Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

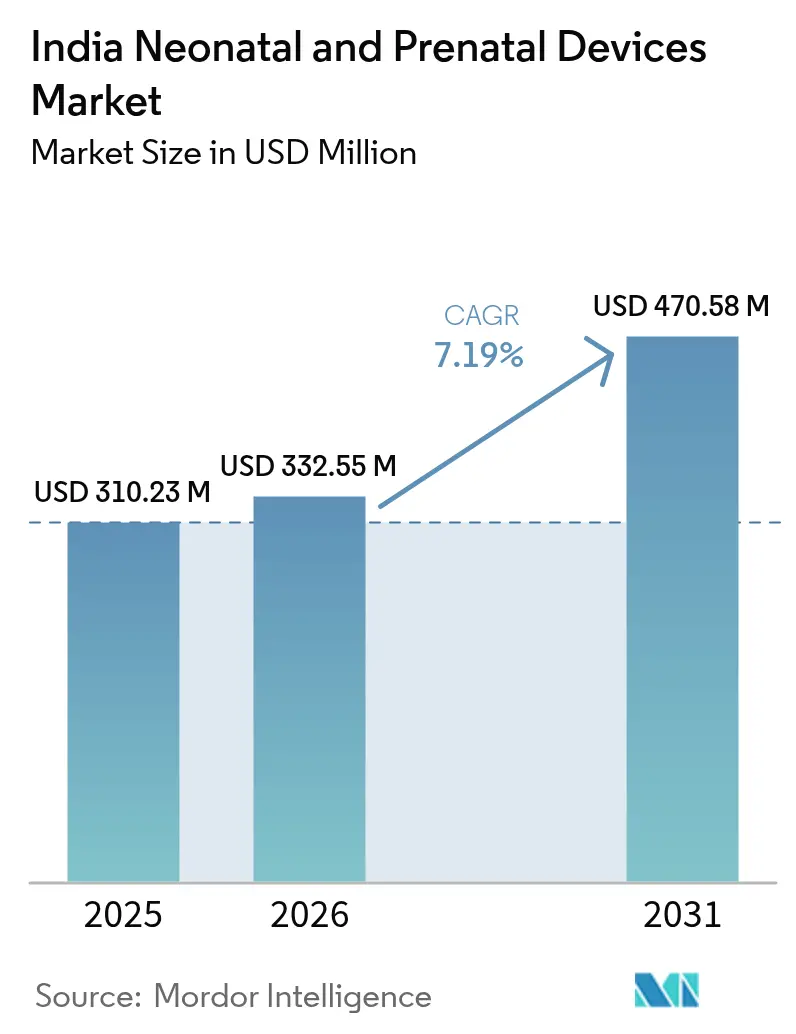

| Base Year Market Size (2025) | USD 310.23 Million |

| Market Size (2026) | USD 332.55 Million |

| Market Size (2031) | USD 470.58 Million |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Neonatal And Prenatal Devices Market Analysis by Mordor Intelligence

The India neonatal and prenatal devices market size was valued at USD 310.23 million in 2025 and estimated to grow from USD 332.55 million in 2026 to reach USD 470.58 million by 2031, at a CAGR of 7.19% during the forecast period (2026-2031). Strong public-sector funding, rapid NICU expansion in secondary cities, and accelerating adoption of AI-enabled monitoring systems are widening clinical coverage while pushing average selling prices upward. Hospitals continue to anchor demand, yet specialty clinics and home-based monitoring solutions are gaining share as healthcare delivery models diversify [1]Ministry of Health and Family Welfare, “Annual Report 2024-25,” mohfw.gov.in . Domestic manufacturing incentives are lowering landed costs for selected devices and trimming import dependence, while stricter quality regulations are encouraging product upgrades. Taken together, these forces are expanding the addressable base of clinicians and patients who can access advanced monitoring therapies.

Key Report Takeaways

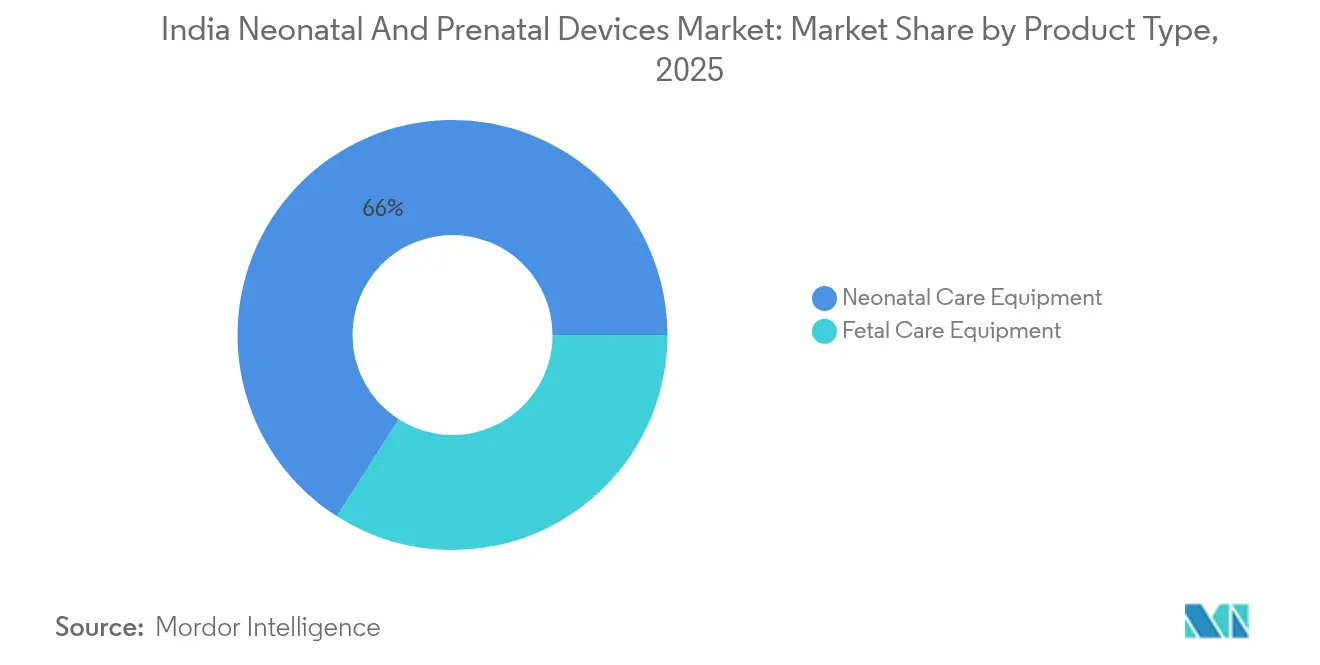

- By product type, neonatal care equipment led with 65.96% revenue share in 2025, while fetal care equipment is projected to advance at an 8.03% CAGR through 2031.

- By end user, hospitals held 49.20% share in 2025, and neonatal and pediatric specialty clinics are forecast to grow at an 8.08% CAGR during 2026-2031.

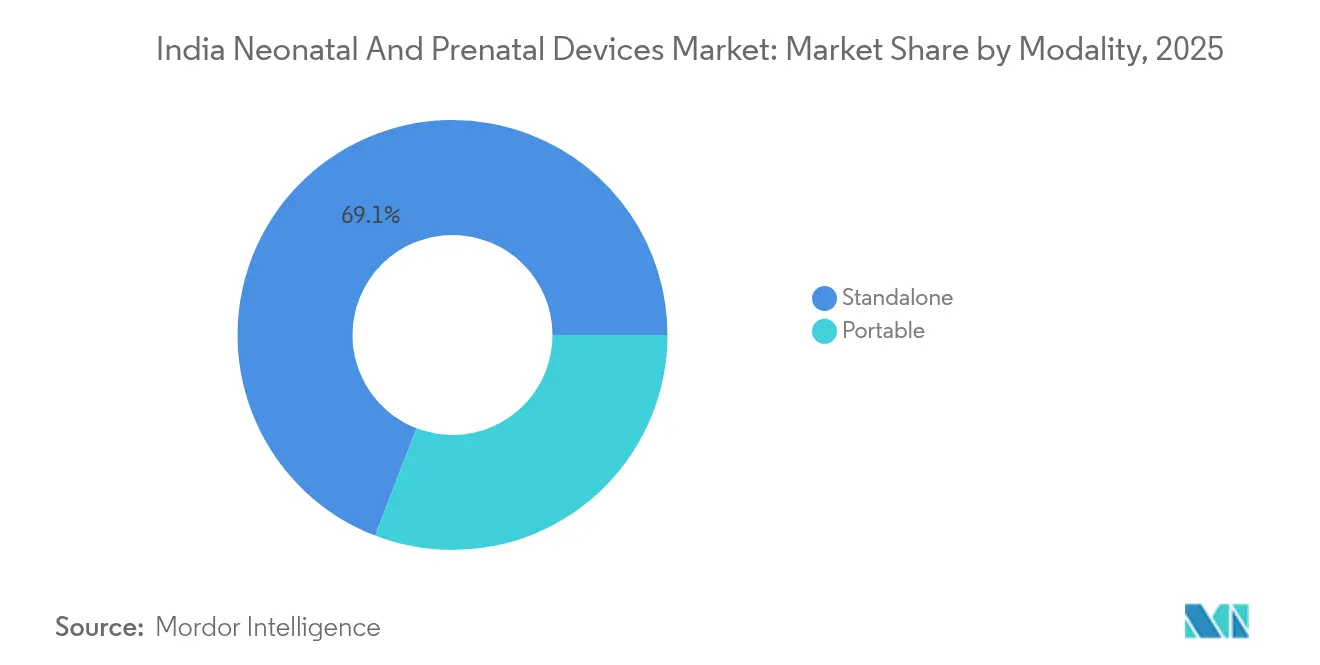

- By modality, standalone systems accounted for 69.14% share in 2025, whereas portable solutions are set to rise at an 8.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Neonatal And Prenatal Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid NICU-bed expansion in Tier 2/3 cities | +1.8% | Tier 2/3 cities, rural catchment areas | Medium term (2-4 years) |

| Shift toward portable and home-based monitoring | +1.2% | Global, with early gains in metro cities | Long term (≥ 4 years) |

| Production-Linked Incentive (PLI) scheme boosts local supply | +1.5% | National manufacturing hubs | Medium term (2-4 years) |

| AI-enabled predictive analytics embedded in devices | +0.9% | Tier 1 cities, premium healthcare segments | Long term (≥ 4 years) |

| Import-substitution push amid high import dependence | +1.1% | National, with focus on manufacturing zones | Medium term (2-4 years) |

| Rise in high-risk pregnancies & late maternal age | +0.7% | Urban centers, educated demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid NICU-bed expansion in Tier 2 and 3 cities drives equipment demand

District hospitals operated 2,847 functional NICUs in 2024, marking a 34% rise since 2020 [2]National Health Mission, “NICU Infrastructure Development Report 2024,” nhm.gov.in . The Ayushman Bharat Health Infrastructure Mission is channeling USD 7.8 billion toward maternal and child health upgrades, prompting private hospital chains to add neonatal units in secondary cities. Higher disposable income and stronger insurance penetration support this wave of construction. Rising bed capacity lifts orders for incubators, phototherapy lamps, and multi-parameter monitors, with procurement teams favoring models that lower total cost of ownership. Vendors that can bundle training, maintenance, and remote support hold a pricing edge.

PLI scheme catalyzes domestic manufacturing capabilities

The medical-device PLI scheme earmarks USD 60 million for firms that expand Indian production of high-end neonatal and fetal equipment. Twenty-one manufacturers have qualified for rebates worth 5-7% of incremental sales [3]Department of Pharmaceuticals, “Production Linked Incentive Scheme for Medical Devices,” pharmaceuticals.gov.in . BPL Medical Technologies invested USD 12 million to extend its incubator line, and Phoenix Medical Systems lifted plant throughput by 40%. Faster product approvals and duty concessions are compressing payback periods, narrowing price gaps with imported devices, and improving after-sales response times.

AI-enabled predictive analytics transforms neonatal monitoring

Artificial-intelligence dashboards can flag sepsis or respiratory distress six to twelve hours sooner than standard alarms. The Edison platform from GE Healthcare cut false alerts by 23% and boosted early sepsis detection by 18% across 150 Indian NICUs. Mindray ventilators now self-titrate oxygen delivery, reducing clinician workload in settings where each neonatologist may oversee eighteen to twenty beds. Uptake is strongest in Tier 1 hospitals that can absorb premium pricing; however, domestic manufacturing scale-up is set to push median selling prices lower, enabling wider diffusion by 2028.

Import-substitution momentum builds amid supply-chain vulnerabilities

Imports still cover 85% of advanced neonatal hardware. A new Quality Control Order mandates BIS certification for twenty-three device classes, and domestic players that meet the norm earn accelerated Central Drugs Standard Control Organisation clearance. Skanray Technologies lifted its share in portable ultrasound systems to 15% after leveraging the regulatory shift. Faster domestic approvals—now eight months rather than eighteen for repeat applicants—shorten commercialization cycles and encourage local innovation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cap-ex & maintenance cost for advanced systems | -1.4% | Tier 2/3 cities, public hospitals | Short term (≤ 2 years) |

| Shortage of trained neonatologists & biomedical engineers | -1.1% | National, acute in rural areas | Long term (≥ 4 years) |

| Fragmented procurement across public hospitals | -0.8% | State-level public healthcare systems | Medium term (2-4 years) |

| Data-privacy gaps for connected devices | -0.6% | Urban centers with digital infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital expenditure constrains adoption of advanced systems

Outfitting a ten-bed NICU demands USD 1.2 million to USD 2 million, and annual maintenance averages 8-12% of equipment value. Budget limitations steer many small hospitals toward stripped-down monitors that meet minimal clinical needs. Lowest-price bid rules in government tenders often elevate upfront savings over lifecycle economics, resulting in frequent repairs and higher downtime. Finance leasing and pay-per-use models are emerging but remain under-penetrated.

Workforce shortage limits equipment utilization and market expansion

India fields only 1,200 certified neonatologists compared with a recommended 1:10,000 live-birth ratio. Less than 5,000 biomedical engineers are available to service a device universe spread across 70,000 facilities. Limited operator expertise discourages hospitals from procuring sophisticated ventilators or AI-driven monitors. Expanded fellowship seats and tele-mentoring programs offer relief, yet meaningful capacity gains will surface only after 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Neonatal Equipment Dominance Faces Fetal Care Innovation

Neonatal care devices captured 65.96% of the India neonatal and prenatal devices market share in 2025. Government policy requires every district hospital to house at least six NICU beds, which secures recurring demand for incubators, phototherapy units, and ventilators. Phoenix Medical Systems supplies 25% of domestic incubators with designs that withstand voltage fluctuations and dusty environments. Hospitals also favor integrated monitoring platforms that combine pulse oximetry, ECG, and temperature tracking to optimize bedside space.

Fetal care equipment is projected to record an 8.03% CAGR through 2031, the fastest among all product groups. Rising maternal age and elective prenatal screening are normalizing electronic fetal monitor use in private clinics. AI-embedded cardiotocography units from GE Healthcare can identify distress patterns thirty minutes earlier than standard monitors, which helps obstetricians lower emergency intervention rates. Portable Doppler probes and handheld ultrasound scanners are also gaining favor for outreach camps and home visits. As technology costs fall, the India neonatal and prenatal devices market size for fetal devices is expected to expand beyond metro clusters toward peri-urban areas.

By End User: Hospital Dominance Challenged by Specialty Clinic Growth

Hospitals accounted for 49.20% of the India neonatal and prenatal devices market in 2025. Public facilities handle 65% of institutional births, creating a baseline demand for standard-spec monitors that comply with procurement guidelines. Large private chains are now segmenting their maternity wings into level-II and level-III NICUs to command premium tariffs. These networks prize devices with remote diagnostics because centralized engineering teams manage multiple campuses.

Neonatal and pediatric specialty clinics are forecast to grow at an 8.08% CAGR during 2026-2031. Urban parents value personalized care and shorter wait times that such clinics offer. Stand-alone neonatal centers in Bengaluru and Chennai manage complex cases referred from satellite towns, pushing up demand for high-frequency ventilators and servo-controlled warmers. Maternity and birthing centers, advancing at 7.56% CAGR, prefer compact equipment footprints. Home-care teams are beginning to rent portable monitors for post-discharge follow-up, hinting at a nascent yet promising service sub-segment.

By Modality: Portable Solutions Gain Momentum Despite Standalone Prevalence

Standalone systems commanded 69.14% of revenue in 2025 as hospital architects still design NICUs around fixed workstations. Integrated servers, larger screens, and built-in data gateways deliver uninterrupted tracking required for critical care. Device makers bundle these consoles with multiyear service pacts that guarantee parts availability and scheduled calibration.

Portable equipment is projected to log an 8.18% CAGR through 2031. Handheld ultrasound devices and battery-powered monitors enable physicians to reach patients in remote clinics or emergency wards without reconfiguring infrastructure. During the COVID-19 pandemic, field hospitals and isolation wards accelerated portable adoption, a trend that has persisted because administrators appreciate redeployment flexibility. As price gaps shrink, the India neonatal and prenatal devices market size for portable devices will broaden to primary health centers, mobile medical units, and even home-care settings.

Geography Analysis

Southern and western states together controlled 57.55% of the India neonatal and prenatal devices market in 2025. Tamil Nadu led with 16.05% share, supported by 450 NICUs across public and private sectors and a dense medical device manufacturing corridor. Karnataka followed at 14.70% share, buoyed by Bengaluru’s cluster of healthcare start-ups and multi-hospital chains that standardize procurement. Maharashtra contributed 12.95% share, with Mumbai and Pune anchoring demand from tertiary centers and acting as distribution nodes for western India.

Northern India, comprising Delhi NCR and Uttar Pradesh, generated 28.25% share in 2025. Uttar Pradesh posted 8.55% share; ongoing Ayushman Bharat investments are elevating equipment density, although specialist shortages persist. Neonatal monitors with simplified interfaces are selling well because clinicians can train nursing staff rapidly. Delhi NCR hospitals demonstrate early adoption of AI-ready monitors, creating reference sites for vendors who later scale to adjoining states. Eastern states, led by West Bengal and Odisha, captured 14.20% share. Budgetary ceilings restrict high-end purchases, but tender wins by Apollo Hospitals and similar operators are raising the bar for device specifications. Portable ultrasound units that run on extended batteries fit outreach camps in hilly terrain. Government projects funded by multilateral agencies are also upgrading district hospitals, adding steady but modest order volumes.

Competitive Landscape

The top five suppliers hold a significant share, signaling a moderately concentrated arena. GE Healthcare, Philips Healthcare, and Medtronic anchor the premium tier with broad portfolios and long-term service contracts. Domestic challengers have leveraged the PLI scheme to sharpen pricing and shorten delivery cycles. Local firms design power-backed modules and dust-resistant casings that match Indian site realities, and they court secondary-city hospitals through in-language training.

Competition increasingly hinges on solution breadth rather than standalone features. Vendors now pitch bundled NICU packages that fold in bedside monitors, warmers, and ventilators, plus staff training and cloud analytics. Contracts often span seven to ten years, locking in consumables and maintenance revenue. White-space remains in Tier 3 cities and rural districts where affordability barriers persist. Creative leasing and subscription models that spread costs across operational budgets can unlock fresh volumes.

International firms are responding with localization strategies. GE Healthcare is building a Chennai plant that can supply Edison-ready monitors for India and Southeast Asia. Philips co-developed wireless neonatal sensors with Apollo Hospitals to cut caregiver workload. Medtronic secured CDSCO clearance for a cloud-linked fetal monitor that supports remote consultations in areas with scarce obstetricians. Such moves illustrate how the India neonatal and prenatal devices industry is shifting from import dependency toward a hybrid model where global and local players co-create products.

India Neonatal And Prenatal Devices Industry Leaders

Atom Medical Corporation

Dragerwerk AG & Co. KGaA

GE Healthcare

Koninklijke Philips NV

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: GE Healthcare announced a USD 50 million facility in Chennai to manufacture neonatal monitors for domestic and Southeast Asian markets.

- December 2024: Philips Healthcare partnered with Apollo Hospitals to install AI-enabled neonatal monitoring across fifteen centers, enabling respiratory distress alerts four hours ahead of symptoms.

- November 2024: BPL Medical Technologies introduced an indigenous neonatal ventilator series with embedded AI algorithms priced 40% below imports.

- October 2024: Phoenix Medical Systems won a USD 25 million tender to supply 500 incubators to Karnataka district hospitals.

India Neonatal And Prenatal Devices Market Report Scope

As per the scope of this report, fetal monitoring devices are vital tools routinely used in gynecology and obstetrics interventions to examine fetal health during labor and delivery. Neonatal devices are extensively used in Neonatal Intensive Care Units (NICUs), where complex machines and monitoring devices are designed for the unique needs of tiny babies. India's neonatal and prenatal devices Market is segmented by Product Type (Prenatal & Fetal Equipment (Fetal Dopplers, Fetal Monitors, Fetal Pulse Oximeter, and Other Prenatal and Fetal Equipment) and Neonatal Care Equipment (Incubators, Neonatal Monitoring Devices, Phototherapy Equipment, Respiratory Assistance, and Monitoring Devices, and Other Neonatal Care Equipment)). The report offers the value (in USD million) for the above segments.

By Product Type

| Fetal Care Equipment | Fetal Ultrasound Systems |

| Fetal Dopplers | |

| Electronic Fetal Monitors (CTG) | |

| Fetal MRI & Pulse-Oximeters | |

| Neonatal Care Equipment | Incubators |

| Infant Warmers & Convertible Warmers | |

| Phototherapy Systems | |

| Neonatal Ventilators & CPAP | |

| Multi-parameter Monitors & Pulse-Oximeters | |

| Resuscitators & Syringe/Feeding Pumps |

By End User

| Hospitals |

| Neonatal & Pediatric Specialty Clinics |

| Maternity & Birthing Centers |

| Home-care or Remote Monitoring Settings |

By Modality

| Portable |

| Standalone |

| By Product Type | Fetal Care Equipment | Fetal Ultrasound Systems |

| Fetal Dopplers | ||

| Electronic Fetal Monitors (CTG) | ||

| Fetal MRI & Pulse-Oximeters | ||

| Neonatal Care Equipment | Incubators | |

| Infant Warmers & Convertible Warmers | ||

| Phototherapy Systems | ||

| Neonatal Ventilators & CPAP | ||

| Multi-parameter Monitors & Pulse-Oximeters | ||

| Resuscitators & Syringe/Feeding Pumps | ||

| By End User | Hospitals | |

| Neonatal & Pediatric Specialty Clinics | ||

| Maternity & Birthing Centers | ||

| Home-care or Remote Monitoring Settings | ||

| By Modality | Portable | |

| Standalone | ||

Key Questions Answered in the Report

What is the current value of the India neonatal and prenatal devices market?

The market is valued at USD 332.55 million in 2026 and is forecast to reach USD 470.58 million by 2031.

Which product segment leads sales today?

Neonatal care equipment leads with 65.96% revenue share in 2025.

Which end-user group is expanding fastest?

Neonatal and pediatric specialty clinics are projected to grow at an 8.08% CAGR through 2031.

How fast are portable devices growing?

Portable equipment revenue is forecast to rise at an 8.18% CAGR between 2026 and 2031.

How concentrated is supplier power?

The top five vendors hold around 45% market share, indicating moderate concentration.

What incentive program supports local manufacturing?

The Production-Linked Incentive scheme grants 5-7% sales rebates on qualifying medical devices, encouraging domestic production.

Page last updated on: