Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

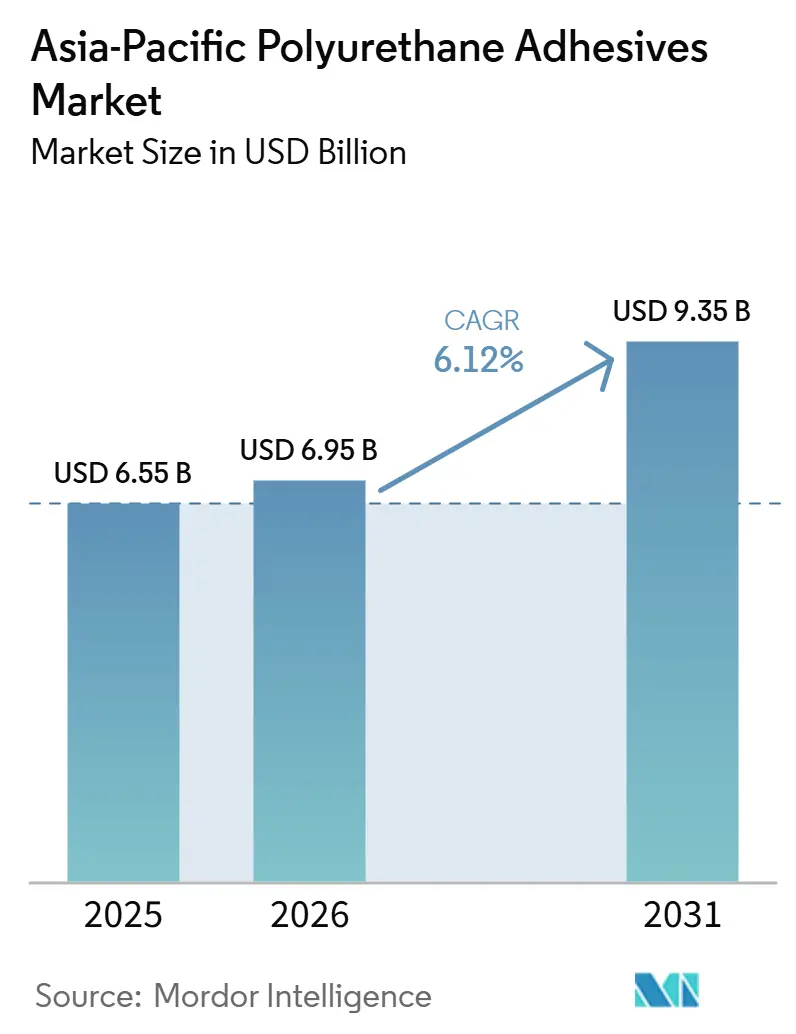

| Base Year Market Size (2025) | USD 6.55 Billion |

| Market Size (2026) | USD 6.95 Billion |

| Market Size (2031) | USD 9.35 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

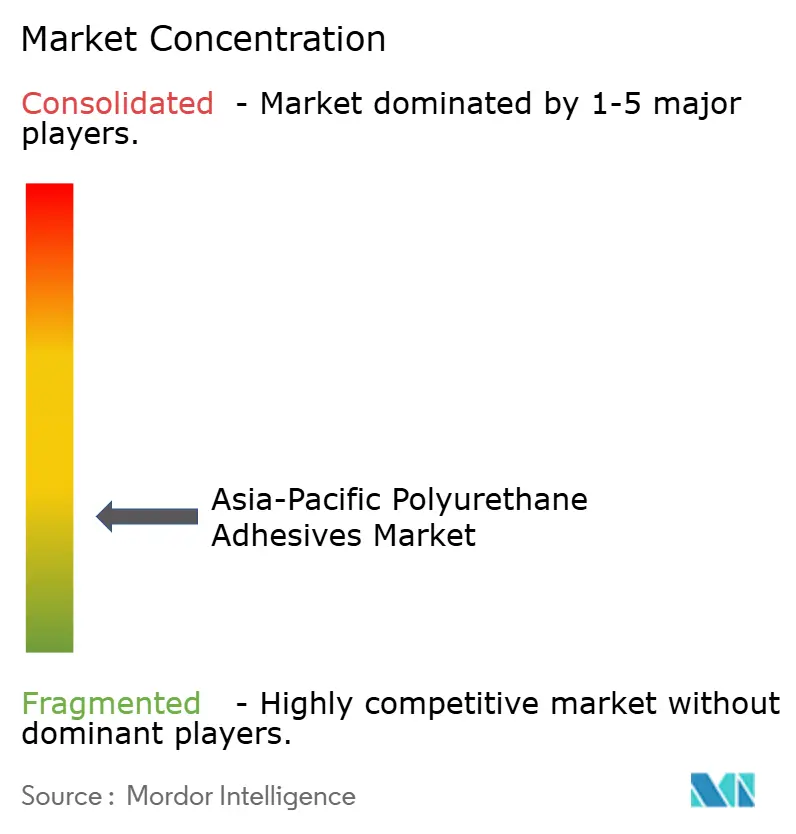

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Polyurethane Adhesives Market Analysis by Mordor Intelligence

The Asia-Pacific polyurethane adhesives market size is expected to grow from USD 6.55 billion in 2025 to USD 6.95 billion in 2026 and is forecast to reach USD 9.35 billion by 2031 at a 6.12% CAGR over 2026-2031. Electric-vehicle battery assembly, e-commerce packaging, and stringent green-building mandates underpin demand while an oversupply of isocyanate feedstocks keeps raw-material costs volatile. Chinese producers retained cost leadership but faced double-digit construction slowdowns that shifted growth toward India, Vietnam, and Indonesia. Hot-melt and moisture-curing systems gained favor because they cut processing energy by up to 15 °C and meet low-VOC rules across footwear, flexible packaging, and electronics.

Key Report Takeaways

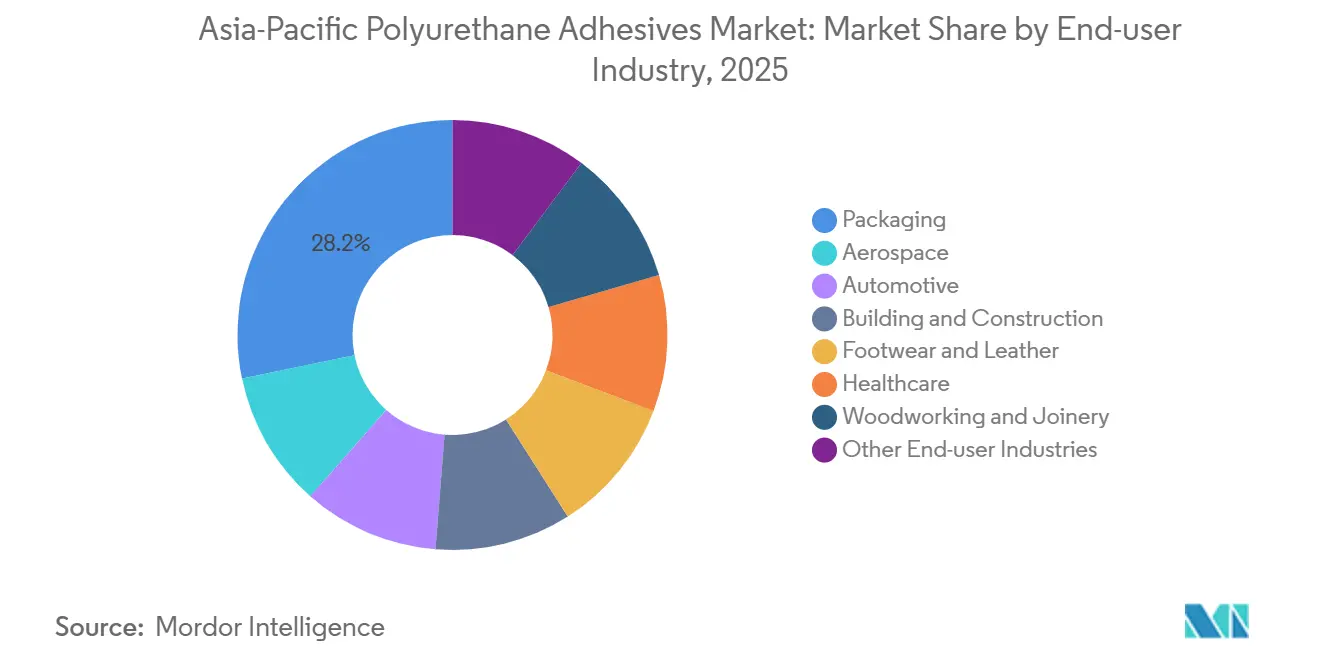

- By end-user industry, packaging led with 28.24% of the Asia-Pacific polyurethane adhesives market share in 2025. Automotives are forecast to expand at a 6.94% CAGR between 2026 and 2031.

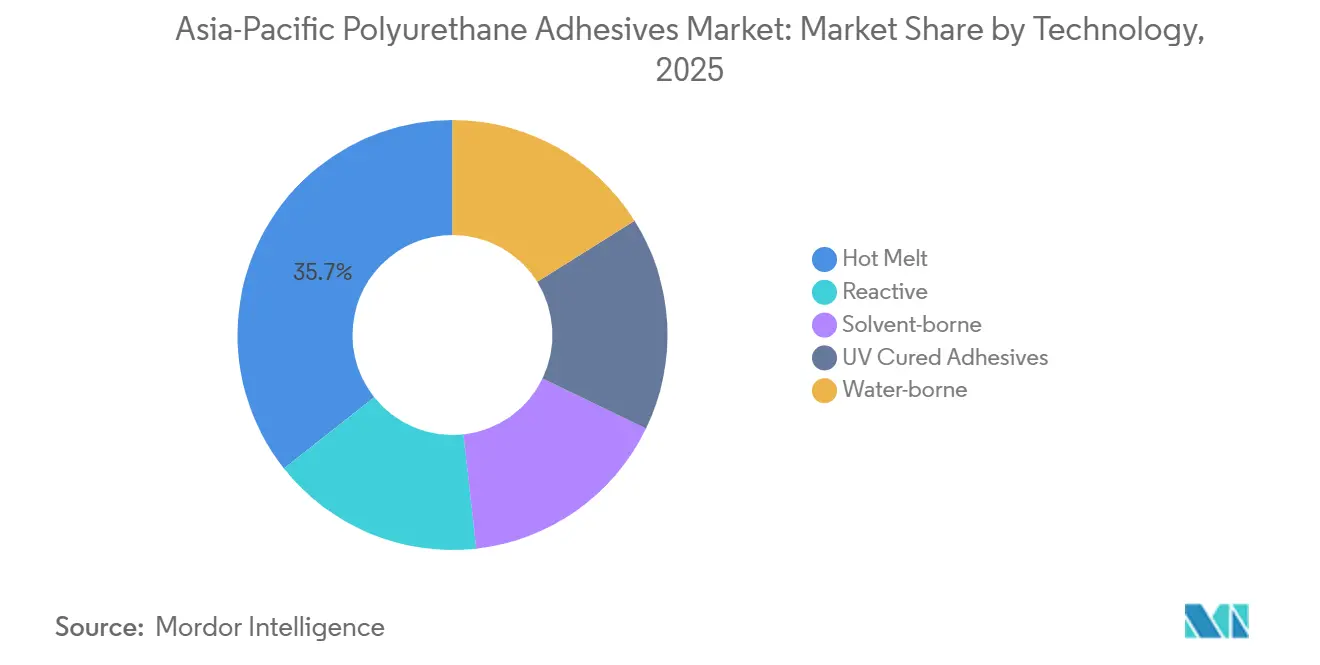

- By technology, hot-melt commanded 35.67% of the Asia-Pacific polyurethane adhesives market share in 2025. Reactive systems are projected to record the fastest 6.66% CAGR during the forecast period (2026-2031).

- By geography, China accounted for 46.92% of 2025 revenue, and India is the fastest-growing country, advancing at a 7.12% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Polyurethane Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in building-envelope retrofits post-COVID era | +1.2% | China, India, Japan, South Korea; concentrated in tier-1/2 cities | Medium term (2-4 years) |

| Automotive lightweighting push for EV range extension | +1.5% | China, Japan, South Korea, India; spillover to Thailand automotive clusters | Long term (≥ 4 years) |

| E-commerce packaging shift to high-performance laminates | +1.1% | Southeast Asia (Vietnam, Indonesia, Malaysia), China coastal provinces | Short term (≤ 2 years) |

| 3C electronics adoption of low-VOC PUR hot-melts | +0.9% | China (Pearl River Delta, Yangtze Delta), Vietnam, Malaysia electronics zones | Medium term (2-4 years) |

| Green-building regulations spurring rigid panel bonding | +0.8% | Singapore, Australia, China (green transition investments), India (smart cities) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Building-Envelope Retrofits Post-COVID Era

As owners pursue lower operating costs and commit to net-zero goals, refurbishment budgets in major cities are on the rise. In a significant move, China invested a whopping USD 550 billion into low-carbon construction, subsequently boosting the demand for polyurethanes, especially in insulation-panel bonding and waterproofing membranes. Under Singapore’s Land Transport Master Plan 2040, newly added rail stations are opting for fire-resistant rigid-foam adhesives. These adhesives are designed to bond with aged steel or concrete, even at ambient cure. Moisture-curing grades are flourishing in the market due to their ability to tolerate surface contaminants, thereby reducing downtime. This trend is mirrored in India's smart-city corridors and Japan's aging high-rise buildings. However, the influx of inexpensive Chinese MDI poses a challenge, potentially squeezing margins for converters. Yet, segment suppliers who combine unique primers with on-site training are managing to capture market share, even amidst pricing pressures.

Automotive Lightweighting Push for EV Range Extension

Automakers are increasingly turning to two-component polyurethanes, moving away from traditional rivets and epoxies. These polyurethanes are adept at bonding cell modules, sealing aluminum housings, and creating thermally conductive gap fillers. H.B. Fuller’s UR4515GF achieves a lap-shear strength of 20.05 MPa on E-coat steel after a 70 °C, 120-minute cure, making it a perfect fit for automated EV assembly lines[1]H.B. Fuller, “UR4515GF Technical Data Sheet,” hbfuller.com . Launched in 2025, Henkel’s Technomelt PUR 6260 ECO boasts over 60% renewable feedstock and softens at a mere 50 °C, leading to energy savings in ovens and safeguarding heat-sensitive substrates[2]Henkel AG, “Technomelt PUR 6260 ECO Press Release,” henkel.com. With OEMs extending their ranges to exceed 600 km per charge, the shift towards adhesive substitution becomes evident. Furthermore, India's automotive sector, growing at a CAGR of 7.12%, presents lucrative opportunities for local formulators who align with localization quotas.

E-Commerce Packaging Shift to High-Performance Laminates

In Vietnam and Indonesia, online retail volumes surged by 17% year-on-year, spurring a shift towards flexible-laminate conversions that depend on fast-setting polyurethane hot-melts. These reactive hot-melts not only reduce storage dwell time but also bolster just-in-time logistics. With footwear exports reaching 7.2 billion pairs in 2024, there was a heightened demand for thin adhesive films. These films bond rubber to synthetic uppers, ensuring a VOC-free process. Furthermore, water-based dispersions have slashed solvent usage by up to 95%, facilitating smoother OEKO-TEX compliance in export factories. Regional converters, by incorporating nitrogen-flush dispensing and in-line migration analytics, have accelerated their food-contact safety measures, outpacing competitors and securing packaging contracts from multinational corporations.

3C Electronics Adoption of Low-VOC PUR Hot-Melts

Smartphones, tablets, and wearables increasingly rely on adhesives that cure swiftly, resist cleaning solvents, and flex seamlessly with miniaturized boards. UV-curable polyurethane acrylates achieve a tack-free state in just 6 seconds under a 100 mW/cm² light, enhancing throughput in touchscreen modules. To meet RoHS audits, assemblers in China and Vietnam are now opting for moisture-curing grades with less than 50 ppm of free isocyanate. Meanwhile, Japanese tape manufacturers have introduced water-based urethane systems, ensuring toluene levels are below detection limits, leading to greater adoption in appliances and automotive interiors. As AI edge devices and foldable screens gain traction, suppliers providing formulations that offer both low-temperature curing and electrical conductivity stand to benefit significantly.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in MDI/TDI feedstock prices | -1.3% | Global, with acute exposure in import-dependent Southeast Asia and India | Short term (≤ 2 years) |

| Fire-safety regulatory scrutiny on combustible cores | -0.6% | Australia, Singapore, Japan; emerging in China tier-1 cities | Medium term (2-4 years) |

| OEM qualification cycles delaying tech substitution | -0.4% | China, Japan, South Korea automotive; India automotive localization | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fire-Safety Regulatory Scrutiny on Combustible Cores

Heightened fire-safety standards for polyurethane adhesives in construction applications impose testing burdens and formulation constraints that act as a market restraint, slowing adoption in certain building segments. Australia’s AS 5637.1 group-number scheme can push an otherwise compliant panel assembly into costly full-scale fire tests if the adhesive layer shrinks or melts. Korean researchers cut peak heat-release rate 30% by adding phosphorylated polyvinyl alcohol plus magnesium-aluminum layered double hydroxides to water-borne polyurethane, yet bonding strength held above 0.70 MPa. Such additives raise viscosity and cost, so adoption lags until mandated by project insurers.

OEM Qualification Cycles Delaying Tech Substitution

Battery-pack adhesives face rigorous testing, enduring thermal shocks from -40 °C to 80 °C, as well as vibration and crush tests. This meticulous process spans 18 to 36 months before receiving the final sign-off. Smaller innovators, often without the luxury of multiple testing lines, find it challenging to manage parallel programs across five or more OEMs, which acts as a market restraint by delaying cash flow. In contrast, established multinationals, with regional labs situated in Suzhou or Pune, adeptly navigate these timelines. By doing so, they secure early design victories, further cementing their dominant position in the Asia-Pacific polyurethane adhesives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Packaging Retains Lead, Automotive Surges

Packaging represented 28.24% of the Asia-Pacific polyurethane adhesives market size in 2025 thanks to flexible-laminate formats used for snacks, pharmaceuticals, and e-commerce mailers. Growth hinges on moisture-curing reactive hot-melts that deliver hermetic seals within seconds and cut energy versus solvent-borne lines. Regional laminate plants that install nitrogen-inerted gravure presses avoid condensation defects, supporting bigger lot sizes for instant noodles and condiments. Automotive uses, although smaller in tonnage, grow at 6.94% CAGR as EV battery modules, lightweight body panels, and acoustic foams demand two-component polyurethanes and thermoplastic polyurethane films. The Asia-Pacific polyurethane adhesives market now prizes suppliers able to certify thermal conductivity ≥2 W/m·K and provide crash simulation data that meet GB /T 33014 side-impact protocols.

Construction adhesives benefit from insulation retrofits but face slow project approvals in China’s tier-3 cities. Footwear factories in Vietnam and Indonesia convert to water-based polyurethane dispersions that slash VOCs by 90–95%. Medical tapes coated with breathable polyurethane interact well with hydrocolloid layers, expanding wound-care exports from Malaysia. Woodworking taps reactive hot-melts for engineered-wood flooring because clamp times drop 50%, boosting line capacity without new kilns. These niche areas collectively sustain baseline growth even if packaging or automotive cycles soften, keeping demand broad-based within the Asia-Pacific polyurethane adhesives market.

By Technology: Hot-Melt Dominates, Reactive Systems Climb

In 2025, hot-melt grades commanded a 35.67% share of the Asia-Pacific polyurethane adhesives market. Their rapid green strength achievement, compatibility with standard slot or swirl coaters, and solvent-free operation make them a preferred choice. This segment is driven by low-viscosity variants, which remain molten at 110-130 °C, for applications like shoe uppers, diaper tabs, and paperback book spines. These variants form bonds resilient to skin oils and talc. Their cost-per-gram advantage ensures baseline volumes, enabling suppliers to recoup reactor investments. Reactive systems, projected to grow at a 6.66% CAGR, are set to double their market share by 2031. This segment's growth is driven by the demand for chemical crosslinks in EV modules, glazing units, and electronics boards, which offer resistance to acid gases, cyclic heat, and vibration. One-component grades, such as 3M TE100, achieve handling strength in just 60 seconds, streamlining vertical assembly lines and minimizing jig requirements.

Water-borne polyurethane dispersions benefit from favorable regulations. This segment is supported by factories transitioning from solvent-borne to aqueous systems, which not only reduce flammable storage insurance premiums but also meet REACH thresholds without the need for regenerative oxidizers. While UV-curable formulations account for less than 4% of the volume, they play a crucial role in providing optical-clear bonds for mini-LED displays and medical devices. Their lap-shear strengths of 14.0 MPa on polycarbonate make them competitive with epoxies, all without the need for thermal curing. Research into bio-based solutions is gaining momentum. For instance, lignin-based polyols produce hot-melts with an impressive 68.37 N/25 mm T-peel strength and antibacterial properties. This aligns with Japan's push towards zero-plastic tax proposals. Overall, the diverse technological advancements signal a shift in the Asia-Pacific polyurethane adhesives market towards premium, eco-friendly solutions over the forecast horizon.

Geography Analysis

In 2025, China held a dominant 46.92% share of the Asia-Pacific polyurethane adhesive market. However, with real estate downturns dampening construction demand, Sika made the strategic decision to reduce its plant network to 25 sites by 2027. On a different note, BASF is ramping up its Caojing facility, expanding to an 18,800 t/y resin capacity, all powered by renewable electricity, with a focus on high-performance coatings and adhesive intermediates. Meanwhile, Wanhua's push at its Fujian line is set to elevate its total MDI capacity to 4.5 million t/y by mid-2026, solidifying China's dominance in feedstock and stabilizing export parity pricing.

India emerges as the fastest-growing hub in the Asia-Pacific polyurethane adhesives market, boasting a 7.12% CAGR. This growth is fueled by infrastructure developments, automotive localization, and a surging appliance market. Domestic formulators are bolstering their backward integration into polyester polyols, reducing reliance on imports, and aligning with automakers in Pune, Chennai, and the Delhi-Mumbai Industrial Corridor. Additionally, government incentives for solar module and electronics assembly are expanding the use of polyurethane in back-sheet lamination and device gasketing.

Southeast Asia showcases a divided landscape. While Vietnam and Indonesia lead in footwear adhesive production, Vietnam's reliance on Chinese hot-melt film imports exposed its vulnerabilities during shipping disruptions in the Red Sea and Taiwan Strait. On the other hand, Indonesia, Malaysia, and the Philippines have become hubs for packaging capacity, drawing businesses from pricier coastal China, bolstered by free-trade agreements and a growing population. Thailand, despite witnessing output declines due to sluggish tourism and auto production, continues to host regional R&D centers for Japanese OEMs, ensuring a steady demand for specialty-grade imports.

Australia and Singapore, despite their size, command significant value in the market. Singapore's construction sector, projected to grow at a 4.1% CAGR through 2028, is driving adhesive demand for MRT tunnels and eco-friendly skyscrapers. In response, Sika has optimized its automated mortar plant, achieving a 30% reduction in batch-cycle energy. Meanwhile, Australia's stringent AS 5637.1 fire code is pushing demand for premium formulations, favoring suppliers capable of conducting cone-calorimetry and full-scale tests in-house. These evolving dynamics across regions are steering the Asia-Pacific polyurethane adhesives market towards a more balanced demand landscape, reducing over-reliance on any single nation.

Competitive Landscape

Asia-Pacific polyurethane adhesives market exhibits a fragmented nature. Multinationals like Henkel, Sika, H.B. Fuller, 3M, BASF, and Dow are countering raw-material volatility by deploying digitalized plants and localized labs. Sika's Fast-Forward program, aiming for annual savings of USD 165-220 million by 2028, is leveraging ERP harmonization and machine-learning formulation software to slash lab cycles by 75%. Meanwhile, Henkel's bio-based PUR 6260 ECO showcases a premium-priced sustainability initiative, and H.B. Fuller is enhancing gap-filler grades with thermal conductivity exceeding 3 W/m·K, targeting the next-gen 4680 cylindrical cells.

Chinese players like Kangda are boosting their capacities, capitalizing on government incentives and their closeness to EV OEM clusters. In India, market leader Pidilite is broadening its Fevicol-brand polyurethane sealants into panel manufacturing lines, fortifying its local market share against imports.

Innovations are emerging in areas like debond-on-demand chemistries for EV battery recycling, lignin-based bio-polyols, and smart adhesives tailored for 5G module conductivity. Start-ups such as Algenesis have rolled out a 100% bio-based non-phosgene isocyanate dubbed “Bio-Iso,” yet scaling up poses challenges. Ultimately, firms that blend robust R&D with regionally integrated supply chains are finding commercial success, underscoring a moderate-concentration landscape in the Asia-Pacific polyurethane adhesives arena.

Asia-Pacific Polyurethane Adhesives Industry Leaders

3M

Sika AG

Henkel AG & Co. KGaA

H.B. Fuller Company

Huntsman International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BASF Coatings has successfully doubled its polyester and polyurethane (PU) resin production capacity at its Caojing plant in Shanghai, China, to 18,800 metric tons per year.

- June 2025: Sika expanded its Suzhou site for high-viscosity polyurethane to serve automotive and construction sealants.

Asia-Pacific Polyurethane Adhesives Market Report Scope

Polyurethane (PU) adhesives are versatile, high-strength polymers formed by reacting isocyanates with polyols, known for their excellent flexibility, durability, and resistance to water and chemicals. These adhesives are ideal for bonding dissimilar materials, such as plastics, metals, wood, and glass, making them popular in construction, automotive, and footwear industries.

The Asia-Pacific Polyurethane Adhesives market report is segmented by technology, end-user industry, and geography. By end-user industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, woodworking and joinery, other end-user industries. By technology, the market is segmented into hot melt, reactive, solvent-borne, uv cured adhesives, water-borne. The report also covers the market size and forecasts for polyurethane adhesives in 9 countries across the Asia-Pacific region. For each segemnt market sizing and forecasts are provided in terms of value (USD).

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-user Industries |

Technology

| Hot Melt |

| Reactive |

| Solvent-borne |

| UV Cured Adhesives |

| Water-borne |

By Country

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| Singapore |

| South Korea |

| Thailand |

| Rest of Asia-Pacific |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-user Industries | |

| Technology | Hot Melt |

| Reactive | |

| Solvent-borne | |

| UV Cured Adhesives | |

| Water-borne | |

| By Country | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| Singapore | |

| South Korea | |

| Thailand | |

| Rest of Asia-Pacific |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the polyurethane adhesives market.

- Product - All polyurethane adhesive products are considered in the market studied

- Resin - Under the scope of the study, thermoset and thermoplastic based polyurethanes are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms