Pediatric Wheelchairs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

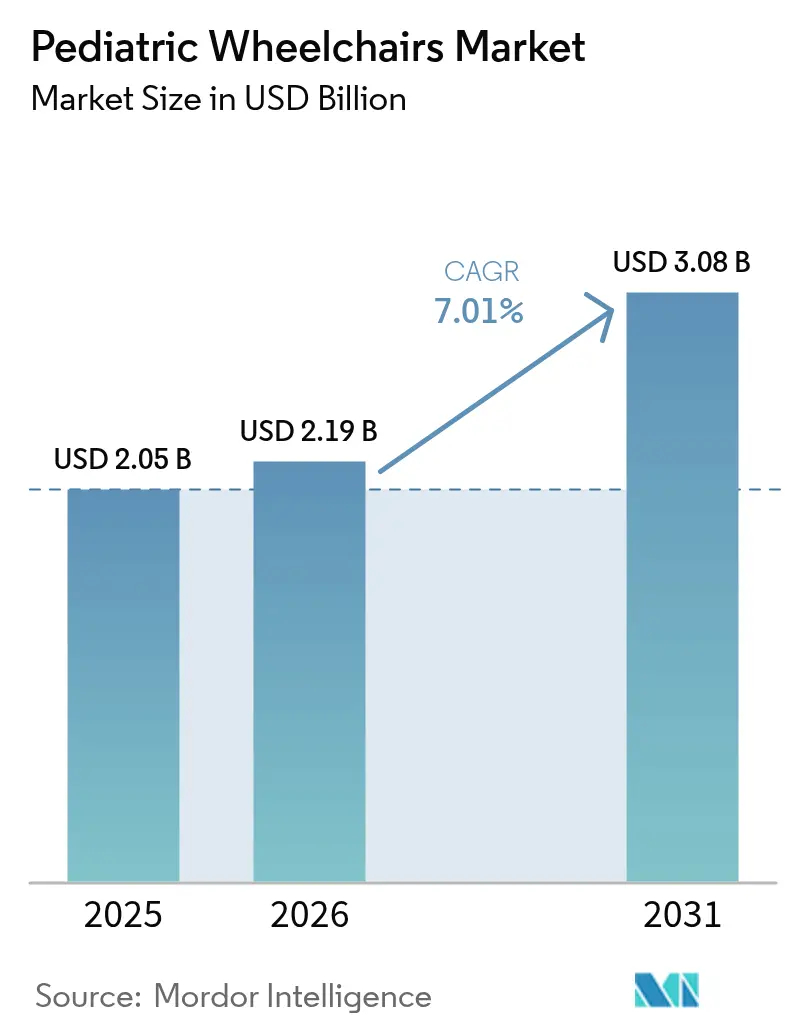

| Market Size (2026) | USD 2.19 Billion |

| Market Size (2031) | USD 3.08 Billion |

| Growth Rate (2026 - 2031) | 7.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

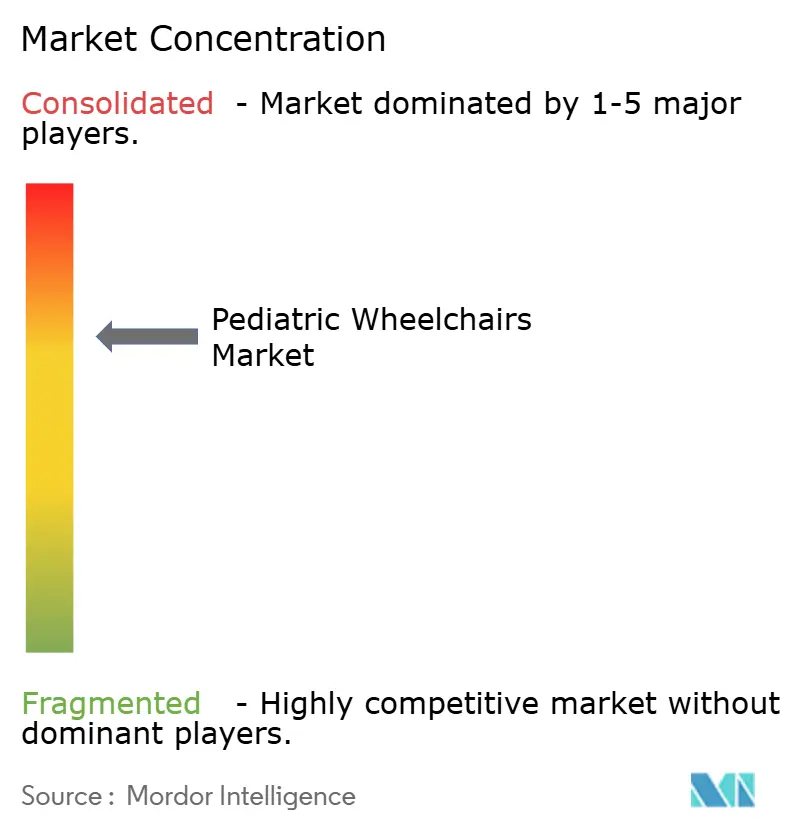

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pediatric Wheelchairs Market Analysis by Mordor Intelligence

The Pediatric Wheelchairs Market size was valued at USD 2.05 billion in 2025 and estimated to grow from USD 2.19 billion in 2026 to reach USD 3.08 billion by 2031, at a CAGR of 7.01% during the forecast period (2026-2031).

Rapid identification of mobility-related disabilities, longer survival of premature and medically complex infants, and a clear shift toward home-based care are expanding the pediatric wheelchairs market. Suppliers are differentiating through advanced materials, digital connectivity, and modular designs that accommodate growth, while payers in high-income countries continue to widen reimbursement for custom devices. Online configuration platforms shorten lead-times, and 3D-printed seating helps clinicians meet individual anatomical needs without raising production costs. Persistent semiconductor shortages and rare-earth dependence, however, expose powered chair makers to supply volatility, prompting near-shoring and dual-sourcing strategies.

Key Report Takeaways

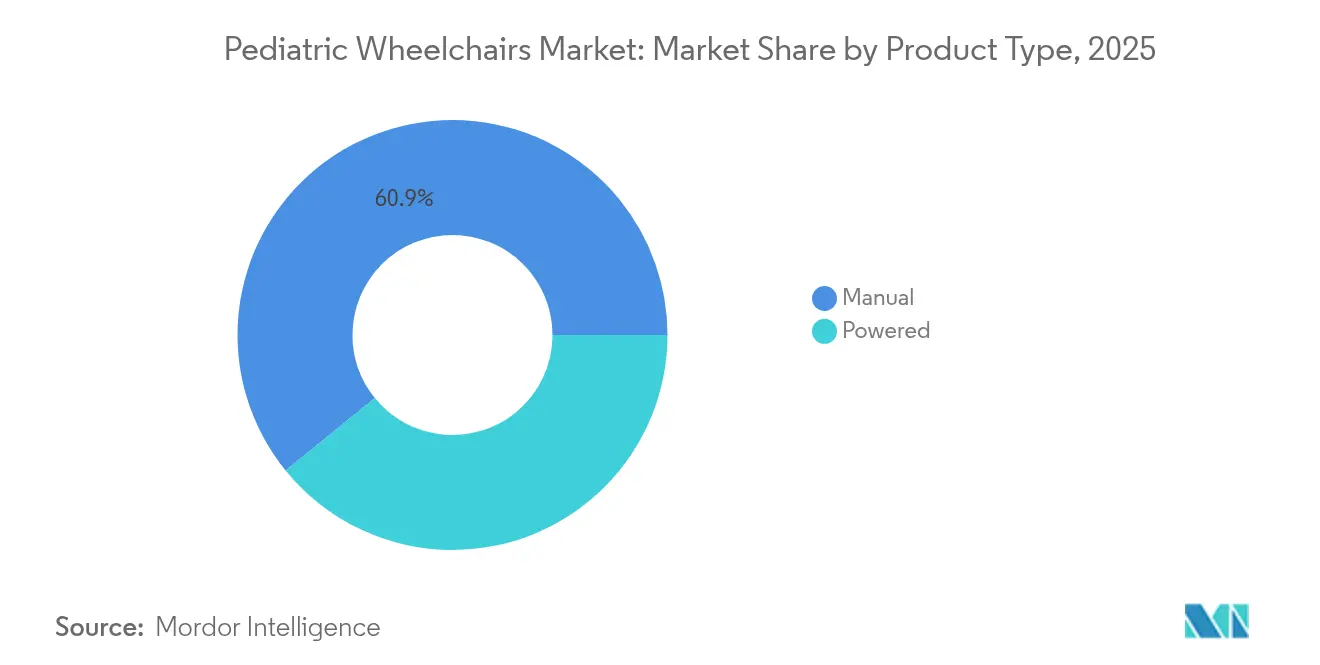

- By product type, manual wheelchairs led with 60.85% revenue share in 2025; powered wheelchairs are forecast to expand at a 9.18% CAGR to 2031.

- By frame type, foldable designs held 48.76% of the pediatric wheelchairs market share in 2025, while tilt-in-space systems are advancing at a 8.72% CAGR through 2031.

- By end user, homecare accounted for a 38.90% share of the pediatric wheelchairs market in 2025 and will grow at an 8.31% CAGR to 2031.

- By distribution channel, offline outlets held 72.65% share in 2025, whereas online sales are rising at an 11.10% CAGR to 2031.

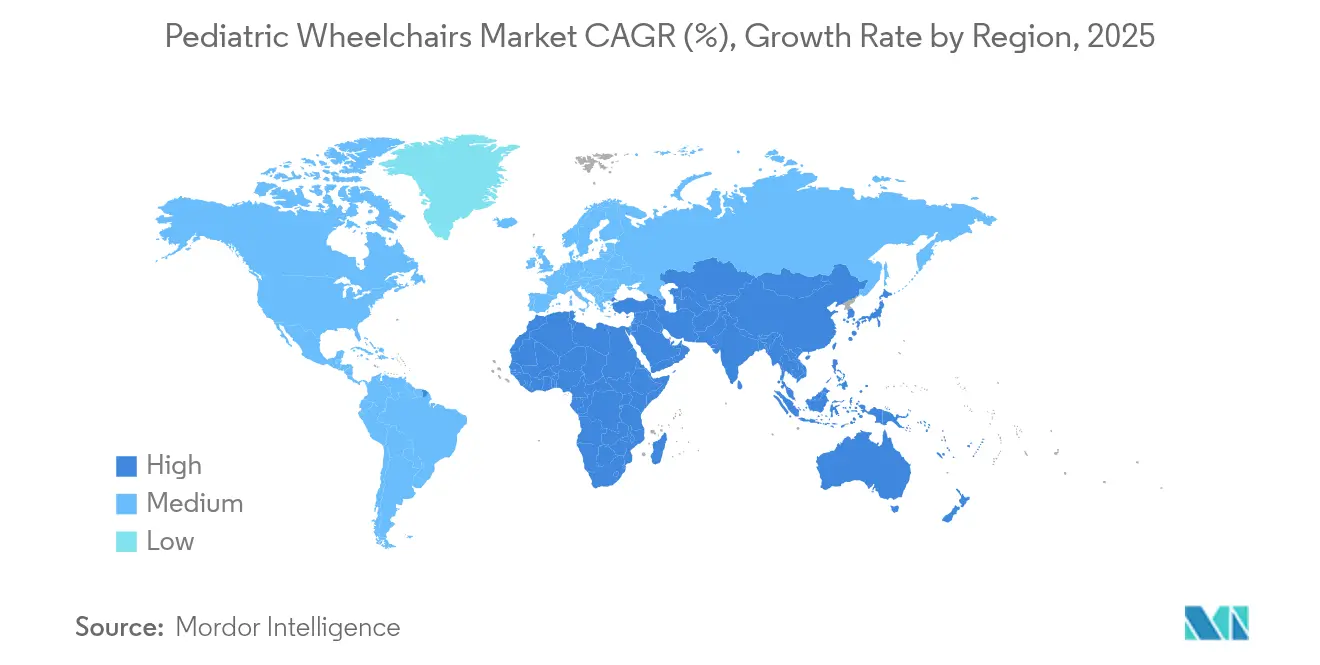

- By geography, North America commanded a 39.02% share in 2025; Asia-Pacific is set to grow fastest at 11.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pediatric Wheelchairs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of pediatric disabilities | +1.8% | Global, higher in developed markets | Long term (≥ 4 years) |

| Government funding programs for assistive technologies | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Technological advances in lightweight & power-assist systems | +1.5% | Global, led by North America & Europe | Medium term (2-4 years) |

| Higher healthcare spending and home-based care adoption | +1.1% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| 3D-printed custom seating accelerating replacement demand | +0.9% | North America & EU, emerging in APAC | Short term (≤ 2 years) |

| Inclusive-school mandates requiring on-site mobility devices | +0.7% | Global, with regulatory variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Pediatric Disabilities

Improved neonatal care is enabling more extremely premature infants to survive, yet many develop cerebral palsy or neuromuscular conditions that require long-term mobility assistance. Earlier diagnosis now occurs during routine well-baby visits, allowing clinicians to prescribe wheelchairs sooner and extend total years of use. This demographic trend enlarges the pediatric wheelchairs market because multiple chair replacements are required as children grow. The National Academies underline that timely assistive technology improves activity participation and later employment prospects.

Government Funding Programs for Assistive Technologies

Federal mandates such as the Individuals with Disabilities Education Act ensure that qualified children receive mobility devices at no cost when listed in their Individualized Education Program. The 2024 update to Section 504 clarified provider obligations, strengthening coverage across Medicaid, school districts, and nonprofit lenders.[1]U.S. Department of Health and Human Services, “Final Rule Revising Section 504 of the Rehabilitation Act,” hhs.gov Forty-eight state assistive-technology programs additionally supply low-interest loans or equipment exchanges, lowering consumer out-of-pocket expenses. Expanded funding encourages adoption of higher-specification models, further stimulating the pediatric wheelchairs market.

Technological Advances in Lightweight & Power-Assist Systems

Carbon-fiber frames and titanium joints now trim chair weight by up to 30%, improving self-propulsion, while smart hubs store user profiles that optimize push effort in real time. Devices such as the Empulse R90 push-assist integrate with Bluetooth apps so therapists can fine-tune propulsion parameters remotely.[2]Sunrise Medical LLC, “Empulse Product Launch Announcement,” sunrisemedical.com University of Houston’s soft exoskeleton prototype pairs AI movement analysis with gentle actuation to aid gait training, signaling convergence of wheelchairs and wearables for pediatric rehabilitation.[3]University of Houston, “Soft Exoskeleton Prototype for Pediatric Gait Training,” uh.edu

Higher Healthcare Spending and Home-Based Care Adoption

Decentralization of care moves complex therapies into family settings, intensifying demand for chairs that maneuver through narrow doorways and fold into car trunks. Home-based monitoring modules now transmit riding posture and vitals to clinicians, cutting clinic visits and aligning with payer preference for lower-cost care. Growth is most pronounced in Asia-Pacific, where rising disposable income and public insurance schemes widen access. The pediatric wheelchairs market therefore benefits from shifted procurement budgets toward homecare equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price & limited insurance in emerging markets | -1.4% | APAC emerging, MEA, Latin America | Long term (≥ 4 years) |

| Complex hospital procurement regulations | -0.8% | Global, stronger in regulated markets | Medium term (2-4 years) |

| Rapid child growth shortening product lifecycle | -1.1% | Global | Short term (≤ 2 years) |

| Rare-earth motor supply volatility for powered models | -0.6% | Global, supply-chain dependent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Price & Limited Insurance in Emerging Markets

A pediatric wheelchair can cost three to five times median monthly income in many lower-income countries, pushing families toward local, low-feature alternatives. Insurance gaps persist where disability support is not embedded in national health plans, limiting uptake of premium devices and tempering the pediatric wheelchairs market trajectory. The fragmented nature of funding sources requires families to navigate complex application processes across multiple agencies, creating delays and administrative burdens that can prevent timely access to mobility solutions. Price sensitivity in these markets has driven demand for simplified, locally-manufactured alternatives that may lack advanced features but provide basic mobility functionality at accessible price points.

Complex Hospital Procurement Regulations

Multilayer tender processes stretch purchase cycles beyond 12 months in large teaching hospitals, delaying replacement of outdated fleets. Manufacturers must navigate divergent coding, import tariffs, and local content rules, raising compliance costs and squeezing small entrants.The challenge is particularly acute for powered wheelchairs where the high initial investment must be amortized over a shorter usage period, creating resistance to adoption despite potential functional benefits. Manufacturers are responding with modular design approaches and adjustable components that can accommodate growth, but these solutions often add complexity and cost to base products while not fully addressing the fundamental challenge of rapid physical development in pediatric users.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Powered Chairs Gain Ground While Manual Remains Core

Manual models generated 60.85% of 2025 revenue. They remain favored for affordability, ease of maintenance, and the therapeutic exercise they provide to children with sufficient upper-body strength. The segment’s large installed base sustains a steady aftermarket for cushions, wheels, and growth kits.

Powered wheelchairs, posting a 9.18% CAGR, address users with severe neuromuscular limitations. Recent releases offer proportional joystick, head-array, and sip-and-puff controls tailored to fine motor variability. Cloud telematics now logs mileage, battery health, and seating angles, allowing clinicians to adjust parameters remotely and schedule preventive service. After the 2024 correction of SmartDrive speed-dial faults, OEMs reinforced software validation and introduced redundant braking circuits, boosting caregiver confidence.

Innovation in compact lithium-iron-phosphate batteries cuts weight and extends range, making powered chairs viable for early-school children who previously relied on strollers. Over the forecast period, the pediatric wheelchairs market size for powered models is projected to compound faster than any other category, though reimbursement hurdles in some regions may temper penetration.

By Frame Type: Tilt-in-Space Receives Clinical Endorsement

Foldable frames controlled 48.76% sales in 2025 due to everyday portability. Updated quick-release cross-braces trimmed folding depth, letting families stow chairs in small sedans. Optional one-hand fold latches support caregivers managing multiple children.

Tilt-in-space systems, growing 8.72% annually, are prescribed for children at risk of pressure ulcers or respiratory compromise. Clinicians value 45-degree posterior tilt and 20-degree anterior tilt to facilitate feeding and engagement. Electronic actuators memorize common positions, helping teachers shift posture throughout the school day without manual effort. Despite higher price, clinical proof of reduced hospitalization is convincing payers. Consequently, the pediatric wheelchairs market share for tilt-in-space is expected to widen steadily through 2031.

By End User: Homecare Dominates and Accelerates

Homecare environments generated 38.90% of 2025 sales and are expanding at an 8.31% CAGR. Families prefer managing therapy at home, where children participate in daily routines. Devices ship with a voice-guided setup that walks parents through seat adjustments. Tele-rehabilitation portals let therapists review ride data and recommend seating tweaks without in-clinic visits.

Hospitals retain importance for post-surgery mobility and initial evaluations, yet once a stable prescription is set, families transition to community use. Rehabilitation centers bridge the gap, offering gait labs and wheelchair skills clinics. These collaborating entities ensure consistent demand across the pediatric wheelchairs market.

By Distribution Channel: Digital Platforms Scale Quickly

Offline specialists supplied 72.65% of units in 2025. They offer pressure-mapping mats, trial fleets, and insurance paperwork assistance. Nonetheless, the online growth of 11.10% CAGR signals acceptance of remote consults. Permobil’s virtual-fit tool models chair geometry using a smartphone LIDAR scan, prompting caregiver adjustments before checkout.

Repeat buyers increasingly order replacement upholstery, growth kits, and accessories through e-commerce after an initial in-person fit. Dealers that blend showrooms with digital portals capture cross-channel synergies, preserving service quality while reaching rural families. Expanding online reach thus injects fresh demand into the pediatric wheelchairs market.

Geography Analysis

North America led with 39.02% revenue in 2025. Broad insurance coverage under Medicaid Early and Periodic Screening, Diagnostic and Treatment provisions and private payer parity laws sustain high penetration. ADA compliance drives schools and parks to purchase chairs that integrate with transfer lifts and accessible playground structures. Supply chain stress, however, has raised battery and semiconductor prices, nudging providers toward local sourcing.

Asia-Pacific posts the fastest 11.72% CAGR, bolstered by universal health scheme rollouts and aggressive disability inclusion policy in countries such as China, Japan, and Australia. National subsidies and tax credits helped middle-income households afford powered models, enlarging the pediatric wheelchairs market in urban hubs. Localization strategies, including assembly plants in Malaysia and Vietnam, lower tariff exposure and meet local content rules, aiding domestic uptake.

Europe shows steady, low-single-digit expansion. Social insurance covers high-cost tilt-in-space systems, but austerity in certain member states restrains premium upgrades. Continuous improvement to EU Medical Device Regulation keeps compliance costs elevated, yet also protects users through strict post-market surveillance. South America and the Middle East & Africa remain underpenetrated, though humanitarian organizations and emerging tele-rehab programs are laying groundwork for future growth.

Competitive Landscape

The market is moderately consolidated. Sunrise Medical, Permobil, and Invacare lead in global reach and R&D investment. MIGA Holdings’ 2024 purchase of Invacare’s North American unit signaled renewed capital infusion aimed at product refresh and customer service upgrades. Sunrise Medical’s Ride Designs purchase strengthened its differentiation in 3D-printed seating, accelerating bespoke fit cycles. Permobil opened a 14,000 m² innovation center featuring environmental chambers and automated test rigs, underscoring commitment to rapid prototyping.

Private equity roll-ups created scale economies but raised debt leverage at some distributors, pressuring service staffing. OEMs now pilot direct-to-consumer portals to safeguard brand experience and gather usage data for iterative design. Start-ups focusing on AI posture analytics collaborate with incumbent chair makers rather than compete head-on, highlighting a partnership-centric innovation model across the pediatric wheelchairs market.

Regulatory scrutiny has increased after isolated motor-control recalls. Leading brands therefore invest in redundant safety circuits and cybersecurity audits for connected wheels. Competitive advantage increasingly hinges on integration of hardware, software, and clinical services, rather than frame fabrication alone.

Pediatric Wheelchairs Industry Leaders

Ottobock

MEYRA GmbH

Sunrise Medical

SORG Rollstuhltechnik GmbH

Invacare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Aveanna Healthcare Holdings announced an agreement to acquire Thrive Skilled Pediatric Care, a major provider of pediatric home care services including skilled nursing and therapy for medically complex children. This acquisition enhances Aveanna's service footprint and integrates specialized care models that support pediatric wheelchair users in home-based settings.

- November 2024: Permobil inaugurated a 14,000 square meter global innovation center in Sundsvall, Sweden, combining production and R&D facilities with specialized accessibility features and sustainability technologies including solar panels and geothermal systems.

- November 2024: MIGA Holdings LLC completed the acquisition of Invacare's North American business, creating opportunities for operational optimization and market expansion in the pediatric wheelchair segment.

- October 2024: Permobil launched the TiLite X and TiLite Z ultra-lightweight manual wheelchairs featuring over 1 billion configurations, with weights of 12.1 pounds and 11.3 pounds respectively, demonstrating advances in customization and weight reduction for pediatric applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pediatric wheelchairs market as global sales of new, child-sized manual and powered wheelchairs designed for users up to eighteen years, covering rigid, foldable, and tilt-in-space frames sold through offline and online channels. According to Mordor Intelligence, the market stood at USD 2.05 billion in 2025 (mordorintelligence.com).

Scope exclusions include adult chairs downsized for children and standalone rehab seating sold without a mobility base.

Segmentation Overview

- By Product Type

- Manual

- Powered

- By Frame Type

- Rigid

- Foldable

- Tilt-in-Space

- By End User

- Hospitals

- Homecare Settings

- Rehabilitation Centers

- Other End Users

- By Distribution Channel

- Offline

- Online

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interviewed pediatric physiatrists, complex-rehab dealers, procurement heads, and parent groups across North America, Europe, and Asia. During these conversations, we gained clarity on replacement cycles, reimbursement triggers, and emerging smart-chair features, filling data gaps flagged during desk work.

Desk Research

We began with public datasets such as the CDC National Health Interview Survey, Eurostat disability modules, and UNICEF childhood-disability tables that size the eligible population. Trade statistics from UN Comtrade and tariff filings provide average import prices, while portals like RESNA and the WHO GATE initiative outline design guidelines.

Financial reports of listed manufacturers, patent families accessed through Questel, and news mined on Dow Jones Factiva let our analysts monitor launches, capacity shifts, and price resets. This is where Mordor Intelligence differentiates; yet the sources listed remain illustrative rather than exhaustive.

Market-Sizing & Forecasting

Our top-down incidence-to-mobility-aid model converts the prevalence of cerebral palsy, spina bifida, and traumatic injuries into annual demand, which is cross-checked against sampled supplier roll-ups for units and average selling prices. Inputs such as live-birth trends, home-care penetration, tender volumes, pediatric health spending, and currency shifts feed an ARIMA forecast that we stress test with expert scenarios. Bottom-up gaps, notably in low-income regions, are bridged through calibrated penetration multipliers.

Data Validation & Update Cycle

Before release, we compare outputs with shipment tallies, customs anomalies, and prior editions; material variances trigger a fresh run. Reports refresh annually, with interim updates whenever major policy, recall, or reimbursement events arise so clients always receive our latest view.

Why Mordor's Pediatric Wheelchairs Baseline Rings True

We observe that published estimates often diverge because firms stretch age bands, bundle sports buggies, or freeze exchange rates at dated levels. Key gap drivers here include others counting users up to twenty-one years or applying retail mark-ups that inflate 2024 values.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.05 B (2025) | Mordor Intelligence | |

| USD 2.24 B (2024) | Global Consultancy A | Wider age scope and inclusion of sports wheelchairs |

| USD 2.50 B (2024) | Industry Journal B | Retail mark-ups applied without incidence validation |

Global Consultancy A valued the market at USD 2.24 billion in 2024. Industry Journal B pegged it at USD 2.50 billion for the same year.

These contrasts show our disciplined scope selection, incidence-anchored modelling, and annual refresh cadence deliver a balanced, transparent baseline that decision-makers can trace and trust.

Key Questions Answered in the Report

What is the current size of the pediatric wheelchairs market?

The pediatric wheelchairs market is valued at USD 2.19 billion in 2026 and is forecast to reach USD 3.08 billion by 2031.

Which region leads the pediatric wheelchairs market?

North America holds the largest share at 39.02% thanks to robust insurance coverage and strict accessibility mandates.

Which product segment is growing fastest?

Powered wheelchairs post the highest growth with a 9.18% CAGR to 2031, driven by lighter batteries and smart control interfaces.

Why are tilt-in-space frames gaining popularity?

Clinical studies show that tilt-in-space improves pressure relief and respiratory function, supporting a 8.72% CAGR for this frame type.

How is 3D printing influencing pediatric wheelchair design?

Additive manufacturing enables precise, rapid production of custom seating, reducing lead-times from eight weeks to three and encouraging more frequent replacements.

What challenges could slow market growth?

High device prices in emerging markets, rapid child growth requiring frequent replacements, and rare-earth motor supply volatility could temper the market’s 7.01% CAGR outlook.

Page last updated on: