Polyurethane (PU) Adhesives In Electronics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

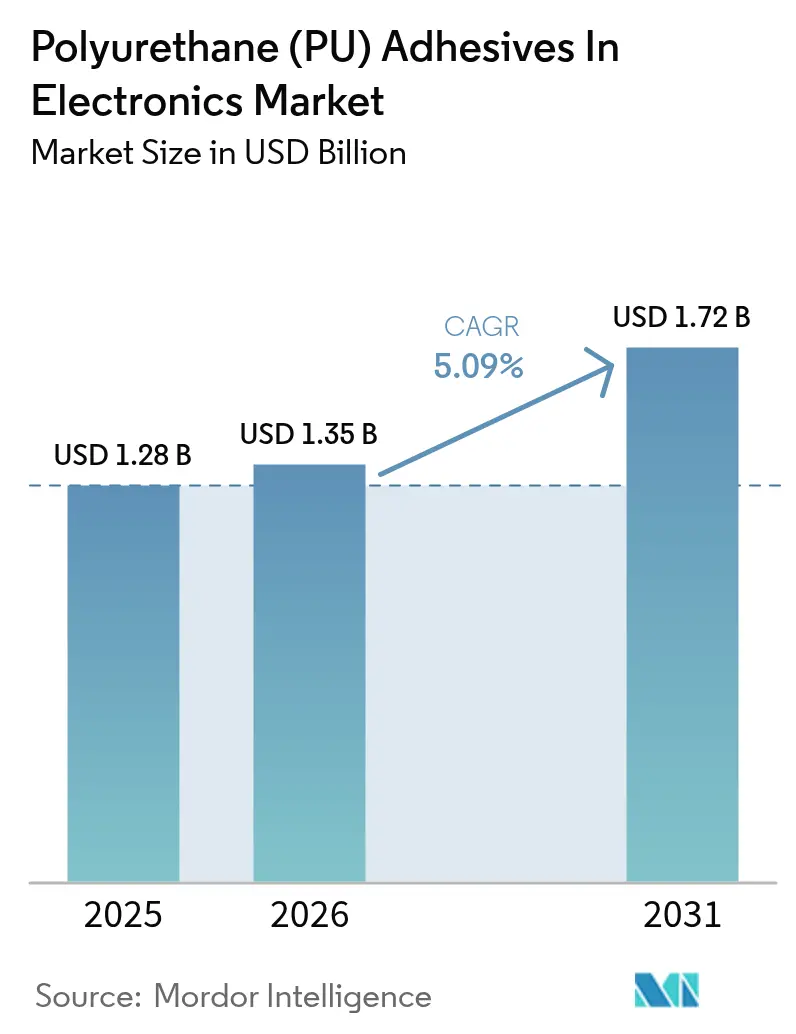

| Market Size (2026) | USD 1.35 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyurethane (PU) Adhesives In Electronics Market Analysis by Mordor Intelligence

The Polyurethane Adhesives In Electronics Market size is projected to be USD 1.28 billion in 2025, USD 1.35 billion in 2026, and reach USD 1.72 billion by 2031, growing at a CAGR of 5.09% from 2026 to 2031. Advancements in miniaturization of consumer devices, the shift to 400 V and 800 V electric vehicle (EV) battery platforms, and stricter global regulations on free diisocyanate content are key factors influencing material selection in high-volume electronics assembly. The polyurethane adhesives market in electronics is supported by UV-curing chemistries that enable sub-second cure cycles on surface-mount-technology (SMT) lines, water-borne dispersions that comply with low-VOC requirements without compromising throughput, and thermally conductive grades that effectively dissipate heat in densely packed power modules. Competitive intensity has increased since 2025, driven by multinational suppliers expanding capacity in the Asia-Pacific region while defending North American and European auto-electronics accounts against regional competitors offering cost-effective custom formulations. Technology convergence, particularly dual-cure systems combining UV initiation with moisture-backup mechanisms, continues to address shadow-cure challenges in increasingly complex three-dimensional assemblies.

Key Report Takeaways

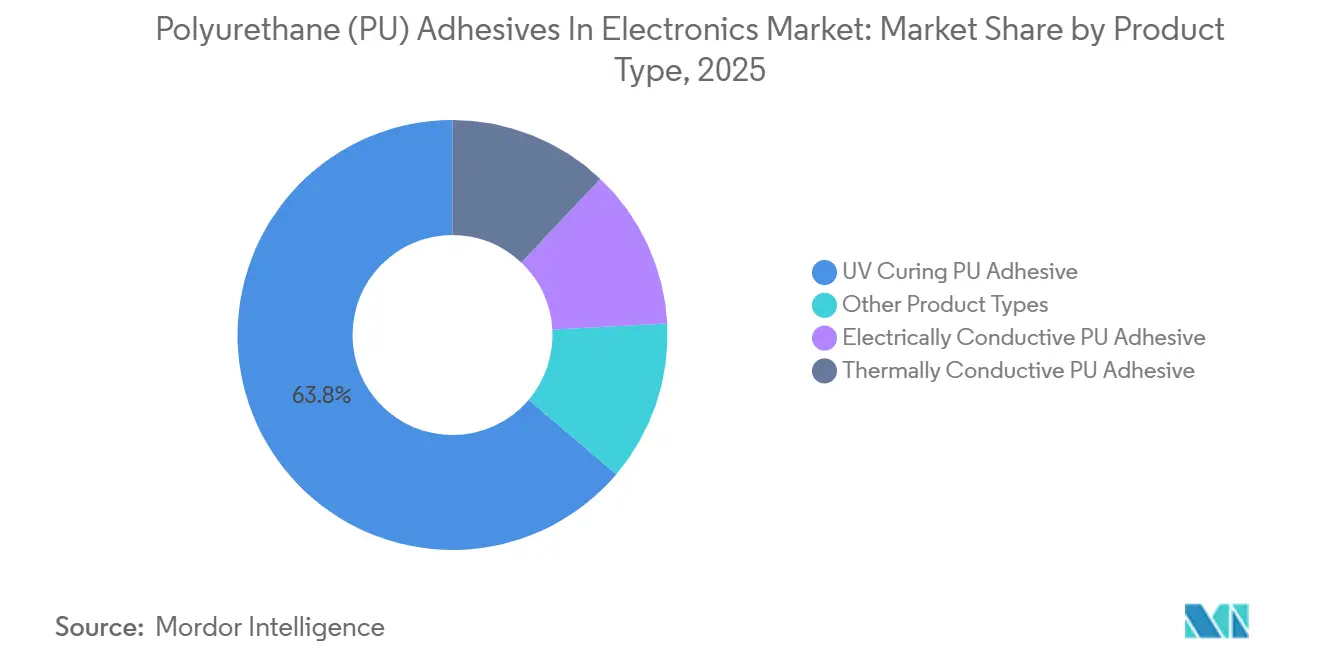

- By product type, UV-curing PU adhesive captured 63.78% of polyurethane adhesives in electronics market share in 2025, and it is projected to rise at a 5.33% CAGR through 2031.

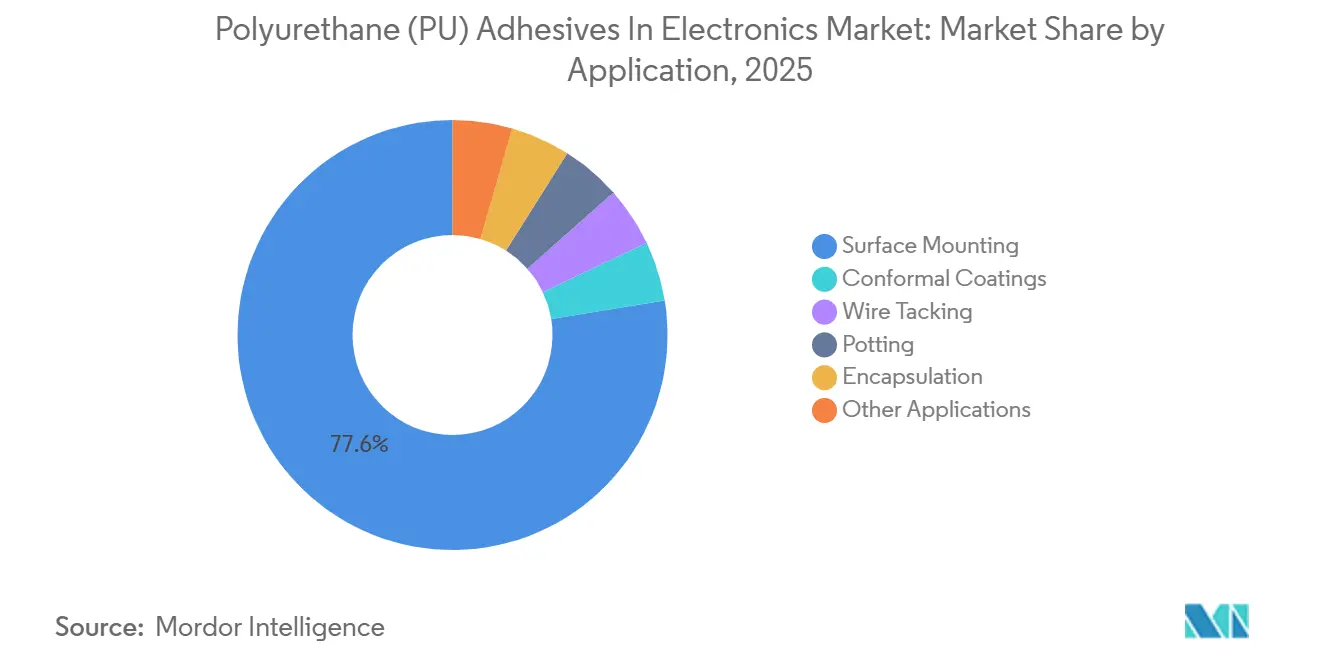

- By application, surface mounting accounted for 77.56% of polyurethane adhesives in electronics market share in 2025, and it is projected to rise at a 5.12% CAGR through 2031.

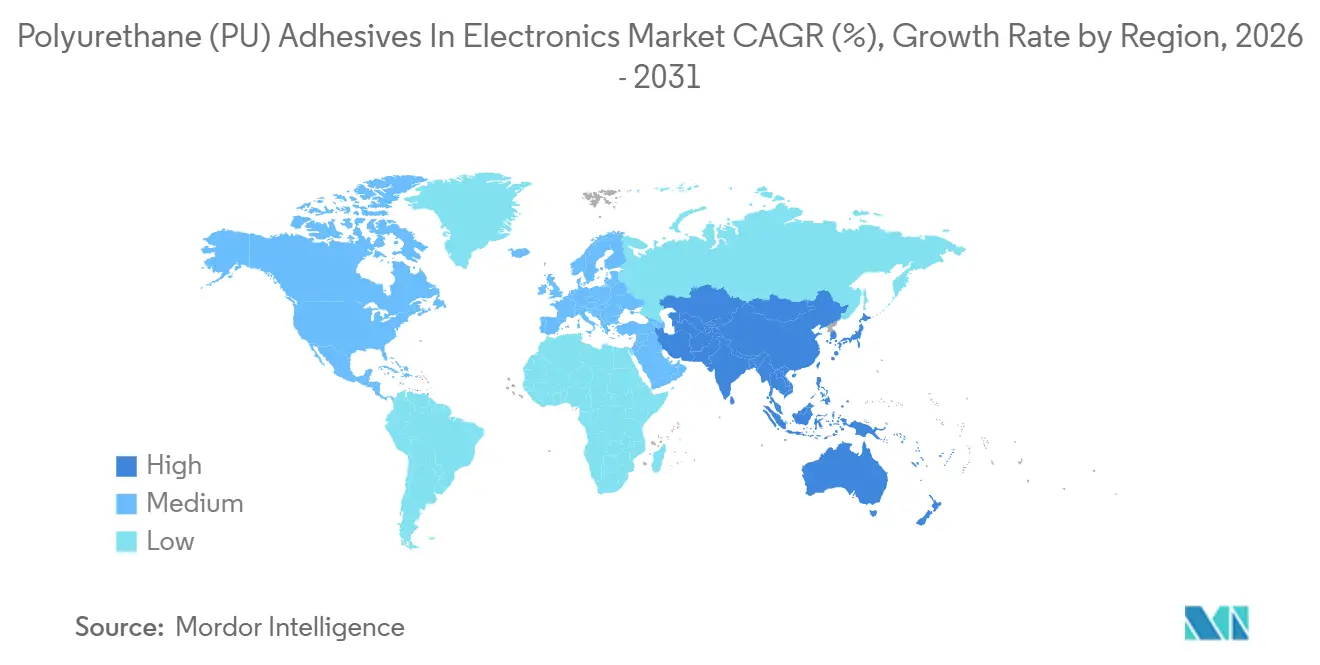

- By geography, Asia-Pacific accounted for 72.69% of polyurethane adhesives in electronics market share in 2025, and it is projected to rise at a 5.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Polyurethane (PU) Adhesives In Electronics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturization of Consumer Devices Boosting Demand for Low-Viscosity PU Potting Adhesives | +1.0% | Global, with concentration in APAC (China, South Korea, Vietnam) and spill-over to North America | Medium term (2-4 years) |

| EV Battery Thermal-Gap Fillers Based on Thermally Conductive PU | +1.3% | North America, Europe, APAC core (China, Japan, South Korea) | Long term (≥ 4 years) |

| Environmental Push toward Water-Borne, Low-VOC PU Dispersions | +0.7% | Europe (REACH compliance), North America (EPA regulations), early adoption in Japan | Short term (≤ 2 years) |

| Flexible Hybrid Electronics Needing Stretchable, Self-Healing PU Bonds | +0.5% | North America and EU (RandD hubs), pilot production in South Korea and Taiwan | Long term (≥ 4 years) |

| Active-Alignment Optics Modules – Ultra-Thin Shear-Stable PU | +0.4% | APAC core (Japan, South Korea, Taiwan), spill-over to North America automotive sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Miniaturization of Consumer Devices Boosting Demand for Low-Viscosity PU Potting Adhesives

Foldable phones, smartwatches, and true-wireless earbuds now feature printed-circuit-board (PCB) traces narrower than 50 µm, requiring potting materials capable of flowing into sub-millimeter gaps without trapping air. Products like Loctite STYCAST US 8000, with a viscosity of 350 cP at 25 °C, endure 10,000 thermal cycles ranging from −40 °C to 85 °C, enabling wearable medical monitors to meet IEC 60601 standards. Flex-PCB designs in foldable phones demand Shore A hardness below 60 to withstand daily bending without delamination, a requirement more cost-effectively met by polyurethane compared to silicone. Additionally, automotive driver-assistance cameras depend on optical-grade polyurethane with haze levels under 2% to maintain lens clarity throughout the vehicle's lifespan.

EV Battery Thermal-Gap Fillers Based on Thermally Conductive PU

As electric vehicle (EV) pack voltages increase to 800 V, original equipment manufacturers (OEMs) require thermally conductive polyurethane with conductivity exceeding 2 W/m·K and dielectric strength above 15 kV/mm to bond cells directly to aluminum cold plates. Bostik XPU TCA 202 achieves 3.2 W/m·K while retaining 8 MPa lap-shear strength after aging at 85 °C/85% RH. DuPont’s BETATECH series offers conductivity up to 4 W/m·K and aligns with aluminum’s thermal-expansion profile, reducing cycle fatigue in high-capacity battery packs. SikaForce 325 CB/L60 provides a 60-minute open time, enabling robotic dispensing across 100 kWh packs without rework. Flame-retardant grades compliant with UL 94 V-0 are essential in regions adopting UNECE R100, solidifying polyurethane’s role in next-generation EV battery systems.

Environmental Regulations Driving Adoption of Water-Borne, Low-VOC PU Dispersions

REACH Annex XVII limits free diisocyanate content to below 0.1 wt%, promoting the use of water-borne dispersions and blocked-isocyanate prepolymers in electronics assembly[1]European Chemicals Agency, “Annex XVII Restrictions: Diisocyanates,” echa.europa.eu . Covestro’s Bayhydrol system achieves VOC levels under 50 g/L while passing IPC-CC-830C adhesion tests on FR-4 laminates. In the United States, the EPA’s 420 g/L VOC limit for miscellaneous coating operations, effective January 2025, is accelerating the transition to low-VOC solutions in North America.

Flexible Hybrid Electronics Needing Stretchable, Self-Healing PU Bonds

Dynamic disulfide exchange enables polyurethane bonds to recover 95% of their tensile strength within 24 hours at room temperature, as demonstrated in 2024 experiments. Commercial prototypes, such as Master Bond EP42HT-2FG, achieve elongation-at-break above 300%, meeting fatigue life requirements for flexible biosensors integrated into athletic apparel. IPC-7351C now recommends peel strength above 5 N/cm and a glass transition temperature (Tg) below −20 °C for adhesives used in bendable circuits, benchmarks that are met by the latest polyurethane formulations.

Restraints Impact Analysis of Polyurethane (PU) Adhesives In Electronics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polyol and Di-Isocyanate Price Volatility | -0.9% | Global, acute in North America (propylene oxide supply) and Europe (energy-cost pass-through) | Short term (≤ 2 years) |

| Silane-Terminated Prepolymer Rise in Wearables | -0.5% | North America, Europe, Japan (wearable-device hubs) | Medium term (2-4 years) |

| Moisture-Cure Reliability in Fan-Out Packaging | -0.3% | APAC core (Taiwan, South Korea, China OSAT hubs), spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Polyol and Di-Isocyanate Price Volatility

Propylene-oxide outages at U.S. Gulf Coast facilities led to a 22% increase in polyol prices during Q4 2024, while MDI costs rose by 18% due to Chinese production restrictions. Smaller formulators without hedging capabilities faced challenges in passing these cost increases to SMT subcontractors operating on narrow margins, resulting in several exits from Southeast Asia's polyurethane adhesives market for electronics. In response, multinational companies pursued backward integration strategies. For instance, Henkel's 2024 investment in a Guangdong polyol unit reduced its regional cost base by 12%.

Silane-Terminated Prepolymer Adoption in Wearables

Isocyanate-free silane-terminated polymers (STPs) have simplified compliance with Occupational Safety and Health Administration regulations, prompting smartwatch OEMs to adopt MS Polymer for sapphire-glass bonding. Testing by Fraunhofer IFAM demonstrated that STPs retained 90% of lap-shear strength after 2,000 hours of xenon-arc exposure, outperforming aromatic-isocyanate polyurethane (PU) equivalents. However, in low-humidity manufacturing environments, the slower cure kinetics of STPs have allowed moisture-cure polyurethane adhesives to maintain their market share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Polyurethane (PU) Adhesives In Electronics Market Segment Analysis

By Product Type:

UV-Curing Adhesives Lead in Speed-Critical ApplicationsUV-curing polyurethane adhesives accounted for 63.78% of the 2025 market share and are projected to grow at a 5.33% CAGR through 2031. Products like Dymax 9014-F-VT, offering 25 MPa tensile strength and 80% elongation, have become benchmarks for rigid-flex PCBs in 125°C under-hood modules.

Advancements in materials, such as the combination of spherical aluminum oxide with boron nitride platelets, have increased thermal conductivity to nearly 5 W/m·K without reducing the 60-minute open time required by SMT integrators. Additionally, graphene nanofillers have reduced silver content in electrically conductive PU to 50 wt% while maintaining over 60 dB shielding at 1 GHz. The adoption of LED sources at 365 nm and 405 nm has decreased energy consumption by 70% compared to mercury lamps, further supporting the sustainability of UV-curing polyurethane adhesives in electronics.

By Application:

Surface Mounting Drives Revenue GrowthSurface mounting contributed 77.56% of 2025 revenue and is expected to grow at a 5.12% CAGR through 2031, driven by the proliferation of 01005 passives, which require adhesives with viscosities below 3,000 cP and a thixotropic index above 3.5.

Potting compounds meeting MIL-I-46058C insulation standards of more than 10¹² Ω at 500 V and UL 746E thermal indices of ≥130°C dominate radar-module encapsulation, reinforcing polyurethane's technical advantages over epoxies. Optically clear polyurethane adhesives with haze levels below 1% support premium OLED smartphone stacks, while UL 94 V-0 flame-retardant grades are used for bonding nickel-plated busbars in EV pack-to-chassis designs, highlighting polyurethane adhesives' relevance across diverse applications.

Geography Analysis

APAC Polyurethane (PU) Adhesives In Electronics Market

Asia-Pacific accounted for 72.69% of global revenue in 2025 and is projected to grow at a 5.23% CAGR through 2031. This growth is driven by China's contract manufacturers, which assemble two-thirds of the world's smartphones, as well as South Korea's OLED production facilities and Japan's precision-optics industry. Vietnam's electronics exports, valued at USD 150 billion in 2025, are also boosting local adhesive consumption[2]Vietnam GSO, “Electronics Export Data 2025,” gso.gov.vn .

North America Polyurethane (PU) Adhesives In Electronics Market

In North America, the U.S. Inflation Reduction Act has incentivized domestic EV battery value chains. Henkel's 2024 expansion in Connecticut is expected to supply 5,000 t/y of thermally conductive grades by 2027. Mexico's Nuevo León cluster consumes 1,200 t/y for control-unit assembly, while Canada's avionics sector demands MIL-spec potting compounds.

EMEA and South America Polyurethane (PU) Adhesives In Electronics Market

In Europe, Germany's automotive electronics ecosystem and the U.K.'s compound semiconductor industry lead regional demand. While South America and the Middle- East and Africa hold smaller shares of global revenue, Brazil's Manaus free zone and Saudi Arabia's Vision 2030 initiatives are expanding the regional footprint of polyurethane adhesives in electronics.

Competitive Landscape

Five leading suppliers, Henkel, 3M, Dow, H.B. Fuller, and Covestro, control 64% of global revenue, indicating moderate concentration. Henkel’s Guangdong polyol line reduced delivered costs by 12%, demonstrating the use of vertical integration to mitigate feedstock volatility. Dow’s co-development agreement with CATL on cell-to-pack adhesives highlights the growing trend of embedded engineering partnerships. Patent filings reveal competition in developing hybrid UV/moisture systems to address shadow-cure voiding; Henkel filed 14 such patents in 2025, while 3M concentrated on silane-modified backbones to eliminate risks associated with free-isocyanate handling.

Regional players Huitian and Kangda exploit lower polyol costs to win consumer-electronics programs, whereas niche specialists like DELO and Master Bond target high-margin optical bonding and hermetic encapsulation. Key trends, including LED curing, REACH compliance, and the thermal management requirements of electric vehicles, continue to shape the feature roadmaps of polyurethane adhesives in the electronics market.

Polyurethane (PU) Adhesives In Electronics Industry Leaders

3M

Henkel AG & Co. KGaA

Dow

H.B. Fuller Company

Covestro AG

- *Disclaimer: Major Players sorted in no particular order

Polyurethane (PU) Adhesives In Electronics Market Companies Covered in this Report

- 3M

- Arkema

- Ashland

- Avery Dennison Corporation

- BASF

- Covestro AG

- DELO Industrie

- Dow

- Dymax

- Epic Resins

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huitian New Materials

- Huntsman International LLC.

- INTERTRONICS

- ITW Performance Polymers

- Kangda New Materials (Group) Co., Ltd

- Master Bond

- Parker Hannifin Corp

- Permabond

- Sika AG

- TEX YEAR

Recent Industry Developments in Polyurethane (PU) Adhesives In Electronics Market

- April 2025: TEX YEAR launched R3220, a bio-based polyurethane reactive hot melt adhesive designed for sustainable electronic product assembly. It featured 40% bio-based content, providing a low-odor, environmentally friendly solution that reduced carbon emissions while ensuring high-performance bonding for electronics.

- February 2025: Researchers at the University of Reading, in partnership with Domino Printing Sciences, developed a modified polyurethane (PU) adhesive that enabled labels to be removed cleanly from plastic bottles, enhancing the quality of recycled materials. This development is expected to influence the use of PU adhesives in electronics by promoting cleaner and more efficient recycling processes.

Global Polyurethane (PU) Adhesives In Electronics Market Report Scope

Polyurethane (PU) adhesives play a critical role in electronics by providing excellent moisture and chemical resistance, flexibility, and vibration damping. These properties are essential for safeguarding sensitive components in devices such as smartphones, wearables, and electric vehicles (EVs). Their use in applications like potting and UV-curing is also growing.

The Polyurethane (PU) Adhesives In Electronics Market is segmented by product type, application, and geography. By product type, the market is segmented into UV curing PU adhesive, electrically conductive PU adhesive, thermally conductive PU adhesive, and other product types. By application, the market is segmented into surface mounting, conformal coatings, wire tacking, potting, encapsulation, and other applications (e.g., display bonding and optical assemblies, battery assembly). The report also covers the market size and forecasts for polyurethane (PU) adhesives in electronics in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

Segmentation Overview

| UV Curing PU Adhesive |

| Electrically Conductive PU Adhesive |

| Thermally Conductive PU Adhesive |

| Other Product Types |

| Surface Mounting |

| Conformal Coatings |

| Wire Tacking |

| Potting |

| Encapsulation |

| Other Applications (Display Bonding and Optical Assemblies, Battery Assembly, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | UV Curing PU Adhesive | |

| Electrically Conductive PU Adhesive | ||

| Thermally Conductive PU Adhesive | ||

| Other Product Types | ||

| By Application | Surface Mounting | |

| Conformal Coatings | ||

| Wire Tacking | ||

| Potting | ||

| Encapsulation | ||

| Other Applications (Display Bonding and Optical Assemblies, Battery Assembly, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the polyurethane (PU) adhesives in electronics market?

The polyurethane adhesives in the electronics market stand at USD 1.35 billion in 2026 and is projected to reach USD 1.72 billion by 2031.

Which product type holds the largest polyurethane adhesives in electronics market share in 2025?

UV-curing polyurethane adhesive leads with 63.78% of 2025 revenue.

Which geographic region dominates demand in 2025?

Asia-Pacific accounts for 72.69% of global 2025 sales.

How are tightening VOC rules affecting formulations?

Suppliers are shifting toward water-borne dispersions and blocked-isocyanate systems that meet REACH and EPA limits without reducing throughput.

Page last updated on: