Phoropters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

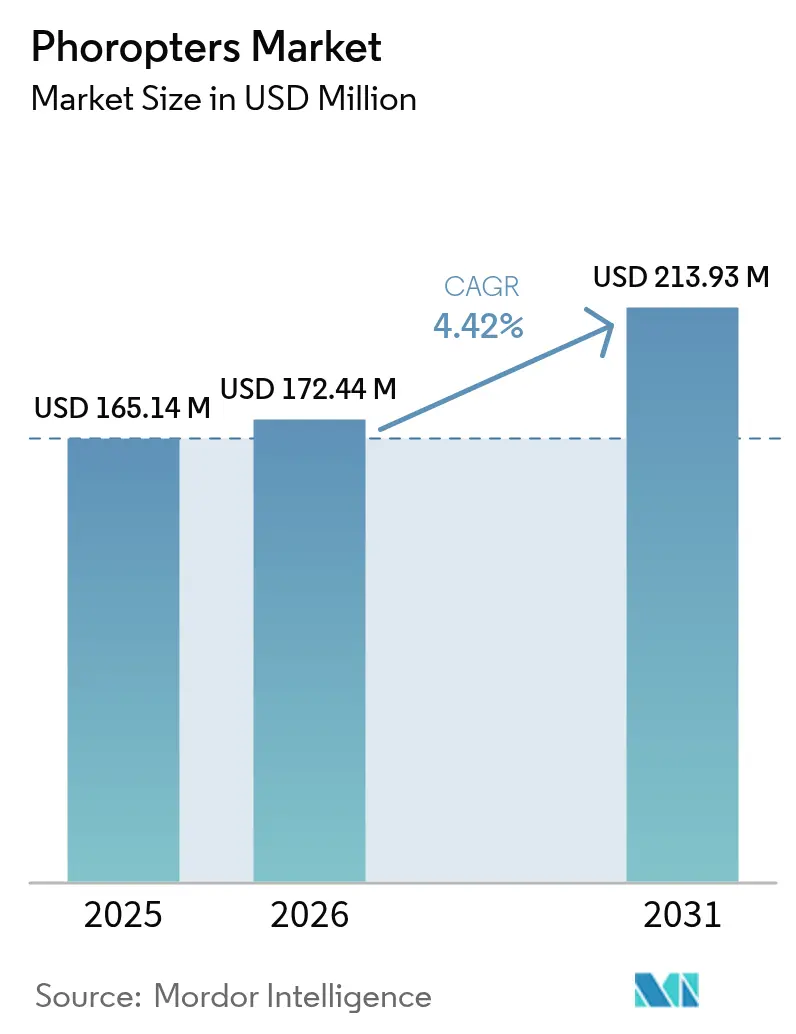

| Market Size (2026) | USD 172.44 Million |

| Market Size (2031) | USD 213.93 Million |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

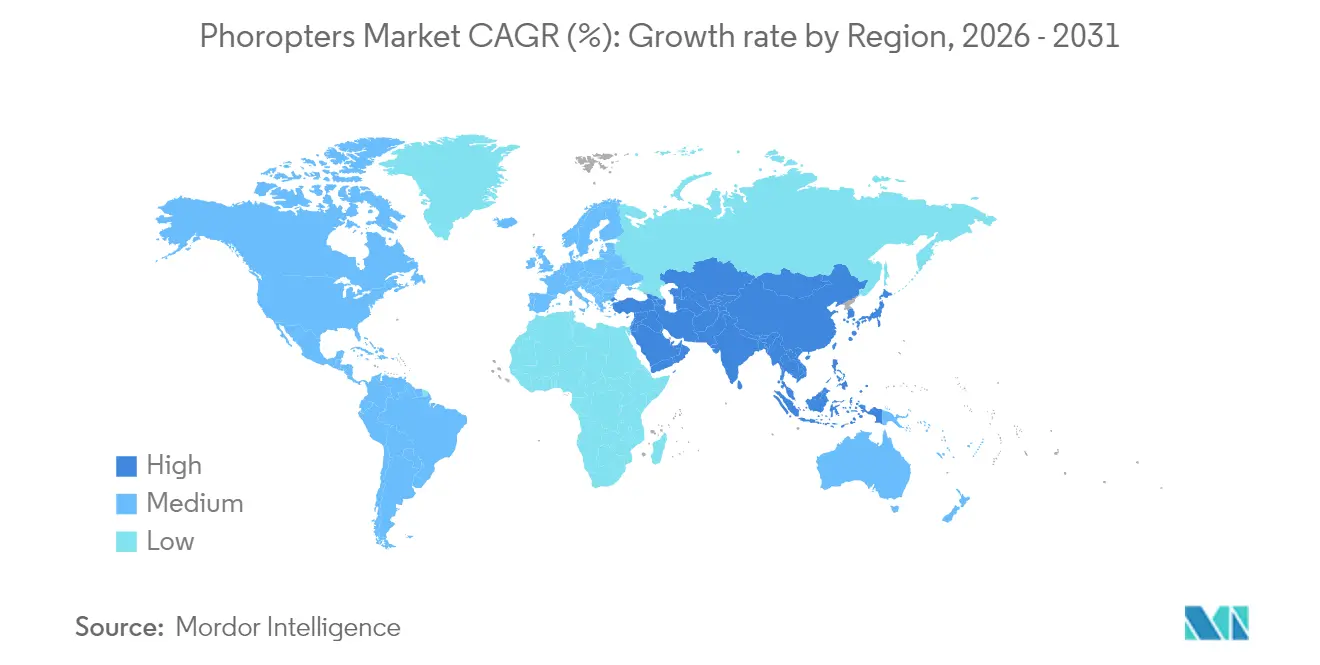

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

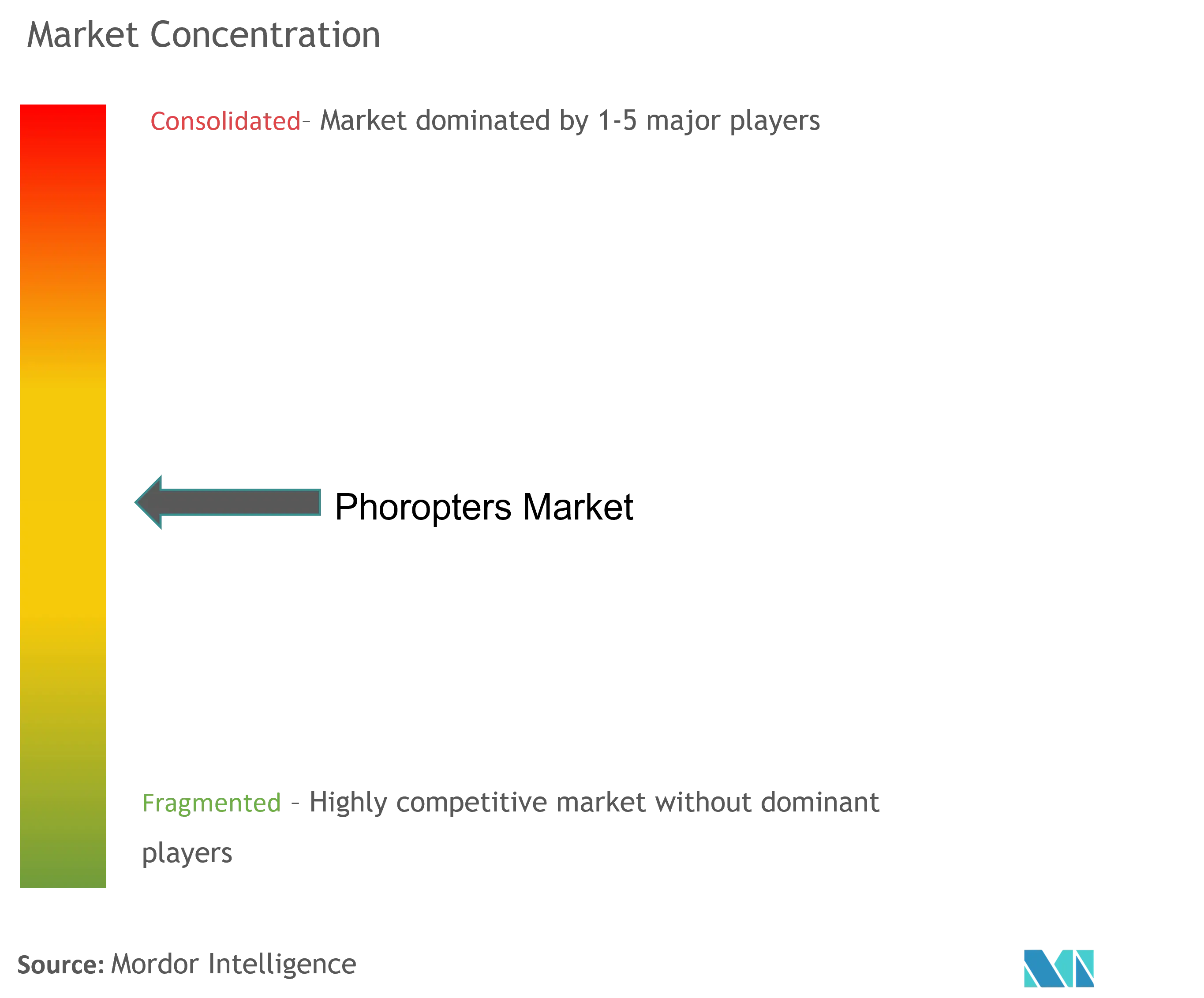

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Phoropters Market Analysis by Mordor Intelligence

The phoropter market size is expected to grow from USD 165.14 million in 2025 to USD 172.44 million in 2026 and is forecast to reach USD 213.93 million by 2031 at 4.42% CAGR over 2026-2031. Demand stems from rising refractive-error prevalence, rapid aging, and the switch from manual refraction to connected diagnostic workflows. Automated models lower examination time, integrate with electronic health records, and support technician-led service models, while traditional manual units still dominate in many independent clinics. Optical retail chains standardize high-volume testing, hospitals upgrade to digital platforms that interface with surgical planning software, and online procurement channels gain ground as specification transparency improves. Vendors now bundle software, analytics, and remote-support contracts, repositioning the phoropter market from a hardware purchase to a workflow solution.

Key Report Takeaways

- By product type, manual systems led with 53.78% of phoropter market share in 2025, while digital and automated units are expanding at a 5.21% CAGR through 2031.

- By end user, hospitals and eye clinics held 46.02% revenue share in 2025; optical retail chains show the fastest trajectory at 5.68% CAGR to 2031.

- By distribution channel, direct sales accounted for 49.65% of the phoropter market size in 2025, whereas online commerce is advancing at a 6.19% CAGR.

- By geography, North America contributed 38.21% revenue in 2025, but Asia-Pacific is scaling at a 6.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Phoropters Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of refractive errors | +1.2% | Global, with concentration in Asia-Pacific | Long term (≥ 4 years) |

| Shift toward digital & automated refraction systems | +0.9% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Aging population demanding frequent eye exams | +0.8% | Global, particularly developed markets | Long term (≥ 4 years) |

| EMR-integrated digital phoropters boost throughput | +0.6% | North America & Europe | Short term (≤ 2 years) |

| Tele-optometry & retail chain upgrades | +0.4% | Global, with early adoption in urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of refractive errors

Myopia now affects 80-90% of high-school graduates in several East-Asian economies, with 10-20% at risk of pathologic complications that need frequent monitoring [1]Source: Emma Liu, “Asian High-School Myopia Now Tops 90%,” BioSpectrum Asia, biospectrumasia.com . COVID-19 lockdowns magnified this burden; Hong Kong documented a 2.5-fold jump in new childhood myopia cases, cementing long-term demand for school-based screening. Outside East Asia, Iranian adults aged 60 and above show 31.65% myopia and 45.36% hyperopia, underscoring that uncorrected refractive error spans age groups[2]Source: Roya Ziaei, “Refractive Error Prevalence in Iranian Seniors,” BMC Ophthalmology, bmcophthalmol.biomedcentral.com . Such demographic and lifestyle shifts keep phoropters central to primary eye care, elevating them from elective tools to public-health necessities.

Shift toward digital & automated refraction systems

Automated binocular units completed tests in 171 seconds versus 190 seconds for legacy digital devices while maintaining accuracy parity. University of Arizona researchers produced a 20-second auto-phoropter that removes subjective answers, which addresses language barriers and standardizes results. Such speed improvements support high-throughput retail chains and rural tele-optometry hubs. When paired with software that auto-uploads refraction data to patient records, the phoropter market aligns with hospital digitization agendas and national e-health mandates.

Aging population demanding frequent eye exams

Presbyopia affects nearly every individual over 50 years, while corneal astigmatism above 1.00 D is present in 44.2% of cataract candidates. Frequent objective testing is vital for surgical planning and systemic disease detection because ophthalmic findings correlate with frailty biomarkers. This predictable, recurring requirement insulates the phoropter market from cyclical economic swings and favors premium models that interface with diagnostic imaging suites.

EMR-integrated digital phoropters boost throughput

Ophthalmology-specific electronic records demand seamless data import in formats absent from generic health IT. The U.S. Technology-based Eye Care Services program served over 70,000 veterans through remote consultations enabled by standardized capture protocols. Carl Zeiss Meditec’s VisioGen suite merges communication tools with auto-refraction upload to trim chair time. Clinics quantify return on investment through reduced transcription errors and faster patient flow, accelerating replacement cycles.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of digital phoropters | -0.8% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Limited reimbursement for advanced eye-exam devices | -0.6% | North America & Europe | Medium term (2-4 years) |

| Shortage of skilled refraction personnel | -0.5% | Global, acute in rural areas | Long term (≥ 4 years) |

| Booming second-hand equipment market | -0.3% | Developing countries, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront cost of digital phoropters

Premium automated units stretch capital budgets, especially for independent optometrists in regions lacking equipment financing. Refurbished devices resolve 43.5% of medical-equipment shortages in developing economies, underscoring cost sensitivity. Until manufacturing scale and local assembly compress prices, adoption splits: high-volume chains upgrade rapidly while smaller clinics hold to manual devices.

Limited reimbursement for advanced eye-exam devices

Payer policies such as Horizon Blue Cross Blue Shield reimburse CPT Code 92015 only for disease-related refractions, not routine screenings. Providers therefore fund equipment amortization through out-of-pocket fees, suppressing upgrade appetite. Evidence demonstrating preventive savings may spur policy change, yet near-term adoption remains uneven across health systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type – Manual Persistence, Digital Momentum

The phoropter market size for manual units stood at USD 88.81 million in 2025 and still accounted for 53.78 % of revenue. Long product lives and lower prices appeal to small clinics, but digital and automated alternatives rise at 5.21 % CAGR through 2031. Automated systems shave consultation time while exporting refraction data directly to cloud records. Their technician-friendly workflow helps mitigate the forecast 30 % shortfall in ophthalmologists by 2035. As regulatory guidance on objective testing solidifies, clinics will gradually trade artistry for repeatable analytics, positioning digital lines to erode manual dominance beyond 2030.

Manual devices will remain viable in refurbish-oriented markets where funding constraints prevail. Emerging subscription models that bundle software, maintenance, and periodic upgrades could accelerate retirement of purely mechanical systems. Manufacturers that retrofit existing frames with sensor modules might capture value from practices unwilling to purchase full replacements.

By End User – Retail Chains Lift Volume

Hospitals and specialty eye clinics drove 46.02 % of 2025 revenue owing to comprehensive care pathways. Their procurement cycles hinge on surgical throughput and accreditation audits that favor integrated platforms. In contrast, optical retail networks expand at 5.68 % CAGR because consumer walk-ins favor one-stop service with transparent pricing. Digital phoropters enable standardized protocols, shorter queues, and store-to-store consistency critical for franchisors.

Independent optometrists confront rising lease expenses and reimbursement ceilings that compress margins. Many respond by diversifying into dry-eye therapy or low-vision aids rather than upgrading refraction hardware. Academic research centers, though small in revenue terms, pioneer validation studies that speed regulatory approvals, thereby influencing market messaging and design priorities.

By Distribution Channel – Digital Commerce Gains Traction

Direct manufacturer deals maintained 49.65 % of 2025 revenue because customers depend on installation, calibration, and training. However, online procurement platforms post 6.19 % CAGR by lowering search costs and publishing transparent specification comparators. Standardized automated phoropters travel well and need minimal onsite setup, suiting courier delivery.

Dealer networks remain essential in emerging economies where import permits, after-sales servicing, and language support shape purchase decisions. Hybrid sales strategies—online lead generation with local service partners—have emerged to blend margin efficiency with hands-on support. As more providers pivot to multi-clinic ownership, centralized digital procurement offices will further legitimize e-commerce channels.

Geography Analysis

North America generated 38.21 % of global revenue in 2025, underpinned by high private-insurance penetration and robust capital spending. United States clinics upgrade frequently to comply with data-security rules and to gain reimbursement advantages for documented outcomes. FDA Class I and Class II device pathways define clear testing benchmarks, which accelerates commercialization timelines. Workforce shortages, with 60 % of optometric practices citing vacant positions, intensify the pivot to technician-run sessions that rely on automated phoropters. The proposed tariff hikes on ophthalmic imports could favor domestic assemblers but may inflate upgrade costs for smaller practices.

Europe presents a mature yet cost-constrained profile. Universal coverage encourages regular eye screenings, supporting steady phoropter replacement cycles. However, single-payer reimbursement rates pressure clinics to justify premium equipment through demonstrated workflow savings. Stringent CE-marking rules advantage incumbent manufacturers with established quality management systems. Cross-border telemedicine pilots in Scandinavia reveal that integrated digital phoropters can serve remote islands effectively, potentially inspiring broader adoption.

Asia-Pacific is the fastest-growing territory at 6.84 % CAGR. Public-health campaigns confront a myopia epidemic where up to 90 % of East-Asian teenagers need corrective lenses. Governments in China, Singapore, and South Korea subsidize school screening programs, spurring bulk procurement of portable automated units. Countries upgrading universal coverage, such as Thailand’s outpatient scheme expansion, fund provincial clinics that require low-maintenance phoropters. Domestic optical-component suppliers shorten lead times and compress costs, enabling local assembly that competes with imported brands.

South America shows fragmented uptake. Urban centers in Brazil and Colombia integrate digital phoropters into chain stores, yet rural areas still rely on manual devices due to constrained budgets and intermittent power. Non-profit vision missions bolster demand for portable units that can survive field conditions, indirectly fostering brand recognition among local practitioners. Middle East and Africa record sporadic hospital buys tied to donor-funded infrastructure projects; refurbished manual equipment dominates private-clinic inventories. Government import-duty relief on essential medical devices, recently enacted in Kenya, may lift shipments of entry-level automated models.

Competitive Landscape

The phoropter market houses a mix of established optical giants and specialist disruptors. Carl Zeiss Meditec, Topcon, and NIDEK reinforce positions through vertical integration. Zeiss consolidated seven optical divisions into a dedicated photonics unit and acquired Dutch Ophthalmic Research Center, enabling synergies from diagnostics to surgery. EssilorLuxottica secured an 80 % stake in Heidelberg Engineering, extending reach from lenses to OCT diagnostics. Such moves bundle refraction with imaging and therapeutic workflows, raising switching barriers.

Innovations differentiate: Zeiss unveiled VisioGen, an AI-driven clinic-operations aid; Reichert pushes Bluetooth-enabled devices that slot into cloud platforms; Visionix markets multifocal end-to-end exam lanes adaptable to space-constrained retail outlets.

Disruptors reshape competitive dynamics. iCRx claims a 60-second objective eye exam, challenging the traditional 15-minute subjective model. University of Arizona’s 20-second portable prototype targets humanitarian deployments and primary-care offices. These entrants weaponize speed, ease of use, and lower unit costs. Incumbents respond by embedding analytics, remote calibration, and subscription firmware. Strategic alliances with EMR vendors and tele-health platforms become decisive because buyers increasingly rate interoperability equal to optical quality.

Phoropters Industry Leaders

Marco

Rexxam Co., Ltd.

Reichert, Inc.

Carl Zeiss AG

Topcon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Carl Zeiss launched the Research Data Platform, an AI cloud system built with Boehringer Ingelheim to advance chronic retinal disease studies.

- December 2024: EssilorLuxottica acquired Espansione Group, expanding into non-invasive eye-therapy devices

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the phoropters market as the annual revenue generated from new manual and digital (software-enabled) ophthalmic instruments that house interchangeable lenses, cylinders, and prisms for subjective refraction during an eye exam. The unit sits between the practitioner and the patient, letting optometrists fine-tune spherical, cylindrical, and axis corrections in real time, which then form the basis of a spectacle or contact-lens prescription.

Scope note, Exclusions: Devices that perform only objective refraction, such as standalone autorefractors and wavefront aberrometers, plus refurbished or rental units are outside the present scope.

Segmentation Overview

- By Product Type (Value)

- Manual Phoropters

- Digital / Automated Phoropters

- By End User (Value)

- Hospitals & Eye Clinics

- Optical Retail Chains

- Independent Optometrists

- Ambulatory Surgical Centers

- Academic & Research Institutes

- By Distribution Channel (Value)

- Direct Sales

- Distributor / Dealer Network

- Online Sales

- By Region (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We complemented desk work with structured interviews and short surveys involving practicing optometrists, biomedical engineers at device manufacturers, procurement heads in multi-site eye hospitals, and senior distributors across North America, Europe, Asia-Pacific, and the Middle East and Africa. Conversations verified phoropter utilization rates, average lifespans, price dispersion, and the pace at which clinics shift toward digital interfaces, thereby anchoring our assumptions.

Desk Research

Our analysts first map the demand pool through openly available, high-credibility sources such as the WHO Vision Impairment database, United Nations population aging tables, national blindness and eye-health surveys, and import-export shipment logs accessed via Volza. Company 10-Ks, ophthalmic trade-association yearbooks, peer-reviewed journals on refraction techniques, and patent families retrieved from Questel help us benchmark technology adoption rates and average selling prices.

Country-level optical retail counts, hospital infrastructure data, and reimbursement tariffs are subsequently gathered from ministries of health and statistical offices; these provide boundary conditions for installed-base growth and replacement cycles. D&B Hoovers and Dow Jones Factiva fill remaining financial or news gaps. The list above is illustrative, not exhaustive; many other secondary sources fed into data gathering, validation, and clarification.

Market-Sizing and Forecasting

A blended top-down, bottom-up construct underpins the model. We start with refractive-error prevalence, optometrist density, and average annual eye-exam volumes to approximate potential demand; installed-base counts and five-year replacement curves translate that demand into unit sales, which are then multiplied by country-specific ASPs.

Supplier roll-ups and channel checks serve as reasonableness tests. Key variables include aging population growth, per-capita healthcare spend, clinic digitization rates, typical four-to-seven-year replacement cycles, and the rising share of automated phoropters. Forecasts are produced through multivariate regression that links those drivers to historical shipment data, with scenario analysis around pricing and regulatory shifts to bound error margins.

Data Validation and Update Cycle

Every output passes two analyst reviews, variance checks against third-party trade statistics, and follow-up calls where anomalies persist. Mordor refreshes the data annually and issues interim updates when policy, currency, or technology shocks materially alter market trajectory.

Why Mordor's Phoropters Baseline Numbers Stand Up to Scrutiny

Published estimates often vary because firms diverge on product mix, ASP inflation, and replacement timelines. Our disciplined scope selection, yearly refresh cadence, and driver-level transparency minimize such drift.

Key gap drivers include differing inclusion of autorefractors, use of list instead of transaction prices, assumed three-year versus seven-year lifecycles, and single-region extrapolations without age-adjusted prevalence multipliers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 165.14 M (2025) | Mordor Intelligence | - |

| USD 153.90 M (2024) | Global Consultancy A | ignores hospital bulk-discount pricing; shorter forecast refresh |

| USD 161.86 M (2024) | Trade Journal B | treats refurbished units as new sales; limited country coverage |

| USD 75.90 M (2024) | Industry Association C | excludes digital phoropters, leading to undercount |

The comparison shows that, while headline numbers differ, Mordor's baseline balances realistic ASPs, complete product coverage, and globally consistent age-adjusted demand drivers, making it a dependable compass for strategic planning.

Key Questions Answered in the Report

What is driving the global shift toward digital phoropters?

Faster exam times, direct EMR integration, and the ability to delegate testing to technicians are the core catalysts. Automated units complete refractions in as little as 171 seconds while exporting results straight to patient records.

How large is the current phoropters-market and how fast is it growing?

The phoropters-market size stands at USD 172.44 million in 2026 and will expand to USD 213.93 million by 2031, reflecting a 4.42% CAGR.

Why is Asia-Pacific considered the fastest-growing region?

A myopia prevalence of up to 90 % among East-Asian teenagers and government-funded school screening programs push the region to a 6.84% CAGR

What limits adoption of premium digital phoropters in smaller clinics?

High upfront cost and limited insurance reimbursement mean independent practitioners often cannot recover investments quickly, especially in emerging markets where refurbished manual units are readily available.

Which market segment is expanding the quickest?

Optical retail chains grow at 5.68% CAGR because consumer demand for fast, transparent, in-store eye exams aligns with technician-operated digital phoropters.

Page last updated on: