Pipeline Pigging Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.38 Billion |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

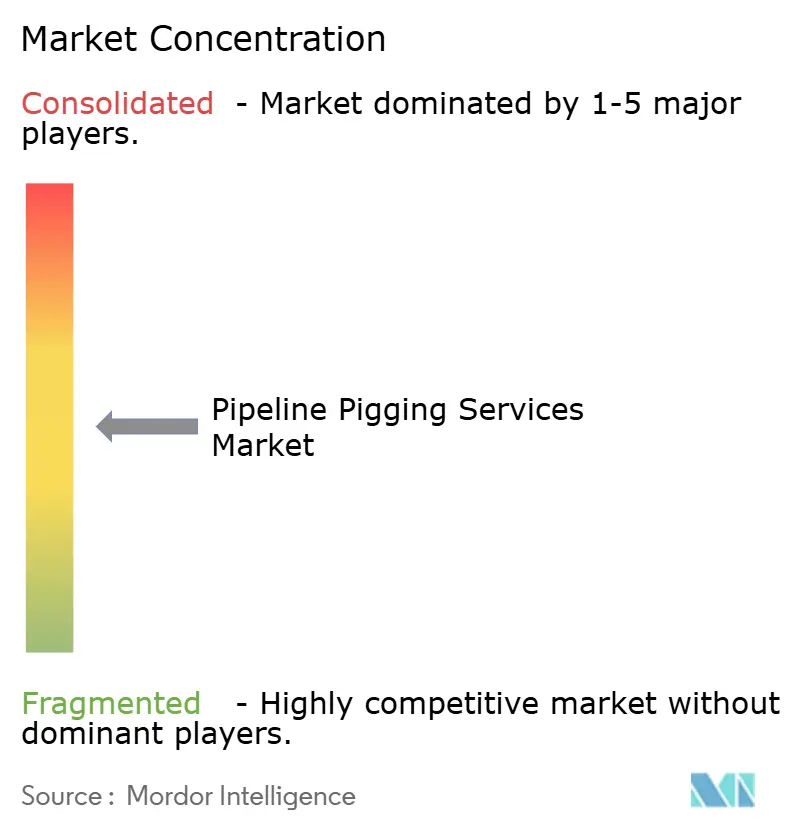

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pipeline Pigging Services Market Analysis by Mordor Intelligence

The Pipeline Pigging Services Market size is expected to grow from USD 1.78 billion in 2025 to USD 1.87 billion in 2026 and is forecast to reach USD 2.38 billion by 2031 at 4.93% CAGR over 2026-2031.

Regulatory tightening, accelerated integrity programs on aging pipelines, and rising adoption of intelligent inspection tools underpin this steady expansion. Mandates issued by the Pipeline and Hazardous Materials Safety Administration (PHMSA) in 2024, which incorporated more than 20 updated consensus standards, strengthened the obligation for in-line inspection of transmission lines, prompting operators to conduct more frequent, data-rich pigging campaigns[1]Pipeline and Hazardous Materials Safety Administration, “Notice of Proposed Rulemaking on Pipeline Repair Criteria,” phmsa.dot.gov. Capital spending on new cross-border lines in the Asia-Pacific and the Middle East, together with the rollout of AI-enhanced data analytics, is expanding service scope while raising technical thresholds for suppliers. At the same time, environmental requirements are driving innovation toward low-emission cleaning pigs, and competitive intensity is intensifying as regional specialists compete with global incumbents to secure high-value contracts.

Key Report Takeaways

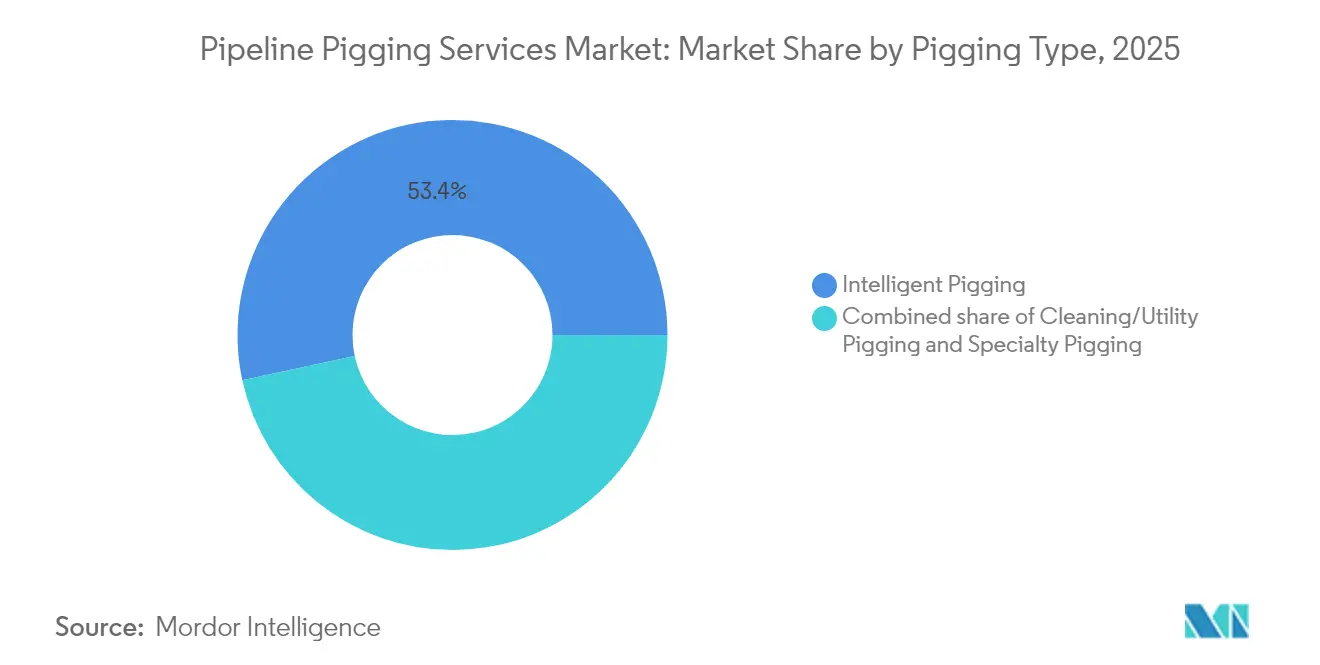

- By pigging type, intelligent pigging led with 53.38% of the pipeline pigging services market share in 2025; specialty pigging is projected to expand at a 7.58% CAGR to 2031.

- By pipeline fluid, crude oil pipelines accounted for a 39.08% share of the pipeline pigging services market size in 2025, while NGL & LPG lines are expected to register an 7.83% CAGR to 2031.

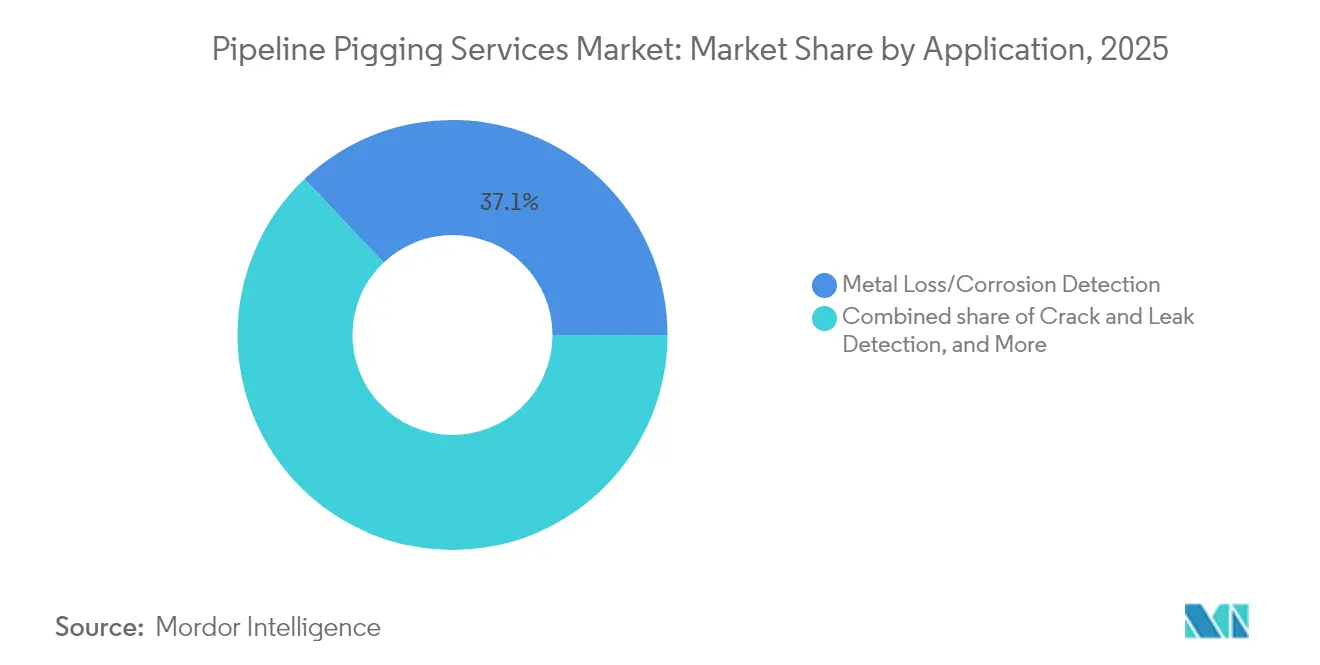

- By application, metal loss and corrosion detection held a 37.09% share of the pipeline pigging services market size in 2025; crack and leak detection is expected to advance at an 8.16% CAGR through 2031.

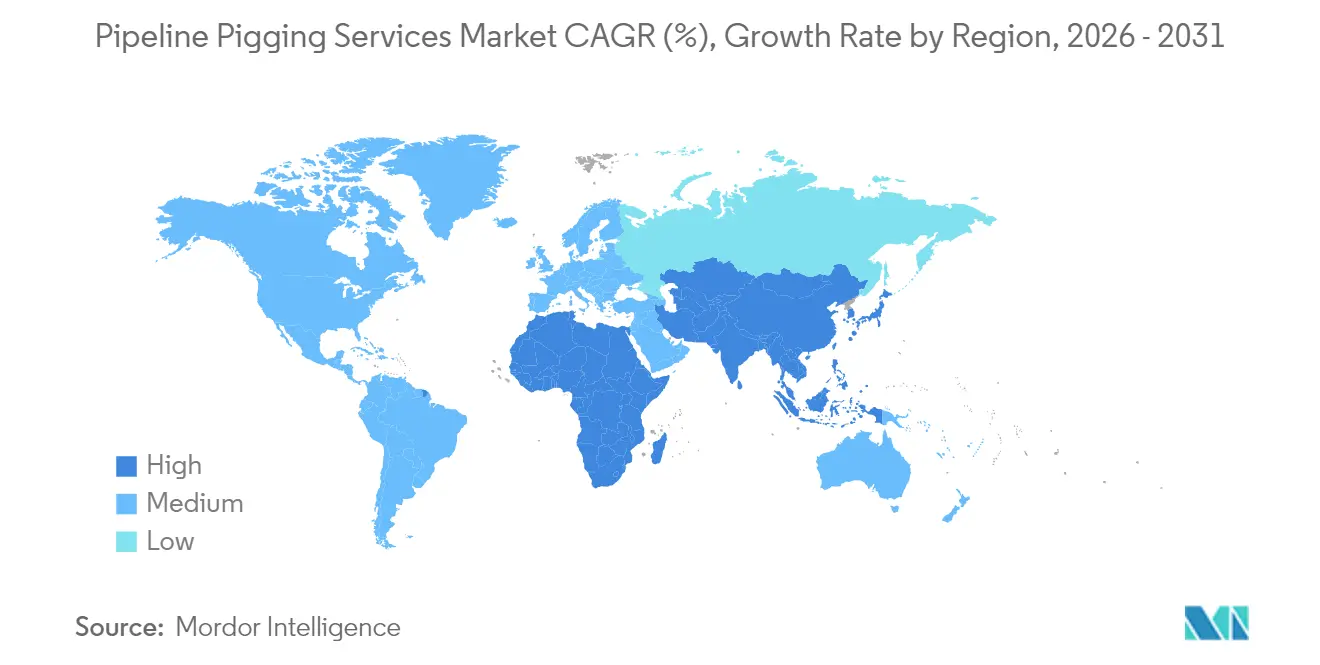

- By geography, North America dominated the market with a 40.71% revenue share in 2025; the Asia-Pacific region is forecast to post the fastest regional growth at a 6.61% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pipeline Pigging Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandates for periodic in-line inspection | +1.2% | North America & Europe core, global adoption spreading | Long term (≥ 4 years) |

| Aging global pipeline infrastructure nearing design life | +1.0% | North America & Europe, spreading to APAC | Long term (≥ 4 years) |

| Expansion of cross-border oil & gas networks | +0.8% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Rising incident rate of corrosion failures | +0.7% | Mature pipeline regions worldwide | Medium term (2-4 years) |

| AI-driven analytics improving data interpretation | +0.6% | North America & Europe early adoption, APAC following | Short term (≤ 2 years) |

| Digital-twin adoption enabling predictive schedules | +0.5% | Global, led by North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory mandates for periodic in-line inspection drive market expansion

Continual refinement of safety statutes is enlarging the addressable base for intelligent pigging. In May 2025, PHMSA opened consultations to modernize repair timelines, a move that obliges operators of gas transmission lines in Class 3 and 4 areas to verify integrity at least once every decade, thereby increasing the frequency of in-line inspections. Requirements under 49 CFR 192.493 to control operating pressure during maintenance have boosted demand for specialized low-friction pigs that safeguard flow integrity. New minimum rupture-detection standards introduced in June 2024 added further impetus, as operators must now prove the efficacy of their leak detection programs with verifiable in-line data. Collectively, these mandates are shifting pigging from discretionary maintenance to a recurring compliance expenditure that only full-service vendors can reliably meet.

Aging infrastructure crisis accelerates pigging service demand

Large stretches of North American and European transmission lines were laid during the 1950s and 1960s and now approach or exceed their nominal design life. Material degradation, weld fatigue, and internal corrosion have correspondingly risen, prompting operators to initiate short-interval pigging cycles targeting metal-loss anomalies before they evolve into failures. The age profile also magnifies the need for specialty pigs capable of maneuvering tight bends and diameter changes common in legacy assets. Because every additional year in service heightens risk, asset owners are retaining pigging contractors on multi-year blanket agreements, locking in pipeline pigging services market revenues through the end of the decade.

Cross-border pipeline expansion fuels regional growth

The Asia-Pacific’s build-out features headline projects, such as China’s 5,111-kilometer East Route pipeline and India’s USD 1.3 billion, 2,800-kilometer LPG trunk line, which was commissioned in June 2025[2]U.S. Energy Information Administration, “International Natural Gas Pipelines Projects,” eia.gov. These mega-lines require pre-commissioning caliper runs, nitrogen purge cleaning, and integrity baseline surveys, creating immediate demand spikes followed by decades of recurring inspections. Cross-border ventures often include performance-based maintenance clauses, allowing service providers to command premium pricing for advanced pigs that can operate over long runs with mixed elevations and products. In turn, equipment portfolios are adapting to hydrogen, ammonia, and CO₂ streams as energy transition pipelines move from concept to construction.

AI-driven analytics transform pigging data interpretation

Machine-learning engines now parse terabytes of MFL and ultrasonic data in hours, rather than weeks, improving anomaly grading accuracy and reducing false positives. Penspen’s September 2024 tie-up with Senslytics exemplifies how vendors are fusing cloud analytics with traditional field services to deliver predictive maintenance dashboards that recommend optimal pigging intervals [3]Penspen Ltd., “Penspen Partners with Senslytics on AI Pipeline Integrity,” penspen.com. Operators running thousands of miles of lines gain fleet-wide visibility, allowing them to schedule pigs based on real-time corrosion growth rather than generic frequency rules. This shift improves uptime and sharpens budgeting precision, reinforcing a service-plus-software model that is reshaping competitive dynamics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operational cost & downtime | -0.8% | Global, higher impact in cost-sensitive regions | Medium term (2-4 years) |

| Limitations in complex or “unpiggable” lines | -0.6% | Global, especially in legacy networks | Long term (≥ 4 years) |

| Safety risks causing delays and permits | -0.4% | Developed markets with strict oversight | Short term (≤ 2 years) |

| Environmental concerns over chemical pigs | -0.3% | North America & Europe core, expanding elsewhere | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High operational costs challenge market adoption

Pigging requires partial or full flow stoppage, specialist crews, and sometimes large-diameter launching barrels. Offshore operators shoulder added vessel and ROV costs, pushing a single deepwater run above USD 1 million in extreme cases. During tight commodity cycles, smaller producers often defer non-statutory inspections, which depresses short-term volumes in the pipeline pigging services market. Incidents in the North Sea where pigs become stalled in low-flow conditions illustrate how costs escalate if retrieval campaigns are necessary. As a countermeasure, service companies are promoting multifunction pigs that combine cleaning and geometry tasks in one pass, cutting downtime and person-hours per inspection.

Limitations in complex or “unpiggable” pipeline geometries

Legacy gathering systems often contain miter bends, diameter reductions, or low-flow segments that conventional pigs cannot traverse. Gel and tethered pig technologies mitigate some constraints, yet they add engineering complexity and safety risks. For operators, redesigning sections to improve piggability competes with alternative strategies such as external corrosion direct assessment. Although specialty pigging is the fastest-growing niche, unresolved technical barriers in certain unpiggable lines continue to cap total serviceable mileage and restrain broader market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pigging Type: Intelligence Drives Market Leadership

Intelligent pigging captured 53.38% of 2025 revenue, driven by MFL, ultrasonic, and EMAT technology, which provides verifiable, high-resolution wall-loss data demanded by regulators. That dominance is reinforced by large-diameter innovations, such as NDT Global’s 56-inch ultrasonic tool, released in collaboration with Saudi Aramco, which allows operators of major export pipelines to run a single inspection instead of multiple smaller tools. Cleaning and utility pigs continue to generate steady call-outs for wax and debris removal, yet the specialty category is rising at a 7.58% CAGR as custom-engineered gels, spheres, and bi-directional designs solve geometry challenges in aging assets. Service providers are expanding their consulting offerings to help clients interpret data and prioritize key insights, turning data services into a margin enhancer.

The pipeline pigging services market size for intelligent pigs is projected to exceed USD 1.31 billion by 2031 as risk-based inspection becomes mainstream. Intelligent pigs introduce digital twin inputs that shorten future planning cycles and boost safety conformance. Meanwhile, specialty pigs cater to hydrogen and CO₂ pilot lines where standard polymers may react with transported media, indicating further diversification potential.

By Pipeline Fluid Type: Crude Oil Dominance, NGL Growth Surge

Crude oil pipelines accounted for 39.08% of global revenue in 2025, as extensive, often decades-old networks in North America, the Middle East, and Russia require routine inline verification to maintain flow assurance and meet spill-prevention regulations. The pipeline pigging services market size tied to crude lines is forecast to grow steadily as aging and capacity expansion offset moderation in volume growth. Conversely, NGL & LPG pipelines are expected to post an 7.83% CAGR as shale output scales in the United States and major greenfield projects go live in India and China. Liquefied gases demand pigs engineered for condensate management and low-temperature operation, opening technical niches for high-integrity seals and differential-pressure control systems.

Natural gas transmission remains a core service domain, especially where operators transition to hydrogen blends. Refined-product systems also provide incremental runs aimed at minimizing interface contamination between gasoline, diesel, and aviation fuels. Water and slurry lines constitute a small slice, but they are drawing attention in mining regions intent on boosting throughput through internal coating maintenance and regular cleaning.

By Application: Corrosion Detection Leads, Crack Detection Accelerates

Metal-loss and corrosion detection retained a 37.09% share of 2025 revenue, as long-established steel assets are prone to thinning due to internal corrosion and external coating failure. Operators favor axial MFL and high-resolution UT tools to quantify defect depth, thereby directing excavation budgets efficiently. The pipeline pigging services market share for crack and leak detection remains smaller; yet, its 8.16% CAGR underscores the shift toward early-stage detection of fatigue and stress corrosion cracking, now mandated in high-consequence areas. Repeat in-line inspection, where consecutive runs overlay data, helps operators chart crack propagation and align repairs with outage schedules.

Crack and leak runs frequently integrate liquid-coupled phased-array UT sensors capable of sizing sub-millimeter defects at 10 mph tool speed, a specification valued in gas transmission lines that operate near allowable pressure limits. Geometry measurement, coupled with cleaning, remains essential for confirming bend radii and ovality deviations before smart pigs enter, thereby sustaining a dependable volume base for utility service fleets.

Geography Analysis

North America retained the largest regional share at 40.71% in 2025, supported by an estimated 2.7 million miles of active gathering, transmission, and distribution pipe. PHMSA rulemaking that strengthens rupture-mitigation measures and compresses repair windows is contributing to increased run volumes, while projects such as the 2 Bcf/d DeLa Express line, slated for service by 2028, will incorporate multi-station launcher and receiver infrastructure from the outset. Service providers benefit from deep client relationships, and advanced analytics hubs in Houston and Calgary anchor high-end data-interpretation contracts.

Asia-Pacific is set to post the fastest growth at 6.61% CAGR through 2031, underpinned by China’s 38 bcm/y east-route gas line and India’s massive LPG corridor, both commissioned or fully operational by 2025. Regional policy goals aimed at expanding gas penetration in residential and industrial sectors translate into extensive new midstream grids requiring commissioning sweeps and periodic inspections. Rising hydrogen and ammonia pilot lines—such as Sinopec’s 400-kilometer hydrogen link financed at 20 billion yuan—add prospects for specialty pigging. Funding models in developing economies are increasing, stipulating life-cycle integrity contracts that lock in long-term service revenues.

Europe keeps a stable outlook driven by life-extension needs on mature North Sea and continental grids. Strict environmental statutes and an aging asset base mean operators are adopting eco-friendly cleaning pigs that curtail chemical discharge. Digitalization programs accelerated by energy security concerns are driving more data analytics contracts toward vendors that can convert legacy run data into predictive maintenance dashboards. The Middle East & Africa, as well as South America, regions show mid-single-digit growth, as greenfield oil and gas export lines, along with regulatory modernization, gradually shift maintenance practices toward global benchmarks.

Competitive Landscape

The global pipeline pigging services market is moderately fragmented. ROSEN Group, T.D. Williamson and Baker Hughes deploy multidisciplinary fleets that span high-resolution MFL, UT, cleaning, and specialty pigs, leveraging proprietary software to bundle inspection with analytics. Their dominance is challenged by niche specialists that focus on local permitting or unique tool formats. Overall differentiation centers on data quality, run-length capacity, and environmental performance. Strategic M&A continued in 2024 when T.D. Williamson acquired Petro-Line, gaining access to PETROSLEEVE repair technology, which enhances its dig-to-repair offering.

Technology competition now hinges on AI-driven workflows. Penspen’s partnership with Senslytics combines inspection databases with machine-learning engines, enabling the pair to position itself as an integrated integrity advisor rather than a transactional service vendor. White-space opportunities exist in emerging Asia-Pacific markets where pipeline growth outstrips local service capacity. Environmental leadership is another battleground: CNX Resources’ HydroPurge innovation, which claims 91% emission reduction during pigging, illustrates how green credentials can win bids with environmentally sensitive operators.

Price pressure persists in commoditized cleaning campaigns, but premium rates endure for intelligent runs on large-diameter or difficult-to-access assets. To safeguard margins, leading contractors are embedding long-term framework agreements that guarantee minimum run volumes and facilitate data subscription add-ons. Regional joint ventures remain a preferred route for foreign entrants seeking to comply with local content rules, especially in India and Saudi Arabia, where national energy companies retain significant procurement influence.

Pipeline Pigging Services Industry Leaders

ROSEN Group

T.D. Williamson, Inc.

Baker Hughes Company

NDT Global (Eddyfi/NDT)

STATS Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Saipem and Subsea7 have revealed plans to merge into Saipem7, creating a USD 21.9 billion (EUR 20 billion) revenue giant with a 60-vessel construction fleet, aiming to provide integrated offshore pipeline solutions.

- January 2025: Baker Hughes introduced the SureCONNECT FE downhole wet-mate system, extending its subsea connection portfolio for deepwater flowlines.

- December 2024: T.D. Williamson closed its acquisition of Petro-Line and PETROSLEEVE technology, broadening its portfolio of pipeline integrity and repair services.

- September 2024: Penspen and Senslytics signed an agreement to embed AI algorithms into pigging data interpretation. In a bid to bolster Penspen's THEIA digital pipeline integrity management, the two companies are collaborating to integrate Senslytics' CausX AI technology.

Global Pipeline Pigging Services Market Report Scope

The pipeline pigging services market report includes:

| Intelligent Pigging |

| Cleaning/Utility Pigging |

| Specialty Pigging (Gel, Bi-Directional, etc.) |

| Crude Oil |

| Refined Products |

| Natural Gas |

| NGL and LPG |

| Water and Slurry |

| Crack and Leak Detection |

| Metal Loss/Corrosion Detection |

| Geometry Measurement & Bend Detection |

| Cleaning and Debris Removal |

| Commissioning and De-commissioning |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Pigging Type | Intelligent Pigging | |

| Cleaning/Utility Pigging | ||

| Specialty Pigging (Gel, Bi-Directional, etc.) | ||

| By Pipeline Fluid Type | Crude Oil | |

| Refined Products | ||

| Natural Gas | ||

| NGL and LPG | ||

| Water and Slurry | ||

| By Application | Crack and Leak Detection | |

| Metal Loss/Corrosion Detection | ||

| Geometry Measurement & Bend Detection | ||

| Cleaning and Debris Removal | ||

| Commissioning and De-commissioning | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the pipeline pigging services market?

The pipeline pigging services market size stood at USD 1.87 billion in 2026 and is projected to reach USD 2.38 billion by 2031.

Which pigging type generates the highest revenue?

Intelligent pigging leads, commanding 53.38% of 2025 revenue owing to stringent inspection regulations and superior data output.

Which region shows the fastest growth?

Asia-Pacific is expected to record the highest regional CAGR at 6.61% through 2031, propelled by large-scale pipeline construction in China and India.

What is the biggest growth restraint?

High operational cost, including downtime and specialized crew mobilization, represents the principal restraint, shaving an estimated 0.8% from forecast CAGR.

How are AI and digital twins influencing the market?

AI-driven analytics and digital-twin platforms enable predictive maintenance scheduling and faster data interpretation, reducing unnecessary pig runs and boosting market demand for high-value inspection services.

Which application segment is expanding the fastest?

Crack and leak detection is advancing at an 8.16% CAGR because of regulatory emphasis on early failure identification and advancements in ultrasonic inspection tools.

Page last updated on: