Photodiode Sensors Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

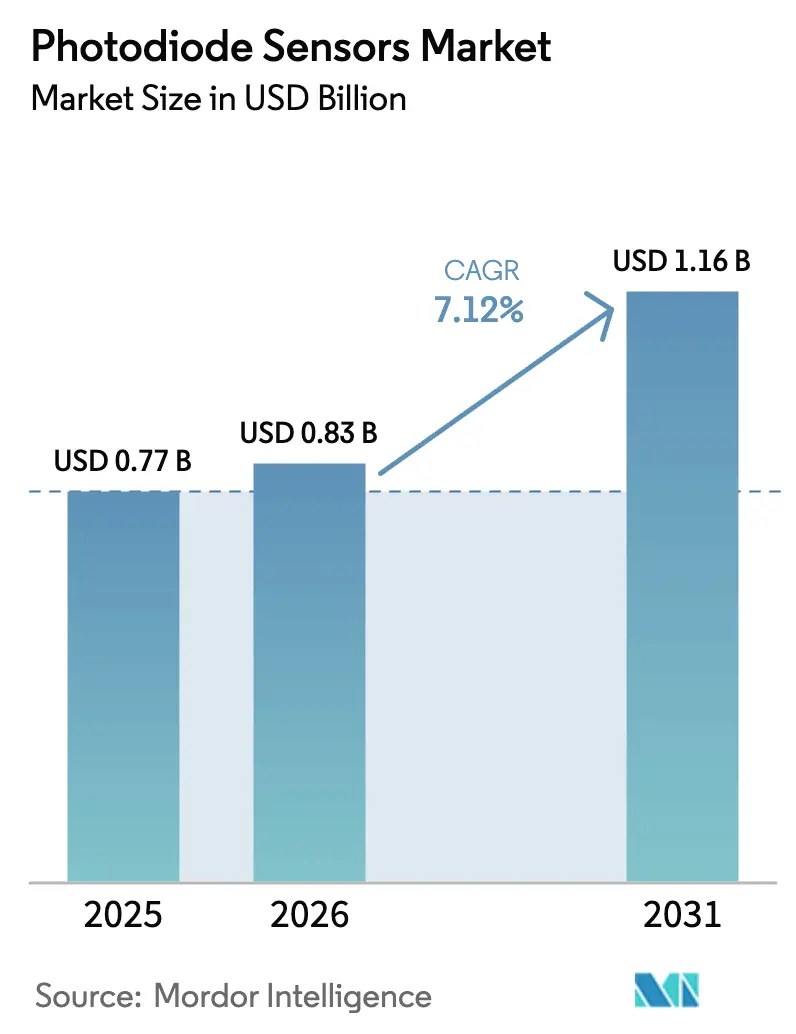

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

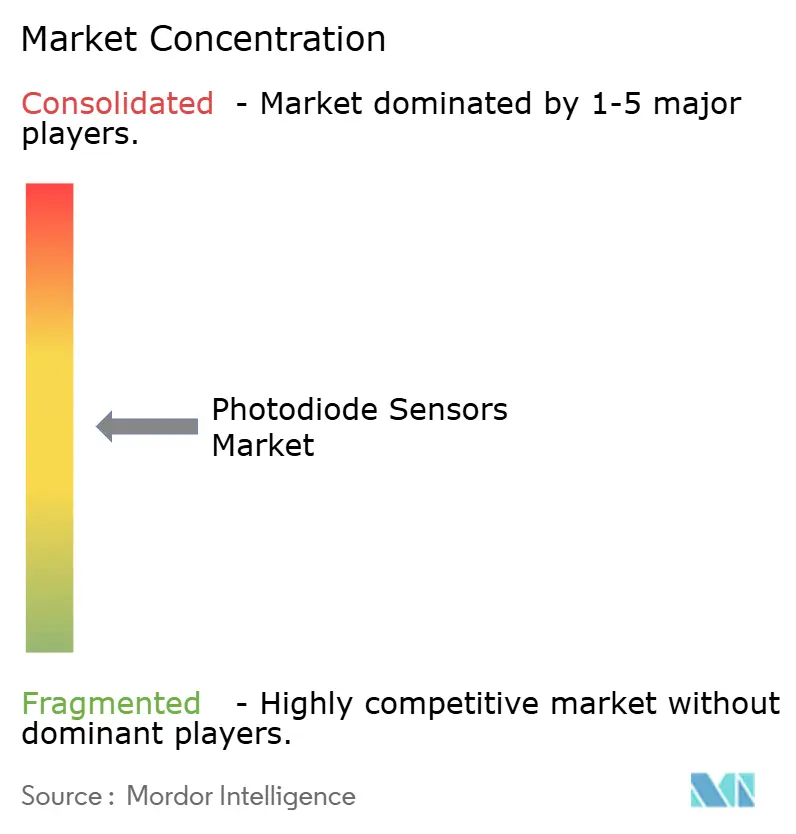

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Photodiode Sensors Market Analysis by Mordor Intelligence

photodiode sensors market size in 2026 is estimated at USD 0.83 billion, growing from 2025 value of USD 0.77 billion with 2031 projections showing USD 1.16 billion, growing at 7.12% CAGR over 2026-2031. Global demand is rising because 5G back-haul, LiDAR-enabled vehicles, and data-center photonics each require precision optical receivers that outperform legacy designs[1]NTT Corporation & NEC Corporation, "IOWN All-Photonics Network With Optical Fiber Sensing Functions Achieves Wide-Area Traffic Flow Monitoring", NEC Corporation, nec.com . The photonics sector’s resilience—valued at USD 865 billion in 2022 and forecast to hit USD 1.2 trillion in 2027—further underpins the photodiode sensors market growth trajectory. Supply chain vulnerabilities for indium and gallium, however, introduce cost and lead-time risks that could temper near-term output levels. [2]Amy Tolcin, "Quantifying Potential Effects of China’s Gallium and Germanium Export Restrictions on the U.S. Economy", U.S. Geological Survey, usgs.gov Competitive differentiation is now shifting from discrete components toward integrated modules that combine photodiodes, signal processing, and packaging in a single unit, shortening customers’ time-to-market in telecommunications, automotive, and medical imaging verticals.

Key Report Takeaways

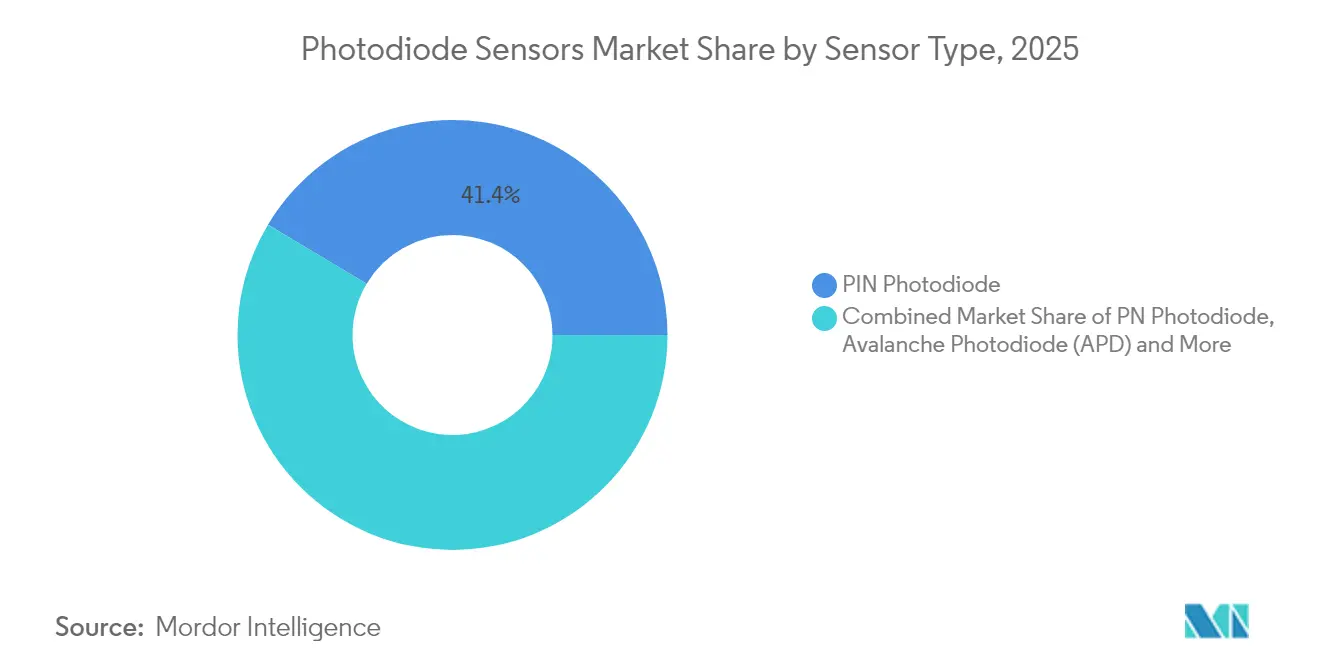

- By sensor type, PIN devices led with 41.42% of the photodiode sensors market share in 2025, while avalanche photodiodes are set to advance at an 8.23% CAGR through 2031.

- By material, silicon captured 57.38% share of the photodiode sensors market size in 2025, whereas silicon-germanium technology is projected to expand at an 8.01% CAGR.

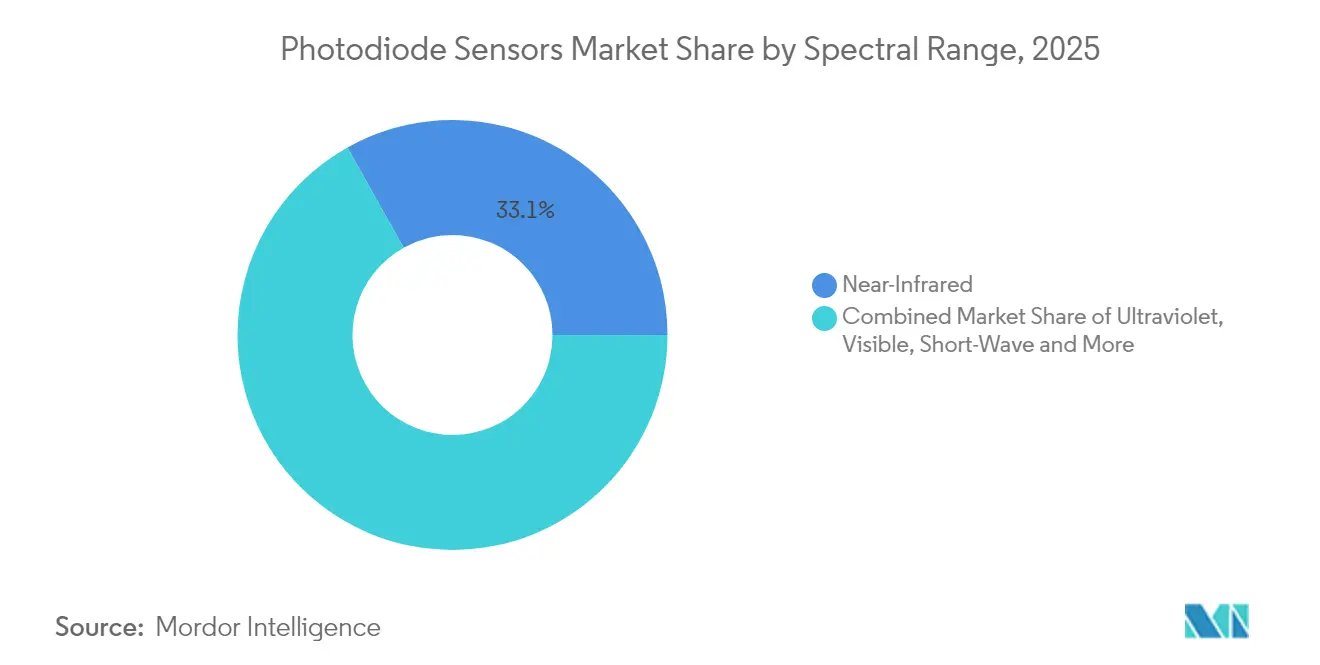

- By spectral range, near-infrared held 33.12% revenue share in 2025; short-wave infrared (SWIR) is the fastest-growing band with an 8.31% CAGR to 2031.

- By end-user industry, consumer electronics accounted for 28.45% of the photodiode sensors market size in 2025, yet automotive LiDAR is forecast to grow at an 8.62% CAGR through 2031.

- By geography, Asia-Pacific dominated at 45.55% share in 2025, whereas the Middle East & Africa region is paced to rise at a 9.22% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Photodiode Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in optical-fiber & 5G back-haul deployments | +1.8% | Global (APAC, North America lead) | Medium term (2–4 years) |

| Accelerating LiDAR/ADAS integration in vehicles | +1.5% | North America, Europe, China automotive hubs | Medium term (2–4 years) |

| Smartphone demand for ambient-light & proximity-sensing | +1.2% | Global, concentrated in APAC manufacturing | Short term (≤ 2 years) |

| Expanded use in medical imaging & pulse-oximetry | +0.9% | North America, Europe, emerging APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Optical-Fiber & 5G Back-haul Deployments

Data-heavy 5G networks are pushing operators to upgrade backbone links using coherent optical transceivers that rely on low-noise photodiodes. Trials by NTT and NEC using IOWN All-Photonics Networks demonstrated real-time traffic monitoring over existing fiber, confirming dual-use value for infrastructure owners.[3]NTT Corporation & NEC Corporation, "IOWN All-Photonics Network With Optical Fiber Sensing Functions Achieves Wide-Area Traffic Flow Monitoring", NEC Corporation, nec.comAcademic prototypes have already moved toward 100 Gbps photodiodes capable of 100-km reach, matching early 6G fronthaul benchmarks. Free-space optical links that hit 36.4 Gbit/s highlight the versatility of high-bandwidth receivers in urban environments where trenches are costly. Power-efficient datacenter interconnects show transmitter-side energy efficiency at 1.59 pJ/bit, putting pressure on detector makers to improve receiver sensitivity at similar power budgets.[4] Combined, these requirements place the photodiode sensors market at the heart of next-generation wireline and wireless convergence strategies.

Accelerating LiDAR/ADAS Integration in Vehicles

LiDAR adoption is moving beyond premium brands as cost curves fall rapidly. Sony’s IMX479 stacked SPAD depth sensor delivers 300-m detection at 37% photon-detection efficiency with sample shipments slated for autumn 2025. Korea’s SPAD roadmap hit 56 ps timing jitter and 8 mm resolution, ideal for short-range driver-assistance systems. Chinese suppliers have spurred price competition, accelerating unit volume growth in mid-range vehicles. VCSEL-to-photodiode co-packaging is cutting bill-of-materials while boosting reliability. FMCW architectures, which depend on heterodyne photodiodes, are now reaching detection limits near theoretical ceilings, validating upcoming production rollouts.[5]

Smartphone Demand for Ambient-Light & Proximity Sensing

Handset makers continue integrating ambient-light, proximity, and PPG biosensing into consolidated modules, driving high-volume silicon photodiode orders. Wearables and smartphones together underpin a good growth for PPG biosensors through 2030, ensuring additional demand for near-infrared detectors in tiny footprints. Under-display fingerprint and facial-ID systems need photodiodes with superior near-infrared performance and minimal crosstalk, pushing innovation in trench isolation and backside illumination. Machine-learning-based gesture recognition further enlarges the addressable sensor pool, while laser-based air-quality modules such as Panasonic’s SN-GCQB1 show how photodiode design know-how scales across adjacent consumer applications.

Expanded Use in Medical Imaging & Pulse-Oximetry

Computed tomography arrays and pulse-oximetry probes require low-noise, high-responsivity photodiodes that maintain calibration stability over device lifetimes. KAIST recently demonstrated room-temperature mid-infrared detectors capable of real-time CO₂ monitoring, indicative of future cost-reductions through CMOS compatibility. [6]Lawrence Livermore National Laboratory, "Depositing Quantum Dots on Corrugated Chips Improves Photodetector Capabilities", Phys.org, phys.org Coherent Corp. identifies healthcare instrumentation as a USD 69 billion addressable segment growing 7% annually, confirming sustained budget allocation for photonics in medicine. Wearable biosensors, powered by miniature photodiodes, are now central to personalized-medicine rollouts within hospital tele-health programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Temperature-dependent dark current & noise | -0.8% | Global, extreme climate regions | Short term (≤ 2 years) |

| Volatile indium & gallium supply chain | -1.1% | Global, APAC manufacturing most affected | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Temperature-Dependent Dark Current & Noise

Dark current rises exponentially with temperature, degrading signal-to-noise ratios in mission-critical photodiode deployments. Thorlabs’ recent benchmarks confirmed germanium detectors show the highest dark-current drift, whereas InGaAs variants offer better thermal stability. Organic photodiodes with cross-linked transport layers now deliver 1 nA cm-² dark-current density at −5 V bias, extending sensor reliability for consumer wearables. Perovskite detectors boasting 2.4×10¹² Jones detectivity promise long-term differentiation once commercial yield hurdles are cleared.

Volatile Indium & Gallium Supply Chain

China’s 2024 export restrictions on gallium and germanium spotlight the resource risk behind every III-V photodiode.[7]Amy Tolcin, "Quantifying Potential Effects of China’s Gallium and Germanium Export Restrictions on the U.S. Economy", U.S. Geological Survey, usgs.govU.S. gallium-arsenide wafer imports fell sharply in 2023, triggering price premiums for high-performance telecommunication receivers. Partnerships such as LightPath-NRL aim to commercialize BDNL4 chalcogenide glass as a germanium substitute, lowering material exposure. Sustainability studies project 6G rollouts could demand up to 4.4% of annual indium production, intensifying sourcing competition within the photodiode sensors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Avalanche Photodiodes Drive Innovation

PIN devices accounted for 41.42% of the photodiode sensors market share in 2025 as telecom and consumer OEMs favored their cost-performance trade-off. Avalanche photodiodes are forecast to post an 8.23% CAGR through 2031, lifting the photodiode sensors market size as LiDAR mandates single-photon sensitivity. Korea’s 56 ps SPAD milestone underscores competitive headroom for timing resolution improvements in automotive safety systems. Device vendors now migrate from discrete components to stacked-sensor architectures, delivering on-chip signal conditioning that simplifies vehicle OEM qualification.

Gallium-nitride PIN avalanche variants target ultraviolet fire-detection and space-borne applications that demand radiation hardness. PN configurations remain viable in value-oriented consumer products, while Schottky designs address microwave photonics where bandwidth trumps quantum efficiency. Ecosystem players invest in laser-receiver co-design to balance gain, linearity, and power, signaling continued divergence within the photodiode sensors market.

By Material: Silicon Dominance Challenged by Compound Semiconductors

Silicon retains 57.38% share of the photodiode sensors market size because CMOS fabs deliver unmatched scale and cost economics. Silicon-germanium devices, with an 8.01% forecast CAGR, improve responsivity at 1.55 µm wavelength yet stay fab-compatible, appealing to telecom OEMs seeking cost parity with legacy Si pipelines. Indium-gallium-arsenide detectors remain indispensable for 700 nm-1.8 µm ranges, commanding premium pricing across data-com optics.

Type-II superlattice architectures show 2.1×10¹¹ cm Hz¹/²/W detectivity, 256% above traditional eSWIR offerings, creating opportunities in machine vision and agriculture. Organic photodiodes and quantum-dot hybrids now achieve 5.55×10¹² Jones detectivity at 1.15 µm, indicating cost-effective paths for niche wearables and environmental testers. STMicroelectronics’ quantum-dot image sensor roadmap combining 1.62 µm pixel pitch with 60% external quantum efficiency at 1,400 nm hints at mainstream adoption inside the photodiode sensors market.

By Spectral Range: SWIR Applications Accelerate Growth

Near-infrared wavelengths delivered 33.12% of 2025 revenue as telecom, biometric, and ambient-light modules rely on 850-1,000 nm performance. SWIR demand is rising at an 8.31% CAGR, expanding the photodiode sensors market size for sorting, moisture detection, and quality-inspection tools. Sony’s SenSWIR chip cuts pixel pitch via Cu-Cu bonds, shrinking camera footprints for factory automation.

Industrial integrators value uncooled room-temperature operation in InGaAs arrays while weighing optional TECs that improve dark-noise floors. Black GeSn photodiodes on silicon deliver 1,960 nm response with reflection losses reduced across 1,200-2,200 nm, positioning CMOS fabs to challenge III-V incumbents. Mid-wave and long-wave IR remain specialized, dominated by indium-antimonide photodiodes for 1-5.5 µm military imaging.

By End-user Industry: Automotive LiDAR Drives Highest Growth

Consumer electronics held 28.45% revenue in 2025 as smartphones, wearables, and home devices integrated ambient-light and biosensing photodiodes. Automotive LiDAR adoption is climbing at an 8.62% CAGR, reinforcing the photodiode sensors market as the safety backbone for Level-3 autonomy. Telecom carriers sustain steady orders on the back of 5G back-haul and coherent optics upgrades.

Healthcare applications are entering a new growth phase, extending beyond pulse-oximetry to computed-tomography and point-of-care diagnostics that embed photodiodes in multi-modal probes. Aerospace and defense budgets support high-reliability demand, as evidenced by Teledyne FLIR’s USD 168.3 million U.S. Army contract for sensor-suite upgrades. Industrial automation embraces indirect time-of-flight cameras like onsemi’s Hyperlux ID, which measures depth to 30 m for pick-and-place robotics.

Geography Analysis

Asia-Pacific dominated the photodiode sensors market with a 45.55% revenue share in 2025, leveraged by dense semiconductor ecosystems in China, Japan, and South Korea. Japan’s collaboration between NICT and Sony achieved the first practical quantum-dot surface-emitting laser at 1,550 nm, improving local component depth in optical-fiber communication. Chinese LiDAR producers Hesai and RoboSense accelerate cost deflation, broadening OEM adoption at sub-USD 500 sensor targets. South Korea’s KIST breakthroughs in 56 ps SPAD arrays place regional vendors ahead on timing-jitter metrics critical for ADAS.

North America balances innovation and defense demand. Coherent Corp. reported USD 1.43 billion Q2 FY25 revenue, up 27% year over year, showcasing diversified exposure across datacom, instrumentation, and aerospace. CHIPS Act allocations for indium-phosphide expansion will insulate domestic photodiode supply lines against future geopolitical shocks. Quantinuum’s new R&D center in New Mexico taps Sandia and Los Alamos labs to accelerate quantum-photonics IP, ensuring a pipeline of next-generation detector prototypes.

Europe commands high-value export niches, shipping EUR 124.6 billion (USD 133.5 billion) in photonics during 2022, equal to 15% global share and supported by 10.5% R&D intensity. Lynred’s EUR 85 million (USD 91.1 million) facility expansion in Grenoble will double cleanroom capacity and secure sovereign infrared supply for EU defense programs. VIGO Photonics’ HyperPic mid-infrared project, funded by EU grants, demonstrates ongoing commitment to integrated photonic circuits targeting medical and industrial gas sensing. The Middle East & Africa region holds the fastest 2026-2031 CAGR at 9.22% as national smart-city agendas and potential advanced fabs in the UAE catalyze future local demand.

Competitive Landscape

Market concentration remains moderate. Hamamatsu Photonics booked FY2024 net sales of JPY 203,961 million (USD 1.37 billion) and is building a new Compound Semiconductor Fab Center to lift opto-semiconductor output. Coherent Corp.’s diversified optics portfolio delivered USD 1.43 billion revenue in Q2 FY25, notching 27% growth through balanced participation in communications, instrumentation, and electronics. SICK AG and Endress+Hauser joined forces in a 50-50 joint venture to embed sensor suites into process-automation channels, broadening cross-selling capacity in refinery and chemical plants.

Strategic playbooks center on vertical integration and differentiated IP. Sony advances stacked SPAD designs to lock in automotive Tier-1s, while onsemi scales indirect time-of-flight sensors for industrial automation, giving OEMs a single-vendor route from pixel to software. TDK’s Spin Photo Detector showcases an emerging niche where spintronics can multiply data-throughput by 10×, aiming to secure sockets in AI inference clusters. Up-starts such as Lidwave leverage 4D lidar-on-chip integration, compressing cost and bill-of-materials, which threatens incumbent price umbrellas.

Supply-chain de-risking remains top of mind. Players pursue dual-sourcing for indium and gallium and evaluate chalcogenide alternatives to germanium, aligning with ESG mandates and reducing trade-policy exposure. Organic and perovskite photodiodes present low-temperature, solution-processed substitutes that may disrupt incumbent wafer-based economics in low-cost consumer and IoT nodes.

Photodiode Sensors Industry Leaders

-

Hamamatsu Photonics K.K

-

Thorlabs, Inc.

-

Edmund Scientific Corporation (Edmund Optics)

-

Centronic, Ltd.

-

Excelitas Technologies Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sony Semiconductor Solutions announced the IMX479 stacked SPAD depth sensor for automotive LiDAR, offering 300-m range and 37% photon-detection efficiency, with samples in autumn 2025 priced at JPY 35,000 (USD 235) per unit

- May 2025: Lawrence Livermore National Laboratory introduced an electrophoretic quantum-dot deposition method that boosts near-infrared detector performance on textured substrates

- April 2025: TDK demonstrated the world’s first Spin Photo Detector achieving 10× data-rate gains aimed at AI accelerator interconnects

- March 2025: Onsemi launched the Hyperlux ID real-time indirect ToF sensor for 30-m industrial depth-sensing

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we view the photodiode sensor market as all packaged solid-state devices that directly convert incident light into an electrical signal and are shipped as stand-alone sensors or as optical front-ends within proximity, ambient-light, color, and LiDAR modules. Sales reported cover PN, PIN, avalanche, and Schottky architectures built on silicon, SiGe, InGaAs, GaN, or related compound substrates that serve consumer electronics, telecom, industrial, automotive, medical, security, and aerospace applications across every major region.

Scope Exclusion: Bare die sold to image-sensor foundries and phototransistors embedded in discrete logic ICs are not counted.

Segmentation Overview

-

By Sensor Type

- PN Photodiode

- PIN Photodiode

- Avalanche Photodiode (APD)

- Schottky Photodiode

-

By Material

- Silicon (Si)

- Silicon-Germanium (SiGe / Ge)

- Indium Gallium Arsenide (InGaAs)

- InGaAsP / InP

- Gallium Nitride (GaN)

-

By Spectral Range

- Ultraviolet (200-400 nm)

- Visible (400-700 nm)

- Near-Infrared (0.7-1.4 µm)

- Short-Wave IR (1.4-3 µm)

- Mid/LW IR (>3 µm)

-

By End-user Industry

- Consumer Electronics

- Telecommunications

- Aerospace and Defense

- Healthcare

- Automotive

- Industrial Automation and IoT

- Security and Surveillance

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

-

APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

-

Middle East and Africa

- GCC

- Turkey

- South Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed design engineers at smartphone OEMs, optoelectronic contract manufacturers in China and Malaysia, purchasing managers at fiber-optic transceiver firms in the United States, and medical-device integrators across Europe. Their insights guided us in validating yield losses, application-level average selling prices, and emerging wavelength requirements that secondary data could not quantify.

Desk Research

Our analysts first mapped global supply by screening publicly available datasets such as UN Comtrade optical-device codes, European Union TARIC shipment logs, and United States Census optical component export tables. We layered in trend indicators from associations such as the Japan Photonics Council, the Optical Society, and SEMI's quarterly billings, while company 10-Ks, investor decks, and patent analytics from Questel helped clarify technology diffusion rates. Paid platforms including D&B Hoovers and Dow Jones Factiva supplied revenue splits and capacity shifts that public sources missed. The sources cited represent only a sample of the wider literature pool reviewed for cross-checks and context gathering.

Market-Sizing & Forecasting

A blended top-down and bottom-up model underpins the market baseline. We reconstructed global demand from optoelectronic export-import volumes and fab utilization reports, then validated the totals with sampled supplier roll-ups of units multiplied by blended ASPs. Key variables include smartphone OLED penetration, 5Gfiber back-haul rollouts, automotive LiDAR attach rates, infrared medical probe shipments, compound-semiconductor wafer output, and currency-adjusted ASP erosion curves. A multivariate regression that links these drivers to historical market values feeds an ARIMA overlay for short-term shocks, while scenario analysis replaces any missing regional series.

Data Validation & Update Cycle

Every iteration passes a three-layer review that screens anomalies, benchmarks totals against external optical-device indices, and secures sign-off by a senior analyst. Reports refresh once a year, and we trigger mid-cycle updates if policy shifts, material shortages, or major M&A events materially alter the baseline. Clients thus receive numbers that mirror the latest industry pulse.

Why Mordor's Photodiode Sensors Baseline Earns Global Trust

Published estimates often diverge because firms choose different device families, currency bases, and forecast cadences before translating volumes into revenue.

Key gap drivers include whether combo modules are counted, how fast ASP compression is assumed, and if telecom-grade InGaAs diodes are grouped with consumer-grade silicon parts. Mordor's model captures the full sensor module spectrum, applies live exchange rates, and refreshes annually, while several other publishers freeze inputs for longer stretches or skip module-level reconciliation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.77 Billion (2025) | Mordor Intelligence | - |

| USD 783.5 Million (2024) | Regional Consultancy A | narrower scope omits telecom back-haul devices and holds ASP static |

| USD 780 Million (2024) | Trade Journal B | derives totals from historic shipment curves only, no material mix adjustment |

| USD 814.5 Million (2025) | Global Consultancy C | excludes integrated ambient-light modules and applies single-country inflation factors |

The comparison shows that when scope breadth, live ASP tracking, and yearly refresh cycles are harmonized, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can retrace to clear variables and reproducible steps.

Key Questions Answered in the Report

What is the current value of the photodiode sensors market?

The photodiode sensors market is valued at USD 825.82 million in 2026 and is projected to reach USD 1,164.64 million by 2031.

Which region leads the photodiode sensors market?

Asia-Pacific holds 45.55% revenue share owing to concentrated semiconductor manufacturing and aggressive 5G deployments.

Which segment grows fastest within the photodiode sensors market?

Automotive LiDAR applications show the highest CAGR at 8.62% during 2026-2031.

What material dominates photodiode production today?

Silicon remains dominant with 57.38% market share, though silicon-germanium and InGaAs are gaining ground for infrared performance.

How are supply chain risks affecting photodiode availability?

Export restrictions on gallium and indium create pricing and lead-time volatility, pushing manufacturers to explore alternative materials.

What is the forecast CAGR for the overall photodiode sensors market?

The market is expected to grow at a 7.12% CAGR between 2026 and 2031.

Page last updated on: