Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.46 Billion |

| Market Size (2026) | USD 4.62 Billion |

| Market Size (2031) | USD 5.52 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mexico Food Additives Market Analysis by Mordor Intelligence

The Mexican food additives market size was valued at USD 4.46 billion in 2025 and estimated to grow from USD 4.62 billion in 2026 to reach USD 5.52 billion by 2031, at a CAGR of 3.62% during the forecast period (2026-2031). A robust domestic food-processing base, deep integration with United States supply chains, and rising urban demand for convenient packaged foods are the primary engines behind this steady expansion of the Mexican food additives market. Ongoing regulatory reforms—most notably, front-of-pack warning labels under NOM-051—are accelerating product reformulation and stimulating investments in natural preservatives, colors, and flavors. Currency volatility and sharp spikes in raw material costs, such as the recent 143% jump in cocoa prices, continue to pressure margins, yet the Mexican food additives market remains resilient as manufacturers diversify sourcing and adopt hedging strategies. Suppliers also benefit from government industrial policy incentives that encourage local production of polymers, packaging resins, and bio-based inputs, lowering structural costs for the Mexican food additives market.

Key Report Takeaways

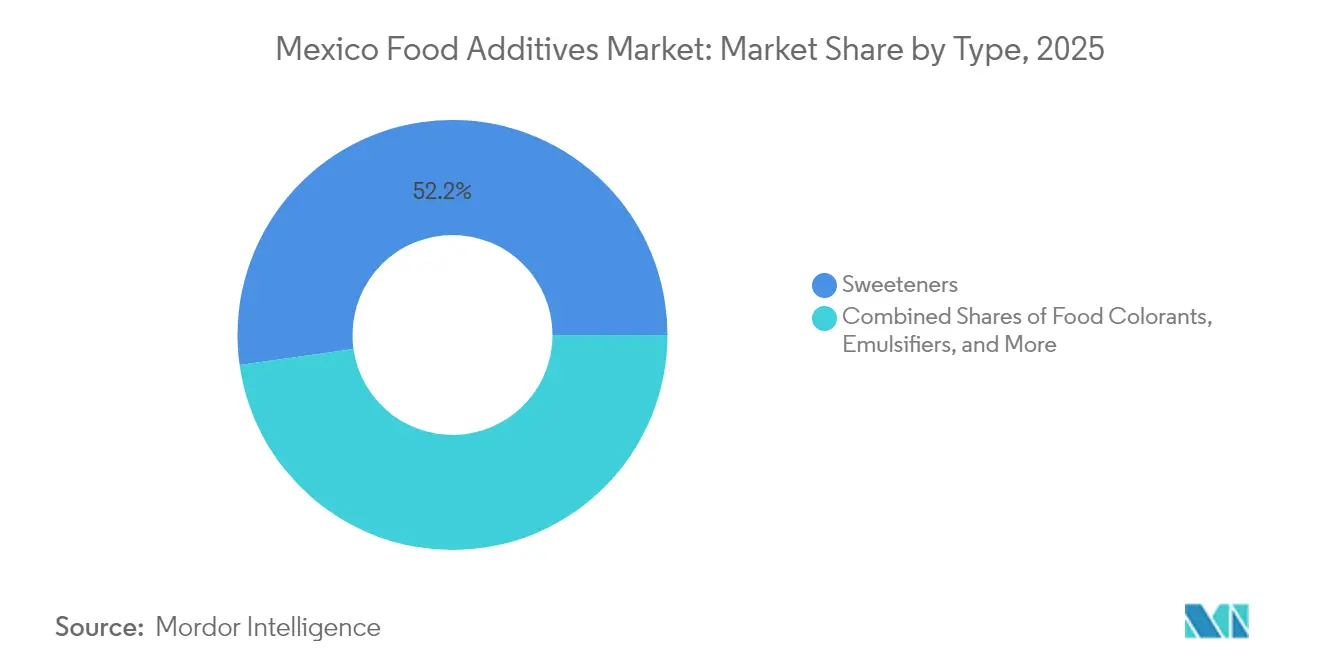

- By product type, sweeteners commanded 52.23% of Mexico's food additives market share in 2025, while food colorants are projected to grow at a 5.38% CAGR through 2031.

- By source, synthetic ingredients held 60.74% of the Mexican food additives market share in 2025, whereas natural additives are advancing at a 5.88% CAGR to 2031.

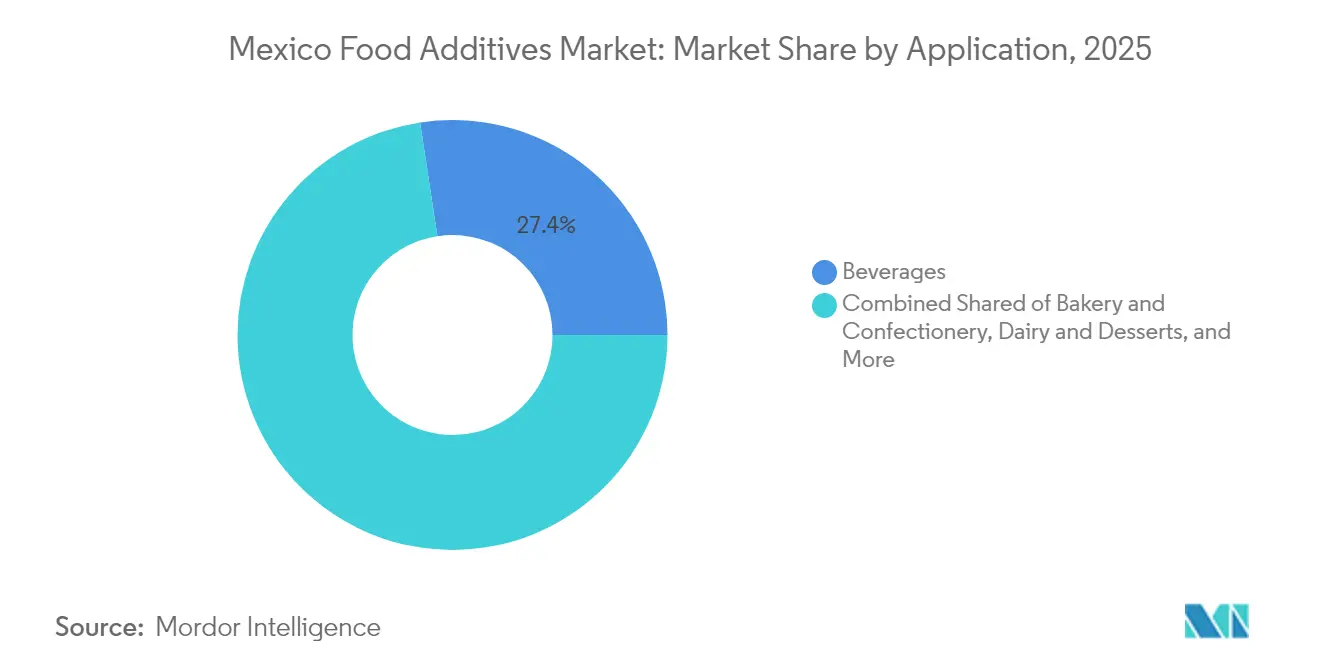

- By application, beverages accounted for 27.41% of Mexico's food additives market share in 2025, and meat and meat products represent the fastest-expanding category with a 4.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Food Additives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient packaged foods | +0.6% | National, with concentration in urban centers Mexico City, Guadalajara, Monterrey | Medium term (2-4 years) |

| Consumer inclination towards natural, clean-label, and organic food additives | +0.7% | Global trend with strong adoption in Mexico's middle-class segments | Long term (≥ 4 years) |

| Government initiatives supporting food processing industry growth | +0.5% | National, with regional focus on Jalisco, Nuevo León, Guanajuato manufacturing hubs | Medium term (2-4 years) |

| Growing applications of additives in dairy, bakery, and beverage manufacturing | +0.5% | National, with beverage concentration in traditional consumption regions | Short term (≤ 2 years) |

| Investments in food technology and R&D for functional and naturally derived additives | +0.4% | National, with R&D centers in major metropolitan areas | Long term (≥ 4 years) |

| Technological advancements in additives processing | +0.4% | Global technology adoption with Mexico-specific implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient Packaged Foods

Mexico's urbanization and changing lifestyle patterns are driving increased demand for convenient packaged foods, which is boosting the use of additives for preservation, flavor enhancement, and shelf-life extension. According to Banco de México's Office of Agricultural Affairs[1]Office of Agricultural Affairs, "Mexico: Poultry and Products Annual," Global Agricultural Information Network, fas.usda.gov in Mexico City, ultra-processed food consumption rose significantly between 2016 and 2022, with the North-Central region reporting the highest consumption rates. This trend is particularly prominent among Mexico's expanding middle class, where dual-income households are prioritizing convenience over traditional cooking methods. This shift is creating significant opportunities for emulsifiers, preservatives, and texture-modifying agents that enhance the shelf life and palatability of ready-to-eat products. However, this growth is challenged by Mexico's new school junk food ban, which restricts products with front-of-pack warning labels in elementary schools, potentially affecting 11.8 million children across 90,000 public schools. The regulatory environment is prompting manufacturers to adopt reformulation strategies that balance convenience with clean-label compliance, driving demand for innovative natural solutions in preservation and flavor enhancement.

Consumer Inclination Towards Natural, Clean-Label, and Organic Food Additives

Health consciousness and Mexico's front-of-pack labeling system are driving Mexican consumers to increasingly prefer natural and clean-label food products. Companies such as Farbe Naturals are at the forefront of this shift, creating natural sorbic acid from rowanberries as a replacement for synthetic preservatives. This movement extends beyond individual preferences to institutional procurement. According to Mexico's General Law on Adequate and Sustainable Food, public authorities are required to allocate at least 15% of their food purchases to small and medium local producers, inherently encouraging the use of less processed, naturally preserved products, as stated in the Diario Oficial de la Federación. Additionally, COFEPRIS is imposing stricter regulations on synthetic dyes, with potential bans on azo dyes under consideration. These measures are prompting manufacturers to explore natural color alternatives, such as AMHPAC's lycopene extraction from tomatoes for use as natural colorants. The alignment of consumer demand and government policy is accelerating the adoption of natural additives. However, widespread implementation faces obstacles, including cost premiums and technical performance limitations.

Government Initiatives Supporting Food Processing Industry Growth

The Mexican government's comprehensive industrial policy framework is fostering growth in food processing, which is driving the expansion of the additives market through increased domestic production capacity and strategic technology investments. President Sheinbaum's Plan México (2024-2030) focuses on replacing USD 14 billion worth of advanced material imports—such as polymers and packaging materials essential for food additives. To support this, the plan includes a 70% accelerated tax deduction incentive for chemical production and an initial funding allocation of USD 1.66 billion for fixed assets. Demonstrating its commitment to biotechnology, SADER has launched Mexico's first bio-inputs plant in Chiapas, aimed at providing sustainable alternatives to agrochemicals and enhancing natural additive production. To address historical energy infrastructure limitations, the National Electrical System Strengthening and Expansion Plan (2025-2030) has allocated USD 22.4 billion to increase generation capacity by 22,674 MW, ensuring sufficient energy supply for energy-intensive chemical processing operations. Additionally, the government is prioritizing workforce development, with plans to train 150,000 skilled workers annually by 2030, establishing a strong foundation for advanced additive manufacturing and R&D activities.

Technological Advancements in Additives Processing

Mexico's food additives sector is witnessing rapid technological advancements, fueled by a combination of multinational investments and domestic innovation. These initiatives are improving both production efficiency and product quality. Air Liquide has launched a hydrogen plant in Nuevo León, while Cryoinfra is building an air separation facility in Monterrey with a daily production capacity exceeding 2,000 tonnes of oxygen, nitrogen, and argon. These developments are strengthening the industrial gas infrastructure, which is essential for advanced additive processing. The investments are supporting key processes such as hydrogenation for edible oils, modified atmosphere packaging, and inert gas processing to enhance additive formulations. A significant focus on technological progress is evident in the extraction and processing of natural additives. Companies are investing in fermentation-derived proteins and biotechnology platforms to enable the commercial-scale production of complex flavor compounds and functional ingredients. However, energy costs in Mexico remain nearly double those in the United States, posing challenges to competitiveness. To address this, the sector is relying on technological innovations to improve process efficiency and optimize yields.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility and fluctuation in raw material prices | -0.3% | National, with particular impact on import-dependent manufacturers | Short term (≤ 2 years) |

| Strict and evolving regulatory requirements causing compliance challenges | -0.2% | National, with cascading effects on export markets | Medium term (2-4 years) |

| Increasing consumer skepticism about artificial and synthetic additives | -0.2% | National, with stronger impact in urban, educated demographics | Long term (≥ 4 years) |

| Supply chain disruptions impacting ingredient availability and pricing | -0.2% | National, with cross-border trade vulnerabilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility and Fluctuation in Raw Material Prices

Mexico's food additives market faces significant challenges, primarily due to raw material price volatility. For example, cocoa prices have risen by 143% over the past year, causing a 13% increase in chocolate prices in Mexico. Similarly, weather and pest issues have driven cilantro prices from MXN 19 to MXN 89 per kilogram. Additionally, fluctuations in the peso against the US dollar exacerbate the situation. Since many additive raw materials are imported, the market is doubly exposed to commodity price fluctuations and currency instability. Rail delays disrupting Mexico-US agricultural trade have further impacted grain imports, which are essential for starch and sweetener production. According to Coca-Cola FEMSA, sugar prices in Mexico increased by 42.1% in 2023, directly affecting the costs of sweeteners and flavor enhancers. To address these challenges, companies are adopting vertical integration strategies. For instance, Dresen Química has started cultivating rosemary for extract production to ensure a stable supply. However, such strategies require substantial capital investment and operational expertise, extending beyond traditional additive manufacturing. This volatility is particularly burdensome for smaller Mexican manufacturers, who often lack the financial resources and supply chain capabilities to implement effective hedging and diversification strategies.

Strict and Evolving Regulatory Requirements Causing Compliance Challenges

Mexico's regulatory environment is becoming increasingly stringent, presenting significant compliance challenges for food additive manufacturers. COFEPRIS, the country's health authority, has introduced requirements that surpass international standards in both complexity and specificity. The new General Law on Adequate and Sustainable Food grants health authorities the authority to identify "critical nutrients and ingredients" and ban harmful substances. This has created uncertainty for companies awaiting detailed implementation guidelines and a list of prohibited substances, as reported by the Diario Oficial de la Federación[2]Diario Oficial de la Federación, "DECRETO por el que se expide la Ley General de la Alimentación Adecuada y Sostenible," dof.gob.mx . Additionally, COFEPRIS's stricter controls on drug precursors are complicating the importation and storage of key raw materials used in flavors and fragrances. These measures have driven up costs and extended lead times for businesses reliant on imported specialty chemicals. At the same time, the front-of-pack labeling requirements under NOM-051 are undergoing changes. Recent discussions on mandatory sodium reduction could force the reformulation of thousands of products that currently meet existing standards. Smaller domestic producers are disproportionately affected by these rising compliance costs. Without the regulatory infrastructure of multinational corporations, they face the risk of being pushed out, potentially leading to market consolidation that benefits larger, well-resourced companies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sweeteners Dominate Amid Colorant Innovation

In 2025, sweeteners hold a dominant 52.23% market share in Mexico, highlighting the country's position as the world's leading per-capita soft drink consumer. This leadership is further supported by the widespread use of high fructose corn syrup (HFCS) and sugar substitutes in traditional beverages and processed foods. According to the Ministry of Economy, Mexico's sweetener market has undergone significant changes, with HFCS's share of total sweetener production. Meanwhile, food colorants are the fastest-growing segment, with a 5.38% CAGR. This growth is primarily driven by regulatory restrictions on synthetic dyes, which are encouraging innovation in natural color alternatives and reformulations in confectionery, beverage, and bakery applications.

Preservatives and emulsifiers continue to serve Mexico's growing packaged food industry, while enzymes are gaining popularity in dairy and bakery applications. Manufacturers are increasingly adopting enzymes to enhance product quality and extend shelf life without relying on synthetic additives. Hydrocolloids and anti-caking agents are used in specialized industrial applications, particularly in Mexico's expanding snack food sector. This sector has seen substantial investments, such as Gruma's USD 43 million investment in a new snack production facility in Puebla. However, the acidulants segment faces challenges due to sodium reduction initiatives. Consumer advocacy group El Poder del Consumidor is advocating for mandatory sodium limits, which could reduce demand for traditional acidifying agents while creating opportunities for potassium-based alternatives.

By Source: Natural Additives Accelerate Despite Synthetic Dominance

In 2025, synthetic additives hold a dominant 60.74% market share, driven by well-established supply chains, cost efficiencies, and technical performance attributes that natural alternatives struggle to replicate. However, natural additives are witnessing strong growth, with a 5.88% CAGR. This growth is propelled by regulatory pressures, evolving consumer preferences, and technological innovations that are narrowing performance gaps in critical applications. Companies such as Farbe Naturals are leading the way by innovating natural preservation technologies. They have developed sorbic acid from rowanberries as a direct alternative to synthetic preservatives. Similarly, AMHPAC is advancing lycopene extraction from tomatoes to support natural coloring applications.

Mexico's front-of-pack labeling system and potential restrictions on synthetic dyes are accelerating the transition to natural sources. These regulatory developments are creating favorable conditions for natural alternatives, despite their higher costs and technical challenges. Grupo Bimbo exemplifies this shift with its commitment to remove artificial colors, flavors, and preservatives from 99% of its core portfolio by 2025, supported by a significant USD 2 billion R&D investment. Nevertheless, the natural segment faces obstacles, including limited domestic production capacity, elevated raw material costs, and a complex supply chain. These challenges are particularly pronounced for exotic botanical extracts and fermentation-derived compounds, which require specialized processing capabilities that are not yet fully developed in Mexico's industrial sector.

By Application: Beverages Lead While Meat Processing Emerges

In 2025, beverages hold the largest market share at 27.41%, highlighting Mexico's significant per-capita consumption of soft drinks, functional waters, and traditional beverages. These beverages heavily depend on various additives for flavor, color, preservation, and nutritional enhancement. Mexico's role as a prominent beverage production hub further supports this segment. Leading companies like Coca-Cola FEMSA operate extensive manufacturing networks that serve both domestic and Latin American export markets. Functional beverages are witnessing robust growth, with 74% of Mexican consumers drinking functional waters weekly. This trend drives the demand for specialized additives, including vitamins, minerals, and bioactive compounds.

Meat and meat products represent the fastest-growing segment, with a 4.18% CAGR. This growth is driven by Mexico's position as the sixth-largest poultry producer globally and increasing domestic protein consumption, primarily due to its cost-effectiveness compared to beef and pork. The segment also benefits from rising private investments in poultry processing, improved feed prices, and expanded access to Central American export markets, which require advanced preservation and quality enhancement systems. Dairy and dessert applications continue to grow steadily, supported by the anticipated expansion of Mexico's dairy market in 2025. This growth is expected to boost domestic cheese and butter production, aided by a greater supply of milk and dairy ingredients. Although bakery and confectionery applications face challenges from school junk food restrictions, they still benefit from urbanization and the growing demand for convenience foods. Meanwhile, soups, sauces, and dressings remain a stable segment, catering to Mexico's diverse culinary traditions and its expanding restaurant industry.

Geography Analysis

Mexico's food additives market is heavily concentrated in key manufacturing and population centers, with the central and northern regions leading in production and consumption. The Bajío region, which includes Guanajuato, Querétaro, and Jalisco, is the primary food processing hub. Significant investments in this area include Nestlé Purina's USD 220 million facility in Silao, Guanajuato, with an annual capacity of 285,000 metric tonnes of dry pet food, and Kellanova's USD 100 million expansion in Toluca, State of Mexico. Northern states, particularly Nuevo León and Sonora, benefit from their proximity to US markets and well-established cross-border supply chains. For example, Air Liquide has commissioned new hydrogen production facilities in Nuevo León to meet industrial processing demands. The Mexico City metropolitan area remains the largest consumption center, driving the need for convenience foods and processed beverages that rely heavily on additives.

Regional development patterns align with Mexico's broader nearshoring trends, with foreign direct investment reaching USD 36.9 billion in 2024, according to preliminary data from the Ministry of Economy, although full-year figures declined due to a weaker fourth quarter, as noted by Mazzanti, Alessio. The Pacific coast regions, such as Jalisco and Sinaloa, serve as both agricultural production centers and food processing hubs, benefiting from proximity to raw materials and port access for exports.

Southern regions, while underdeveloped in industrial food processing, are receiving increased government focus. For instance, SADER's bio-inputs plant in Chiapas represents the country's first facility dedicated to sustainable agricultural alternatives, as reported by GBR Reports. Border regions face challenges from organized crime and security issues, complicating logistics and distribution. However, the strategic importance of US trade relationships continues to attract investments in manufacturing capabilities in these border states, despite these operational risks.

Competitive Landscape

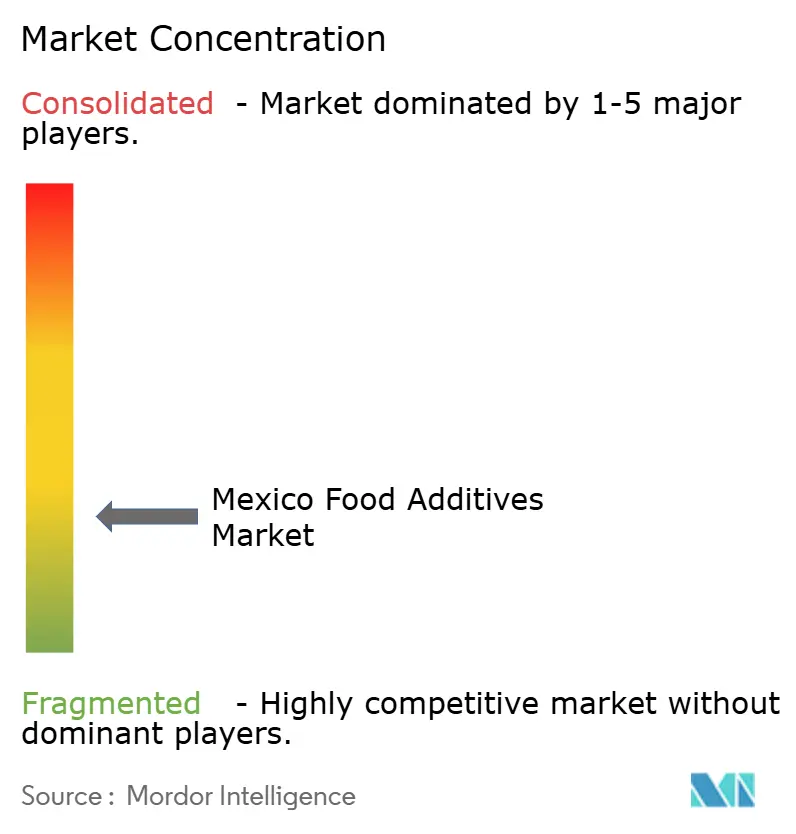

Mexico's food additives market maintains a fragmented structure with a concentration score of 3 out of 10, indicating significant consolidation opportunities as regulatory pressures and capital requirements favor larger, well-resourced players. The competitive landscape is characterized by a mix of multinational corporations with established Mexican operations and domestic companies seeking to capitalize on local market knowledge and supply chain proximity.

Multinational leaders like Cargill, ADM, and Ingredion leverage their global R&D capabilities and regulatory expertise to navigate Mexico's evolving compliance requirements, while domestic players focus on specialized applications and regional distribution advantages. Strategic patterns reveal increasing emphasis on natural and clean-label product development, with companies investing heavily in biotechnology platforms and extraction technologies to meet regulatory requirements and consumer preferences. The market presents white-space opportunities in natural preservation technologies, plant-based flavor systems, and functional additives that address Mexico's specific health challenges, including obesity and diabetes.

Emerging disruptors are primarily technology-focused companies developing fermentation-derived ingredients and botanical extraction capabilities, though their market penetration remains limited by capital constraints and regulatory approval timelines. COFEPRIS's procedural simplifications implemented in March 2025 are expected to reduce barriers for smaller innovators while maintaining safety standards, potentially accelerating competitive dynamics in specialized additive categories

Mexico Food Additives Industry Leaders

-

Cargill, Incorporated

-

DuPont de Nemours, Inc.

-

The Archer Daniels Midland Company

-

Chr. Hansen A/S

-

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: IFF consolidated its Mexican operations at the new Tecnoparque business hub in Mexico City. This strategic development will establish one of IFF’s largest global office sites, hosting up to 650 employees across Health & Biosciences, Scent, Taste, and Food Ingredients divisions.

- July 2023: The company launched sugar reduction toolkit with the launch of TASTEVA® Sol. TASTEVA® SOL is a tasting stevia that has over 200x the solubility of Reb M and D products on the market. TASTEVA® SOL solves for solubility challenges often found in beverage concentrates, dairy fruit preparations and sweet syrups at high sugar replacement levels.

- May 2023: The company expanded its product portfolio by launching extracts, dehydrated ingredients, and flavors. The company states that these products are made under the Upcycling Food concept by-products of plants and fruits that are normally discarded, thereby helping to reduce food waste.

Mexico Food Additives Market Report Scope

The Mexico food additives market is segmented on the basis of type as emulsifiers, starches and sweeteners, colorants, flavors, and others. By application the market studied is segmented into, dairy, bakery, meat products, beverages, confectionery, and others.

By Product Type

| Preservatives |

| Sweeteners |

| Sugar Substitutes |

| Emulsifiers |

| Anti-Caking Agents |

| Enzymes |

| Hydrocolloids |

| Food Flavors and Enhancers |

| Food Colorants |

| Acidulants |

By Source

| Natural |

| Synthetic |

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Soups, Sauces, and Dressings |

| Other Applications |

| By Product Type | Preservatives |

| Sweeteners | |

| Sugar Substitutes | |

| Emulsifiers | |

| Anti-Caking Agents | |

| Enzymes | |

| Hydrocolloids | |

| Food Flavors and Enhancers | |

| Food Colorants | |

| Acidulants | |

| By Source | Natural |

| Synthetic | |

| By Application | Bakery and Confectionery |

| Dairy and Desserts | |

| Beverages | |

| Meat and Meat Products | |

| Soups, Sauces, and Dressings | |

| Other Applications |

Key Questions Answered in the Report

What are the fastest-growing food additives in Mexico?

Natural food colorants are growing fastest at 5.38% CAGR through 2031, followed by natural preservatives and clean-label flavors.

Which food categories use the most additives in Mexico?

Beverages dominate additive consumption with 27.41% market share, followed by bakery products and processed meats.

What is the Overall Size of the Market?

The Mexico food additives market is valued at USD 4.62 billion in 2026 and is projected to reach USD 5.52 billion by 2031, growing at a compound annual growth rate (CAGR) of 3.62% during the forecast period (2026-2031).

What regulatory changes are affecting food additives in Mexico?

Recent changes include COFEPRIS procedural simplifications (March 2025), potential restrictions on synthetic dyes, the General Law on Adequate and Sustainable Food (April 2024), and an upcoming decree to ban hazardous pesticides that may affect agricultural inputs used in additive production.

Page last updated on: