Nordic Countries Architectural Coatings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

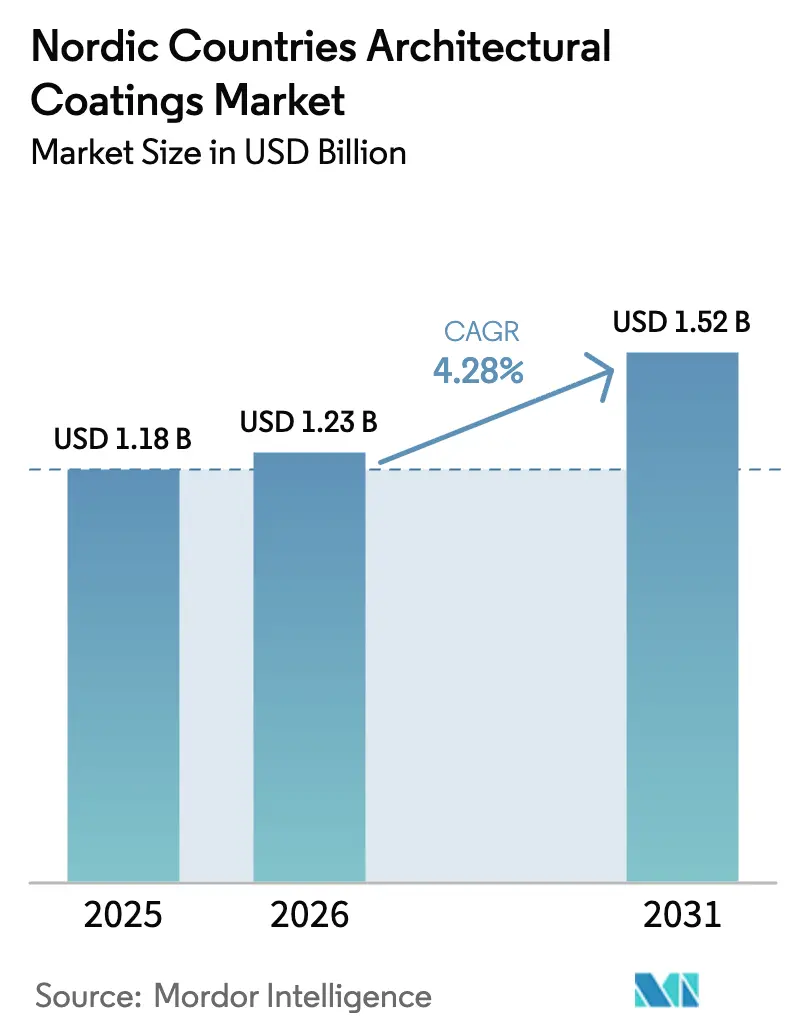

| Base Year Market Size (2025) | USD 1.18 Billion |

| Market Size (2026) | USD 1.23 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nordic Countries Architectural Coatings Market Analysis by Mordor Intelligence

The Nordic Countries Architectural Coatings Market size is projected to expand from USD 1.18 billion in 2025 and USD 1.23 billion in 2026 to USD 1.52 billion by 2031, registering a CAGR of 4.28% between 2026 to 2031. Residential renovation dominates demand, while digital retail and color-matching apps shorten decision cycles and steer shoppers toward premium, low-odor waterborne paints. Titanium dioxide and acrylic feedstock inflation squeezes margins, yet subsidy-backed bio-based chemistry offers a defensive hedge for innovators able to access EU funding. Competitive concentration sits in the middle ground; four multinationals hold roughly two-thirds of regional volume, but smaller challengers are winning share online with Nordic Swan–certified ranges and next-day delivery. Norway’s 100% emission-free public-tender rule from 2025 is a pivotal catalyst because it effectively bans solventborne offerings and accelerates the shift toward hybrid acrylic-polyurethane dispersions.

Key Report Takeaways

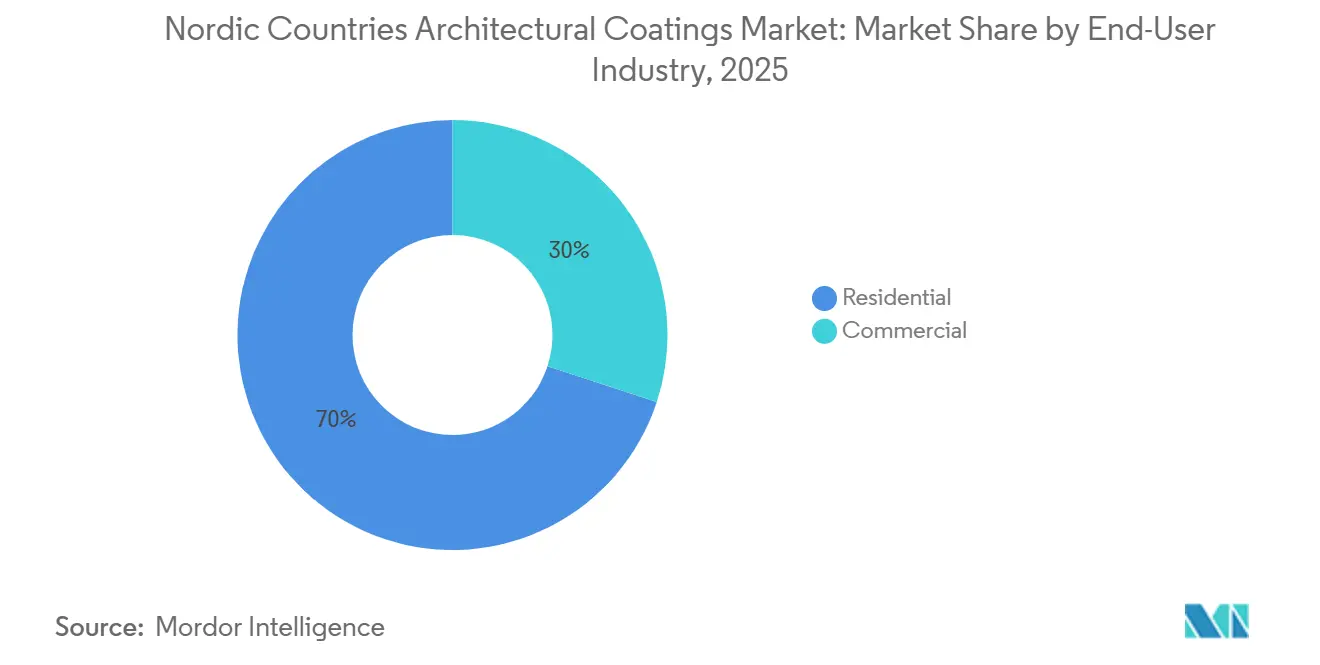

- By end-user, residential captured 69.96% of the architectural coatings market share in 2025, while it also recorded the fastest 4.54% CAGR through 2031.

- By technology, waterborne systems led with 84.42% of the architectural coatings market share in 2025 and are projected to advance at a 4.74% CAGR to 2031.

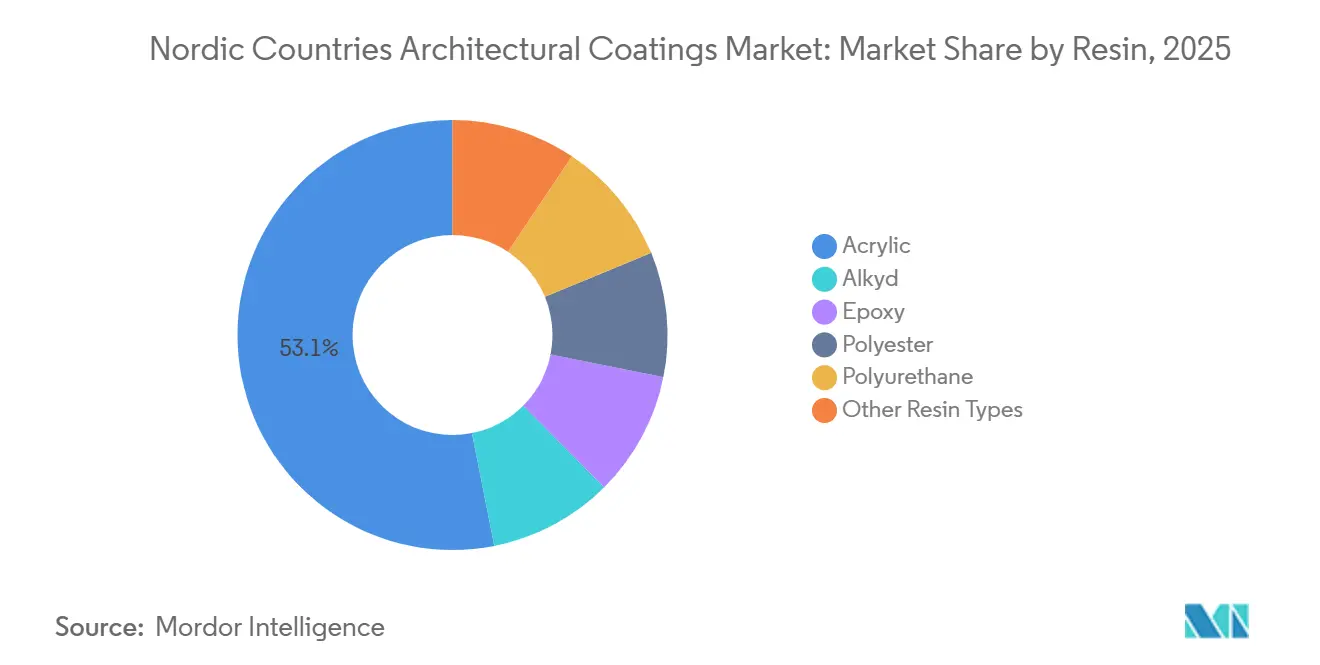

- By resin, acrylic formulations commanded 53.11% share of the architectural coatings market size in 2025 and are set to grow at a 4.67% CAGR over 2026-2031.

- By geography, Sweden contributed 34.56% of regional volume in 2025; Norway is expected to post the fastest 4.77% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Nordic Countries Architectural Coatings Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation-led DIY boom in detached housing | +1.2% | Sweden, Denmark, Norway | Medium term (2-4 years) |

| Green-building codes accelerating low-VOC uptake | +1.0% | All Nordic markets; Norway leads | Long term (≥4 years) |

| Weather-proofing demand from harsh Nordic climate | +0.8% | Finland, Norwegian coast, northern Sweden | Long term (≥4 years) |

| E-commerce paint retail and color-matching apps | +0.6% | Stockholm, Oslo, Copenhagen, Helsinki | Short term (≤2 years) |

| EU/EEA subsidies for bio-based chemistry scale-up | +0.5% | Denmark, Sweden | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Renovation-Led DIY Boom in Detached Housing

Nordic households continue to refinance renovation rather than relocate, which lifts unit volumes for interior wall and trim paints. Online engagement is decisive; 80% of private painting customers in Flügger’s network begin their journey digitally, and that online interaction correlates with same-store sales gains. Survey data show 45% of Swedes plan paint projects and 72% feel confident applying coatings themselves, prompting brands to launch smaller pack sizes and virtual color visualizers that curb mismatches[1]Swedish Paint and Printing Ink Makers Association, “Home Renovation Survey 2025,” sveff.se. Detached homes, which dominate Nordic housing stock, absorb waterborne acrylics able to dry in cool, humid climates. Mortgage-rate headwinds dampen new-build activity, yet renovation spend remains stable, preserving throughput for retail channels. Suppliers therefore prioritize quick-drying, low-odor products that allow residents to occupy rooms immediately after application.

Green-Building Codes Accelerating Low-VOC Uptake

Regulation is compressing product life cycles and pushing solventborne lines to the margins. Norway’s net-zero energy code and 100% emission-free tender rule from 2025 effectively remove hydrocarbon solvents from publicly funded projects[2]InfraSweden2030, “Zero-Emission Public Procurement,” infrasweden2030.se. Sweden mandates carbon footprint declarations for construction products, while Denmark invested DKK 2.5 billion into green construction research and development in 2023. Across the region, the Nordic Swan Ecolabel caps VOCs at 30 g/L for interior matt paints and 100 g/L for exterior coatings; retailers prioritize Swan-certified SKUs on shelf, cementing low-VOC dominance. Compliance drives rapid portfolio rationalization, and suppliers with digital product passports stand to win public contracts as data auditing tightens. Consequently, waterborne acrylic-polyurethane hybrids become the default selection in both residential and commercial segments.

Weather-Proofing Demand from Harsh Nordic Climate

Large swings between –40 °C winters and +30 °C summers subject façades to freeze-thaw cycles and UV stress. Brands respond with binder innovations such as silicate-based paints that deliver 15-year durability in coastal conditions and alkyd-acrylic hybrids that retain flexibility and hardness across the temperature span. Finland’s Wood Building Programme, which aims to double wooden structures, escalates the need for breathable, alkali-resistant coatings that prevent moisture entrapment. Infrared-reflective pigments that lower surface temperature by up to 20 °C mitigate thermal degradation, while self-cleaning silicone additives reduce biofouling in humid fjord regions. The net effect is sustained demand for premium exterior systems that lengthen repaint intervals, offsetting volume pressure from slower construction growth.

E-Commerce Paint Retail and Color-Matching Apps

Digital channels compress the path from inspiration to purchase. Flügger’s webstore lists every tintable option online, reversing the historical dominance of white paint in shops and lifting colored-paint mix ratios. Third-party scanners such as Innovatint and ColorMatchic enable small retailers to match competitor shades within minutes, undermining brand lock-in and shifting differentiation to service and sustainability. An OECD study shows Nordic retailers that integrate e-commerce and payment technology enjoy 20-40% higher labor productivity than peers, giving them room to absorb raw-material inflation. As professional painters adopt mobile workflow apps, order velocity rises and just-in-time delivery becomes a standard expectation, further advantaging suppliers with regional warehouses and API-integrated ordering systems.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile TiO₂ and acrylic feedstock prices | –0.9% | All Nordic countries; Denmark and Sweden most import-exposed | Short term (≤2 years) |

| Skilled-labor shortage slowing repaint cycles | –0.7% | Norway, Finland, Denmark, Sweden | Medium term (2-4 years) |

| Microplastics regulation driving reformulation cost | –0.5% | EU-wide; Denmark leads pilot substitution projects | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile TiO₂ and Acrylic Feedstock Prices

Tronox lifted titanium dioxide prices by 2-4% in Q1 2026 after closing its 90,000-ton Botlek plant, while Venator idled 650,000 tons of global capacity, tightening supply and amplifying sulfur-price spikes of 160%. EU anti-dumping duties block cheaper Chinese imports, locking Nordic buyers into higher-cost European supply. BASF raised acrylic monomer prices by USD 0.12 per pound in 2025 as propylene disruptions roiled the chain, with spot acrylic acid swinging between USD 1,290 and USD 1,457 per ton. Smaller local brands lack hedging leverage and may either accept margin erosion or dilute formulations with extenders that risk warranty claims.

Skilled-Labor Shortage Slowing Repaint Cycles

Norway’s employer confederation reports 6 in 10 contractors cannot secure skilled workers, and construction output fell NOK 67 billion over three years as foreign labor exited on a weak krone. Denmark’s foreign construction workforce climbed to 26,500 in 2024, yet electricians and HVAC technicians remain scarce despite a pay-limit scheme of DKK 514,000 per year. Finland counts a 15,000-worker deficit, with 40% of technicians above 55 years. When crews are unavailable, building owners stretch repaint cycles and specify 10-15 year durability products, shifting the revenue mix toward higher-margin premium ranges while constraining overall volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Residential Renovation Drives Volume

The residential industry segment dominated sales with 69.96% of the architectural coatings market share in 2025, and it is set to log a 4.54% CAGR to 2031. The architectural coatings market size for residential repainting therefore remains the critical barometer for distributors. Sweden’s private renovation outlays held firm even as new residential investment fell 55% since mid-2022. Digital color visualization converts online browsers into in-store transactions, underpinning offline sales. DIY demand favors low-odor waterborne acrylics in 1-2.5-liter packs and extends to niche sample pots for home-office accent walls.

Commercial premises represent the balance of volume, and stricter building codes make them an anchor customer for Nordic Swan–certified waterborne systems. Norway’s net-zero rules eliminate solventborne lines in government projects from 2025. Prefabricated timber modules popular in Sweden’s offsite sector require factory-cured polyurethane or UV-cured films that can withstand transport abrasion and on-site assembly. Growth is solid but slower than residential because public tenders often extend over multiyear funding cycles.

By Technology: Waterborne Systems Cement Supremacy

Waterborne coatings captured 84.42% of regional demand in 2025 and will outpace the overall architectural coatings market at a 4.74% CAGR through 2031. Low-VOC regulations and consumer preference for odorless products hard-wire waterborne dominance. Nordic Swan limits of 30 g/L VOC for interior matt finishes, and 100 g/L for exterior paints have become the de facto market threshold. High-solid acrylic-polyurethane hybrids now rival solventborne alkyds on hardness and adhesion, closing historical performance gaps.

Solventborne products persist in specialist niches such as steel primers and heritage woodwork that demand extended open time or deep penetration. Yet REACH microplastic deadlines add cost to both chemistries, eroding remaining solventborne advantages. Suppliers investing in waterborne research and development benefit from shorter regulatory-approval cycles and broader shelf access at major retailers.

By Resin: Acrylic Leads, Hybrids Create Premium Upside

Acrylic systems held 53.11% of regional volume in 2025 and are projected to expand at a 4.67% CAGR to 2031. They meet stringent VOC targets, offer UV stability and bond to mineral substrates prevalent in Nordic housing. Feedstock volatility in acrylic monomers motivates formulators to integrate styrene or bio-based carbon black from CO₂ capture, as showcased in Teknos’s UP Catalyst tie-up.

Alkyds, once dominant for exterior wood, are losing share to waterborne alkyd emulsions that cure via autoxidation without solvent release. Epoxy and polyurethane resins serve smaller, value-dense niches such as industrial floors and high-traffic wood surfaces. The Circular Bio-based Europe call earmarks EUR 14 million for bio-based thermosets, signaling a path for renewable epoxy and polyurethane feedstocks that could disrupt the segment hierarchy over the next decade.

Geography Analysis

Sweden generated 34.56% of Nordic architectural coatings demand in 2025, yet its growth tempo trails peers because high mortgage rates depress new-build starts. Mandatory carbon declarations and a 50% CO₂-reduction target by 2030 favor coatings suppliers able to document low embodied carbon. InfraSweden2030 funding of 150 start-ups creates a pipeline of digital and bio-based solutions that incumbents can license, from AR color apps to lignin-based binders.

Norway will deliver the region’s quickest expansion at a 4.77% CAGR during 2026-2031, lifted by a state procurement policy that mandates emission-free sites and waterborne products. Skilled-labor scarcity magnifies the appeal of long-life silicone-modified acrylics with 10-year warranties, reducing repaint frequency for owners. Coastal freeze-thaw cycles drive the adoption of silicate and polysiloxane façades able to resist salt spray and ice abrasion.

Denmark’s market benefits from a DKK 2.5 billion green-construction research and development package that incentivizes recycled-content pigments and bio-based resins. Yet labor bottlenecks in technical trades may cap project throughput. Finland focuses on wood construction under its Wood Building Programme, boosting demand for breathable exterior systems that prevent moisture entrapment in timber. Across both countries, migration policy and aging workforces affect painting-contractor availability, again favoring premium long-cycle coatings.

Competitive Landscape

The Nordic countries architectural coatings market is moderately consolidated. AkzoNobel’s announced USD 25 billion all-stock merger with Axalta, due to close by early 2027, will yield USD 600 million in synergies and amplify raw-material purchasing power. Jotun leverages a global marine platform to transfer low-friction binder research into Nordic façade products, while Hempel invests in microplastics-free dispersions ahead of REACH deadlines.

Flügger’s “Flügger Organic” road map targets professional painters with mobile project-management apps, reducing administrative overhead for small contractors. Teknos occupies the sustainability niche, commercializing CO₂-derived carbon blacks that improve tint strength while lowering cradle-to-gate emissions. Digital-native challenger, Gebenna sells 30,000 tintable colors online and promises delivery within three days, placing margin pressure on store-based incumbents.

Nordic Countries Architectural Coatings Industry Leaders

AkzoNobel N.V.

Flügger group A/S

PPG Industries, Inc.

Teknos

Jotun

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Flügger announced new production lines in Kolding, Denmark, and Bollebygd, Sweden, to bolster its “Flügger Organic” portfolio and support rising professional demand.

- January 2025: Teknos signed an MoU with UP Catalyst to scale CO₂-derived carbon black for Nordic paints, financed by EUR 6.4 million equity, EUR 8 million grants and EUR 18 million EIB venture debt.

Nordic Countries Architectural Coatings Market Report Scope

Architectural coatings are specialized products designed for application on residential and commercial buildings to deliver aesthetic appeal, weather resistance, and long-term durability. These coatings protect structures from moisture, UV radiation, and corrosion, while enhancing the visual appearance of both interior and exterior surfaces.

The Nordic countries architectural coatings market is segmented by end-user industry, technology, resin, and geography. By end-user industry, the market is segmented into residential and commercial. By technology, the market is segmented into waterborne and solventborne. By resin, the market is segmented into acrylic, alkyd, epoxy, polyester, polyurethane, and other resin types. The report also provides market sizing and forecasts for four major countries in the region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Residential |

| Commercial |

| Waterborne |

| Solventborne |

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

| Denmark |

| Finland |

| Norway |

| Sweden |

| By End-User Industry | Residential |

| Commercial | |

| By Technology | Waterborne |

| Solventborne | |

| By Resin | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types | |

| By Geography | Denmark |

| Finland | |

| Norway | |

| Sweden |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms