Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

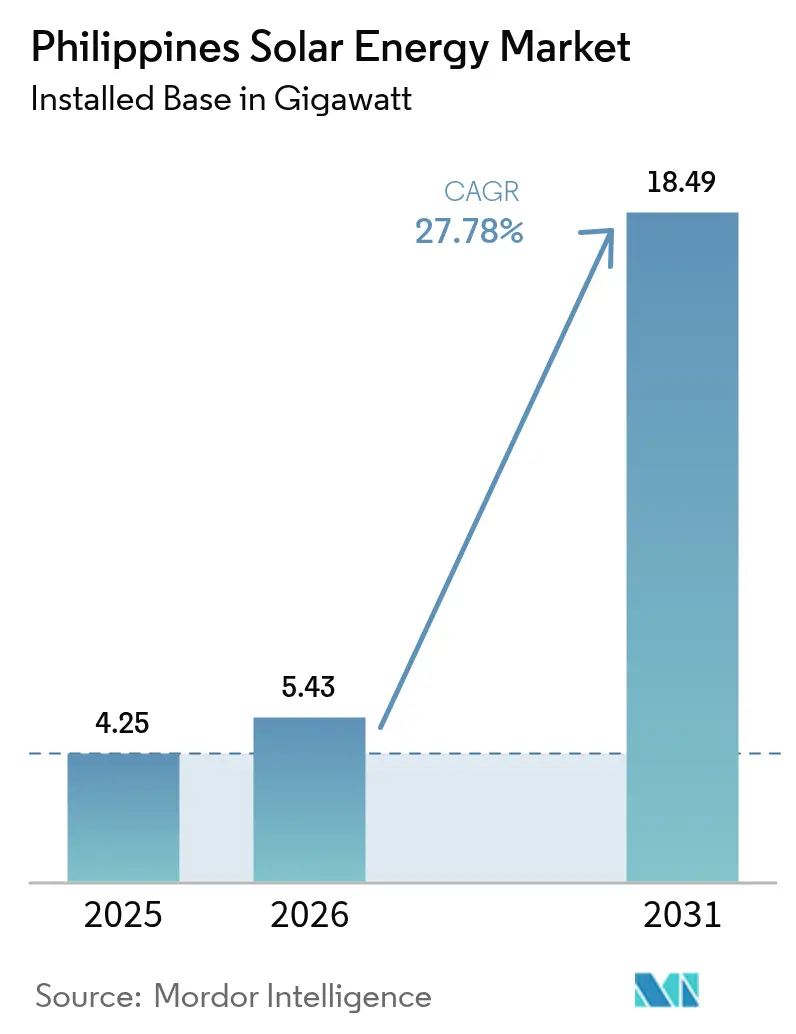

| Base Year Market Size (2025) | 4.25 gigawatt |

| Market Volume (2026) | 5.43 gigawatt |

| Market Volume (2031) | 18.49 gigawatt |

| Growth Rate (2026 - 2031) | 27.78% CAGR |

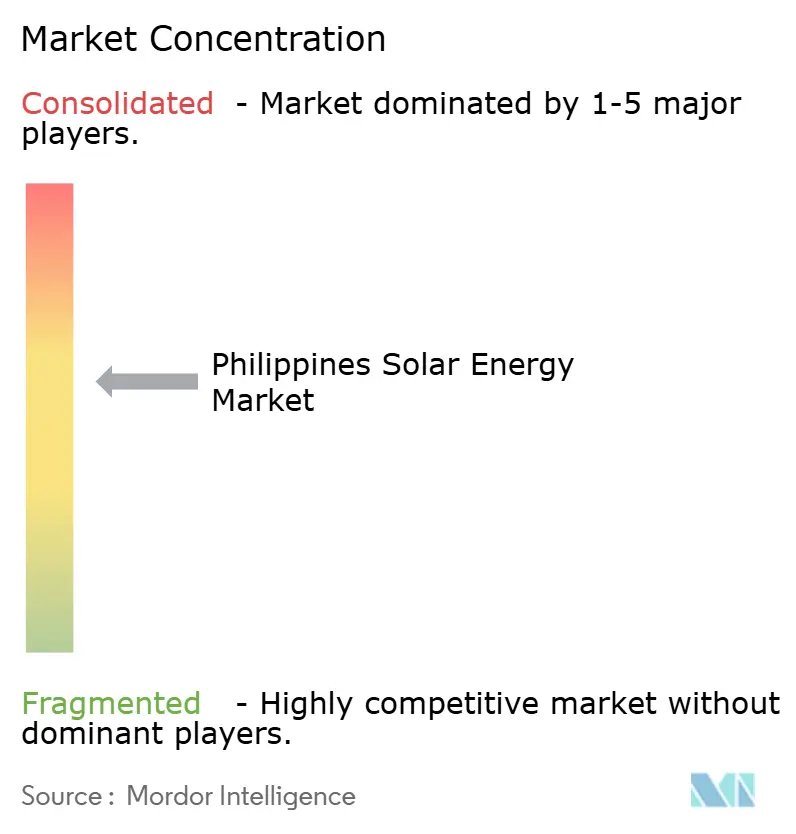

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Solar Energy Market Analysis by Mordor Intelligence

The Philippines Solar Energy Market size is expected to grow from 4.25 gigawatt in 2025 to 5.43 gigawatt in 2026 and is forecast to reach 18.49 gigawatt by 2031 at 27.78% CAGR over 2026-2031. Declining module and balance-of-system costs have driven the levelized cost of utility-scale solar down to USD 0.044 per kWh, making new photovoltaic capacity the least-cost choice for meeting baseload demand. Strong demand from hyperscale data centers and business-process outsourcing firms is accelerating hybrid solar-plus-storage projects that guarantee 24/7 clean power. Meanwhile, the Department of Energy’s Green Energy Auction Program (GEAP) has awarded 10.2 GW of capacity in its fourth round, pushing the national development pipeline above 36 GW. Floating solar on Laguna Lake and irrigation reservoirs is emerging as a land-neutral alternative, and reforms that lifted the net-metering ceiling from 100 kW to 1 MW are expected to unlock commercial and industrial rooftops.

Key Report Takeaways

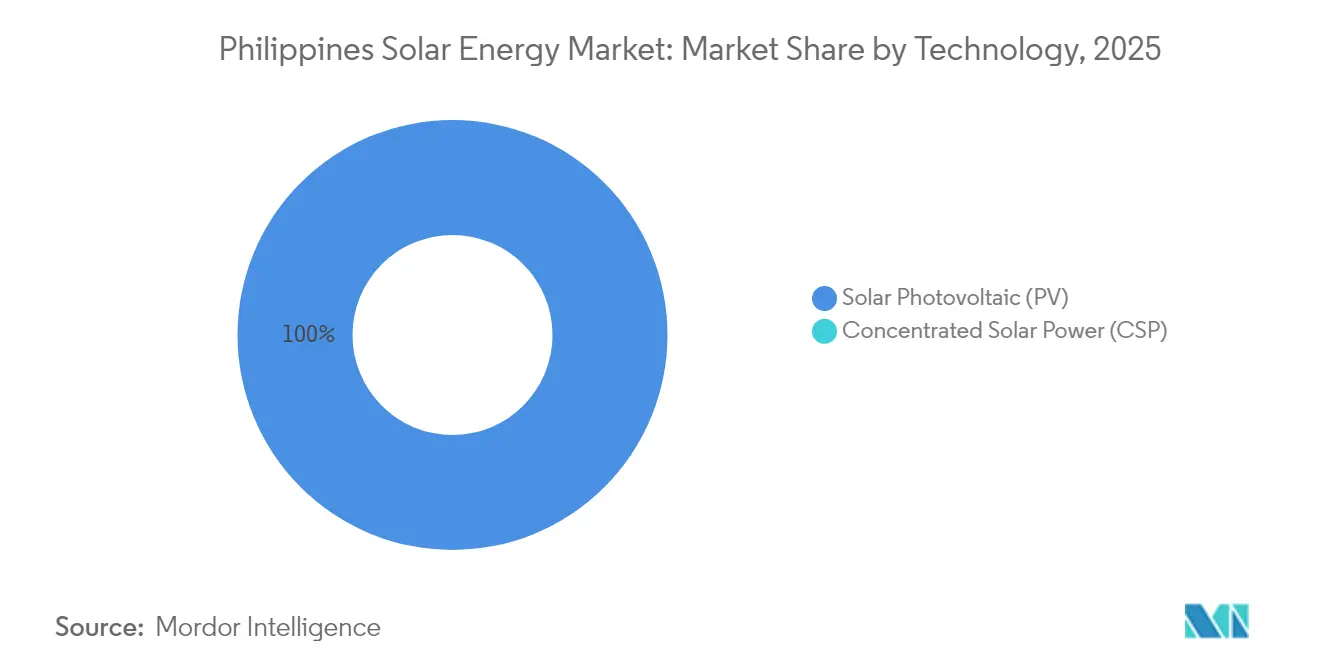

- By technology, solar photovoltaic captured 100.00% of 2025 capacity, while concentrated solar power remained absent due to land and climate constraints.

- By grid type, on-grid installations held 97.15% of capacity in 2025; off-grid systems will register the fastest 31.15% CAGR through 2031.

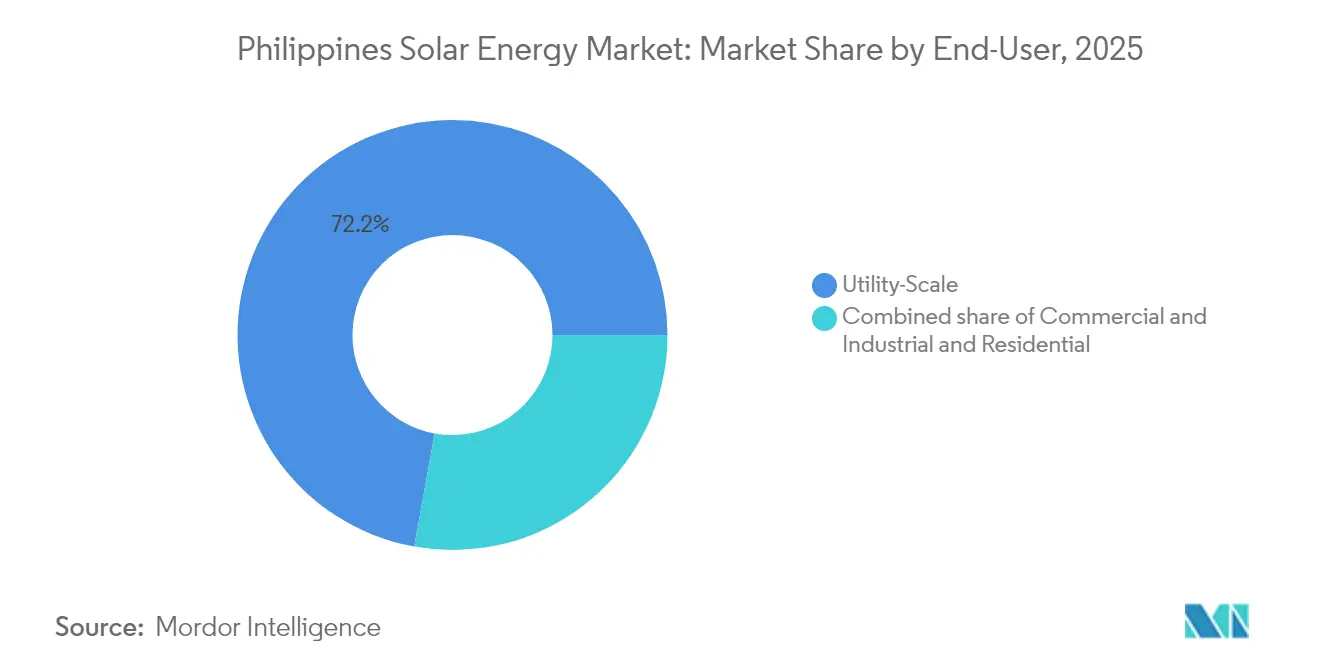

- By end-user, utility-scale projects commanded 72.15% of 2025 capacity, whereas residential rooftops are forecast to expand at a 31.60% CAGR to 2031.

- Citicore, ACEN, and Aboitiz Power secured the bulk of GEAP-4 awards, and Trina Solar’s 3 GW module partnership with Citicore highlights equipment supply consolidation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Philippines Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decline in PV module & BOS costs | 6.20% | Nationwide, led by Luzon corridors | Short term (≤ 2 years) |

| Green energy auctions unlocking ≥1 GW yearly | 8.50% | Luzon & Visayas | Medium term (2-4 years) |

| Corporate PPAs from hyperscalers & BPOs | 5.10% | Metro Manila, Cavite, Laguna, Cebu | Medium term (2-4 years) |

| Net-metering reform raising cap to 1 MW | 3.80% | Urban residential & C&I clusters | Long term (≥ 4 years) |

| Floating-solar buildout on reservoirs | 2.70% | Laguna Lake, Mindanao impoundments | Long term (≥ 4 years) |

| ASEAN carbon-border adjustment pressure | 2.40% | Export zones in Cavite, Laguna, Bataan, Cebu | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in PV Module & BOS Costs

Global utility-scale solar leveledized costs fell to USD 0.044 /kWh in 2023, a 90% drop since 2010, slashing capital outlays for every Philippine project.[1]International Renewable Energy Agency, “Renewable Power Generation Costs in 2023,” irena.orgLocal firms now receive price quotes under USD 0.19 /W for Tier-1 modules, widening project margins and spurring Sol-Go to locate assembly lines in the country. Balance-of-system spending, historically 75% of Asian solar budgets, is becoming a new domestic value-add avenue, with metal frame, inverter, and cable manufacturers repositioning for export.[2]Institute for Energy Economics and Financial Analysis, “Asia’s Solar BOS Cost Trends,” ieefa.org This cost trajectory raises the competitive standing of the Philippines' solar energy market against imported LNG and legacy coal, accelerating utility procurement and corporate PPAs. Over the medium term, it also underpins a nascent local manufacturing base that could supply 3-5 GW of modules annually by 2030, further anchoring the supply chain.

Green Energy Auctions (GEAP) Unlocking ≥1 GW Solar Pipeline from 2025

The Department of Energy's competitive tender model replaces static feed-in tariffs with price discovery, awarding 1 GW of solar in its inaugural round and setting a 9,378 MW target for the fourth auction that includes solar-storage hybrids. Developer appetite remains robust, GEA-3 drew 7,500 MW of solar bids for a 4,650 MW cap, compressing tariffs and ensuring 20-year off-take certainty. Auction-linked PPAs lower financing risk, enabling lenders to trim spreads and developers to stretch capacity factors with storage add-ons. The integration of mandatory battery systems from GEA-4 onwards signals policy maturation toward grid-friendly renewables that can address midday curtailment. Collectively, auctions move the Philippines' solar energy market toward predictable build-out cycles and transparent cost benchmarks.

Corporate PPAs by Hyperscalers & BPOs Demanding 24/7 Clean Power

Rising data-center footprints and BPO campuses are shifting demand to hourly hourly-matched renewable supply. Digital Edge secured hydro-based power for its NARRA 1 facility, while the USD 2.7 billion Narra Technology Park pledges 100% clean electricity within five years. First Gen has lined up 180 MW of data-center PPAs, illustrating the scale of private offtake outside utilities. Contracts now embed real-time carbon accounting and require storage or hybrid portfolios to assure continuous green coverage. This has catalyzed niche integrators capable of blending solar, wind, hydro, and batteries for bespoke load profiles, adding depth to the Philippines' solar energy market.

DOE Net-Metering Reform Lifting 100 kW Cap to 1 MW (2024)

Expanding net-metering unlocks commercial rooftops previously constrained by a residential-sized ceiling. Aboitiz Power pegs rooftop solar headroom at 13 GW, while a study of 139 factories found 132 becoming bankable once the cap moved to 1 MW, totaling 1,035 MWp of capacity. The Senate is considering full removal of size limits, underscoring bipartisan support. Coupled with rising grid tariffs and diminishing panel prices, payback periods for warehouse or mall installations fall below five years, igniting fresh momentum in the Philippines' solar energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak grid capacity in Visayas-Mindanao corridor | -4.30% | Visayas & Mindanao | Medium term (2-4 years) |

| High financing costs vs. Vietnam & Malaysia (≥9% WACC) | -3.60% | Nationwide | Short term (≤ 2 years) |

| Land-acquisition disputes under CARP | -2.10% | Rural Luzon & Visayas | Long term (≥ 4 years) |

| Typhoon-related O&M disruptions | -1.80% | Coastal and island sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Weak Grid Capacity in Visayas-Mindanao Corridor

Only 6 of 16 priority transmission projects were completed by 2023, delaying the PHP 52 billion Mindanao-Visayas backbone by three years.[3]ScienceDirect, “Transmission Delays in Visayas-Mindanao,” sciencedirect.comBottlenecks restrict solar additions south of Luzon, compelling developers to cluster where interconnection is available and leaving ample irradiance unexploited. The Transmission Development Plan 2022-2040 maps expansions, but execution lags grid demand. Until high-voltage lines catch up, project pipelines will stay skewed toward Luzon.

High Financing Costs vs Vietnam & Malaysia (≥9% WACC)

The weighted average cost of capital for Philippine power projects stands above 9%, versus sub-8% in Malaysia and Thailand. Transmission operator NGCP carries an approved 15.04% rate of return, inflating developer hurdle rates and limiting solar-plus-storage ventures. Sovereign risk premiums, currency volatility, and shallow green bond markets keep spreads elevated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Dominance, CSP Absent

Solar photovoltaic accounted for the entire 2025 installation base, reinforcing a Philippines solar energy market share of 100.00%. High-efficiency n-type i-TOPCon and bifacial modules lift output and cut land needs, helping the Philippines' solar energy market size for PV rise at a 27.78% CAGR. CSP remains commercially non-viable due to land scarcity and typhoons, and the DOE master plan allocates no targets for the technology.

The market's equipment shift toward string inverters and hybrid PV-plus-storage architectures improves uptime and meets 24/7 procurement clauses in corporate PPAs. Terra Solar's 3.5 GW PV and 4.5 GWh storage confirm this hybrid trend, locking in long-duration supply contracts with hyperscalers.

By Grid Type: On-Grid Leads, Off-Grid Accelerates

On-grid projects held 97.15% of 2025 installations, reflecting GEAP awards and corporate rooftop growth near Luzon load centers. Off-grid systems, however, will log a 31.15% CAGR, aided by PHP 5 billion in rural electrification grants that lower costs for mini-grids serving remote barangays. On-grid scale keeps installed costs near USD 0.80 per watt, while off-grid hybrids remain upward of USD 1.20 per watt yet still undercut diesel generation.

Policy enables cross-subsidy: GEAP guarantees offtake for on-grid plants, and cost-plus tariffs de-risk off-grid service providers. Although the Philippines' solar energy industry treats off-grid additions as small in absolute terms, they are critical for universal electrification.

By End-User: Utility-Scale Dominates, Residential Surges

Utility-scale assets captured 72.15% of 2025 capacity, securing economies of scale and cheaper finance. Residential rooftops, supported by the expanded 1 MW net-metering cap, are forecast to outpace all categories at a 31.60% CAGR. Commercial and industrial roofs occupy a middle tier, motivated by tariff hedging and ESG commitments. Upfront cost and financing access remain the main barriers slowing residential growth despite a sub-five-year payback.

Geography Analysis

Luzon commands roughly 78.40% of national technical potential and most commissioned capacity thanks to denser transmission, industrial demand, and auction focus. Flagship builds such as the Philippines' solar energy market-size-defining 3.5 GW Terra Solar and ACEN’s 1,120 MW floating-solar program underline the region’s dominance. Transmission reinforcement, while ongoing, is better funded here than elsewhere.

Visayas, with around 14.60% potential, continues to suffer curtailment risk because NGCP delays hold back substation and line upgrades. Aboitiz Power’s 173 MWp Calatrava plant illustrates that well-capitalized sponsors can co-invest in grid upgrades, though many smaller developers cannot absorb the extra costs. Cebu’s export-led economy fuels PPA demand, yet projects face queue times that inflate financial models.

Mindanao captures only about 7.00% of the potential and features the weakest grid. Electrification funds are channeling into solar mini-grids for Sulu, Tawi-Tawi, and Palawan, shifting market focus there from utility-scale to distributed hybrids. Grid-scale projects wait for the Visayas-Mindanao interconnection upgrade now slated for post-2027, tempering near-term additions.

Competitive Landscape

The Philippines' solar energy industry shows moderate fragmentation, with the top five players together controlling just under 40% of installed capacity in 2024. ACEN Corp leads with 7 GW in service or late-stage development, aiming for 20 GW by 2030, and recently consolidated Islasol to solidify its presence in Visayas. Solar Philippines, via SP New Energy Corp, focuses on ultra-large farms, including Terra Solar, backed by Actis's USD 600 million investment for a 40% stake, underscoring foreign appetite for bankable assets. Vena Energy accelerated expansion through a 550 MW greenfield commitment, reinforcing its regional strategy.

Strategically, domestic utilities leverage vertical integration to combine generation, distribution, and retail offers. Meralco PowerGen's Terra Solar 2 proposes a second giga-scale plant in Batangas, pairing solar with multi-hour storage to defer grid upgrades. Joint ventures such as Citicore-San Miguel's 153.5 MW Bataan farm illustrate risk sharing: local conglomerates supply land and permits, while renewable specialists contribute EPC and O&M expertise. New entrants eye floating solar, rooftop leasing, and manufacturing localization as white-space plays, further broadening the competitive fabric of the Philippines' solar energy market.

M&A remains active: Acciona's entry via the Daanbantayan PPP, PATRIZIA's USD 100 million fund placement, and multiple BESS groundbreakings by Aboitiz Power reflect deal diversity across generation and storage verticals. With auctions providing visibility and corporate PPAs deepening, developer portfolios increasingly bundle solar, wind, hydro, and batteries into integrated proposals.

Philippines Solar Energy Industry Leaders

Solar Philippines Power Project Holdings

ACEN Corp.

Vena Energy

Citicore Power Inc.

Aboitiz Power Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Actis closed USD 600 million for a 40% share in Terra Solar Philippines, marking the country’s largest greenfield FDI.

- March 2025: Acciona Energia began construction of the 176 MW Daanbantayan Solar Plant in Cebu under the green lane PPP scheme.

- January 2025: Citicore and San Miguel launched a 153.5 MW Bataan solar project with a PHP 6 billion investment, aiming for 2026 completion.

Philippines Solar Energy Market Report Scope

Solar energy is heat and radiant light from the Sun that can be harnessed with technologies such as solar power (used to generate electricity) and solar thermal energy (used for applications such as water heating). The market sizing and forecasts for each segment have been done based on installed capacity (GW). The Philippines Solar Energy Market report includes:

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

How fast is capacity expected to grow in the Philippines solar energy market?

Installed capacity is projected to rise from 5.43 GW in 2026 to 18.49 GW by 2031, advancing at a 27.78% CAGR.

Which technology dominates new builds?

Photovoltaic systems hold 100.00% of current installations, and no concentrated solar power projects are in the pipeline.

What share do utility-scale projects hold today?

Utility-scale plants account for 72.15% of 2025 capacity, reflecting auction-driven growth and large corporate PPAs.

Why is floating solar gaining traction?

Reservoir-based arrays avoid land-acquisition delays, deliver up to 10% higher yields, and have 2.6 GW of announced capacity led by ACEN and Blueleaf Energy.

What challenges slow rural adoption?

High upfront costs, limited consumer financing, and interconnection delays limit residential rooftop uptake despite a four-year payback.

How do financing conditions compare with neighbors?

Weighted average cost of capital averages ?9% in the Philippines, versus 6-7% in Vietnam and ?6% in Malaysia, raising hurdle rates for developers.

Page last updated on: