Polyester Hot Melt Adhesives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

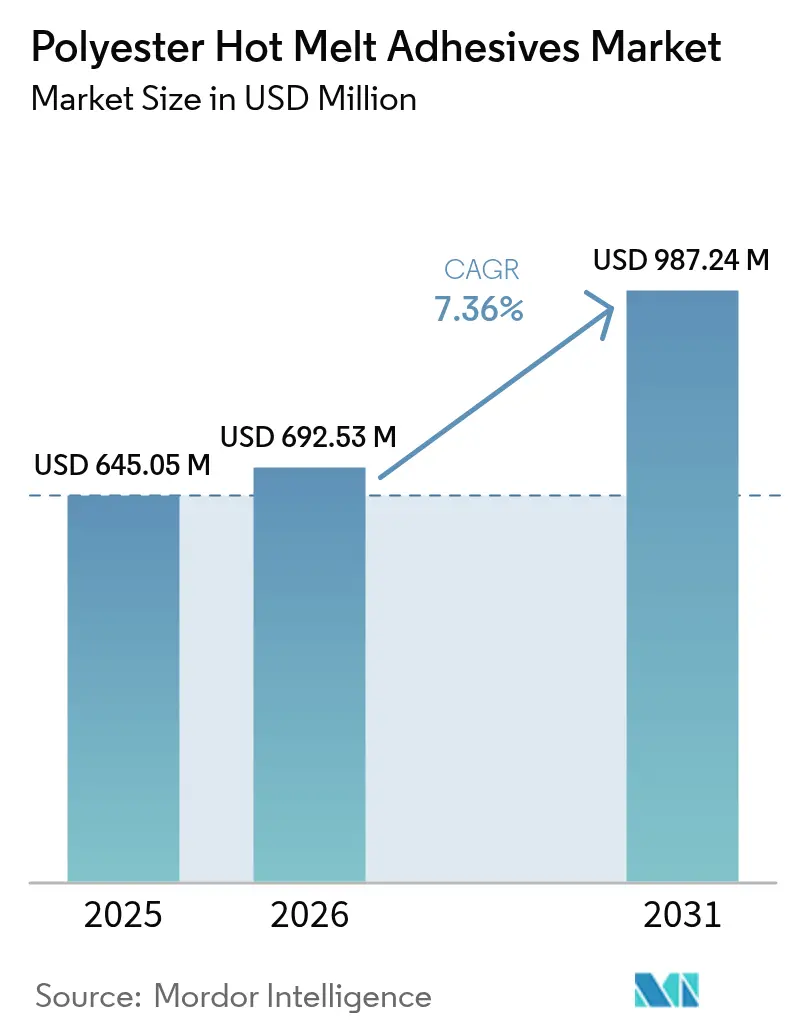

| Market Size (2026) | USD 692.53 Million |

| Market Size (2031) | USD 987.24 Million |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyester Hot Melt Adhesives Market Analysis by Mordor Intelligence

The Polyester Hot Melt Adhesives Market size is expected to grow from USD 645.05 million in 2025 to USD 692.53 million in 2026 and is forecast to reach USD 987.24 million by 2031 at 7.36% CAGR over 2026-2031. Growth reflects the global transition from solvent-based systems to thermoplastic solutions that avoid volatile organic compounds, comply with tightening regulations, and deliver high bonding strength across automotive, electronics, packaging, textile, and medical uses. Regulatory pressure—most notably the European Union’s restriction on diisocyanates—continues to accelerate uptake of polyester formulations that combine structural performance with low emissions. Demand is further underpinned by lightweight vehicle programs, miniaturised consumer electronics, and rapid advances in smart-textile and medical disposables that all require adhesives capable of bonding dissimilar substrates, surviving thermal cycling, and meeting biocompatibility rules. Feedstock volatility and emerging bio-based alternatives add cost and competitive complexity, yet sustained capacity investments by leading suppliers in Asia Pacific secure raw material access, shorten delivery times, and foster application-specific innovation. Together, these forces keep the polyester hot melt adhesives market on a long-term, mid-single-digit growth trajectory despite cyclical raw-material cost swings.

Key Report Takeaways

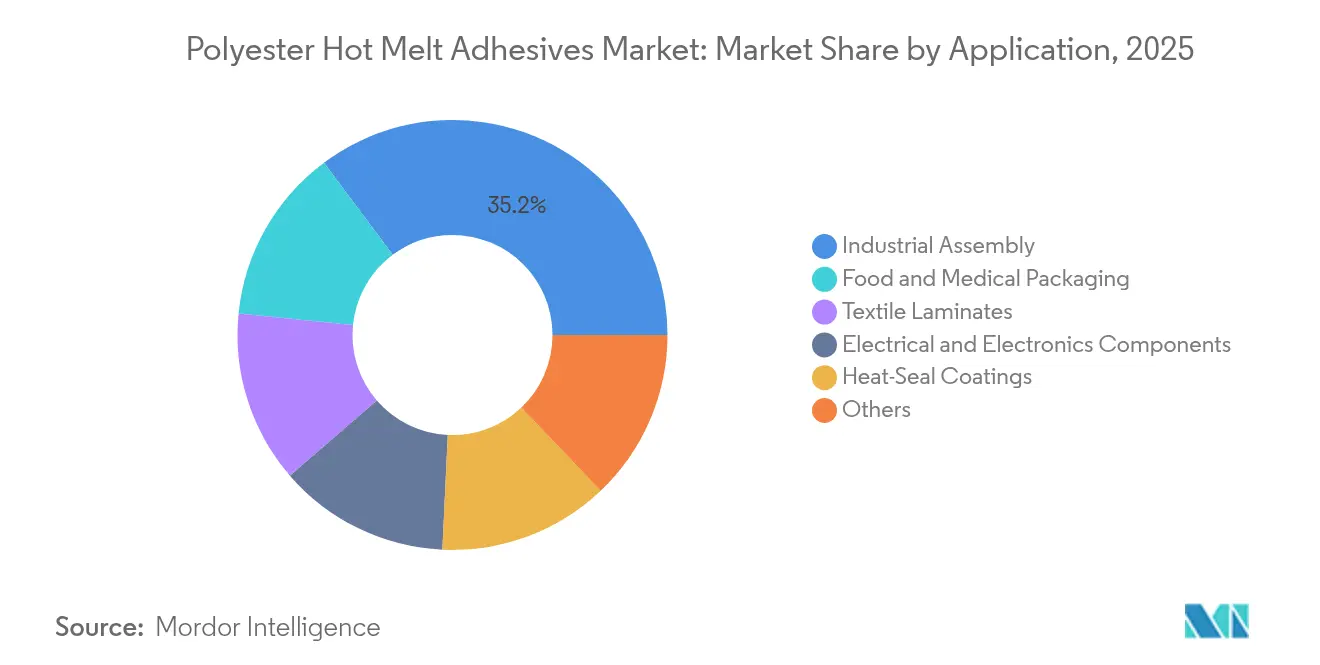

- By application, Industrial assembly led with 35.20% of the polyester hot melt adhesives market share in 2025; food and medical packaging is projected to expand at an 8.24% CAGR to 2031.

- By resin chemistry, Aromatic polyester captured 46.00% share of the polyester hot melt adhesives market size in 2025; bio-based polyester is forecast to grow at an 8.22% CAGR between 2026-2031.

- By form, Pellets and granules accounted for 48.10% share of the polyester hot melt adhesives market size in 2025, while powder and microspheres record the fastest projected CAGR at 8.18% through 2031.

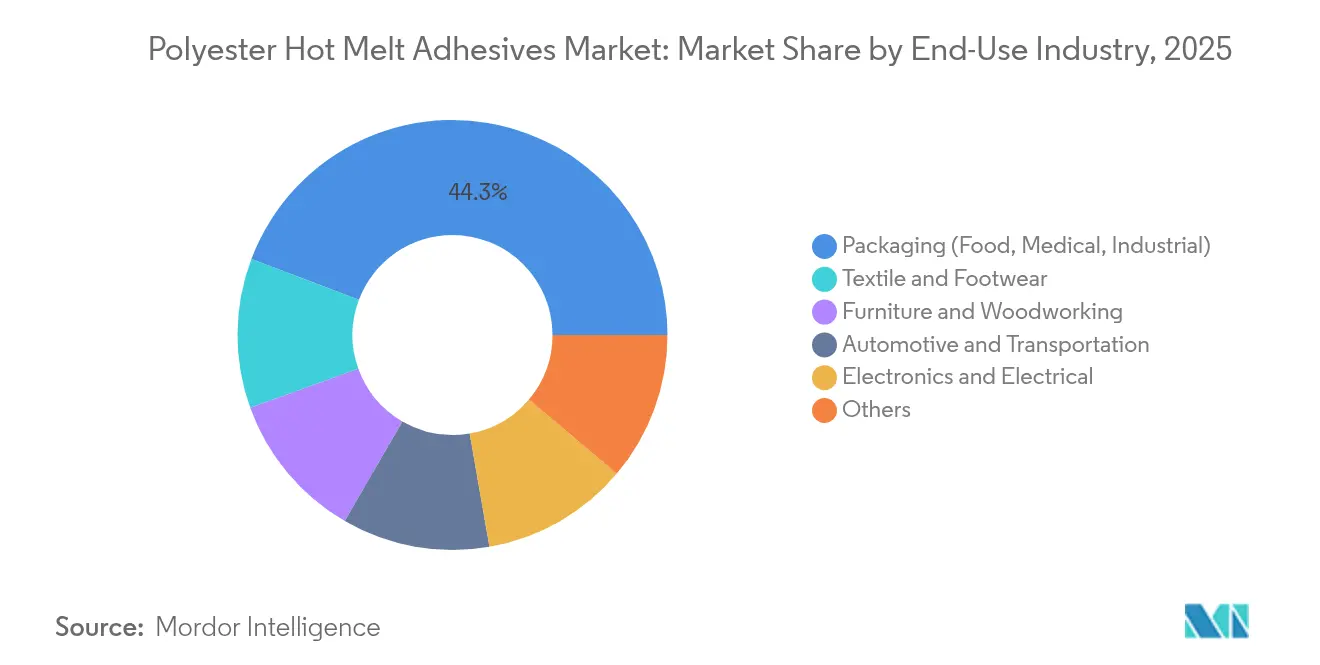

- By end-use industry, Packaging commanded 44.25% share of the polyester hot melt adhesives market size in 2025; textile and footwear is the fastest-growing end-use, rising at an 8.01% CAGR to 2031.

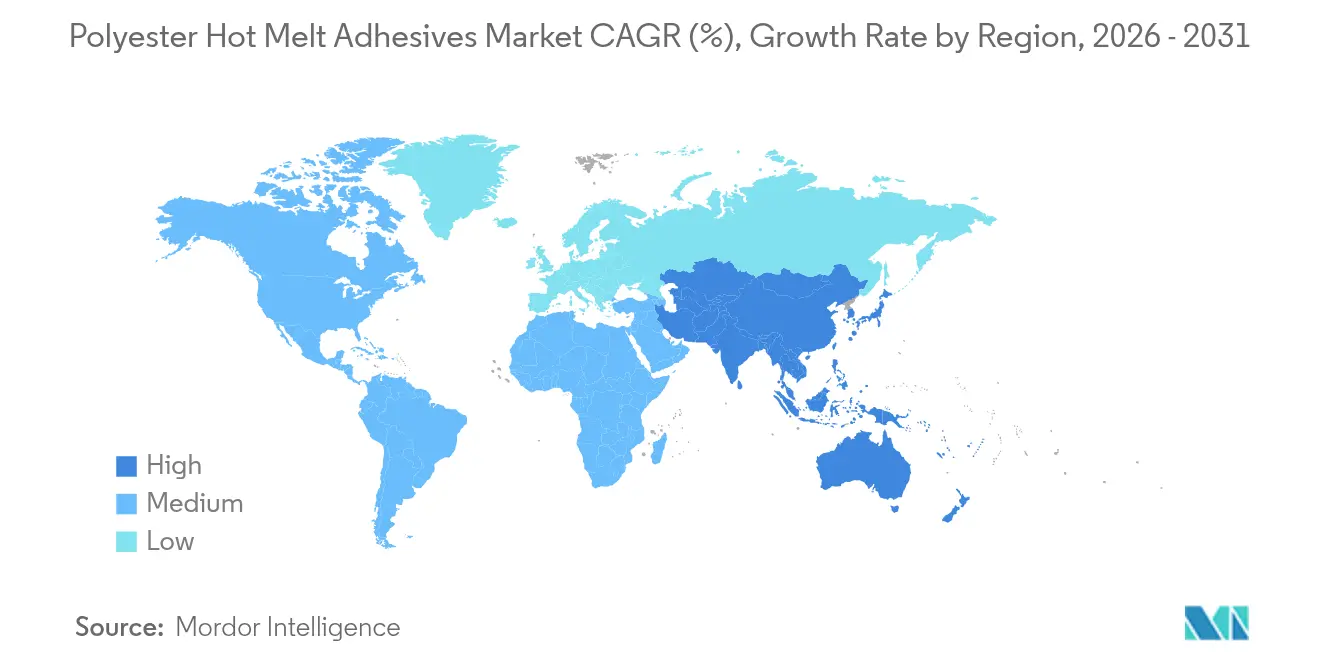

- By geography, Asia Pacific held 39.60% revenue share of the polyester hot melt adhesives market in 2025 and is advancing at an 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Polyester Hot Melt Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for solvent-free packaging adhesives | +1.80% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Lightweight automotive bonding requirements | +2.10% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Growth in miniaturised electronic components | +1.50% | APAC dominance, expanding to global markets | Short term (≤ 2 years) |

| Wearable smart-textile bonding emergence | +1.20% | North America & EU early adoption, APAC manufacturing | Medium term (2-4 years) |

| Medical-grade low-temperature film adhesives | +0.90% | Global, with regulatory leadership in EU & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Solvent-Free Packaging Adhesives

Packaging producers are eliminating solvent emissions and cutting energy use by shifting from solvent-borne laminating products to 100% solids polyester hot melts. Henkel, Dow, and Kraton recently cut the carbon footprint of the TECHNOMELT range by 25% by introducing bio-based tackifiers without sacrificing food-contact safety[1]Henkel AG & Co. KGaA, “TECHNOMELT® EcoDesign in Packaging,” henkel.com . Tightening EU VOC limits further accelerates this switch, while converters benefit from quicker line speeds and the elimination of costly solvent-recovery equipment. Polyester formulations also improve adhesion to metallised films and enhance moisture resistance, making them attractive for premium barrier packaging.

Lightweight Automotive Bonding Requirements

Vehicle makers pursuing weight reduction and electrification rely on polyester hot melts to join aluminium, carbon fibre, and advanced steels that cannot be riveted or welded cost-effectively. These thermoplastic adhesives withstand wide temperature swings, damp vibration, and allow easier component disassembly for end-of-life recycling. Increasing power-electronics density in electric vehicles heightens under-hood thermal stress; polyester chemistries tailored for 150 °C service safely insulate battery modules while maintaining mechanical integrity.

Growth in Miniaturised Electronic Components

High-density circuit boards and flip-chip packaging demand adhesives that survive multiple reflow cycles yet provide electrical insulation. Polyester hot melts deliver precise dot placement, rapid green strength, and reworkability superior to traditional epoxies. Wearable and IoT devices need flexible bonding of films, antennas, and sensors; modified polyester grades accommodate repeated bending and low-temperature assembly, supporting high-volume Asian electronics production.

Wearable Smart-Textile Bonding Emergence

Integrating conductive yarns and flexible sensors into fabrics calls for adhesives compatible with ultrasonic welding and low-bulk lamination. Polyester hot melts bond electronics into garments while retaining drape and wash durability[2]Chung Seung & Kim Jae-Ho, “Thermoplastic Adhesives for Smart-Textile Applications,” mdpi.com . Footwear brands deploy them to embed force and temperature sensors in performance shoes, opening a fast-rising niche that rewards suppliers offering soft-handle, durable adhesive films.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availiablity Of subsitutes | -1.40% | Global, with higher impact in price-sensitive markets | Short term (≤ 2 years) |

| Volatile petrochemical diacid & glycol prices | -2.20% | Global, with acute impact in Asia Pacific manufacturing | Medium term (2-4 years) |

| High Raw Material & Production Costs | -1.80% | Global, with concentration in high-cost manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Substitutes

Lignin-based hot melts, reactive polyurethane systems, and advanced cyanoacrylates match or exceed polyester performance in certain uses and attract buyers seeking lower cost or higher green content[3]Laine Jani et al., “Lignin-Based Hot Melt Adhesives for Paperboard,” ACS Sustainable Chemistry & Engineering, pubs.acs.org . As these alternatives scale, they cap pricing power for polyester suppliers and can divert new projects when technical differences are minimal.

Volatile Petrochemical Diacid & Glycol Prices

Terephthalic acid and ethylene glycol price swings create margin pressure and budgeting uncertainty. Energy-market shocks, geopolitical events, or unplanned shutdowns ripple quickly through polyester value chains. Producers hedge with forward contracts, inventory buffers, and bio-feedstock experiments, yet sustained volatility remains a structural headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Industrial Assembly Drives Market Leadership

Industrial assembly remains the largest slice of the polyester hot melt adhesives market, holding 35.20% share in 2025 and topping the USD polyester hot melt adhesives market size rankings. Automotive bonding dominates this segment, where the adhesive’s ability to unite multi-material structures and survive life-cycle temperature extremes is critical. Vehicle electrification raises peak under-hood temperatures, further reinforcing the need for thermally resilient polyester hot melts. Other industrial uses include appliance, furniture, and filter assembly, each benefiting from fast set times and clean processing.

Food and medical packaging is the fastest-growing application, advancing at an 8.24% CAGR through 2031. Brand owners favour solvent-free, low-odour adhesives that meet stringent migration limits while reducing line energy demand. Peelable heat-seal coatings for retort pouches and lidding films illustrate the crossover between industrial assembly and packaging functions. Electronics packaging and heat-seal coatings add diversity, while textile laminates offer an emerging arena where flexible adhesion, breathability, and wash resistance converge.

By Resin Chemistry: Aromatic Polyester Dominance Faces Bio-Based Challenge

Aromatic polyester commands 46.00% of 2025 revenues, prized for high glass-transition temperature, cohesive strength, and resistance to automotive and electronic operating conditions. The polyester hot melt adhesives market share advantage stems from decades of optimisation, ready availability of raw materials, and broad formulation know-how.

Bio-based and partially bio-based polyester, however, is the fastest-growing chemistry at 8.22% CAGR. Suppliers leverage plant-derived diacids, recycled PET, and CO₂-based intermediates to cut carbon footprint without losing mechanical performance. Customers in consumer goods and medical devices value the sustainability story, and legislative pressure on petrochemical dependence will narrow legacy cost advantages. Aliphatic polyester serves niche biodegradable or compostable end-uses, while copolyester chemistries fine-tune crystallinity and melt viscosity for tailored substrate wet-out or reworkability. Continuous R&D keeps the polyester hot melt adhesives market dynamic as performance and sustainability benchmarks rise in tandem.

By Form: Pellets Maintain Processing Advantages

Pellets and granules deliver 48.10% of 2025 sales, driven by automated feeders that ensure consistent melt flow in high-speed packaging and automotive lines. Bulk pellet logistics cut handling loss and facilitate precise dosing, safeguarding quality in lean manufacturing environments.

Powder and microspheres post the highest growth at 8.18% CAGR. Electronics miniaturisation demands exact adhesive placement at the micron scale, prompting the adoption of screen-printable polyester powders and laser-activatable microbeads. Films and webs serve roll-to-roll textile lamination and large-area composite fabrication, while blocks, slabs, and sticks remain relevant for maintenance, repair, and craft applications where manual application still predominates. The diversified product mix lets converters choose the optimal delivery vehicle for their specific process constraints.

By End-Use Industry: Packaging Leadership Faces Textile Disruption

Packaging remains the largest end use with 44.25% revenue in 2025, reflecting global food, beverage, and medical handling needs. Solvent-free polyester hot melts deliver hermetic seals for barrier films, suit cold-chain logistics, and support high-speed case and carton sealing. The shift to monomaterial flexible structures for easier recycling accentuates polyester’s role because its polarity matches many polyolefin and PET substrates.

Textile and footwear, at an 8.01% CAGR, is the fastest-growing segment as apparel brands integrate sensors, LEDs, and heating elements into garments. Polyester hot melts bond electronics into fabric with soft handfeel and wash durability, giving the sector a new functional dimension. Automotive, electronics, furniture, woodworking, and construction collectively diversify demand and buffer macro-sector volatility, ensuring volume stability for suppliers.

Geography Analysis

Asia Pacific held 39.60% of global sales in 2025 and is on track for an 8.12% CAGR to 2031. China’s electric-vehicle buildout, India’s smartphone assembly hubs, and Japan’s high-precision electronics plants all consume large volumes of polyester hot melts. Regional authorities promote investment in advanced materials, encouraging Henkel and Sika to add local capacity, which shortens delivery cycles and integrates technical support into customers’ product-development workflows. Consolidated net sales at Pidilite Industries reached INR 12,337 crore (USD 1.48 billion) in 2025, underscoring the region’s maturing demand base.

North America remains an innovation powerhouse, driving stringent automotive lightweighting targets and pioneering bio-based chemistries. EU regulations steer materials away from diisocyanates and high-VOCs, making polyester hot melts a go-to solution. Both regions collaborate with academia and start-ups to scale CO₂-derived monomers, showcasing leadership in circular-economy adhesives.

South America, the Middle East, and Africa register smaller volumes but represent untapped potential. Infrastructure expansion and growing packaged-food sectors support wider adoption. As regional converters modernise equipment and embrace solvent-free lines, polyester hot melt suppliers win green-field projects that lock in multi-year contract volumes and strengthen global network resilience.

Competitive Landscape

The polyester hot melt adhesives market is moderately fragmented. Henkel, H.B. Fuller, 3M, Bostik-Arkema, and Dow (through specialty joint ventures and technology partnerships) head the global roster. Their competitive edge rests on wide product portfolios, backward integration into polymer synthesis, and technical-service teams that embed with OEMs during design-in cycles.

Recent portfolio realignment illustrates strategic focus: Dow divested its flexible-laminating adhesives assets to Arkema for USD 150 million in December 2024, sharpening its emphasis on higher-margin specialty segments while bolstering Arkema’s reach in sustainable hot melts. Henkel partnered with Celanese to pioneer CO₂-based polyester, signalling that decarbonisation can coexist with performance leadership. Bostik earmarked USD 27 million for 2025 to expand high-molecular-weight polyester at its Massachusetts plant, reinforcing its heat-activated adhesive franchise for footwear and automotive interiors.

Regional specialists thrive by tailoring grades to local substrates and regulatory nuances. Price competition is limited because automotive, medical, and electronics qualification cycles can exceed 18 months, rewarding incumbents with proven track records. R&D centres increasingly concentrate on bio-feedstock substitution, reactive extrusion for faster melt-index control, and AI-driven formulation screening, indicating that intellectual property and application engineering—not scale alone—determine long-run market share shifts.

Polyester Hot Melt Adhesives Industry Leaders

3M

Arkema (Bostik)

Dow

H.B. Fuller Company

Henkel AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bostik, part of Arkema, is investing USD 27 million to expand high molecular weight polyester production at its Middleton, Massachusetts, plant, a key facility for its heat-activated specialty hot melt technology platform.

- April 2024: Henkel Adhesive Technologies, Kraton Corporation, and Dow Inc. have effectively reduced the carbon footprint of two flagship end-of-line packaging products from Henkel in North America: TECHNOMELT SUPRA 100 and TECHNOMELT SUPRA 106M. These efforts are expected to foster further innovations in polyester hot melt adhesives production.

Global Polyester Hot Melt Adhesives Market Report Scope

The Polyester Hot Melt Adhesives Market report include:

| Industrial Assembly | Automotive |

| Others | |

| Food and Medical Packaging | |

| Electrical and Electronics Components | |

| Heat-Seal Coatings | |

| Textile Laminates | |

| Others |

| Aromatic Polyester |

| Aliphatic Polyester |

| Copolyester |

| Bio-based/Partially Bio-based Polyester |

| Pellets/Granules |

| Blocks/Slabs |

| Sticks |

| Film/Web |

| Powder/Microspheres |

| Packaging (Food, Medical, Industrial) |

| Automotive and Transportation |

| Electronics and Electrical |

| Textile and Footwear |

| Furniture and Woodworking |

| Others |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Industrial Assembly | Automotive |

| Others | ||

| Food and Medical Packaging | ||

| Electrical and Electronics Components | ||

| Heat-Seal Coatings | ||

| Textile Laminates | ||

| Others | ||

| By Resin Chemistry | Aromatic Polyester | |

| Aliphatic Polyester | ||

| Copolyester | ||

| Bio-based/Partially Bio-based Polyester | ||

| By Form | Pellets/Granules | |

| Blocks/Slabs | ||

| Sticks | ||

| Film/Web | ||

| Powder/Microspheres | ||

| By End-use Industry | Packaging (Food, Medical, Industrial) | |

| Automotive and Transportation | ||

| Electronics and Electrical | ||

| Textile and Footwear | ||

| Furniture and Woodworking | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the polyester hot melt adhesives market?

The market stands at USD 692.53 million in 2026 and is forecast to hit USD 987.24 million by 2031.

Which application dominates demand for polyester hot melt adhesives?

Industrial assembly, led by automotive bonding, holds 35.20% of revenue in 2025.

Why are polyester hot melts preferred over solvent-based laminating adhesives in packaging?

They eliminate VOC emissions, cut line energy use, and meet stricter food-contact regulations while delivering strong heat-seal performance.

Which region shows the fastest growth?

Asia Pacific leads with an 8.12% CAGR thanks to electric-vehicle production, electronics assembly, and ongoing capacity investments.

How are suppliers addressing feedstock price volatility?

Strategies include forward-buy contracts, regional sourcing diversification, and development of bio-based or CO₂-derived monomers that lower dependence on petrochemical inputs.

Page last updated on: