Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.79 Billion |

| Market Size (2026) | USD 0.82 Billion |

| Market Size (2031) | USD 1.02 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Architectural Coatings Market Analysis by Mordor Intelligence

The Poland Architectural Coatings Market size was valued at USD 0.79 billion in 2025 and is estimated to grow from USD 0.82 billion in 2026 to reach USD 1.02 billion by 2031, at a CAGR of 4.45% during the forecast period (2026-2031). A tightening of EU VOC regulations, the resurgence of residential renovation following monetary easing, and sustained interest in modular timber construction are combining to lift volumes, especially for premium, water-borne acrylic systems. Raw-material cost volatility and a widening labor shortage are tempering the outlook, yet manufacturers continue to invest in low-carbon production and multifunctional product lines to defend margins. E-commerce paint platforms, together with color-visualization apps, are reshaping DIY buying behavior, while digital-first private-label brands are squeezing middle-tier producers on price. Competitive pressure remains moderate because the top five suppliers still control roughly three-fifths of demand, but regional specialists are using online channels to chip away at share, particularly in price-sensitive suburban markets.

Key Report Takeaways

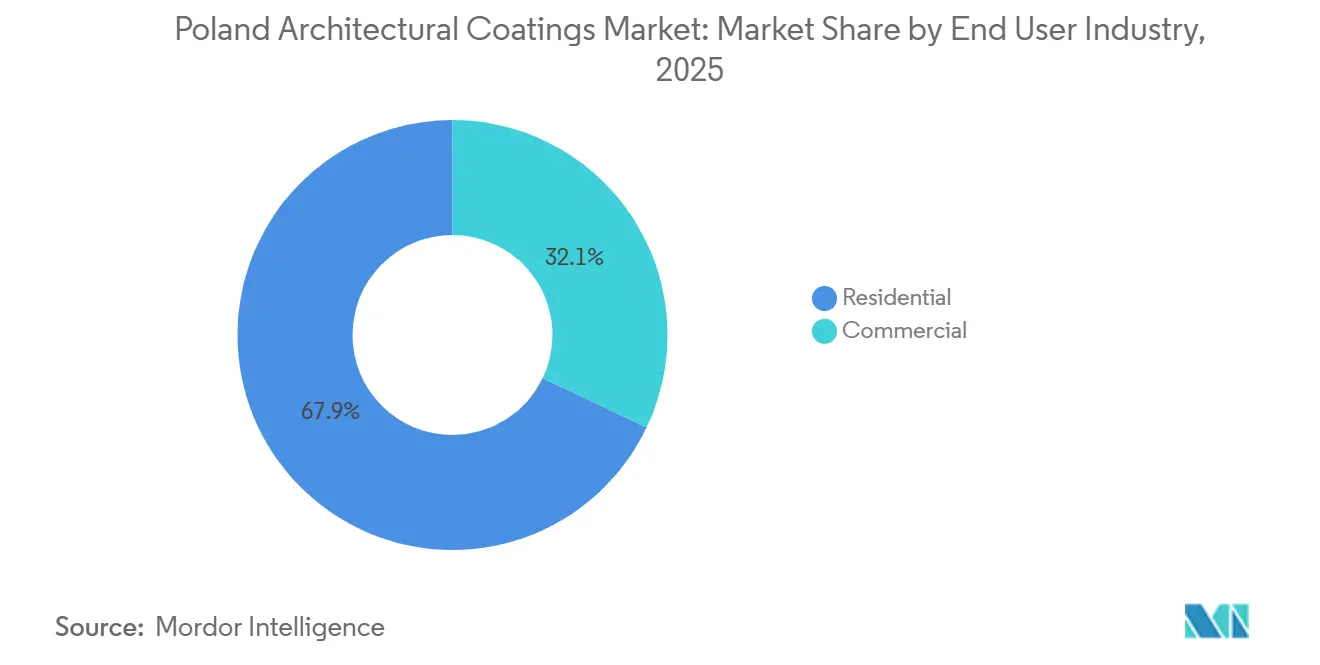

- The residential end-user segment captured 67.92% of demand in 2025 and is forecast to grow at 4.73% annually, outpacing commercial construction despite a slowdown in new building permits.

- Water-borne technology held 81.11% of the Poland architectural coatings market share in 2025 and is advancing at a 4.96% CAGR through 2031, maintaining its position as both the largest and fastest-growing technology segment.

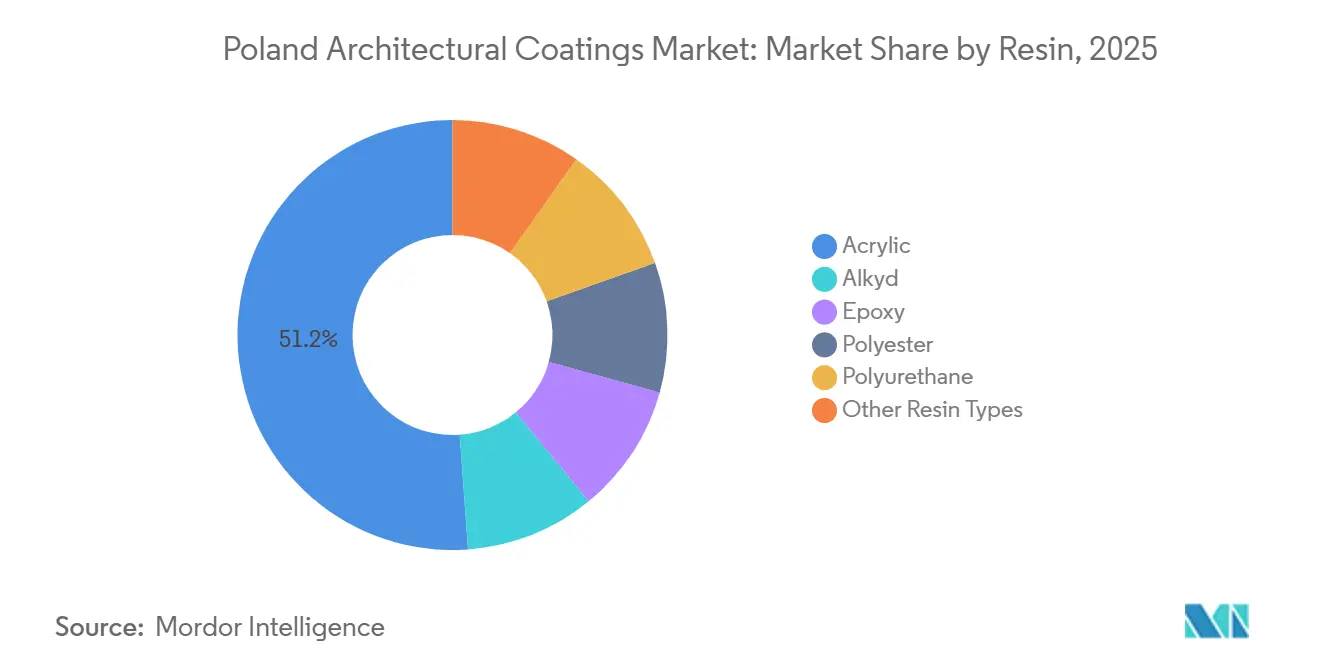

- Acrylic resins accounted for 51.16% of the Poland architectural coatings market size for resins in 2025 and are on track to expand at a 4.88% CAGR, reinforced by their compatibility with water-borne systems and rising timber-frame housing adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU VOC limits accelerating water-borne transition | +1.2% | Poland (national compliance with EU Ecolabel 2026 criteria) | Medium term (2-4 years) |

| Residential renovation boom after mortgage-rate relief | +1.5% | National, concentrated in Mazowieckie, Wielkopolskie, Małopolskie | Short term (≤ 2 years) |

| Growing DIY e-commerce platforms for paint personalization | +0.6% | National, urban centers with high internet penetration | Medium term (2-4 years) |

| Modular timber construction lifting demand for low-VOC exterior paints | +0.8% | National, early adoption in single-family suburban developments | Long term (≥ 4 years) |

| 3-in-1 self-cleaning and anti-microbial interior coatings gaining traction | +0.5% | National, residential and healthcare segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU VOC Limits Accelerating Water-Borne Transition

The EU’s 2026 Ecolabel revision cut VOC ceilings to 15 g/L for interior matt walls and 30 g/L for exterior paints, forcing Polish producers to reformulate or lose access to public procurement and eco-retail channels[1]European Coatings, “Water-Borne Paints Outpace Solvent Products in CEE,” european-coatings.com. Water-borne systems already held 81.11% share in 2025 and are projected to climb to 83.9% by 2031, spurred by investments in acrylic copolymers that match alkyd opacity while keeping VOCs below 20 g/L. AkzoNobel’s 2025 roll-out of a radiative-cooling water-borne topcoat illustrates how research and development budgets are shifting toward compliant, energy-saving chemistries[2]European Business, “AkzoNobel Unveils Radiative-Cooling Coating,” european-business.com. The pace of adoption will follow cost parity with solvent lines and alignment with Poland’s tightening NZEB rules.

Residential Renovation Boom After Mortgage-Rate Relief

Narodowy Bank Polski cut policy rates by 175 basis points in 2025, plus 25 basis points in March 2026, to 3.75%, unlocking mortgage demand. Dwelling completions reached 208,400 units in 2025, an 8,300 units jump year-over-year, while the share of energy-efficient retrofits climbed alongside central-heating and sewer-network extensions. Renovations center on Mazowieckie, Wielkopolskie, and Małopolskie, where aging prefabricated blocks require façade and interior refreshes. Although dwelling starts fell 9.2% in 2025, the renovation backlog should support coatings demand into 2028 unless fiscal incentives are withdrawn.

Growing DIY E-Commerce Platforms for Paint Personalization

Digital paint-mixing services from E-kolor, Kolorowy-Dom, Kolor Zone, and Colorownia raised e-commerce penetration in Poland’s home-improvement sector to roughly 18–20% of sales in 2025. Same-day urban delivery and augmented-reality color apps are prompting consumers to order smaller (1–2.5 L) water-borne packs online, benefitting agile local brands integrated with these platforms. Incumbents now release annual color trends directly within mobile apps. For instance, AkzoNobel’s “Kolory Roku 2026” palette is a flagship example, which enables it to retain mindshare among digitally native DIY buyers.

Modular Timber Construction Lifting Demand for Low-VOC Exterior Paints

Prefab timber-frame builds accounted for 8–10% of single-family starts in 2025, up from 5–6% two years earlier. Timber needs breathable, flexible coatings; hence, water-borne acrylic-silicone hybrids with VOCs below 30g/L are winning specifications. Jotun’s Northern European supply position allows quick service for Polish modular builders seeking solar-reflective, high-SRI finishes. Higher per-liter pricing partially offsets TiO₂ cost inflation.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile titanium-dioxide and resin input costs | -0.9% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Construction-permit slowdown amid high financing costs | -0.7% | National, concentrated in secondary cities (Katowice, Łódź) | Medium term (2-4 years) |

| Acute shortage of skilled painting contractors | -0.5% | National, most severe in Mazowieckie and Dolnośląskie | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Titanium-Dioxide and Resin Costs

TiO₂ pigment remained 18–22% above pre-pandemic levels by August 2025, squeezing margins among producers lacking hedged contracts. Śnieżka’s 1.4% revenue dip to EUR 175.5 million (USD 190.8 million) in 2025 reflected an inability to pass costs through price-sensitive DIY channels. Exterior paints burdened with 18–25% TiO₂ by weight are most exposed, forcing exploration of calcium-carbonate blends that undermine opacity and durability.

Construction-Permit Slowdown Amid High Financing Costs

Permit issuance tumbled as developers digested a 14,000-unit overhang of unsold flats in Poland’s seven biggest metros; starts fell 9.2% year-on-year in 2025. Confirmed residential projects for 2026 total just PLN 31 billion (USD 7.8 billion) versus PLN 77 billion in 2025, chilling coatings demand for new builds. Katowice and Łódź face multi-year absorption horizons, dampening regional orders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Residential Dominates, Commercial Slows

The Poland architectural coatings market size for residential uses contributed 67.92% of the total consumption in 2025 and is growing at a 4.73% CAGR through 2031. Owner-occupier culture, a homeownership rate near 84%, and 208,400 completions sustain sales of freeze-thaw-resistant exterior finishes. Renovation is heaviest in pre-1980 blocks across Mazowieckie, Wielkopolskie, and Małopolskie, where façade remediation supports premium, mold-resistant interiors.

Commercial demand faces a softer growth as office and retail permits stagnate. Healthcare builds over PLN 1 billion in Q1 2025 spur niche uptake of ISO 22196-compliant antimicrobials, while warehouse projects continue to specify two-component epoxy floors.

By Technology: Water-Borne Extends Lead

Water-borne products held 81.11% Poland architectural coatings market share in 2025 and is anticipated to grow with 4.96% CAGR through 2031 as sub-20 g/L VOC limits bite. Advanced acrylic dispersions now match alkyd scrub resistance, easing trade-offs for DIY buyers. Solvent-borne coatings retreat to metal primers and high-gloss accents, especially as Castorama and Leroy Merlin reallocate shelf space to low-odor lines. Compliance costs under the Industrial Emissions Directive further discourage solvent production.

By Resin: Acrylic Ascendant

Acrylics represented 51.16% of Poland architectural coatings market share for resins in 2025 and will climb on a 4.88% CAGR through 2031 as timber-frame builds spread. Alkyds lose ground due to 200–400 g/L VOC content, despite flow advantages. Epoxies stay niche in chemical-resistant floors; polyurethanes grow in premium exteriors; vinyl-acetate and silicone-modified blends find spots in self-cleaning and elastomeric façades.

Geography Analysis

Mazowieckie, Wielkopolskie, and Małopolskie together contributed a significant share of Poland architectural coatings market demand in 2025. Warsaw’s PLN 8–10 billion 2026 pipeline underwrites steady sales of both interior emulsions and high-reflectance façades. Wielkopolskie’s diversified economy supports balanced housing and logistics builds, while Małopolskie leverages tourism-driven renovations.

Śląskie and Łódzkie confront over-inventory and minimal new starts, suppressing regional volumes. Tricity ports in Pomorskie anchor industrial and logistics spending, sustaining orders for floor epoxies and protective walls. The smallest provinces, including Opolskie and Świętokrzyskie, rely on budget DIY products sold via regional hardware chains.

AkzoNobel’s 1.9 MWp solar array at Pilawa in Mazowieckie now covers 25% of site power and hedges energy-price swings. MIPA’s HAERING Polska acquisition near Bydgoszcz adds northern capacity for industrial and architectural lines, signaling long-term confidence despite permit headwinds.

Competitive Landscape

The Poland architectural coatings market is partially consolidated. White-space growth favors timber-compatible low-VOC exteriors, self-leveling one-coat interiors, and digital-only private labels. Flügger’s mold-resistant emulsion and new Warsaw and Kraków stores exemplify agile niche attacks. AkzoNobel now offers Bureau Veritas-verified product carbon footprints, supporting low-carbon bids, while PPG deploys automated tinting to shorten contractor wait times.

Poland Architectural Coatings Industry Leaders

AkzoNobel N.V.

DAW SE

Flügger group A/S

PPG Industries, Inc.

Sniezka SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: :AkzoNobel released Interpon D2525 Low-E powder coatings with an Environmental Product Declaration for façade durability. The product targets architectural markets and is relevant for specifiers in Poland concerned with durability and environmental credentials.

- April 2024: MIPA SE bought HAERING Polska near Bydgoszcz to secure local production and expand industrial and architectural supply.

Poland Architectural Coatings Market Report Scope

Architectural coatings are specialized products designed for application on residential and commercial buildings to deliver aesthetic appeal, weather resistance, and long-term durability. These coatings protect structures from moisture, UV radiation, and corrosion, while enhancing the visual appearance of both interior and exterior surfaces.

The Poland architectural coatings market is segmented by end-user industry, technology, and resin. By end-user industry, the market is segmented into residential and commercial. By technology, the market is segmented into water-borne and solvent-borne. By resin, the market is segmented into acrylic, alkyd, epoxy, polyester, polyurethane, and other resin types. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By End User Industry

| Residential |

| Commercial |

By Technology

| Water-borne |

| Solvent-borne |

By Resin

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

| By End User Industry | Residential |

| Commercial | |

| By Technology | Water-borne |

| Solvent-borne | |

| By Resin | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms