geared toward attracting foreign talent and capital. Pilot zones for fintech innovation in Fukuoka and Sapporo aim to disperse opportunities beyond the capital while supporting nationwide digitization.

Natural disaster risk in the Kanto region propels contingency planning; institutions diversify data-center footprints and encourage flexible work arrangements to ensure continuity. Meanwhile, aging demographics skew more sharply in rural areas, prompting targeted outreach programs that pair digital education with mobile advisory units. Geographic segmentation, therefore, amplifies the scope for differentiated distribution strategies within the Japan asset management market.

Regulatory Landscape

Japan’s asset management regulation is centered on the Financial Services Agency (FSA), with policy framing the industry as a strategic pillar of the financial sector and a lever to shift household savings toward productive investment. Since October 2024, the Japan Asset Management Forum (JAMF) has provided an industry-regulator dialogue platform. It had 57 members as of March 2026 and is running multiple working groups spanning digital transformation and sustainable finance, supporting coordinated implementation.

Reform actions have also targeted market entry and operating models. The FSA has set up a one-stop support office to assist foreign financial institutions through pre-application consultation, registration, and supervision in English. It has also promoted an Emerging Managers Promotion Program (Japanese EMP) that relaxes certain registration requirements for emerging managers not receiving client assets. Amendments effective May 2025 expanded permissible outsourcing for investment managers, including full outsourcing of middle/back-office functions to registered providers and outsourcing of investment execution to specialized fund management companies, which reduces fixed-cost barriers and enables more specialized operating structures.

Value Chain Analysis

The value chain runs from asset owners (households using vehicles such as investment trusts and tax-advantaged accounts, plus institutional allocators such as pensions and insurers) through product manufacturing (investment management business operators, including bank- and securities-affiliated managers and independent firms) to distribution (banks, broker-dealers, advisors, and digital platforms) and supporting infrastructure (custody, fund administration, transfer agency, valuation/NAV calculation, and technology/risk systems). Industry structure remains concentrated, with the top 10 investment management business operators controlling about 60% of total AUM and conglomerate affiliation common among leading firms, reinforcing scale advantages in distribution and operations.

A key operational shift in the chain is the unbundling of non-core functions. Regulatory changes effective May 2025 allow broader outsourcing of middle and back office processes and execution to approved third-party providers, increasing the role of specialized service operators and lowering operational barriers for newer and foreign managers. These changes let them focus more on portfolio management and client service. On the demand side, the New NISA framework introduced in 2024 has been a notable channel for retail inflows into investment trusts. Product architecture has also tilted toward low-cost implementation, with index funds growing to 37% of total market AUM by 2025 (from 10% in 2015), shaping fee models and platform economics across manufacturing and distribution.

Competitive Landscape

The Japan asset management market exhibits moderate concentration, with top domestic managers holding a significant share of assets while foreign firms and domestic specialists expand in targeted niches. Scale-driven consolidation is reshaping capabilities, enabling major players to direct flows into alternatives such as infrastructure debt and private markets. Differentiation is increasingly visible through specialized strategies, including growth equity funds for mid-cap innovators and tokenized REITs that allow fractional ownership and continuous trading. White-space opportunities persist in mass-affluent robo-advisory, alternative sleeves for smaller pensions, and ESG-linked transition strategies that broaden the investable set. At the same time, digital challengers are pushing incumbents to modernize platforms and develop clean-fee products, particularly in defined-contribution accounts.

Technology adoption is central to risk management and compliance, with major managers implementing enterprise risk platforms to enable real-time stress testing and enhanced reporting. Legacy systems in trust-bank and megabank affiliates slow product launch cycles, limiting innovation compared to digital-native entrants that iterate quickly on data and client experience. Foreign managers are selectively expanding where product strength pairs with local distribution capabilities, focusing on alternatives, ETFs, and solutions that complement domestic offerings. Regional banks continue to favor proprietary or affiliated products, maintaining tight access unless managers provide differentiated capabilities and strong client service. Overall, competition is shifting toward platforms that demonstrate operational resiliency, transparent value, and aligned incentives suited to fiduciary oversight.

Fee disclosure reforms have compressed margins for traditional active equity funds, accelerating a move toward zero-load ETFs, clean-fee classes, and advice-led bundles tailored to household budgets. Managers are responding by combining lower-cost index building blocks with higher-margin alternative sleeves to balance economics while delivering client outcomes. Distribution is increasingly oriented toward advisory accounts, where fees are linked to planning, risk monitoring, and measurable service deliverables. Product menus emphasize simplicity and transparency, helping clients compare options and understand fee-service alignment. This evolution favors firms that combine breadth, clarity, and consistent performance, reinforcing the importance of service quality alongside investment capabilities.

Japan Asset Management Industry Leaders

Nomura Asset Management

Nikko Asset Management

Daiwa Asset Management

Sumitomo Mitsui Trust Asset Management

Asset Management One

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy-led efforts to position Japan as a leading asset management center are creating whitespace for new operating models and new entrants, especially where reduced setup friction supports ecosystem participation. The FSA’s one-stop support for foreign institutions, together with the FY2026 Financial Start-up Support Program offering reimbursements of up to JPY 15 million for establishing operations in Japan (with a May 2026 application deadline), supports incremental market entry and local build-outs by specialist managers. The May 2025 reforms that permit fuller outsourcing of middle/back office operations and investment execution also enable managers to scale with lighter local infrastructure, opening space for third-party fund administration, compliance, and delegated execution providers as fund ranges expand.

Product and channel opportunities are clearest where regulation and investor behavior overlap. The New NISA framework (introduced in 2024) has strengthened retail participation in investment trusts and complements the broader shift from deposits to managed products. The JAMF (launched October 2024, 57 members as of March 2026) provides a structured venue to advance digital transformation, sustainable finance, and capability building that managers can translate into new strategies, including transition and ESG-aligned funds, as well as improved client disclosure. Institutional demand for specialist exposures also remains an opening, with allocators using alternatives sleeves and, in some cases, offshore delegation to access capabilities not fully developed onshore. This has encouraged partnerships, acquisitions, and platform build-outs focused on private markets, infrastructure, and other long-duration assets.

Recent Industry Developments

- July 2026: Nomura Asset Management listed the NEXT FUNDS Japan Equity Policy Focus Exchange Traded Fund on the Tokyo Stock Exchange. The launch broadens domestic ETF choice with a policy-linked equity angle and supports the marketwide shift toward transparent, tradable, lower-cost building blocks in portfolio construction.

- April 2026: Amova Asset Management (formerly Nikko Asset Management) commenced operations of its joint venture, Tikehau Amova Investment Management Pte. Ltd., on 2 April 2026 following regulatory approval from the Monetary Authority of Singapore. The move expands the firm’s alternatives-oriented footprint and adds a new route for cross-border product and investment capability development relevant to Japanese allocators seeking specialist exposures.

- March 2025: Daiwa Asset Management executed a capital and business alliance to acquire 51% of Mitsui & Co. Alternative Investments Limited, making it a subsidiary. The acquisition strengthened Daiwa’s alternative investment management capabilities and reflects the sector’s push to build in-house expertise for private markets and other non-traditional asset classes.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Japan asset management market is sized as the total value of assets that are professionally managed for investors in Japan, across major investment portfolios like equity, fixed income, multi-asset, and alternatives. It reflects assets under management (AUM) rather than the fee revenue earned by managers.

Scope exclusions: We exclude self-directed brokerage holdings, custody-only mandates, and enterprise IT asset management tools because they do not represent discretionary investment management AUM.

Segmentation Overview

- By Asset Class

- Equity

- Fixed Income

- Alternative Assets

- Other Asset Classes

- By Firm Type

- Broker-Dealers

- Banks

- Wealth Advisory Firms

- Other Firm Types

- By Mode of Advisory

- Human Advisory

- Robo-Advisory

- By Client Type

- Retail

- Institutional

- By Management Source

- Offshore

- Onshore

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the Japan demand and supply context around managed assets, then aligning it with the definitions used by regulators and industry bodies. In practice, this anchors on Financial Services Agency of Japan releases and statistics, Bank of Japan time series on yields and flows, Japan Investment Advisers Association publications, and Japan Securities Dealers Association materials. We also include select OECD and IMF macro series as a consistency check for broader drivers that can affect AUM over time.

We also review annual reports, investor presentations, and fund disclosures to track product mix changes and distribution shifts that can move AUM, even when headline market conditions look stable. Where needed, we use paid subscriptions for company financials and intelligence, and we review patent databases to track product structuring trends that later show up in flows. These examples are not exhaustive, and other public sources were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test AUM definitions, confirm how mandates are counted, and sanity check growth drivers like retail inflows, institutional reallocations, and alternative allocation appetite. We spoke with a mix of asset managers, distributors, platform and servicing stakeholders, and institutional allocators across Japan, and then reconciled differences through follow-up questions when assumptions did not line up.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | |

| Mid tier: 54% | Functional/Unit leaders: 33% | |

| Smaller Players: 19% | Managers: 55% |

Market-Sizing & Forecasting

The sizing model begins with a top-down rebuild of Japan AUM using investable asset pools and allocation behavior, then maps those totals to professionally managed mandates that meet the study definition. Before final totals are locked, selective bottom-up checks are run using sampled manager AUM disclosures, product-level splits, and channel checks on how assets are reported, so the totals do not drift away from what is observable.

Key inputs used to explain AUM movement include net fund flows by channel, equity and bond market performance (which lifts or compresses AUM even without new money), Japan interest rate levels and yield curve direction, the pace of retail participation through tax-advantaged investment accounts, and shifts in institutional allocations into alternatives and multi-asset strategies. Where disclosure gaps exist, missing splits are filled using proxy ratios from similar mandate types and then adjusted after interview validation.

Forecasts are built using scenario analysis supported by trend-based smoothing of AUM drivers, since market returns and flows can swing year to year. Assumptions on inflow momentum, asset mix, and valuation effects are reviewed with practitioners so the forward path remains realistic and easy to explain.

Data Validation & Update Cycle

Outputs are checked against independent signals such as industry AUM releases, fund flow direction, and macro indicators that should logically move managed assets. If a figure looks unusual, the drivers are re-opened and the inputs are traced back to the specific series or assumption that created the variance, followed by a second analyst review before sign-off.

The model is refreshed annually, and interim updates are made when there are material events like major regulatory changes, sharp market repricing, or large structural shifts in retail participation. Right before delivery, a final review pass is completed so clients receive an up-to-date view with the same definitions kept consistent over time.

Mordor Intelligence's Japan Asset Management Market Size Compared With Other Published Estimates

Published market values for Japan asset management often do not match because some sources size fee revenue, while others size AUM, and the currency timing and portfolio coverage are not always aligned. Differences also come from whether offshore-sourced assets managed by Japan-based teams are included, and how non-discretionary or custody-only assets are treated.

The main gap comes from mixing AUM with revenue-style measures, where Mordor Intelligence keeps the model tied to professionally managed portfolio values. Offshore-sourced assets are counted only when the investment mandate is run by Japan-based managers, and custody-only mandates and self-directed holdings are excluded.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.63 T (2026) | |

| Industry Publisher A | USD 30.30 B (2025) | Sizes a much narrower value pool that reads like revenue or a restricted service scope rather than total AUM, which makes the number structurally smaller even before any growth assumptions are applied. |

| Regional Consultancy B | USD 6.87 T (2024) | Uses an earlier base year and presents a range, and the page-level scope does not clearly state exclusions like custody-only or self-directed assets, which can shift what is counted as managed AUM. |

The spread mainly comes down to what is being measured and what gets counted as managed assets. When scope is kept consistent around discretionary, professionally managed portfolios, and the year and currency basis are clearly stated, the market size becomes easier to reconcile with observable AUM signals and repeatable driver checks.

Key Questions Answered in the Report

What is the Japan asset management market outlook to 2031?

The Japan asset management market is projected to reach USD 10.95 trillion by 2031 at a 14.22% CAGR from USD 5.63 trillion in 2026, supported by pension reform, higher policy rates, and product innovation.

Which asset classes are set to grow fastest in Japan through 2031?

Alternative assets are forecast to expand at a 16.34% CAGR as GPIF and corporate pensions build allocations to infrastructure, private equity, and real assets, complementing equity-led core portfolios.

Which channels and firm types are gaining share in Japan?

Wealth advisory firms and registered investment advisors are projected to grow at a 15.81% CAGR, while robo-advisory expands at a 20.18% CAGR as hybrid advice models gain traction across segments.

How is offshore management expected to grow?

Offshore-delegated assets are projected to grow at a 16.85% CAGR through 2031, reflecting increasing investor appetite for global diversification and access to international expertise.

Which client segment dominated Japan's asset management market?

Institutional investors dominate, accounting for 71.27% of assets in 2025, driven by large mandates from GPIF, corporate pension plans, and prefectural systems.

Page last updated on: