Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 84.24 Billion |

| Market Size (2030) | USD 106.85 Billion |

| Growth Rate (2025 - 2030) | 4.87% CAGR |

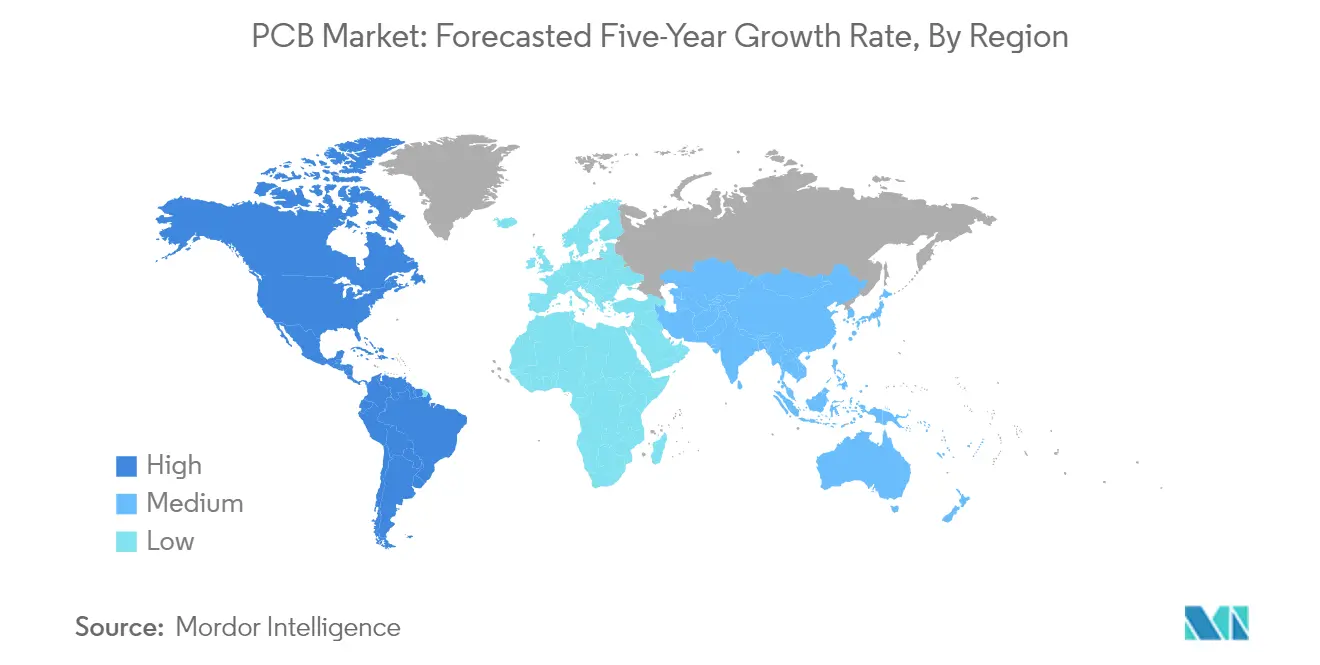

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Printed Circuit Board (PCB) Industry Analysis

The Printed Circuit Board Industry is expected to grow from USD 84.24 billion in 2025 to USD 106.85 billion by 2030, at a CAGR of 4.87% during the forecast period (2025-2030).

The Printed Circuit Board (PCB) industry is intricately linked to the broader dynamics of the electronics and technology sectors. Emerging technologies such as 5G, IoT, and AI are not only reshaping industries but also driving the demand for advanced PCBs, influencing PCB design to support these innovations. For example, the proliferation of IoT devices, projected to grow from 12,393 million in 2023 to 25,150 million by 2027, underscores the increasing reliance on PCBs in diverse applications. Concurrently, sustainability is becoming a pivotal consideration, influencing PCB manufacturing practices towards the adoption of recyclable and biodegradable materials. Geographically, the Asia-Pacific region remains a powerhouse in PCB production, with leading printed circuit board manufacturers in China leading the charge, while other regions are actively pursuing reshoring and supply chain diversification to bolster resilience.

Several specific trends are defining the trajectory of the PCB industry. The ongoing miniaturization of electronic devices has spurred demand for High-Density Interconnect (HDI PCBs) and flexible PCBs, which provide compact and efficient solutions. The automotive industry, particularly with the rise of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), represents a significant growth driver in the automotive PCB sector, as the PCB content in EVs is notably higher compared to traditional vehicles. The rapid adoption of EVs, evidenced by the increase in global sales from 206,000 units in 2013 to 10,522,000 units in 2022, highlights this trend. Additionally, consumer electronics, including smartphones and wearable devices, continue to be a major segment, with advancements in PCB design and materials enhancing the performance and reliability of these products.

The trends shaping the PCB market can be viewed across multiple dimensions. At a macro level, technological advancements and sustainability imperatives are key drivers. Regionally, the dominance of Asia-Pacific in the global PCB market and the strategic push for reshoring are influencing production dynamics. For instance, the announcement by Kaynes Solutions in August 2023 to invest USD 100 million in a PCB manufacturing unit in Karnataka, India, exemplifies the regional focus on expanding manufacturing capabilities. On an industry-specific level, the demand for HDI and flexible PCBs is being propelled by the miniaturization of devices and the evolving needs of sectors such as automotive and consumer electronics. Collectively, these trends underscore the PCB market's critical role in enabling technological innovation and addressing environmental challenges, solidifying its position as a cornerstone of the global electronics industry.

Printed Circuit Board (PCB) Industry Industry Segmentation

Rising Demand for Miniaturization of Technology

The trend towards miniaturization in technology is emerging as a pivotal force shaping the market landscape. This movement is driving innovation in PCB design and production of components, enabling the development of smaller, more efficient systems. In consumer electronics, for instance, the demand for compact devices such as smartphones and wearables necessitates intricate and space-efficient circuit designs. This has spurred advancements in manufacturing techniques and materials, fostering the growth of technologies like High-Density Interconnect (HDI PCBs) and flexible PCBs, which are instrumental in achieving miniaturization. Moreover, the proliferation of the Internet of Things (IoT) has further accelerated this trend, as IoT devices often require compact yet powerful electronic systems, driving innovation in PCB design. Looking ahead, the miniaturization trend is poised to continue driving innovation, enhancing efficiency, and reshaping product design across industries, influencing PCB industry trends.

Beyond consumer electronics, miniaturization is making significant inroads in sectors such as healthcare and automotive. In healthcare, the push for portable and minimally invasive medical devices has led to the adoption of compact and efficient electronic components, including specialized medical PCBs. Similarly, in the automotive industry, the integration of advanced features like driver assistance systems and connectivity solutions hinges on miniaturized technology. The ability to produce smaller, lighter, and more efficient components, such as PCB components, is becoming increasingly critical to meet the evolving demands of these industries. This trend not only enhances product functionality but also contributes to sustainability and cost-effectiveness, underscoring its role as a key driver of market growth.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Demand from End-user Industries

The expanding demand from diverse end-user industries is another significant factor propelling market growth. Sectors such as consumer electronics, automotive, healthcare, and industrial applications are increasingly relying on advanced electronic components, such as PCBs, to enhance their offerings. In consumer electronics, the widespread adoption of devices like smartphones, tablets, and smart home systems has heightened the need for efficient and reliable components. This has catalyzed innovation in electronic system design and PCB manufacturing, ensuring these systems meet the stringent performance and reliability standards demanded by modern applications. The automotive sector is also a major contributor, with the transition towards electric and autonomous vehicles driving the need for sophisticated electronic systems, including specialized automotive PCBs. These systems are essential for functionalities such as navigation, safety, and connectivity, highlighting their critical role in the industry's evolution.

In healthcare, the growing use of advanced medical devices and diagnostic tools is fueling demand for specialized electronic components, such as medical PCBs. Devices such as imaging systems, monitors, and wearable health trackers depend on reliable and efficient electronic systems to deliver accurate and consistent performance. Similarly, industrial applications are leveraging advanced electronics, including industrial PCBs, to enable automation, monitoring, and control processes. The increasing complexity and sophistication of these applications demand high-performance components tailored to specific industry requirements. Collectively, the rising demand across these diverse end-user industries underscores the importance of this market driver in shaping the trajectory of growth and innovation.

Printed Circuit Board (PCB) Industry Trends

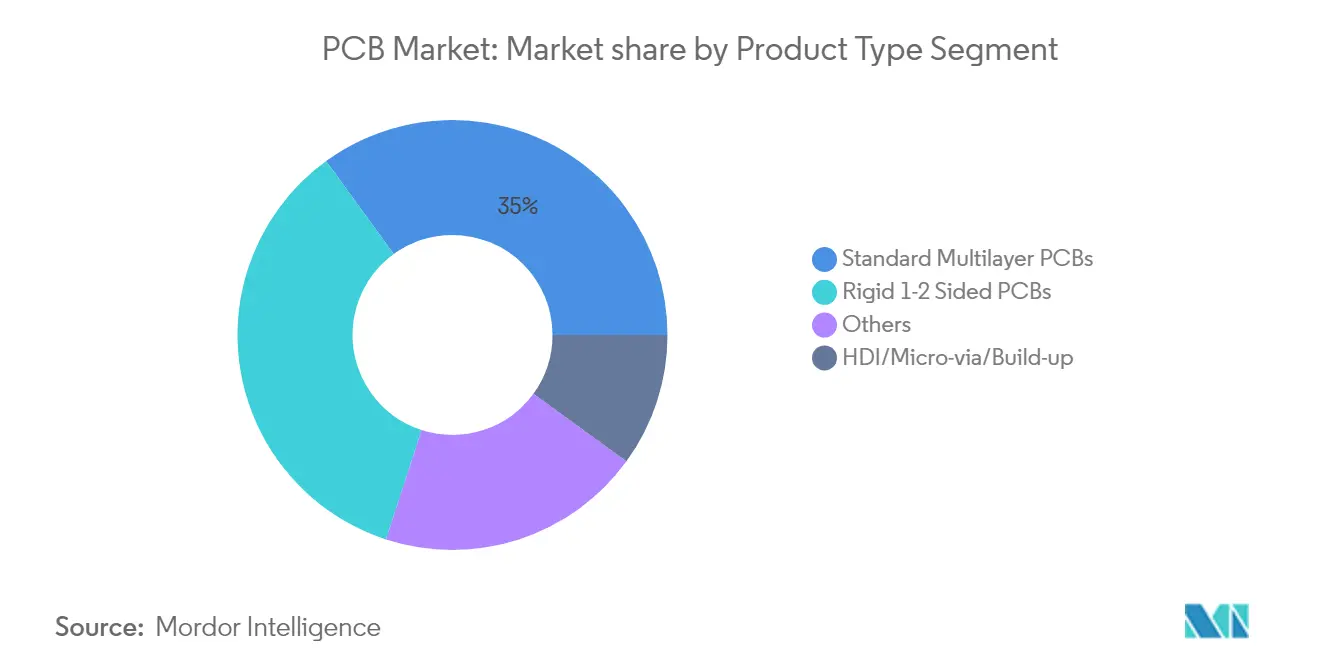

Standard Multilayer PCBs Market Analysis

Standard Multilayer PCBs represent the largest segment in the printed circuit board market, holding a significant market share of approximately 35% as of 2022. This dominance is attributed to their widespread application across various industries, including consumer electronics, automotive, and telecommunications. The ability of multilayer PCBs to support complex circuitry in a compact form factor makes them indispensable in modern electronic devices. The segment benefits from continuous advancements in PCB manufacturing technologies, which have improved their reliability and performance. Additionally, the increasing demand for miniaturized and high-performance electronic devices has further driven the adoption of multilayer PCBs. Companies in this segment are focusing on innovation and cost optimization to maintain their competitive edge. As a result, Standard Multilayer PCBs continue to play a pivotal role in the growth and evolution of the PCB market.

Rigid-flex PCBs Market Analysis

Rigid-flex PCBs are the fastest-growing segment in the PCB market, with an impressive forecasted CAGR of approximately 10% from 2023 to 2028. This growth is driven by their unique combination of the durability of rigid PCBs and the flexibility of flexible PCBs, making them ideal for applications requiring complex geometries and dynamic bending. Industries such as aerospace, medical devices, and consumer electronics are increasingly adopting rigid-flex PCBs due to their ability to reduce assembly errors and improve reliability. The segment is also benefiting from the trend towards miniaturization and lightweight designs in electronic devices. Furthermore, advancements in materials and manufacturing processes have enhanced the performance and cost-effectiveness of rigid-flex PCBs. These factors collectively contribute to the robust growth trajectory of this segment.

Other Product Type Segments in PCB Market Analysis

The remaining segments, including Rigid 1-2 Sided PCBs, HDI/Micro-via/Build-up PCBs, flexible PCBs, and Others, each contribute uniquely to the PCB market. Rigid 1-2 Sided PCBs are widely used in simpler electronic devices due to their cost-effectiveness and ease of manufacturing. HDI/Micro-via/Build-up PCBs are gaining traction for their high-density interconnect capabilities, which are essential for advanced applications such as smartphones and high-performance computing. Flexible PCBs are valued for their adaptability and are increasingly used in wearable devices and automotive applications. The 'Others' category encompasses specialized PCBs tailored for niche applications, showcasing the diversity and innovation within the market. Collectively, these segments enhance the overall market landscape by addressing a wide range of consumer and industrial needs, ensuring the PCB market remains dynamic and resilient.

PCB Market End-user Industry Segment Analysis

Consumer Electronics Market Analysis

Consumer Electronics is the largest segment in the PCB market, holding approximately 34% of the global market share as of 2022. This segment is characterized by its extensive application in devices such as smartphones, televisions, laptops, and gaming consoles, which rely heavily on PCBs for their functionality. The demand for compact, lightweight, and efficient PCBs has driven innovation in this sector, with flexible and rigid-flex PCBs gaining prominence. The increasing adoption of advanced consumer electronics, coupled with the integration of cutting-edge technologies, has further solidified this segment's dominance. Trends such as the rise of foldable smartphones and the growing emphasis on durability and performance in electronic devices are shaping the market dynamics. Additionally, the global proliferation of smartphones and other portable devices continues to fuel the demand for high-quality PCBs. As a result, the Consumer Electronics segment remains a cornerstone of the PCB market, driving significant growth and innovation.

Automotive Market Analysis

The Automotive segment is the fastest-growing in the PCB market, with a projected CAGR of approximately 5% from 2023 to 2028. This growth is driven by the increasing adoption of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), which require sophisticated PCB designs to support their functionalities. The shift towards sustainable and energy-efficient transportation solutions has further accelerated the demand for PCBs in this sector. Innovations in automotive electronics, such as infotainment systems, battery management systems, and autonomous driving technologies, are also contributing to this rapid expansion. The integration of PCBs in critical automotive components ensures reliability and performance, making them indispensable in modern vehicles. Additionally, government incentives and policies promoting EV adoption are bolstering the market for automotive PCBs. This segment's growth trajectory highlights its pivotal role in the evolution of the automotive industry.

Other End-user Industry Segments in PCB Market Analysis

The remaining segments, including Industrial Electronics, Healthcare, Aerospace and Defense, and Other End-user Industries, each play a vital role in the PCB market. Industrial Electronics relies on PCBs for automation and control systems, driving efficiency in manufacturing and production processes. The Healthcare segment benefits from PCBs in medical devices such as diagnostic equipment and wearable health monitors, which are becoming increasingly sophisticated. Aerospace and Defense applications demand high-reliability PCBs for mission-critical systems, including avionics and communication devices. Lastly, Other End-user Industries encompass diverse applications, from energy systems to educational tools, showcasing the versatility of PCBs. These segments collectively contribute to the market's diversity and resilience, addressing a wide range of technological and industrial needs. Continuous advancements in PCB technology and tailored solutions for specific applications ensure steady growth across these sectors.

Printed Circuit Board (PCB) Industry Overview

North America PCB Market Analysis

The North America PCB market is projected to account for approximately 4% of the global PCB market size in 2024. This region plays a pivotal role in the PCB industry due to its advanced technological infrastructure and the presence of key industries such as aerospace, defense, and automotive, which heavily rely on PCB applications. Growth in this market is driven by increasing demand for advanced electronics in sectors like telecommunications and healthcare, as well as the rising adoption of electric vehicles. Recent trends indicate a focus on domestic manufacturing, supported by government initiatives like the Defense Production Act and the Protecting Circuit Boards and Substrates Act of 2023, aimed at revitalizing the PCB manufacturing industry. Additionally, collaborations between global and regional players are fostering innovation and enhancing the region's competitive edge in the global PCB market.

Europe PCB Market Analysis

The Europe PCB market experienced approximately a 1% PCB CAGR from 2019 to 2024, reflecting its steady yet modest growth trajectory. Europe plays a pivotal role in the global PCB market due to its advanced technological infrastructure and its focus on innovation, particularly in sectors like automotive, aerospace, and industrial automation. Notable PCB industry trends include the increasing adoption of electric vehicles, advancements in 5G technology, and the region's commitment to sustainability, as evidenced by initiatives like the development of recyclable PCB substrates. Recent efforts highlight Europe's initiative to enhance local semiconductor production and reduce dependency on external supply chains, supported by government policies such as the European Chips Act. Additionally, the region's emphasis on high-tech manufacturing and environmental standards reflects a positive printed circuit board industry outlook, positioning it as a leader in sustainable and innovative PCB solutions.

Asia PCB Market Analysis

The Asia PCB market is characterized by its pivotal role in the PCB manufacturing industry, contributing significantly to the global PCB market size, driven by the region's robust industrial base and technological advancements. Key growth drivers include the increasing demand for consumer electronics, automotive electronics, and telecommunications infrastructure, which necessitate advanced PCB solutions. Notable trends include the shift towards high-density interconnect (HDI) and the growth of the flexible PCB industry, catering to the miniaturization and multifunctionality requirements of modern devices. Additionally, countries like China, Taiwan, and South Korea dominate the market, hosting some of the largest PCB manufacturers in the world due to their established supply chains, cost-effective manufacturing, and innovation in PCB technologies. The region's strategic focus on enhancing production capabilities and adopting cutting-edge technologies positions it as a leader in the global PCB industry.

Australia and New Zealand PCB Market Analysis

The Australia and New Zealand PCB market is characterized by its strategic importance in the global electronics supply chain, serving as a hub for innovation and specialized manufacturing. The region's PCB market growth is driven by increasing demand for advanced electronics in industries such as telecommunications, automotive, and healthcare, coupled with government initiatives promoting local manufacturing and technological advancements. A notable PCB industry trend is the adoption of environmentally sustainable practices in PCB production, aligning with global standards and consumer expectations. Additionally, the rise of IoT and smart devices has spurred the need for high-performance PCBs, fostering innovation and investment in the sector. The market's evolution reflects a shift towards high-value, technologically advanced products, positioning the region as a key player in the global PCB industry.

Latin America PCB Market Analysis

The Latin America PCB market is characterized by its growing importance as a strategic hub in the PCB manufacturing industry, driven by nearshoring trends and increasing investments in electronics and automotive industries. Countries like Mexico are emerging as key players, leveraging their proximity to North American markets and benefiting from collaborations with the United States and Canada to develop robust PCB production capabilities. The region is witnessing a surge in demand for PCBs due to the expansion of consumer electronics manufacturing, contributing to PCB market growth, with Mexico being a global leader in the production of flat-screen TVs and computers. Additionally, the adoption of electric vehicles (EVs) in countries such as Brazil is fostering the growth of power electronics, further boosting the PCB market. Government initiatives and foreign investments, particularly from Asian companies, are enhancing the region's manufacturing infrastructure, making it a pivotal area for PCB production and innovation.

Middle East and Africa PCB Market Analysis

The Middle East and Africa region is emerging as a significant player in the global PCB market, aligning with recent PCB market trends driven by its strategic initiatives and growing technological infrastructure. Key growth drivers contributing to PCB market growth include government investments in renewable energy projects, the expansion of electric vehicle infrastructure, and the adoption of advanced manufacturing technologies. Notable PCB industry trends include the UAE's Industry 4.0 initiatives and Saudi Arabia's NEOM project, which emphasize the integration of smart technologies and sustainable practices. Additionally, the region's focus on semiconductor and chip manufacturing, as evidenced by events like the World Semiconductor and Chip Summit in Oman, highlights its commitment to becoming a hub for high-tech industries. These developments underscore the region's potential to contribute significantly to the global PCB market through innovation and localized production capabilities.

Printed Circuit Board (PCB) Industry Leaders

Top companies in the PCB Market

- Jabil Inc.

- Wurth elektronik group (Wurth group)

- TTM Technologies Inc.

- Becker & Muller Schaltungsdruck Gmbh

- Advanced Circuits Inc.

- Sumitomo Electric Industries Ltd (Sumitomo Corporation)

- Murrietta Circuits

- Unimicron Technology Corporation

- Tripod Technology Corporation

- AT&S Austria Technologie & Systemtechnik AG

- Nippon Mektron Ltd (nok Group)

- Zhen Ding Technology Holding Limited

The PCB market is characterized by continuous innovation, with the largest PCB manufacturers advancing technologies such as high-density interconnect (HDI) and flexible PCBs. Firms demonstrate operational agility by adapting to trends like miniaturization and the integration of 5G and IoT technologies. Strategic initiatives include capacity expansions, R&D investments, and partnerships with key industry players. Geographic expansion is also a focus, with firms establishing manufacturing facilities in regions to meet local demand and optimize supply chains.

Competitive landscape shaped by global leaders

The global PCB market features a mix of global conglomerates and specialized manufacturers, with firms like Zhen Ding Technology and TTM Technologies being prominent. Market consolidation is moderate, with leading players holding a significant PCB market share, reflecting a competitive yet concentrated environment. Mergers and acquisitions are a key trend, with companies acquiring specialized manufacturers to enhance capabilities and market presence. Such activities are aimed at diversifying product offerings and entering new geographical markets.

Innovation and specialization drive future success

Incumbents can grow by investing in advanced technologies such as AI-assisted PCB design and manufacturing. New entrants or smaller players may find opportunities in niche markets, such as flexible PCBs for wearables or high-frequency PCBs for telecommunications. The market's reliance on key sectors like automotive and consumer electronics underscores the importance of tailored solutions and strong client relationships. Regulatory pressures, particularly in sustainability, are prompting shifts towards eco-friendly materials and processes, which could redefine competitive advantages.

PCB Market Leaders

-

Jabil Inc.

-

Wurth elektronik group (Wurth group)

-

TTM Technologies Inc.

-

Becker & Muller Circuit Printing GmbH

-

Advanced Circuits Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

PCB Market News

- January 2024 - Amber Group signed an agreement with Korean Circuit to strengthen its printed circuit board (PCB) portfolio. The company also acquired a 60% stake in the South Korean firm. According to Amber, this association will encompass the entire portfolio of PCBs required for numerous applications and strengthen the company's presence in the market studied.

- January 2024 - Jiva Materials, in partnership with the University of Portsmouth, announced the development of a new laminate called Soluboard to replace the glass fiber epoxy laminate currently used in the majority of PCBs. This launch aims to tackle the global problem of e-waste, which contributes to rising carbon emissions and ground, water, and air pollution.

Printed Circuit Board (PCB) Industry News

The study tracks the revenue accrued through the sales of printed circuit boards (PCBs) by various players in the global market. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which accounts for market estimations and growth rates. The study further analyzes the overall impact of COVID-19 and other macroeconomic factors on the global market. The scope of this report encompasses the sizing and forecasts for the various market segments.

The printed circuit board (PCB) market is segmented into type (standard multilayer PCBS, rigid 1-2 sided PCBS, HDI/micro-via/build-up, flexible PCB, rigid-flex PCB, and others), by end-user industry (industrial electronics, healthcare, aerospace and defense, automotive, communications, consumer electronics, and other end-user industries), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The report offers market forecasts and size in value (USD) for all the above segments.

| By Product Type | Standard Multilayer PCBs |

| Rigid 1-2 Sided PCBs | |

| HDI/Micro-via/Build-up | |

| Flexible PCBs | |

| Rigid-flex PCBs | |

| Others | |

| By End-user Industry | Industrial Electronics |

| Healthcare | |

| Aerospace and Defense | |

| Automotive | |

| Consumer Electronics | |

| Other End-user Industries | |

| By Geography*** | North America |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

By Product Type

| Standard Multilayer PCBs |

| Rigid 1-2 Sided PCBs |

| HDI/Micro-via/Build-up |

| Flexible PCBs |

| Rigid-flex PCBs |

| Others |

By End-user Industry

| Industrial Electronics |

| Healthcare |

| Aerospace and Defense |

| Automotive |

| Consumer Electronics |

| Other End-user Industries |

By Geography***

| North America |

| Europe |

| Asia |

| Australia and New Zealand |

| Latin America |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Printed Circuit Board (PCB) Industry Research FAQs

How big is the PCB Market?

The PCB Market size is expected to reach USD 84.24 billion in 2025 and grow at a CAGR of 4.87% to reach USD 106.85 billion by 2030.

What is the current PCB Market size?

In 2025, the PCB Market size is expected to reach USD 84.24 billion.

Which is the fastest growing region in PCB Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in PCB Market?

In 2025, the Asia Pacific accounts for the largest market share in PCB Market.

What years does this PCB Market cover, and what was the market size in 2024?

In 2024, the PCB Market size was estimated at USD 80.14 billion. The report covers the PCB Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the PCB Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.