Power Distribution Twisted Cables Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

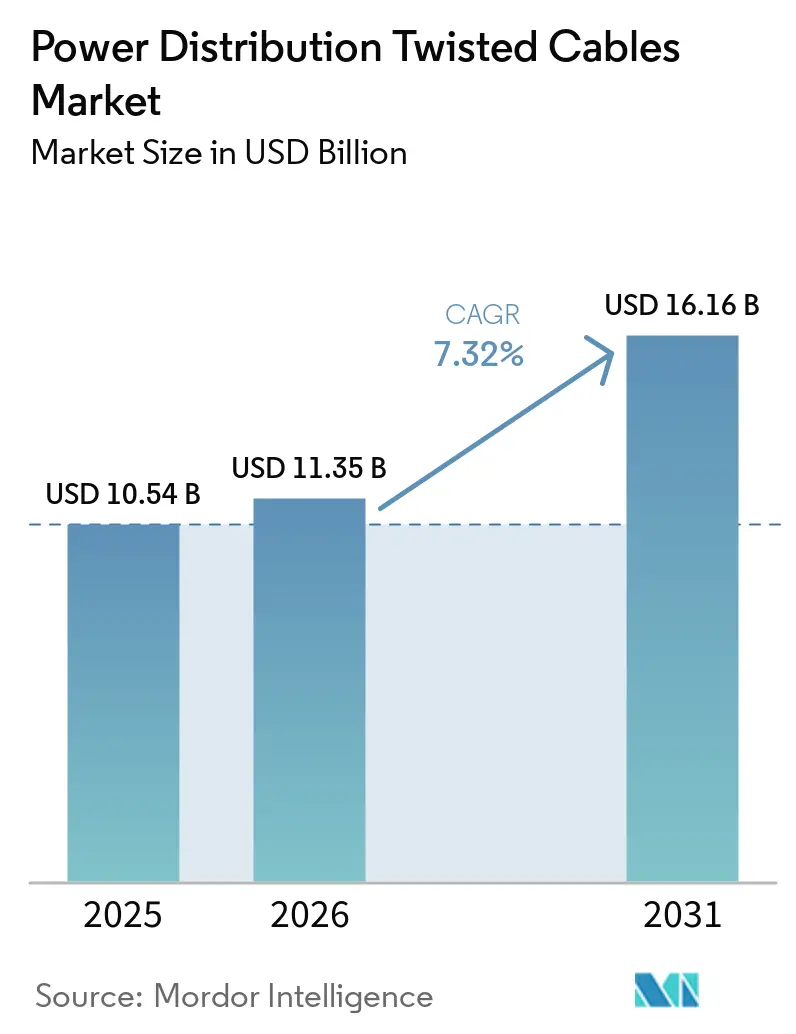

| Market Size (2026) | USD 11.35 Billion |

| Market Size (2031) | USD 16.16 Billion |

| Growth Rate (2026 - 2031) | 7.32% CAGR |

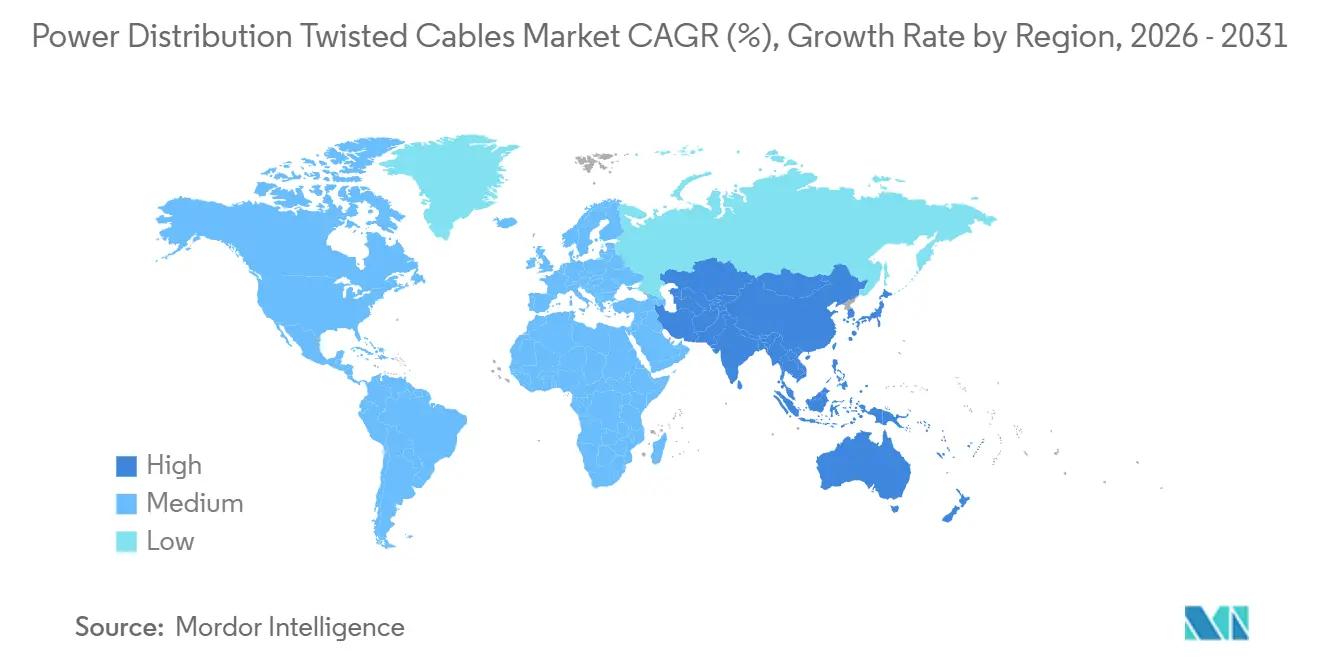

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

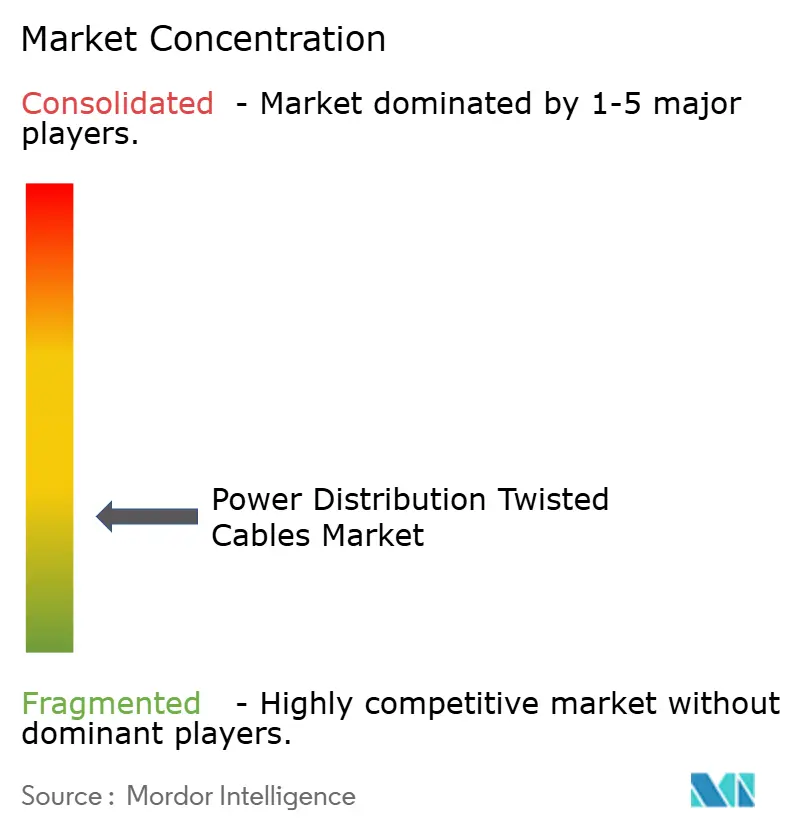

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Power Distribution Twisted Cables Market Analysis by Mordor Intelligence

The Power Distribution Twisted Cables Market size is expected to grow from USD 10.54 billion in 2025 to USD 11.35 billion in 2026 and is forecast to reach USD 16.16 billion by 2031 at 7.32% CAGR over 2025-2031. Rapid undergrounding of distribution feeders, grid-hardening projects in storm-prone regions, and the electrification of transport are lifting capital spending by utilities and commercial developers. Hyperscale AI data centers are ordering feeders with ultra-low impedance to stabilize 800-kilowatt racks, a specification that favors large-cross-section twisted conductors over retrofit busbars. At the same time, utility procurement rules in the United States, the European Union, and India now award bonus points for domestic-content compliance, prompting manufacturers to regionalize rod-drawing and cable-finishing operations. Submarine interconnectors that link offshore wind hubs and island grids are opening a steep growth pocket for 525-kilovolt XLPE-insulated twisted designs. Across all regions, volatile copper and aluminium prices are nudging utilities to hybrid conductors that pair aluminium weight savings with copper ampacity, broadening the product mix and tempering margin risk for suppliers.

Key Report Takeaways

- By conductor material, copper led with 67.9% of power distribution twisted cables market share in 2025, while aluminium-clad and Cu-Al hybrids are forecast to post the fastest 7.5% CAGR through 2031.

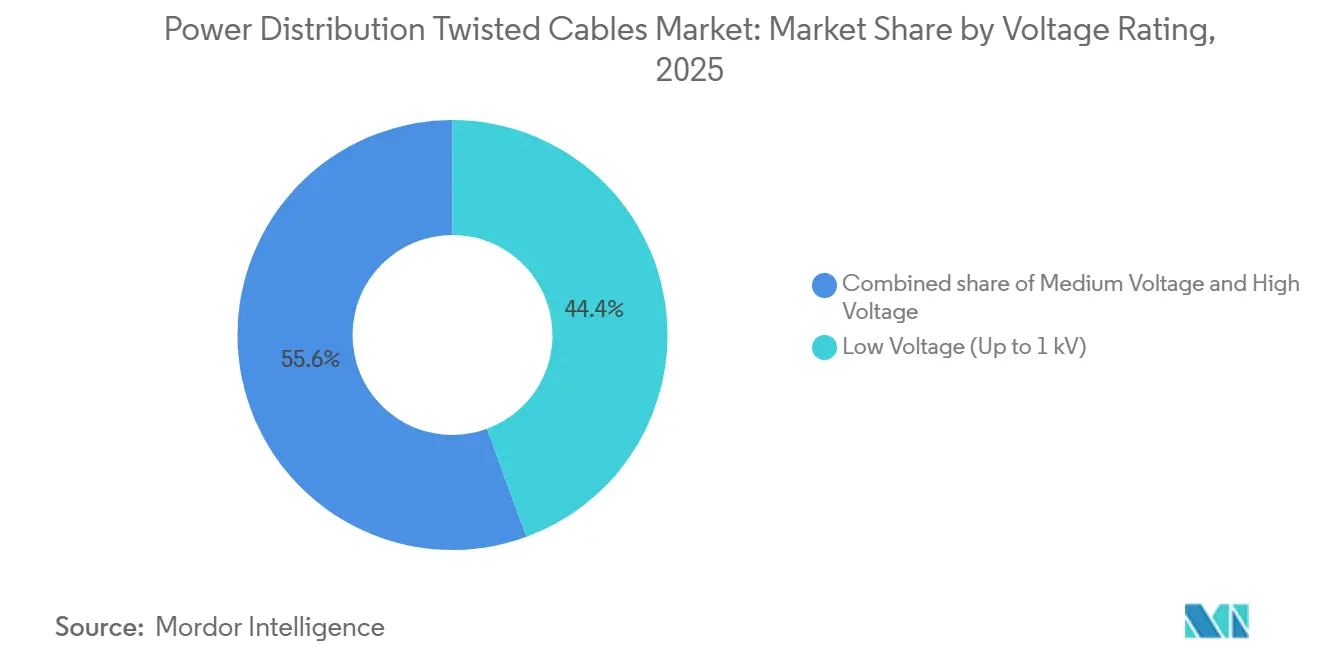

- By voltage rating, low-voltage cables up to 1 kilovolt held 44.4% of the power distribution twisted cables market size in 2025, whereas high-voltage grades above 35 kilovolts are projected to expand at an 8.0% CAGR to 2031.

- By core configuration, single-core products commanded 59.0% share in 2025, yet multi-core formats exceeding four conductors are on track for the highest 8.8% CAGR over the same horizon.

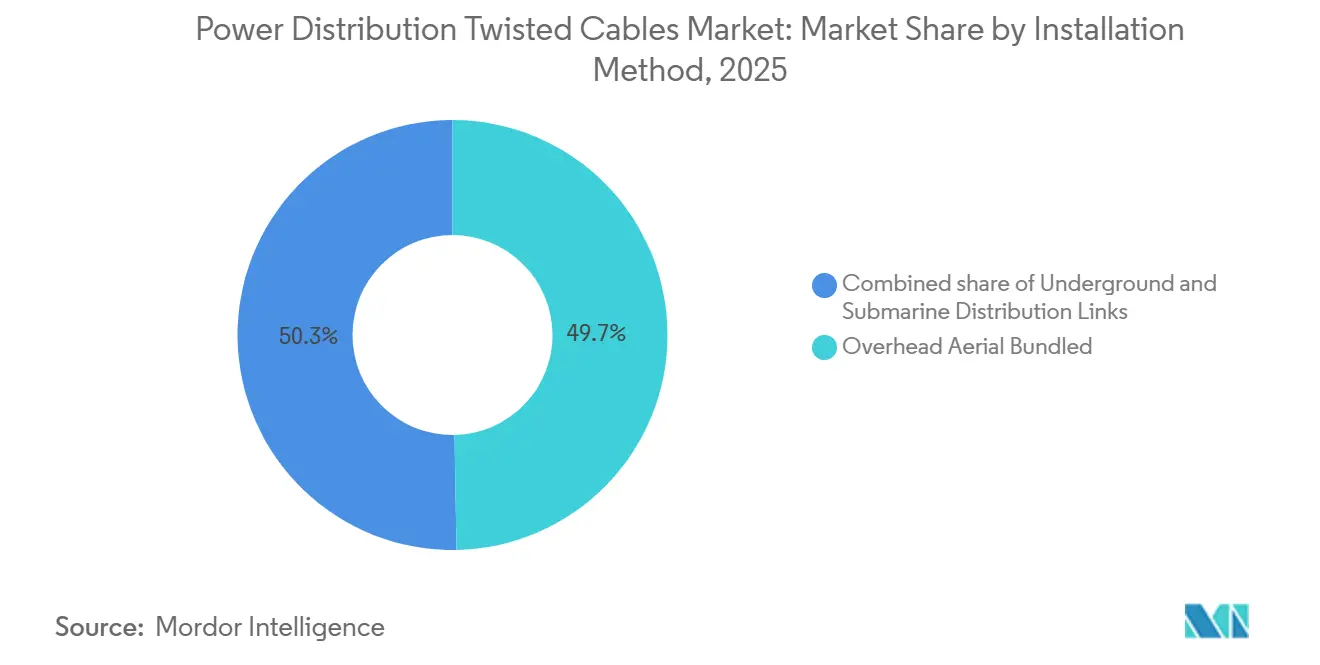

- By installation method, overhead aerial bundled systems accounted for 49.7% revenue in 2025; submarine links are expected to advance at a 9.6% CAGR on an offshore-wind-led build-out.

- By application, utilities led with 47.1% revenue share in 2025; the same segment is pacing at an 8.3% CAGR to 2031.

- By geography, Asia-Pacific contributed 43.9% of 2025 sales and is set to maintain the strongest 7.8% CAGR through 2031 on the back of large-scale grid-modernization budgets in India and China.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Power Distribution Twisted Cables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging undergrounding of urban distribution networks | +1.20% | North America & EU, APAC urban centers | Medium term (2-4 years) |

| Grid-hardening programs in storm-prone regions | +0.90% | North America, Caribbean, Southeast Asia | Short term (≤ 2 years) |

| Rapid build-out of EV fast-charging corridors | +1.10% | Global, with early gains in California, Germany, China | Medium term (2-4 years) |

| Decentralised micro-grids in mining & remote camps | +0.70% | APAC, North America, Africa mining regions | Long term (≥ 4 years) |

| AI data-centre demand for ultra-low-impedance feeders | +1.30% | Global, concentrated in Virginia, Singapore, Ireland | Short term (≤ 2 years) |

| Mineral supply-chain localisation in USMCA for copper conductors | +0.60% | North America (US, Canada, Mexico) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Undergrounding Of Urban Distribution Networks

Urban utilities are converting exposed overhead lines into underground twisted-cable corridors to curb vegetation-related faults and cut wildfire ignition risk. Delhi distribution companies allocated USD 478 million in 2024 to bury 2,500 circuit-kilometers of 11-kilovolt feeders across dense commercial districts [1]Delhi Electricity Regulatory Commission, “Order on Undergrounding 11 kV Feeders,” derc.gov.in. In Anchorage suburbs, Chugach Electric spent USD 55 million in 2025 on a direct-buried XLPE triplex, reporting 40% fewer ice-storm outages after completion. The U.S. Department of Energy’s 2024 guidance recommends XLPE insulation for all new sub-35 kilovolt underground builds, increasing demand for twisted geometries that simplify jointing. Eversource Energy is retiring high-pressure fluid-filled assets in favor of multi-core XLPE, trimming right-of-way width and speeding splice work across Connecticut and Massachusetts.

Grid-Hardening Programs In Storm-Prone Regions

Utilities on hurricane-exposed coasts are embedding twisted conductors in concrete duct banks to survive Category 4 winds and storm-surge floods. Entergy Texas won regulatory approval in 2024 for USD 335 million of undergrounding in Beaumont and Port Arthur after Hurricane Laura’s USD 19 billion damages. Florida Power & Light finalized a USD 280 million submarine project in 2025 that replaced vulnerable overhead spans across the Intracoastal Waterway. NOAA logged 18 named storms during the 2024 Atlantic season, the fourth-highest on record, prompting coastal U.S. utilities to shift budgets into ducted or subsea twisted feeders [2]National Oceanic and Atmospheric Administration, “Atlantic Hurricane Season Summary 2024,” noaa.gov. A parallel policy pivot is unfolding in Metro Manila, where MERALCO earmarked USD 209 million for duct-bank builds to shield circuits from typhoons.

Rapid Build-Out Of EV Fast-Charging Corridors

The rise of 350-kilowatt DC chargers is driving low-voltage twisted cables rated for continuous 400-ampere operation. California’s 2024 Title 24 update mandates pre-installed conduit and cable infrastructure in new commercial parking structures, cutting labor by 25% when installers pull triplex or quadruplex assemblies instead of multiple single cores. NREL testing shows twisted-pair geometries reduce electromagnetic interference by 18 decibels under sustained 80 ampere loads, a benefit for chargers sited near telecom equipment [3]National Renewable Energy Laboratory, “Electrical Performance of EVSE Cables,” nrel.gov. Automakers’ 2024-2025 embrace of the North American Charging Standard locks in uniform conductor specifications across 15,000 Supercharger sites, each requiring several twisted runs from pad-mounted transformers. Europe’s Alternative Fuels Infrastructure Regulation compels one fast charger every 60 kilometers of highway by 2030, a target equating to 120,000 circuit-kilometers of medium-voltage twisted feeders.

AI Data-Center Demand For Ultra-Low-Impedance Feeders

Hyperscale operators that deploy NVIDIA H100 and AMD MI300 clusters are specifying feeder bundles with cross-sections above 1,000 square millimeters to hold voltage drop below 2% across 200-meter runs. A Center for Strategic and International Studies white paper estimates North America will need up to 140,000 additional electricians by 2028 to install and terminate these large cables [4]Center for Strategic and International Studies, “AI Infrastructure Workforce Outlook,” csis.org. The 2026 draft of the National Electrical Code caps impedance at 0.05 ohms per 100 meters for GPU pods, a threshold that favors flexible twisted feeders over rigid busway in retrofits. Microsoft disclosed 800-volt DC backbones in new Azure regions, cutting copper mass by 40% versus 480-volt AC while keeping compatibility with 1,000-volt insulation ratings. Google’s 2025 design guide calls for parallel twisted runs rather than oversized single feeders to improve redundancy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile copper & aluminium prices | -0.9% | Global | Short term (≤ 2 years) |

| Rising adoption of busbars in commercial buildings | -0.6% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Fire-performance certification bottlenecks in APAC | -0.4% | China, India, ASEAN countries | Medium term (2-4 years) |

| Skills shortage in medium-voltage jointing & termination | -0.5% | North America, Europe, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper & Aluminium Prices

London Metal Exchange prices ranged between USD 9,500–10,000 per ton for copper and USD 2,400–2,600 per tonne for aluminium during 2024-2025, trimming cable-maker gross margins by 200-300 basis points on fixed-price bids. Simultaneous mine disruptions in Zambia and Peru kept supply tight, leaving producers to hedge higher-priced futures curves while carrying 6-12 month order backlogs. Indian and Southeast Asian electrification tenders have shifted 8-10% of low-voltage demand toward aluminium conductors to blunt copper volatility. The International Copper Study Group projects refined supply will trail demand growth to 2030, signaling continued swings that push manufacturers to long-term offtake agreements.

Rising Adoption Of Busbars In Commercial Buildings

Data centers and high-rise offices are adopting prefabricated busbar trunking that saves 30% tray space and reduces on-site terminations, eroding 15-20% of the low-voltage share once held by twisted cables in North America and Europe. Legrand’s 800-volt DC busbar, launched in 2024, is displacing cables in new hyperscale facilities where modular scalability justifies its premium. North American busbar shipments climbed 12% year-over-year in 2025, yet the technology remains unfit for outdoor, underground, or submarine routes, keeping its encroachment bounded to climate-controlled interiors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Conductor Material: Hybrid Formats Challenge Copper Dominance

Copper-twisted products captured 67.9% of 2025 revenue as utilities relied on proven ampacity data and familiar termination practices. Aluminium-clad and Cu-Al composite conductors are poised for a 7.5% CAGR, driven by 30-40% weight savings that let utilities extend span lengths and cut structure costs. The power distribution twisted cables market size for hybrid formats is therefore on track to outpace the overall curve through 2031. Pilots in the United States and South Africa show that lower scrap value reduces theft, further tilting rural projects toward hybrids.

Energy losses favor copper in dense urban feeders over a 30-year lifecycle, yet aluminium dominates cost-sensitive rural builds where lighter poles lower civil spend. Prysmian’s 2025 Cu-Al conductor reached 85% of copper ampacity at 65% weight, while Southwire is testing aluminium-clad designs that diversify supply chains without sacrificing performance. As grid-modernization rolls into mountainous terrain, hybrids will continue to chip away at copper’s legacy lead.

By Voltage Rating: High-Voltage Cables Accelerate Amid Renewable Integration

Low-voltage grades up to 1 kilovolt held 44.4% share in 2025, reflecting deep penetration in service drops and building risers. High-voltage products above 35 kilovolts are projected to clock an 8.0% CAGR as offshore wind and long-haul renewables require 230–525 kilovolt submarine and underground circuits. This shifts the power distribution of twisted cables market share at the top end of the voltage spectrum.

Medium-voltage feeders benefit from the replacement of paper-insulated lead-covered lines with XLPE, while California’s 230-kilovolt offshore connections and the ERCOT push to 765-kilovolt overhead corridors are opening new demand layers. Conversely, busbar adoption caps low-voltage growth in indoor environments, though twisted cables stay dominant where environmental exposure or fire codes curb busway use.

By Core Configuration: Multi-Core Formats Gain In Industrial Settings

Single-core cables remained the largest slice at 59.0% in 2025, favored by utilities for fault isolation and simplified splicing. Multi-core constructions above four conductors are forecast to expand at 8.8% CAGR, reflecting compact tray gains in petrochemical, data-center, and mining plants. For instance, Shell’s Pulau Bukom site chose 12-core armored twisted cables that cut tray congestion by 30%.

Triplex aerial bundled assemblies dominate residential service drops, lowering vegetation faults and labor. In high-voltage corridors above 69 kilovolts, IEEE guidance still calls for single cores in trefoil to ease partial-discharge testing. Factory-terminated multi-core kits for AI data halls are shortening commissioning schedules, a tangible advantage where skilled labor is scarce.

By Installation Method: Submarine Links Post Fastest Growth

Overhead aerial bundled systems held 49.7% of 2025 sales on the strength of rural electrification and mining operations. Submarine distribution links, however, will surge at a 9.6% CAGR through 2031, riding offshore wind interconnection pipelines in Europe and Asia. The power distribution twisted cables market size tied to subsea routes is therefore set to jump faster than any other installation class. NKT’s USD 734.9 million Bornholm contract and Prysmian’s USD 961 million Eastern Green Link 2 award underscore the capital swing offshore.

Urban overhead lines are steadily converted to underground duct banks for wildfire safety and aesthetics, while submarine projects confront deep-water burial complexity that inflates cost by 20-25% but slashes anchor-strike risk by 85%. Underground twisted cables retain dominance in data centers where fire codes restrict exposed runs.

By Application: Utilities Lead Share And Growth

Utilities controlled 47.1% of 2025 revenue and will pace an 8.3% CAGR as governments plow funds into grid resilience, renewable integration, and undergrounding. Residential demand benefits from rooftop solar interconnects aligned with IEEE 1547-2024 bidirectional rules. Commercial buildings are gradually adopting busbars for risers, yet continue to employ twisted feeders for emergency circuits. Industrial facilities, especially AI data centers and petrochemical plants, favor fire-rated multi-core assemblies that speed installation amid a skilled-labor crunch.

India earmarked USD 31 billion for 500,000 circuit-kilometers of new distribution cables, and China State Grid budgeted USD 88 billion for urban reinforcements, keeping utilities the principal demand engine.

Geography Analysis

Asia-Pacific delivered 43.9% of 2025 revenue and will maintain a 7.8% CAGR through 2031. India’s USD 31 billion grid program and China State Grid’s USD 88 billion urban upgrade are the twin pillars. Japan assigned USD 9.6 billion to seismic-resilient underground cables after the 2024 Noto quake, while Indonesia’s PLN booked 12,000 circuit-kilometers for renewable integration. Harmonized ASEAN specifications at 230 and 500 kilovolts underpin regional trade in high-voltage twisted conductors.

North America and Europe channel funding into resilience and decarbonization. The U.S. Grid Resilience and Innovation Partnerships program supplied USD 10.5 billion in 2024 grants, and the European Union allocated USD 654.1 billion toward digital and renewable-ready networks. Consolidated Edison alone plans to replace 800 circuit-kilometers of aging lead-covered stock in New York City, while Canada’s cross-border hydro exports will double high-voltage twisted cable volume by 2032.

Secondary growth pockets span South America, the Middle East, and Africa. Brazil approved USD 4.4 billion for loss-reduction upgrades, Saudi Arabia budgeted USD 8 billion for Red Sea submarine links, and Egypt committed USD 1 billion to underground Cairo feeders. South Africa’s anti-theft program pilots aluminium-clad cables to curb 1,200 yearly incidents, proving regulatory levers can reshape conductor choice.

Competitive Landscape

The Power Distribution Twisted Cables Market is fragmented. The five largest suppliers are Prysmian, Nexans, Southwire, Sumitomo Electric, and LS Cable & System, which control a major share of global sales, leaving room for agile regional players such as KEI Industries, Polycab India, Riyadh Cables, and Ducab. Vertical integration is a rising moat: Prysmian’s captive rod mills in Italy and Brazil shield bids from metal swings, while Southwire’s Carrollton expansion secures USMCA-qualified capacity. Only a handful of firms own purpose-built cable-laying vessels, granting NKT and Prysmian disproportionate leverage in offshore wind tenders.

Process innovation is sharpening cost curves. Nexans deployed machine learning on extrusion lines, trimming insulation variability by 18% and scrap by 12%. IEC 60332-1-2:2025 flame and smoke upgrades require USD 2-5 million per test line, capital that tilts the field toward diversified multinationals. Patent races in hybrid conductors are heating; Southwire locked a 2025 U.S. patent for an aluminium-clad copper design that slices skin-effect losses by 8%, giving utilities a bridge between copper performance and aluminium economics.

Chinese manufacturers ZTT and Hengtong leverage scale and export credits to win African and Southeast Asian tenders, but localization incentives in the United States and Europe blunt their reach. Overall, the market’s moderate concentration fosters price competition in low-voltage bids while rewarding technological depth in high-voltage and submarine segments.

Power Distribution Twisted Cables Industry Leaders

Prysmian Group

Nexans SA

Southwire Company

Sumitomo Electric

LS Cable & System

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Engie announced a USD 14.1 billion acquisition of UK Power Networks, which manages extensive electricity distribution cable systems. This acquisition aims to enhance electricity networks to support low-carbon energy initiatives and EV charging infrastructure, thereby increasing the demand for advanced distribution cables, including twisted cable configurations in low-voltage (LV) and medium-voltage (MV) networks.

- December 2025: Ofgem approved a USD 37.5 billion, five-year investment plan (2026–2031) to upgrade the UK's gas and electricity networks. This funding, under the RIIO-3 framework, is intended to expand grid capacity for renewable energy, replace aging infrastructure, and improve network security.

- July 2025: Prysmian secured a framework agreement with Terna to support the enhancement of the Italian power grid. The agreement, spanning three years with an optional additional year, has a potential total value of USD 428 million. Under this agreement, Prysmian will supply HVAC cables and provide maintenance for high-voltage cables. Terna has committed to purchasing a minimum of 50 km of high-voltage cable annually, with the possibility of increased quantities based on their requirements.

- June 2025: Eastern Power Distribution Company Limited announced the implementation of a large underground cabling project covering 876 km, scheduled for completion by August 2026. This project aims to improve grid resilience and reliability, highlighting the critical role of insulated and twisted cable systems in urban distribution networks.

Global Power Distribution Twisted Cables Market Report Scope

Power Distribution Twisted Cables are electrical cables designed by twisting two or more insulated conductors together to efficiently transmit power while reducing electromagnetic interference (EMI). The twisting pattern mitigates noise and minimizes signal distortion, ensuring greater stability and reliability compared to parallel conductors. These cables are widely used in low- to medium-voltage power distribution systems, particularly in environments where electrical noise, space limitations, or mechanical flexibility are critical.

The Global Power Distribution Twisted Cables Market is segmented by conductor material, voltage rating, core configuration, installation method, application, and geography. By conductor material, the market is segmented into copper, aluminium, and hybrid. By voltage rating, the market is segmented into low, medium, and high voltage. By core configuration, the market is segmented into single, triplex/quadruplex, and multi-core. By installation method, the market is segmented into overhead, underground, and submarine. By application, the market is segmented into residential, commercial, industrial, and utilities. The report also covers market size and forecasts for the global power distribution twisted cables market across major countries and regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, market sizing and forecasts have been provided on the basis of value (USD).

| Copper-twisted cables |

| Aluminium-twisted cables |

| Hybrid (Cu-Al, Cu-Clad, etc.) |

| Low Voltage (Up to 1 kV) |

| Medium Voltage (1 to 35 kV) |

| High Voltage (Above 35 kV) |

| Single-core |

| Triplex/Quadruplex |

| Multi-core (Greater Than 4) |

| Overhead Aerial Bundled |

| Underground |

| Submarine Distribution Links |

| Residential |

| Commercial |

| Industrial |

| Utilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Conductor Material | Copper-twisted cables | |

| Aluminium-twisted cables | ||

| Hybrid (Cu-Al, Cu-Clad, etc.) | ||

| By Voltage Rating | Low Voltage (Up to 1 kV) | |

| Medium Voltage (1 to 35 kV) | ||

| High Voltage (Above 35 kV) | ||

| By Core Configuration | Single-core | |

| Triplex/Quadruplex | ||

| Multi-core (Greater Than 4) | ||

| By Installation Method | Overhead Aerial Bundled | |

| Underground | ||

| Submarine Distribution Links | ||

| By Application | Residential | |

| Commercial | ||

| Industrial | ||

| Utilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the power distribution twisted cables market by 2031?

The market is expected to reach USD 16.16 billion by 2031, growing at a 7.32% CAGR from 2026 to 2031.

Which voltage class is forecast to grow the fastest?

High-voltage twisted cables above 35 kilovolts are set to register an 8.0% CAGR through 2031 as utilities integrate large-scale renewables.

Who are the leading suppliers in this space?

Prysmian, Nexans, Southwire, Sumitomo Electric, and LS Cable & System together account for 35–40% of global sales.

Why are submarine twisted cables gaining momentum?

Offshore wind build-outs and island-grid interconnections require 525 kilovolt XLPE-insulated subsea links, pushing submarine installations to a 9.6% CAGR.

How are material price swings influencing conductor choice?

Volatile copper prices encourage utilities to adopt aluminium-clad and Cu-Al hybrid conductors that balance cost savings with acceptable ampacity.

Page last updated on: