Medium Voltage Cable Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

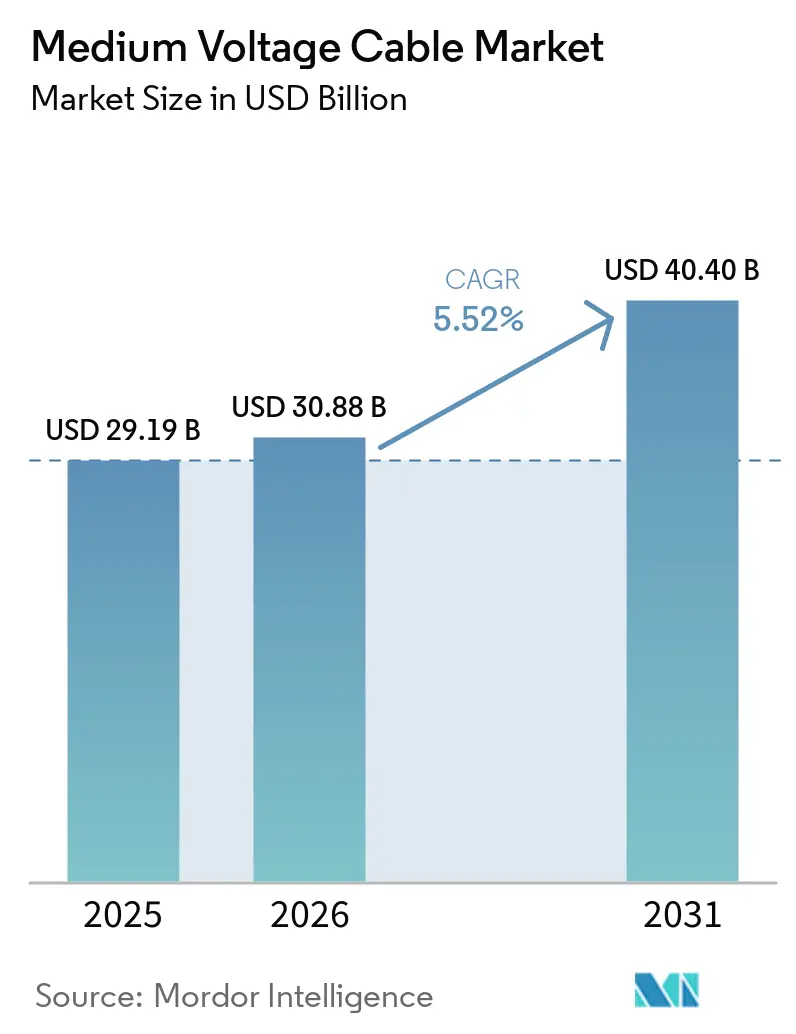

| Market Size (2026) | USD 30.88 Billion |

| Market Size (2031) | USD 40.40 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

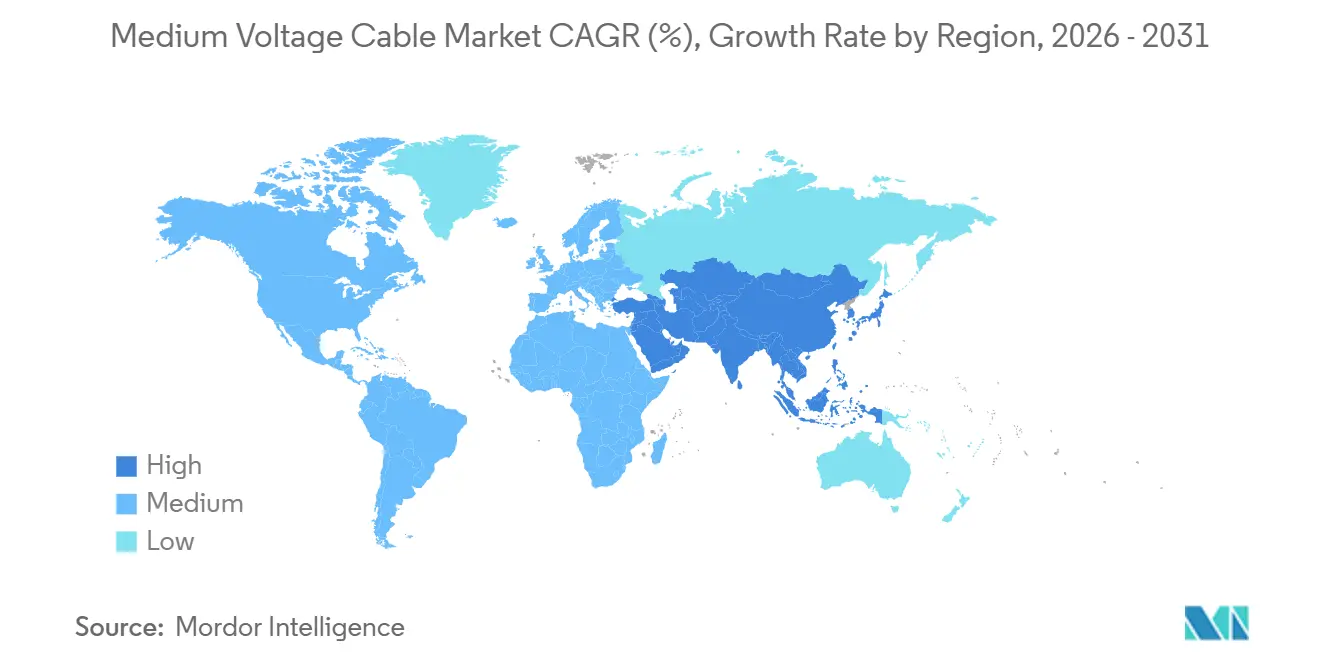

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medium Voltage Cable Market Analysis by Mordor Intelligence

The Medium Voltage Cable Market size is projected to expand from USD 29.19 billion in 2025 and USD 30.88 billion in 2026 to USD 40.40 billion by 2031, registering a CAGR of 5.52% between 2026 to 2031.

Rapid grid-renewal mandates tied to renewable roll-outs, hyperscaler demand for private distribution loops, and deeper offshore wind arrays are sustaining orders even while raw-material volatility compresses producer margins. Policy shifts that outlaw per- and polyfluoroalkyl substances (PFAS) in cable jackets are forcing mid-cycle retooling, yet they also open premium niches for fluorine-free compounds. Aluminium and cross-linked polyethylene (XLPE) cost swings have narrowed EBITDA on legacy bids, but suppliers with captive rod and compound assets continue to win volume by offering fixed-price contracts. The medium-voltage cable market is further buttressed by industrial decarbonization projects that require high-ampacity feeders for electric furnaces and electrolyzers, while early superconducting trials hint at a future step-change in urban transfer density.

Key Report Takeaways

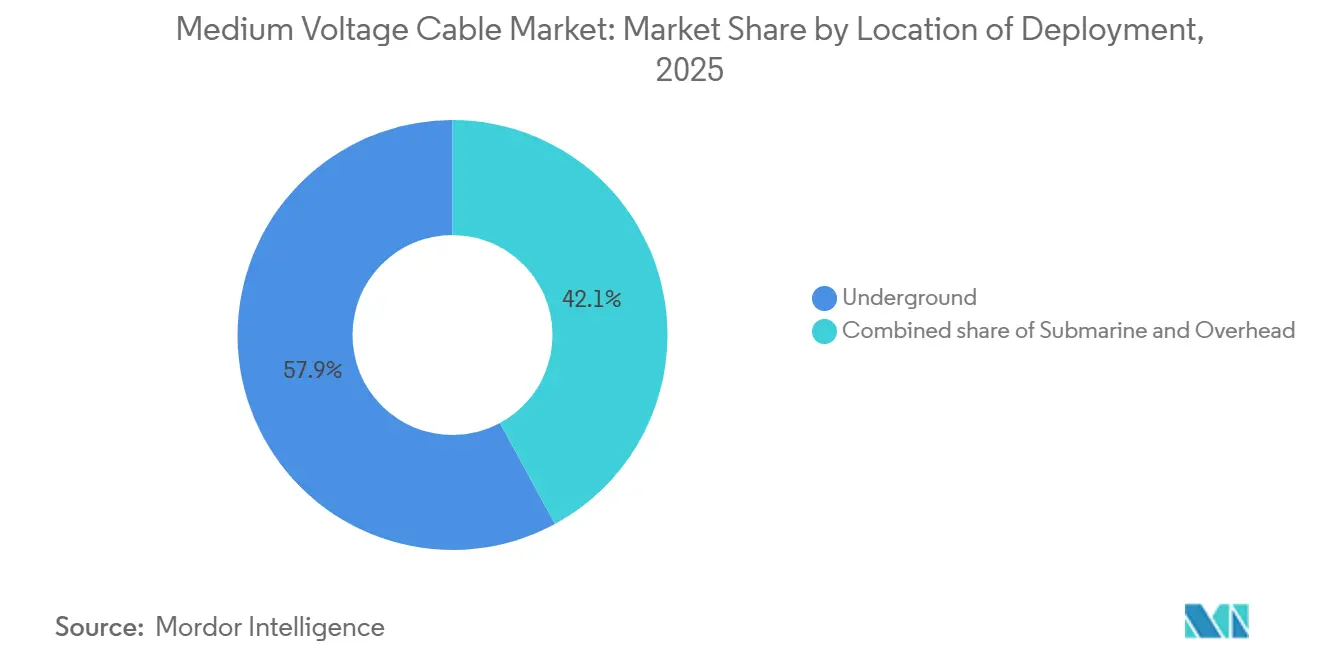

- By location of deployment, underground installations captured 57.9% of 2025 revenue, whereas submarine installations are forecast to expand at a 7.2% CAGR through 2031.

- By type, AC products led with 72.5% share in 2025, yet DC variants are expected to post the highest 8.1% CAGR to 2031.

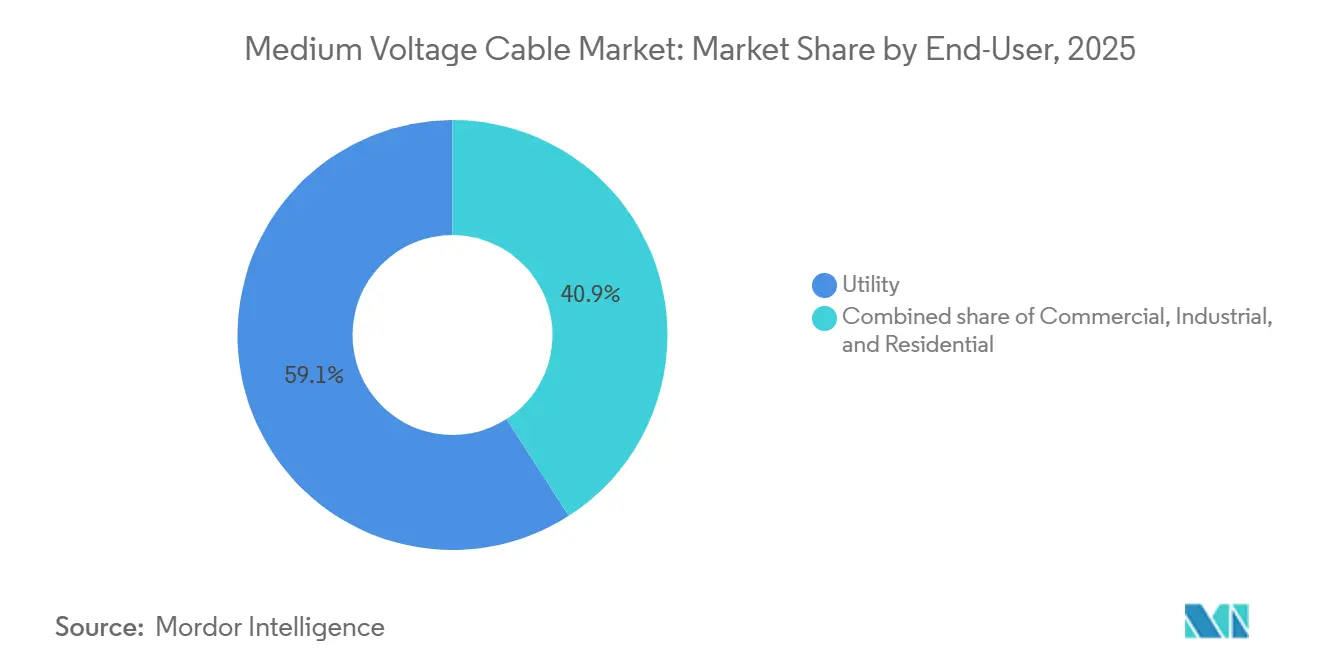

- By end-user, utilities absorbed 59.1% of 2025 shipments; industrial customers are poised for the fastest 7.9% CAGR during 2026-2031.

- By geography, Asia-Pacific accounted for 48.3% of global sales in 2025 and is projected to grow at a 6.5% CAGR, the quickest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medium Voltage Cable Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-linked grid-upgrade mandates (2026-2031) | 1.8% | Global, peak impact in EU, China, India | Medium term (2-4 years) |

| Surge in utility-scale battery energy storage roll-outs | 1.2% | North America, APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Electrification of high-temperature industrial heat | 0.9% | EU industrial belt, China coastal provinces | Long term (≥ 4 years) |

| Rapid inter-data-center power looping (hyperscalers) | 0.7% | North America, Western Europe, Singapore | Short term (≤ 2 years) |

| Mainstream urban electrified mass-transit extensions | 0.6% | APAC metros, Latin America capitals | Medium term (2-4 years) |

| Offshore hydrogen demo clusters (≥ 20 MW) | 0.4% | North Sea, Australia, Middle East coastlines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renewable-Linked Grid-Upgrade Mandates Drive Feeder Replacement Cycles

Germany’s 2025 directive compels distribution operators to modernize 18,000 circuit-kilometers of 20 kV lines by 2029, tripling the historic replacement rate.[1]Bundesnetzagentur, “Grid Expansion Plan,” bundesnetzagentur.de China earmarked CNY 320 billion (USD 44 billion) for county-level 10-35 kV upgrades over five years, with early work concentrated in Inner Mongolia and Qinghai. India now ties renewable-certificate issuance to proof of spare grid capacity, prompting state utilities to pre-lay feeders in solar and wind zones. Because penalties range from subsidy claw-backs to direct fines, cable demand remains inelastic even when aluminium prices spike. Medium-voltage cable market participants with turnkey installation services are best placed to capture this captive volume, as distribution companies favor single-supplier contracts to shorten approval cycles.

Utility-Scale Battery Storage Amplifies Cable Demand

The United States added 9.4 GW of standalone batteries in 2024, each park using 34.5 kV loops between inverters and substations.[2]U.S. Department of Energy, “Battery Storage Factbook 2025,” energy.gov Frequent cycling accelerates insulation aging, so vendors have begun to specify thicker XLPE and upgraded screening tapes that extend design life past 30 years. Three 500 MW projects in New South Wales combined require over 180 kilometers of 33 kV feeders, illustrating the material intensity of storage assets. Retrofit co-location at retired coal plants also multiplies orders because corrosion often necessitates complete cable replacement, not partial re-termination. This surge positions the medium-voltage cable market as a direct proxy for storage deployment momentum over the next two years.

Industrial Electrification Opens Niche Demand

ArcelorMittal’s Hamburg pilot of a 25 MW electric induction furnace runs on 20 kV dedicated loops, cutting on-site Scope 1 emissions by 18%.[3]ArcelorMittal Communications, “Hamburg Induction Furnace Pilot,” arcelormittal.com BASF plans to install 40 kilometers of 30 kV cable by 2028 to power steam-cracker electrification at Ludwigshafen. These loads need cables rated for 90 °C continuous operation and 40 kA fault-withstand, a combination that pushes cross-sections larger and raises copper content. IRENA projects that industrial heat electrification may add 15-20 GW of European demand by 2030, equating to nearly 8,000 circuit-kilometers of new feeders. As a result, the medium-voltage cable market finds a stable outlet even when broader construction cycles soften.

Rapid Inter-Data-Center Power Looping Eases Utility Bottlenecks

Microsoft’s Virginia campus operates a 13.8 kV private ring that links four buildings and defers a USD 80 million substation upgrade.[4]Microsoft Investor Relations, “Data Center Infrastructure Update 2025,” microsoft.com Google installed a 34.5 kV tie line in Iowa to pool backup-generator capacity and reduce diesel storage by 30%. Cables here must achieve five-nines availability, so buyers pay 25-30% more for triple-extruded insulation and built-in partial-discharge sensors. The Uptime Institute estimates hyperscalers will lay 600 kilometers of private feeders between 2025 and 2028, a volume equal to some small national grids. Consequently, the medium-voltage cable market gains a high-margin niche shielded from public-sector budget cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile aluminium & XLPE input prices | -1.1% | Global, acute in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Utility CAPEX deferrals in sub-Saharan Africa | -0.6% | Sub-Saharan Africa, spillover to North Africa | Medium term (2-4 years) |

| Installation permit bottlenecks in dense metros | -0.4% | North America, Western Europe, select APAC cities | Medium term (2-4 years) |

| Stricter PFAS-free insulation compliance costs | -0.5% | EU, North America (California, New York, Maine) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile aluminium & XLPE input prices

London Metal Exchange aluminium futures peaked at USD 2,680 per tonne in February 2025 before sliding to USD 2,320 by mid-year, while Brent-linked XLPE resin rose 14% then eased. Utilities still tender cables 12-18 months ahead, locking suppliers into fixed prices even when inputs rise, as Prysmian’s Q1 2025 call showed with a 220-basis-point EBITDA drop. Smaller Asian manufacturers, lacking hedging tools, have already declared three bankruptcies since late 2024. If volatility persists, the medium-voltage cable market could see more consolidation as cash-light players exit.

Utility CAPEX deferrals in sub-Saharan Africa

Kenya Power postponed 40% of planned 33 kV feeders in 2025 due to a USD 150 million funding gap. Nigeria’s Transmission Company cannot open letters of credit for imported cables, stalling 11 kV extensions around Lagos. The African Development Bank lists 18 countries at debt-distress risk, curbing co-financing capacity for distribution projects. The International Finance Corporation warns that unmet demand could reach 45,000 circuit-kilometers by 2030, worth USD 1.8 billion in lost medium-voltage cable market size. Without fiscal relief, regional suppliers face a shrinking order book and longer receivable cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Submarine Share Rises With Offshore Energy

Underground installations controlled 57.9% of 2025 revenue, reflecting dense-city mandates and wildfire-mitigation rules. Overhead spans remain cheaper, USD 180,000 per circuit-kilometer versus USD 620,000 for buried lines, but liability and visual objections limit new aerial builds in many developed regions. Submarine projects, though smaller in absolute dollars, are forecast at a 7.2% CAGR to 2031, powered by offshore wind arrays that now site turbines farther than 60 kilometers from shore and by hydrogen pilot plants needing 20 MW plus feeds. A 66 kV system delivered by NKT to Hollandse Kust West in 2025 showed that inter-array runs can exceed 15 kilometers without intermediate platforms. Rising water depths also spur accessory innovation, adding 12-18% to project cost but boosting reliability in harsh seabed conditions.

The medium-voltage cable market size for submarine projects is anticipated to reach USD 7.1 billion by 2031, up from roughly USD 4.7 billion in 2026, underscoring how offshore wind and hydrogen corridors are recasting deployment patterns. Overhead solutions will persist in low-density zones, yet their share will slip as more regulators demand undergrounding for resiliency. Underground growth likewise benefits from smart-city programs that hide utility assets below grade to free surface real estate. Suppliers able to package cable, joints, and real-time monitoring stand to win margin as customers shift toward total-cost-of-ownership procurement.

By Type: DC Installations Gain Momentum

AC products accounted for 72.5% of the value in 2025 because most legacy distribution and load equipment is still synchronous. The DC sub-segment, however, should log an 8.1% CAGR through 2031 thanks to battery storage, long-haul renewable corridors, and data-center interties that prioritize lower resistive losses. Tesla’s Megapack installations now specify 1,500 VDC collection grids that step directly to medium-voltage DC and skip an inverter stage, lifting round-trip efficiency by up to 3 points. China’s pilot feeders in Xiong’an run at 20 kV DC and integrate rooftop solar, EV chargers, and building loads on a common bus, trimming conversion loss by 8% versus AC.

Medium-voltage cable market size for DC designs is projected to grow from USD 8.4 billion in 2026 to USD 14.1 billion by 2031, reflecting both volume and higher per-meter pricing. Space-charge in XLPE under DC stress forces thicker insulation or alternative dielectrics such as polypropylene, raising material content. Protection relies on traveling-wave detection, so owners often bundle specialized breakers and sensors, deepening supplier stickiness. AC will dominate base-grid replacement, but the faster compound rate of DC highlights a structural pivot toward applications that reward controllability and efficiency.

By End-User: Industrial Loads Accelerate

Utilities bought 59.1% of shipments in 2025 owing to mandated grid reinforcement, yet industrial customers are set for the quickest 7.9% CAGR to 2031. Tata Steel’s 33 kV ring main in Jamshedpur consumed 22 kilometers of cable for a single electric arc furnace, illustrating density in heavy-process electrification. BHP’s Escondida mine will lay 18 kilometers of ruggedized cable to charge battery-electric haul trucks, signaling a broad mining shift. Commercial sites, airports, malls, and hospitals grow in line with GDP, while residential demand remains indirect through step-down transformers.

The medium-voltage cable market share tied to industrial buyers is expected to climb from 22% in 2025 to 26% by 2031, representing nearly USD 10 billion in incremental spend. Carbon pricing in Europe and voluntary corporate targets worldwide make electric heat competitive with fossil fuels even before counting emissions costs. Vendors that certify high-fault-current designs and accelerated-aging insulation will secure premium margins in this segment.

Geography Analysis

Asia-Pacific generated 48.3% of worldwide revenue in 2025, and the region is projected to register a 6.5% CAGR to 2031 thanks to Chinese county-level upgrades, Indian rail electrification, and Southeast Asian renewables. China allocated CNY 320 billion through 2029 to modernize 10-35 kV feeders, mostly in provinces with high wind and solar penetration. India is electrifying 25,000 route-kilometers of rail, each kilometer demanding up to 10 circuit-kilometers of 25 kV traction cable. ASEAN nations collectively plan 12,000 circuit-kilometers of feeder cable for solar and wind farms between 2025 and 2028.

North America held a roughly 22% share in 2025, underpinned by the U.S. Infrastructure Investment and Jobs Act and Canadian provincial programs. The U.S. Department of Energy’s Grid Resilience and Innovation Partnerships awarded USD 3.5 billion in 2024 to underground medium-voltage lines in wildfire corridors. Hyperscaler demand concentrates in Virginia, Iowa, and Dallas metro zones, where private loops often bypass congested substations. Canada’s push to phase out coal by 2030 compels utilities in Saskatchewan and Alberta to add distribution capacity for wind-sited battery projects.

Europe represented about 20% of 2025 sales. REPowerEU targets drive offshore wind and hydrogen pilots, yet permit delays and labor shortages slow execution. Urban retrofit needs are acute; many city centers still rely on paper-insulated lead-covered cable that must be replaced without full excavation. Suppliers offering compact, high-voltage-rated products able to snake through old ducts meet this requirement. South America and the Middle East-Africa together contributed near 10% in 2025; Brazil’s auction pipeline and Saudi Arabia’s NEOM program stand out, though exchange-rate swings and financing costs temper broader uptake. Overall, Asia-Pacific remains the growth engine, while mature Western markets pivot toward resiliency and decarbonization retrofits.

Competitive Landscape

The medium-voltage cable market shows moderate concentration, with the top five players (Prysmian, Nexans, NKT, LS Cable & System, and Sumitomo Electric) holding 38% of 2025 revenue. Commodity AC feeders see fierce price competition, whereas submarine, DC, and high-temperature variants command 40-60% premiums and attract fewer qualified bidders. Prysmian’s 2024 acquisition of a Malaysian XLPE compounder and Nexans’s 2025 copper-rod mill in South Carolina reflect a vertical-integration race to blunt raw-material shocks. Regional challengers such as KEI Industries, Elsewedy Electric, and Furukawa Electric leverage local content rules and shorter lead times to win tenders unattractive to global majors.

Retrofit demand in dense cities is spawning compact designs that slip inside legacy ducts and require specialized pulling gear. Firms embedding fiber-optic sensors for real-time temperature and partial-discharge monitoring now bundle multiyear service contracts, raising customer switching costs. M&A has accelerated: Prysmian spent USD 340 million on a European submarine specialist in 2024, while LS Cable & System teamed with a Saudi conglomerate to secure NEOM volume. Nexans inked a 2025 framework with Ørsted, guaranteeing medium-voltage array cable supply through 2030 in exchange for price stability.

Niche disruptors target sustainability. A Swedish start-up released a fully recyclable thermoplastic design in 2025, appealing to utilities with circular-economy mandates even though long-term field data remain scarce. The 2024 IEC 60502 revision tightened partial-discharge limits and added carbon-accounting annexes, compelling incumbents to re-certify products and raising the bar for new entrants. Suppliers that pair material science advances with lifecycle services appear best positioned as customers move toward total-cost frameworks.

Medium Voltage Cable Industry Leaders

Nexans SA

NKT A/S

Prysmian Group

LS Cable & System

Southwire Company LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ABB announced an investment of approximately USD 200 million to expand its medium-voltage equipment manufacturing capacity across Europe. This investment includes the establishment of a new facility in Dalmine, Italy, along with upgrades to existing plants in Germany, Poland, Finland, Norway, and Bulgaria. The initiative aims to meet the growing demand from utilities, data centers, EV infrastructure, and industrial electrification.

- February 2026: Nexans signed a seven-year framework agreement worth USD 699 million with Enedis for the supply of medium-voltage (HTA) cables across France. This agreement is intended to support grid modernization, the undergrounding of power lines, the expansion of EV charging infrastructure, and the integration of renewable energy.

- February 2026: Prysmian secured a framework agreement valued at up to USD 640 million with Enedis for the supply of a full range of medium-voltage cables. The agreement, spanning from 2026 to 2032 (including three optional years), focuses on modernizing the French power grid while promoting sustainable and circular economy practices.

- June 2025: Prysmian Group completed its USD 1 billion acquisition of Channell to strengthen its U.S. market presence and expand medium voltage cable capabilities in the North American market.

Global Medium Voltage Cable Market Report Scope

The medium voltage cable is a medium that is used to facilitate the transfer of electricity to different end-consumers. Medium voltage cables are predominantly used to distribute electricity from substations to transformers. A medium voltage cable is comprised of a conductor, insulation, internal semiconductor screen, cable external semiconductor, cable metal screen, inner and outer sheath, and armor.

The medium-voltage cable market is segmented by location of deployment, type, end user, and geography. By location of deployment, the market is segmented into underground, submarine, and overhead cables. By type, the market is segmented into alternating current (AC) and direct current (DC) cables. By end user, the market is segmented into utility, commercial, industrial, and residential sectors. The report covers market size estimates and forecasts for the medium-voltage cable market across various countries in regions. For each segment, market sizing and forecasts are provided on the basis of value (USD).

| Underground |

| Submarine |

| Overhead |

| AC |

| DC |

| Utility |

| Commercial |

| Industrial |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Location of Deployment | Underground | |

| Submarine | ||

| Overhead | ||

| By Type | AC | |

| DC | ||

| By End-user | Utility | |

| Commercial | ||

| Industrial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the medium-voltage cable market today?

The medium-voltage cable market size reached USD 30.88 billion in 2026 and is forecast at USD 40.40 billion by 2031.

What CAGR is expected for medium-voltage cables between 2026 and 2031?

Revenue is projected to rise at a 5.52% CAGR over the period.

Which region leads demand for medium-voltage cables?

Asia-Pacific accounted for 48.3% of 2025 sales and is projected to grow at the fastest 6.5% CAGR to 2031.

Why are DC medium-voltage cables gaining traction?

Battery storage and long-haul renewable corridors favor DC because lower resistive losses and simpler reactive-power management improve efficiency.

Which end-user segment is growing fastest?

Industrial customers, notably steel and chemical producers electrifying heat processes, are expected to post a 7.9% CAGR through 2031.

How are raw-material price swings affecting cable projects?

Volatile copper and aluminium prices introduce budgeting uncertainty, prompting index-linked contracts and encouraging adoption of copper-clad aluminium conductors.

Page last updated on: