Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

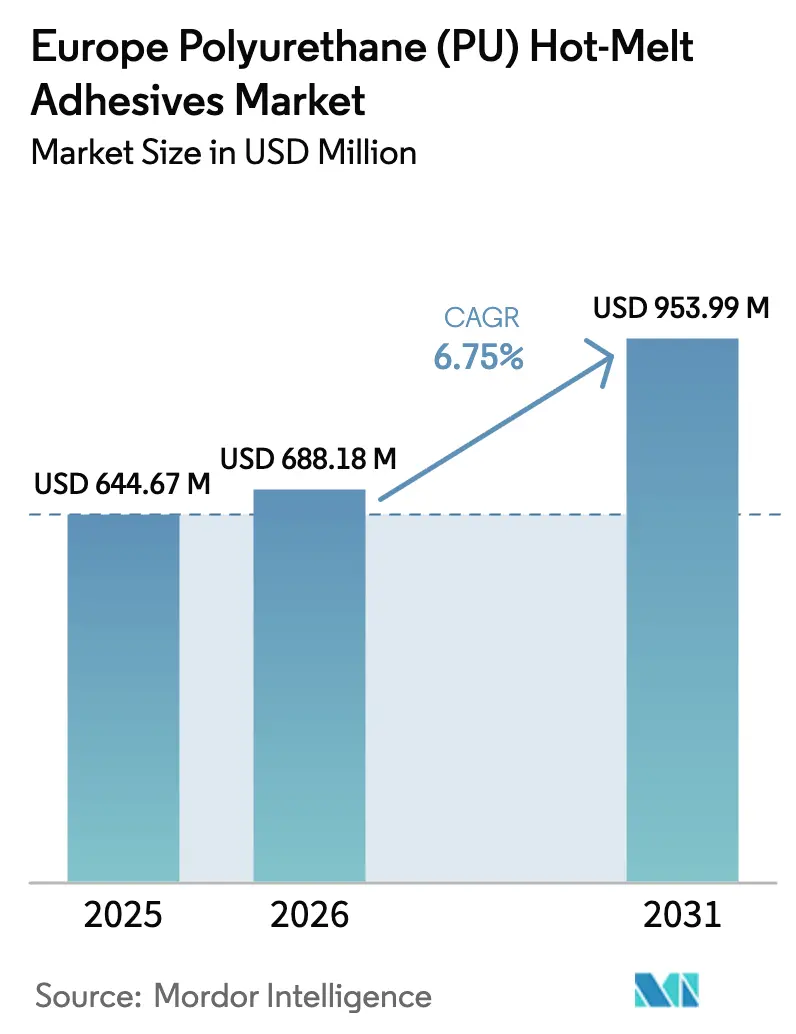

| Base Year Market Size (2025) | USD 644.67 Million |

| Market Size (2026) | USD 688.18 Million |

| Market Size (2031) | USD 953.99 Million |

| Growth Rate (2026 - 2031) | 6.75% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Polyurethane (PU) Hot-Melt Adhesives Market Analysis by Mordor Intelligence

The Europe Polyurethane Hot-Melt Adhesives Market size is projected to expand from USD 644.67 million in 2025 and USD 688.18 million in 2026 to USD 953.99 million by 2031, registering a CAGR of 6.75% between 2026 to 2031. Accelerated migration away from solvent-based chemistries, rising automation in edge-banding and vehicle assembly, and the quest for lighter, repair-friendly packaging are steering volume toward high-performance reactive formulations. Western European parcel networks handled 2.1 billion intra-EU shipments in 2025, broadening the customer base for fast-setting grades that tolerate recycled board and high-speed case sealers. Automotive OEMs are substituting mechanical fasteners with polyurethane bonding to cut body-in-white weight by up to 2 kg per roof panel, directly improving electric-vehicle range. At the same time, furniture lines in Germany, Poland, and Italy have adopted zero-joint edge-banding equipment that demands adhesives curing in less than 10 seconds at 25 m min line speeds. Supply risk for isocyanate feedstocks has elevated input-cost volatility, but leading formulators are hedging by backward-integrating polyol capacity and experimenting with bio-based intermediates to soften exposure.

Key Report Takeaways

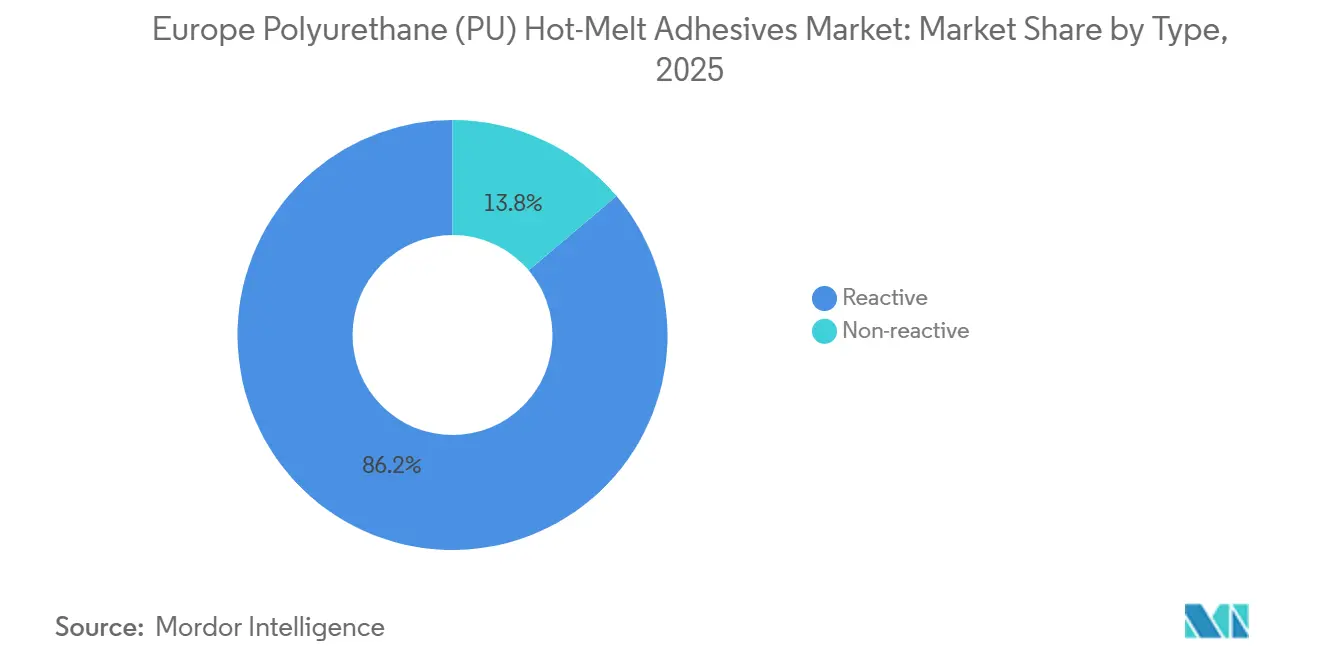

- By type, reactive grades captured 86.20% of the Europe polyurethane (PU) hot-melt adhesives market share in 2025. Non-reactive grades lag in growth, while reactive grades are forecast to expand at a 6.92% CAGR during the forecast period (2026-2031).

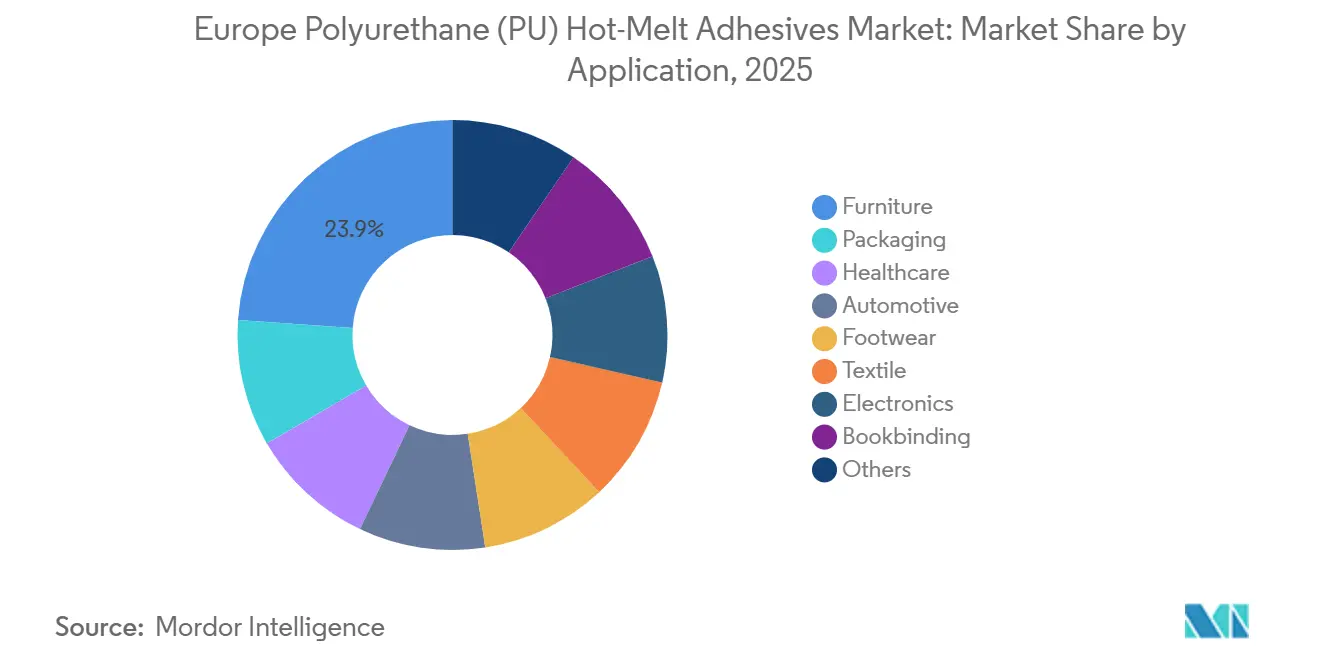

- By application, furniture accounted for 23.89% of 2025 revenue, whereas healthcare is advancing at a 7.26% CAGR during the forecast period (2026-2031).

- By geography, Germany led with 28.21% revenue share in 2025 and is on track for a 7.16% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Polyurethane (PU) Hot-Melt Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce packaging volumes | +1.20% | Western Europe (Germany, France, UK, Benelux), with spillover to Spain and Italy | Medium term (2-4 years) |

| Electronics assembly shift toward low-VOC bonding | +0.70% | Germany, Netherlands, France, Czech Republic (electronics manufacturing hubs) | Medium term (2-4 years) |

| European Union VOC rules accelerating solvent-free adhesive adoption | +1.50% | EU-wide, strongest enforcement in Germany, France, Netherlands, and Scandinavia | Long term (≥ 4 years) |

| Automotive lightweight structures needing fast-cycle bonding | +0.90% | Germany, France, Italy, Spain (core automotive manufacturing hubs) | Medium term (2-4 years) |

| Edge-banding automation in modular furniture lines | +0.80% | Western Europe, particularly Germany, Poland, Italy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in E-Commerce Packaging Volumes

Cross-border parcel traffic within the European Union rose 12% year-on-year to 2.1 billion units in 2025. Higher throughput has pushed fulfillment centers to replace slower water-based adhesives with reactive grades that set within five seconds on recycled corrugated substrates. Henkel’s Technomelt Supra 100 series, launched in early 2025, withstands the impact loads of automated sorters while bonding to lower-grammage liners. Upcoming European Union (EU) Packaging and Packaging Waste Regulation targets 65% recycled content by 2030, further tilting specifications toward chemistries that perform on rougher fiber surfaces[1]Directorate-General Environment, “Packaging and Packaging Waste Proposal,” ec.europa.eu. Bostik recorded a 15% jump in European packaging-adhesive revenue in 2025, noting that polyurethane hot melts supplied more than half of the incremental growth.

European Union VOC Rules Accelerating Solvent-Free Adhesive Adoption

The Industrial Emissions Directive caps plant-level VOC emissions at 50 g kg adhesive applied, eliminating most solvent-based contact adhesives from new European installations. Germany’s TA Luft revision in 2024 tightened the limit to 20 g/kg for furniture and automotive lines, cementing the transition to 100%-solids polyurethane hot melts[2]Federal Ministry for the Environment, “TA Luft 2024 Update,” bmuv.de. Covestro’s Desmomelt portfolio, which emits zero VOCs (Volatile Organic Compounds) and cures via ambient moisture, registered a 22% sales rise in 2025 as OEMs (Original Equipment Manufacturers) prioritized compliance-ready alternatives. France’s ICPE (Installations classified for environmental protection) framework now requires annual VOC audits for plants using more than one ton of adhesive, raising fixed administrative costs and favoring solvent-free systems. Consolidation is accelerating: Sika purchased two regional producers in Poland and Spain during 2025, citing the regulatory hurdle as a catalyst.

Automotive Lightweight Structures Needing Fast-Cycle Bonding

Battery-electric vehicle output in Europe touched 2.8 million units in 2025, with OEMs targeting a 10% curb-weight reduction to push range beyond 500 km per charge. Polyurethane hot melts facilitate multi-material bonding, aluminum, steel, and CFRP (Carbon Fiber Reinforced Polymer), without introducing galvanic corrosion. Henkel’s Loctite PUR 8100, unveiled mid-2025, reaches 15 MPa lap-shear strength on aluminum in 90 seconds at 140°C, cutting body-shop takt time by half. Volkswagen’s 2025 annual report disclosed that adhesive bonding now makes up 18% of body-in-white assembly within its MEB (Modularer E-Antriebs-Baukasten) platform, up from 12% in 2023. Stellantis named SikaMelt PUR for battery-pack enclosure bonding, underscoring the chemistry’s importance for thermal management.

Edge-Banding Automation in Modular Furniture Lines

European furniture production rebounded 7% in 2025, buoyed by renovation activity and export demand out of Germany, France, and Poland. Zero-joint laser edge-banding lines require adhesives that cure in fewer than ten seconds and show heat resistance above 120°C. Jowatherm-Reaktant 506.90, commercialized late 2024, satisfies these parameters and secures invisible glue lines on high-gloss panels. Equipment maker IMA Schelling reported that 70% of its 2025 Western-European edge-bander installs feature PU-compatible heads, up from 50% in 2023. Henkel noted an 18% increase in edge-banding-adhesive revenue in 2025, with reactive grades outgrowing EVA (Ethylene Vinyl Acetate) products in premium kitchens.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Isocyanate feedstock price volatility | -0.70% | EU-wide, with acute impact on Western European formulators dependent on imported MDI/TDI | Medium term (2-4 years) |

| Mandatory di-isocyanate worker-training regulation (EU 2023/C) | -0.50% | EU-wide, disproportionately affecting SME formulators in Italy, Spain, and Eastern Europe | Short term (≤ 2 years) |

| High European energy prices raising melt-line OPEX | -0.60% | Western Europe (Germany, France, UK, Italy), particularly energy-intensive production sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Isocyanate Feedstock Price Volatility

European MDI spot prices averaged EUR 2,450 t in 2025, an 18% leap over January 2024, driven by Chinese production cuts and Europe’s elevated gas costs. BASF, Covestro, and Huntsman trimmed regional output by 12%, prioritizing higher-margin rigid foam customers and tightening adhesive supply. TDI prices fluctuated between EUR 2,100 and EUR 2,900 t during 2025, reflecting outages at BASF Ludwigshafen and Covestro Dormagen. Margin compression exceeded 300 basis points for spot-buying converters, pushing several Italian and Spanish shops to halt new-product development. Brussels opened an antitrust investigation into isocyanate producers in late 2025, injecting added uncertainty into expansion plans.

Mandatory Di-Isocyanate Worker-Training Regulation (EU 2023/C)

Effective August 2023, workers handling products with more than 0.1% free isocyanate must complete certified training and recertify every five years. A midsize formulator with 50 operators spends EUR 15,000-25,000 per year on fees, downtime, and audit documentation. Eight adhesive plants in Italy and Spain closed in 2025 as owners avoided the compliance burden. H.B. Fuller capitalized by acquiring a Spanish producer for EUR 28 million in March 2025, citing unmanageable training costs at the target firm. The rule also reaches downstream users, nudging cabinet makers and tier-1 automotive suppliers to prefer turnkey adhesive packages from multinational vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Reactive Chemistry Dominates, Non-Reactive Finds Niches

Reactive grades accounted for 86.20% of the Europe Polyurethane (PU) Hot-Melt Adhesives market size in 2025 and are projected to grow at 6.92% during the forecast period (2026-2031), propelled by urethane-urea crosslinking that yields heat- and moisture-resistant joints above 10 MPa. Automobile body-in-white bonding, battery-pack encapsulation, and medical wearables rely on this chemistry to resist sterilization at 134°C or endure 1,000 charge-discharge vibration cycles. Converters also prize the adhesives for their ability to bond to low-surface-energy substrates such as polyolefin elastomers after plasma activation. Germany’s stringent VOC limits provide a regulatory tailwind because reactive formulations are 100% solids and solvent-free.

Non-reactive polyurethane hot melts' utility persists in bookbinding, textile lamination, and temporary footwear lasting since they cool-set rapidly and can be heat-reactivated. Book manufacturers value the open time flexibility for multi-signature alignment, while flexible-packaging converters laud the sub-120°C application that cuts natural-gas usage. Footwear factories in Portugal have shifted to non-reactive grades for toe-lasting, where the bond must release cleanly post-thermoforming. Despite these strengths, the segment faces structural headwinds: EU circular-economy guidelines reward durable assemblies and recyclability, diminishing the appeal of easy-rework adhesives. Consequently, the Europe polyurethane (PU) hot-melt adhesives market will continue tilting toward reactive chemistries, but non-reactive systems will defend niches tied to short dwell times and low-heat substrates.

By Application: Furniture Leads, Healthcare Surges

Furniture retained 23.89% of 2025 revenue, anchoring the Europe Polyurethane (PU) Hot-Melt Adhesives market through continued investment in zero-joint edge-banding and automated case-good assembly. Kitchen-cabinet fabricators require bonds that set in under ten seconds so that line speeds can exceed 25 m min, while office-furniture makers demand heat-resistant joints that survive week-long container transport in summer. German firms SieMatic and Nolte have standardized on moisture-curing PUR grades across all gloss levels, citing tight seam aesthetics and post-form moisture stability. Poland exported EUR 18 billion of furniture in 2025, up 9% versus 2024, and is retrofitting plants near Poznań with laser edge-banders compatible only with PUR adhesives.

Healthcare is the fastest-growing application, forecast to deliver a 7.26% CAGR during the forecast period (2026-2031) and expand its slice of the market. Wearable sensors for real-time cardiac and glucose monitoring require skin-safe adhesives that maintain adhesion for 72 h yet peel without erythema. Transdermal drug patches are migrating from acrylic to PUR matrices to achieve controlled release while resisting sweat. EU medical-device regulations that entered full force in 2025 demand traceability of all constituent chemicals, and global suppliers have invested in digital product passports to document ISO 10993 and cytotoxicity data, a hurdle that regional formulators struggle to clear. As a result, large multinational suppliers are capturing the bulk of incremental healthcare demand, deepening competitive moats through regulatory compliance.

Geography Analysis

Germany represented 28.21% of 2025 regional revenue, affirming its position as the anchor of the Europe Polyurethane (PU) Hot-Melt Adhesives market. Vehicle assembly volume of 4.1 million units, the continent’s largest, underwrites demand for structural bonding in EV battery packs and multimaterial bodies. Edge-banding demand mirrors furniture output valued at EUR 18 billion, with premium kitchens favoring reactive systems for seamless aesthetics. German environmental policy acts as a growth catalyst: TA Luft’s 20 g kg VOC ceiling eliminates solvent alternatives sooner than other EU states, locking in polyurethane adoption.

French production is concentrated near Lyon, where Arkema’s Bostik division added 15% capacity in 2025 for packaging adhesives. Italy’s Lombardy and Veneto clusters rely on PUR grades for both furniture and designer footwear, while Spain leverages Seat’s Barcelona plant and Ford’s Valencia facility to drive automotive use. The United Kingdom (UK) market rebounded from Brexit-related import friction; Henkel and H.B. Fuller maintained local compounding to serve just-in-time lines in Midlands auto plants. Across these countries, national implementations of EU VOC legislation are converging, smoothing technical specification and encouraging cross-border sourcing deals.

Central and Northern Europe, including Poland, Czech Republic, Netherlands, Belgium, and the Nordics hold headroom as manufacturers migrate from EVA to PUR for climate resilience and automation compatibility. Poland alone consumed EUR 45 million worth of polyurethane hot melts in 2025, fed by robust furniture exports to Germany and France. Jowat’s 2025 plant opening near Wrocław shortened lead times and offered technical service in Polish, accelerating adoption. Nordic packaging lines transitioned to PUR case-sealing to withstand cold-chain logistics, while the Netherlands emphasized circular-economy adhesives that debond on demand for plastic crate reuse. Russia, with 6-8% share, remains supply constrained under sanctions, importing Chinese isocyanates and developing local capacity that lags Western product performance.

Competitive Landscape

The Europe Polyurethane (PU) Hot-Melt Adhesives market is highly consolidated. Smaller innovators retain relevance through specialization. Artimelt and Klebchemie focus on ultra-low-temperature reactive systems (less than 100°C) for polyethylene foams and TPU films, circumventing energy costs and substrate warping. Energy remains a watchpoint: natural-gas prices averaged EUR 45 MWh in 2025, prompting waste-heat recovery installations and resin reformulation to lower melt viscosity by 10-15%, trimming kiln-electricity demand.

Europe Polyurethane (PU) Hot-Melt Adhesives Industry Leaders

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

Arkema

Jowat SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lubrizol announced that Bjørn Thorsen A/S expanded its distributorship for Lubrizol’s industrial thermoplastic polyurethane (TPU) resins in Germany and Hungary. This agreement can boost the market of Europe polyurethane (PU) hot-melt adhesives in the coming years.

- November 2025: Henkel Adhesive Technologies and Dow announced plans to deepen their collaboration to focus on reducing SBTi-relevant emissions by integrating low-CO₂ raw materials and renewable electricity in the production of hot melt adhesives, catering primarily to the packaging and consumer goods sectors.

Europe Polyurethane (PU) Hot-Melt Adhesives Market Report Scope

Polyurethane (PUR) hot-melt adhesives, known for their 100% solid and reactive nature, are moisture-curing agents. They achieve high-strength, flexible bonding through a two-step process: an initial physical cooling followed by a chemical reaction. These adhesives remain solid at room temperature, melt when applied, and cure by interacting with atmospheric moisture.

The Europe Polyurethane (PU) Hot-Melt Adhesives market is segmented by type, application, and geography. By type, the market is segmented into reactive and non-reactive. By application, the market is segmented into packaging, healthcare, automotive, furniture, footwear, textile, electronics, bookbinding, and others. The report also covers the market size and forecasts for carbon composites in 6 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Type

| Non-reactive |

| Reactive |

By Application

| Packaging |

| Healthcare |

| Automotive |

| Furniture |

| Footwear |

| Textile |

| Electronics |

| Bookbinding |

| Others |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Type | Non-reactive |

| Reactive | |

| By Application | Packaging |

| Healthcare | |

| Automotive | |

| Furniture | |

| Footwear | |

| Textile | |

| Electronics | |

| Bookbinding | |

| Others | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe polyurethane (PU) hot-melt adhesives market?

The market stood at USD 688.18 million in 2026 and is forecast to reach USD 953.99 million by 2031.

Which chemistry dominates sales in Europe?

Reactive polyurethane hot melts command 86.20% of 2025 revenue and are expanding at a 6.92% CAGR during the forecast period (2026-2031) on the back of superior moisture-curing performance.

Why are polyurethane hot melts gaining share in e-commerce packaging?

Parcel growth and new EU recycled-content rules favor fast-setting, high-strength bonds that reactive PUR grades deliver on recycled corrugated board.

Which application is growing fastest?

Healthcare adhesives are advancing at a 7.26% CAGR during the forecast period (2026-2031) as skin-safe reactive grades enable multi-day wearables and transdermal patches.

How will EU di-isocyanate training rules influence the supplier base?

Compliance costs are accelerating consolidation because small formulators struggle with the required certification expense, enabling multinationals to buy distressed assets.

Page last updated on: