Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

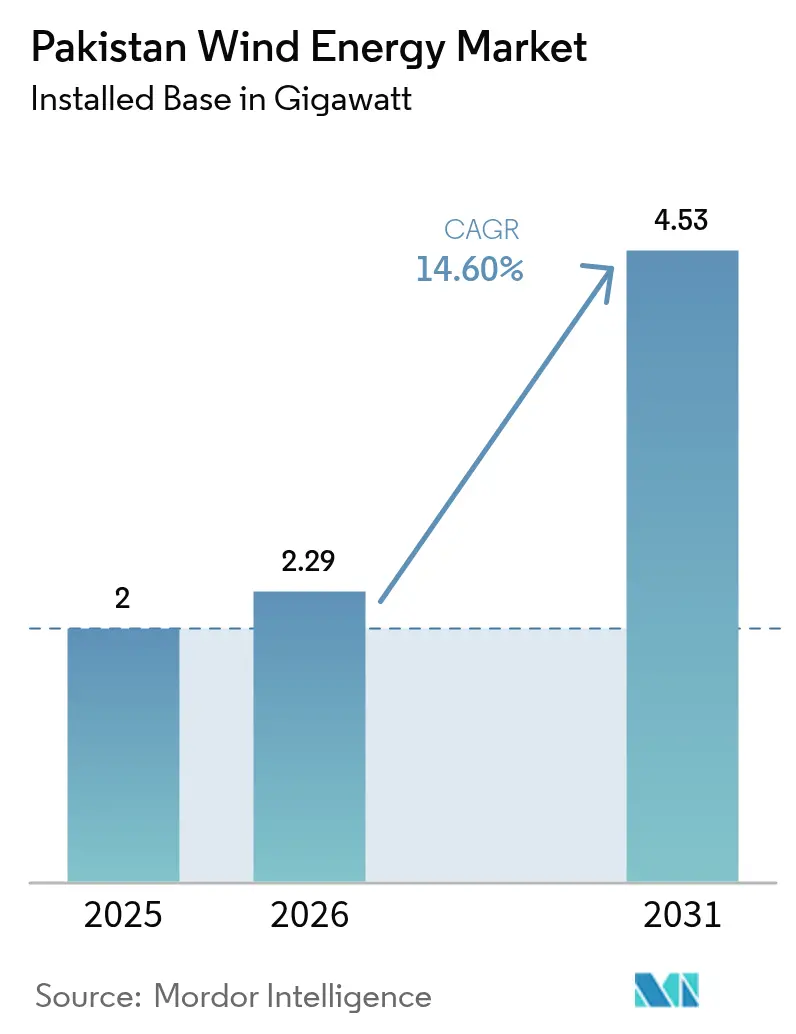

| Base Year Market Size (2025) | 2 gigawatt |

| Market Volume (2026) | 2.29 gigawatt |

| Market Volume (2031) | 4.53 gigawatt |

| Growth Rate (2026 - 2031) | 14.60% CAGR |

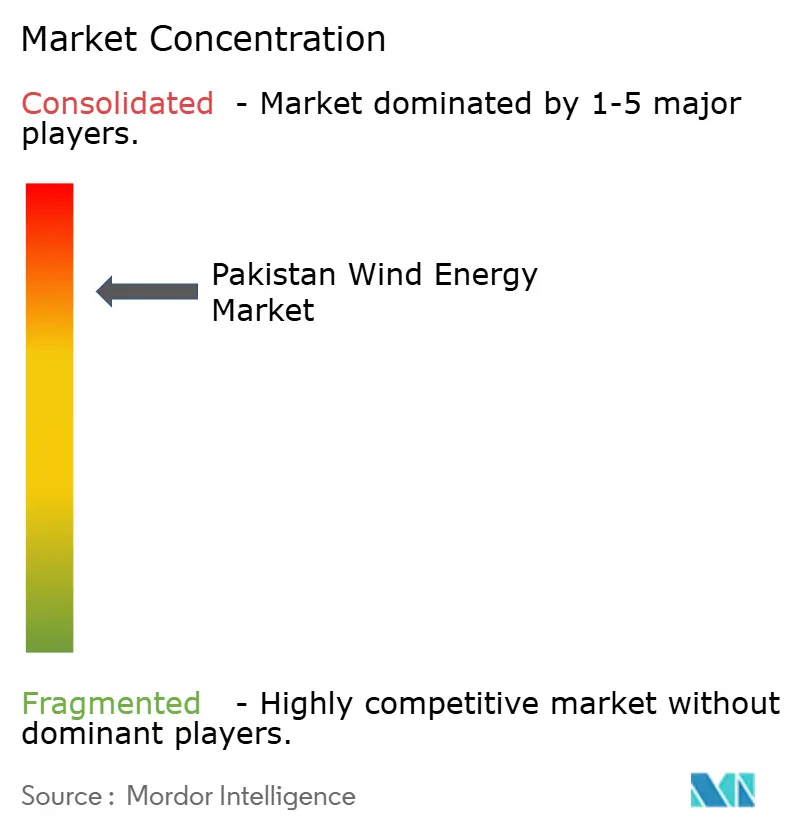

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Wind Energy Market Analysis by Mordor Intelligence

Pakistan Wind Energy Market size in 2026 is estimated at 2.29 gigawatt, growing from 2025 value of 2 gigawatt with 2031 projections showing 4.53 gigawatt, growing at 14.6% CAGR over 2026-2031.

Growth is anchored in the government’s Alternative and Renewable Energy Policy, which targets 60% renewables by 2030 and grants attractive fiscal and foreign-exchange protections. Accelerated depreciation under the 2024 Finance Act, hybrid wind–solar tenders, and a maturing corporate power-purchase agreement (PPA) ecosystem have reduced levelized costs and unlocked new revenue streams. Rising demand from export-oriented textiles, improved grid integration through storage pilots, and steady capital inflows, clean-energy investment rose 915% to USD 475 million in 2023, further reinforcing momentum. Nonetheless, transmission congestion on the 500 kV Jhimpir–Jamshoro line, Rs 2.6 trillion circular-debt exposure, and currency-linked turbine cost inflation temper near-term upside.

Key Report Takeaways

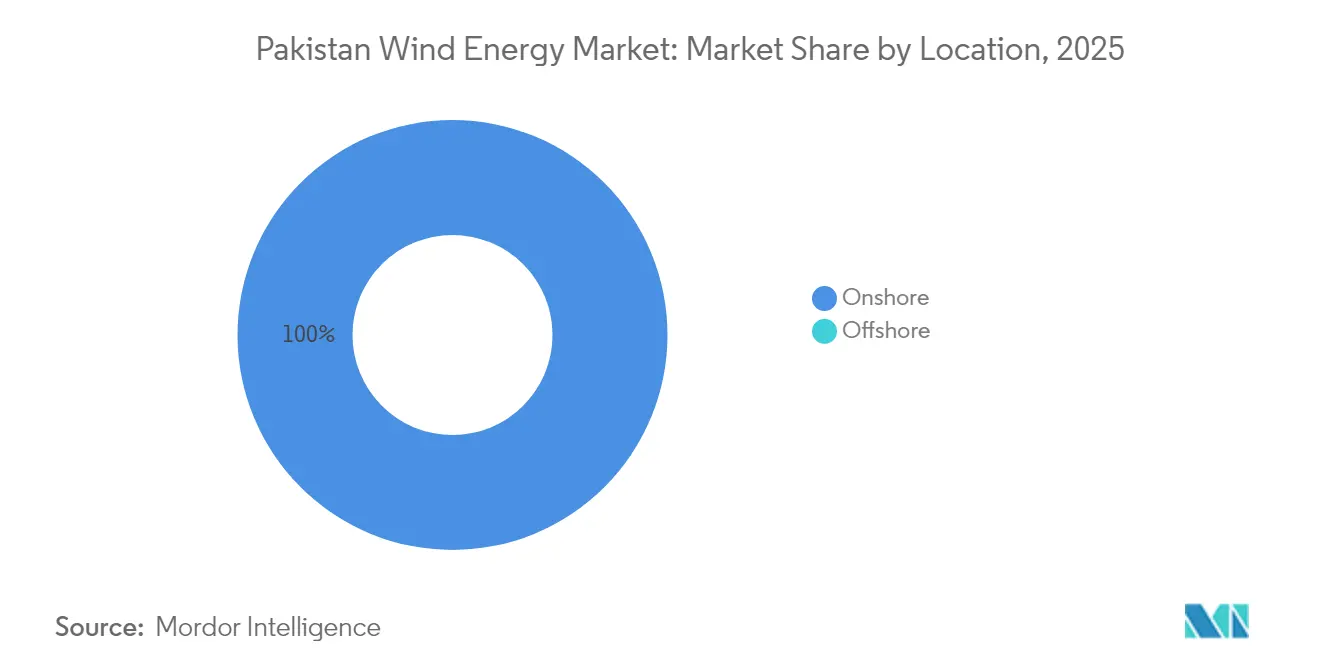

- By location, onshore installations captured 100.00% of the Pakistan wind energy market share in 2025, whereas offshore capacity is projected to register the fastest growth rate of 23.4% through 2031.

- By turbine capacity, units with a capacity of up to 3 MW commanded a 64.15% share of the Pakistan wind energy market size in 2025; turbines with a capacity above 6 MW are forecast to expand at a 20.9% CAGR from 2026 to 2031.

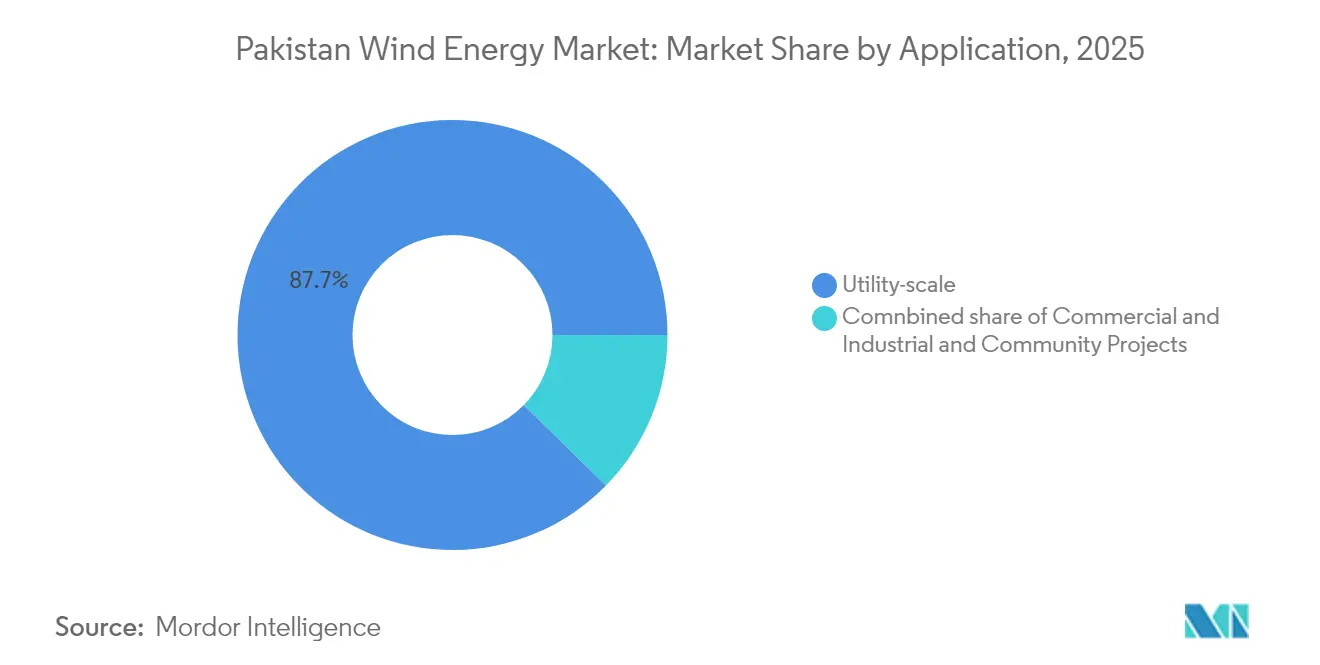

- By application, utility-scale projects accounted for 87.65% of the Pakistan wind energy market size in 2025, while commercial and industrial demand is projected to advance at a 18.8% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 60% renewables target by 2030 | +3.20% | National / Sindh corridor | Medium term (2-4 years) |

| Accelerated depreciation for wind IPPs | +1.80% | National | Short term (≤ 2 years) |

| Bankable hybrid wind–solar PPAs | +2.10% | Sindh expanding to Punjab & Balochistan | Medium term (2-4 years) |

| Corporate PPAs from textile exporters | +1.90% | Punjab & Sindh industrial clusters | Short term (≤ 2 years) |

| CPEC Phase-II green-energy pivot | +2.40% | National focus on Sindh & Balochistan | Long term (≥ 4 years) |

| Commercial rollout of 6 MW+ turbines | +1.70% | Coastal Sindh, interior Balochistan, southern Punjab | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

60% Renewables Target by 2030

The 2019 Alternative and Renewable Energy Policy, implemented in 2020, grants foreign investors 100% equity ownership, hard-currency accounts, and legal protection, creating a predictable framework for utility-scale procurement. Targets rose to 60% renewables by 2030 in 2024, forcing planners to accelerate interconnection approvals despite licensing queues that still average 6-12 months.(1)Practice Guides, “Energy & Infrastructure M&A 2024—Pakistan,” practiceguides.chambers.com About 50 GW of the country’s 346 GW technical wind potential lies in coastal Sindh, positioning the corridor as the anchor zone for the Pakistan wind energy market. Alignment with Pakistan’s updated Nationally Determined Contribution elevates wind energy to a strategic pillar for climate and energy security commitments, ensuring continued eligibility for grants and concessional loans from multilateral agencies. Provincial facilitation centers in Sindh have begun issuing land-use certificates within 60 days, thereby reducing development cycles and enhancing bankability for prospective sponsors.

Corporate PPAs from Textile Exporters

Export-oriented textiles consume roughly 35% of Pakistan’s industrial electricity, prompting mills such as Gul Ahmed, Interloop, and Nishat to pursue off-site wind PPAs with tenure up to 25 years. Levelized tariffs priced 10-15% below the 2023 grid-weighted average of USD 90.18/MWh improve earnings resilience amid volatile utility rates.(2)Global Climatescope, “Climatescope 2024 | Pakistan,” global-climatescope.org The Private Power and Infrastructure Board now permits direct bilateral contracts subject to grid-wheeling fees, simplifying compliance with buyer ESG mandates. State Bank concessionary lines finance rooftop metering and embedded generation assets, but utility-scale off-take remains predominant due to economies of scale. The Competition Commission enforces transparent wheeling-charge disclosure, minimizing anticompetitive practices and fostering wider corporate adoption.

CPEC Phase-II Green-Energy Pivot

The China-Pakistan Economic Corridor transitioned to a “high-quality development” agenda in 2024, earmarking USD 3 billion of prospective Phase-II loans for renewable energy. Yet, cumulative payment arrears topping USD 1.4 billion and intermittent security incidents in Sindh and Balochistan dampen the repeat investment appetite of early movers such as China Three Gorges Corporation. Goldwind’s 2022 establishment of a Karachi “solution factory” mitigates foreign-exchange exposure by localizing tower fabrication and after-sales services.(3)Windpower Monthly, “Windpower Intelligence Global Forecast: March 2024,” windpowermonthly.com Green Belt-and-Road policies oblige lenders to incorporate environmental and social safeguards, encouraging Pakistan to expedite transmission upgrades and strengthen payment-security mechanisms. Anti-terror insurance and currency devaluation reserves have become standard features in recent EPC contracts, pushing bid margins higher but improving risk allocation.

Commercial Rollout of 6 MW+ Turbines

Siemens Gamesa’s multiyear O&M deal on Din Energy’s 50 MW Jhimpir plant showcases the reliability of 6 MW platforms under Pakistani conditions, with FY 2024 availability above 95% and net output of 111.38 GWh.(4)PACRA, “Rating Report: Din Energy Limited,” pacra.com Larger rotors capture low-speed interior winds, expanding the viable development map to southern Punjab and inland Balochistan. Advanced supervisory controls slash reactive-power penalties, a recurring curtailment trigger for first-generation turbines. Vestas and GE are conducting dust-abrasion field trials on silicon-carbide leading-edge protection, aiming to extend blade overhaul intervals to 12 years. Overall, higher-capacity machines reduce the balance-of-plant cost per MW by 8-10% and support Pakistan's wind energy market penetration into previously marginal wind pockets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rupee depreciation and import-led cost inflation | -2.30% | National | Short term (≤ 2 years) |

| Congestion on 500 kV Jhimpir–Jamshoro corridor | -1.80% | Sindh | Medium term (2-4 years) |

| Circular-debt risk to IPP payment security | -2.10% | National | Short term (≤ 2 years) |

| Balochistan land-acquisition delays | -1.20% | Balochistan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rupee Depreciation and Cost Inflation

Pakistan imports over 85% of turbine components, exposing developers to currency swings that lifted EPC quotes by nearly 19% between Q4 2023 and Q4 2024. Central-bank dollar rationing extends the issuance of letters of credit beyond 60 days, delaying site mobilization and incurring liquidated-damages risk. Sponsors hedge through forward contracts, yet residual volatility compresses debt-service coverage ratios, prompting lenders to demand higher base-rate spreads. Local foundries can only manufacture towers and anchor cages, limiting near-term import substitution. Unless onshore fabrication expands to include nacelles and blades, currency-linked capital expenditures will continue to erode Pakistan's wind energy market competitiveness.

Circular-Debt Risk

Sector arrears ballooned to Rs 2.6 trillion by December 2024, with generation companies owed Rs 1.3 trillion, triggering payment‐security drawdowns for sixteen wind IPPs. Eight development-finance institutions issued a joint warning in March 2025 that unilateral tariff renegotiations could breach sovereign obligations and freeze USD 2.7 billion of future climate finance.(5)Business Recorder, “Tariff Readjustment: MoF Weighs Impact of DFIs' Joint Letter,” brecorder.com While the Ministry of Finance introduced a Sustainable Investment Sukuk Framework in April 2025 to refinance debt, uptake remains uncertain until PPAs are insulated from retroactive revisions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Offshore Potential Emerges Despite Onshore Dominance

Onshore plants retained 100.00% Pakistan wind energy market share in 2025, an outcome of proven meteorological data, grid proximity, and established land-lease protocols in the Jhimpir-Thatta corridor. Offshore feasibility, however, advanced during 2025 after World Bank studies confirmed 21 GW of commercially exploitable potential within 50 km of the shoreline, encouraging policymakers to draft leasing guidelines. Planned capacity additions through 2031 would increase onshore installations to 3,980 MW; however, the offshore rollout could accelerate post-2028 once marine environmental-impact frameworks are finalized, underpinning the fastest 23.4% CAGR in the segment. Onshore dominance also stems from cost parity; the average all-in capital cost for coastal projects dipped to USD 1.15 million per MW in 2024, whereas offshore estimates remain above USD 3 million, inclusive of subsea cable and monopile foundations. Nevertheless, offshore concessions near Keti Bunder could unlock year-round capacity factors above 50%, materially lifting Pakistan's wind energy market size in later forecast years.

The onset of hybrid configurations, where coastal solar arrays supply off-peak power to shared transmission assets, is starting to offset onshore curtailment risk. Sindh's special economic zone framework now includes expedited customs clearance for offshore survey vessels, signaling proactive provincial engagement. Environmental regulators aim to harmonize fishery coexistence guidelines with those of neighboring India and Oman, thereby facilitating international cooperation. As grid‐modernization projects introduce high-voltage direct-current backbones, offshore injections can bypass congested AC corridors, bolstering dispatch reliability and diversifying the Pakistan wind energy market footprint beyond Jhimpir.

By Turbine Capacity: Large Turbines Drive Technology Transition

Units up to 3 MW held 64.15% of Pakistan's wind energy market share in 2025, a legacy of early CPEC‐funded farms that relied on field-tested Chinese platforms. Mid-range 3-6 MW turbines constitute 27.25% of the installed base and remain attractive for repowering infill opportunities where crane access and pad upgrades are constrained. Above 6 MW machines, however, will propel future expansions, reflecting a 20.9% CAGR through 2031 on the back of favorable wind heterogeneity and falling blade-transport costs. The Pakistan wind energy market size associated with these large-format turbines is expected to reach 542 MW by 2031, underscoring the technology shift underway. Energy's rational metrics, including 95% availability and a 35% net capacity factor, affirm its economic viability under local dust and temperature regimes.

Larger rotors lower the cut-in speed to 2.5 m/s, enabling development in southern Punjab, where median wind velocities hover around 6.3 m/s. Developers achieve balance-of-plant savings through fewer foundations and reduced collector circuits, trimming project-level capital expenditures by roughly USD 120,000 per MW compared with three-megawatt arrays. Grid-code amendments in 2024 raised low-voltage ride-through thresholds, a specification already embedded in the latest Vestas and GE models, thus expediting type certification. Long-term service agreements, bundled with manufacturer-guaranteed availability above 97%, further mitigate operational risk premiums, ensuring that the adoption curve for large turbines remains steep within the Pakistani wind energy industry.

By Application: Industrial Demand Accelerates Commercial Adoption

Utility-scale wind accounted for 87.65% of Pakistan's wind energy market size in 2025, underpinned by standardized cost-plus PPAs that lock 25-year revenue visibility. Competitive bidding, introduced in 2022, shaved tariffs by 14% within two rounds, demonstrating buyer discipline without compromising bankability. Corporate and industrial offtake, however, constitutes the most dynamic application, posting a 18.8% CAGR and likely to exceed 623 MW by 2031 as export-oriented textiles backstop their Scope 2 emissions. Artistic Milliners' November 2024 purchase of Tenaga Generasi's 49.5 MW asset exemplifies vertical integration by industrial incumbents.

State Bank refinancing at 5% fixed for 10 years reduces the weighted-average cost of capital on embedded generation, nudging cement, fertilizer, and dairy processors toward bilateral wind PPAs. The Private Power and Infrastructure Board's merger with the Alternative Energy Development Board in 2023 established a one-stop window for captive wheeling, truncating approval time from 14 to 8 months. Community-scale ventures remain nascent; less than 6 MW was online by end-2025, impeded by credit security concerns and partial-risk-guarantee availability. Even so, the Alternative and Renewable Energy Policy authorizes mini-grid licenses and net-metering for clusters up to 5 MW, offering a framework for rural electrification pilots that can extend Pakistan's wind energy market penetration into off-grid territories after 2027.

Geography Analysis

Sindh held virtually the entire installed base of 1,920 MW in 2025 and is projected to preserve leadership through 2031, advancing at a 14.9% CAGR on the strength of superior wind regimes and entrenched supply chains. The Jhimpir–Thatta strip alone could add 1,000 MW under existing land leases, though congestion on the adjacent 500 kV backbone requires urgent STATCOM and reconductoring upgrades to maintain dispatch priority.

Balochistan, despite possessing 20,000 MW of technical capacity, recorded negligible commissioned projects by 2025. Tribune-mediated land rights disputes, limited road infrastructure, and investor security premiums elevate project timelines; however, the forthcoming Gwadar East Bay expressway and 220 kV Makran grid extension could unlock 310 MW by 2029, broadening Pakistan's wind energy market share across provinces. Punjab and Khyber Pakhtunkhwa feature modest resources in southern and northwestern pockets; yet, the proximity of textile clusters and wheeling concessions lures entrepreneurs to pilot 50-MW clusters that pair wind with rooftop solar for blended load portfolios. International development lenders, historically focused on Sindh, began scoping multi-province transmission guarantees in 2025, signaling their intent to diversify geographic exposure and mitigate over-concentration risk.

Competitive Landscape

China Three Gorges Corporation and Goldwind jointly account for an estimated 48% of operational capacity, but market concentration has declined as European OEMs and local industrial investors secure new awards. Siemens Gamesa, Vestas, and GE now collectively capture roughly 35% of pending turbine supply agreements, leveraging advanced 6–7 MW platforms and extended-warranty operations and maintenance (O&M) packages. Strategic positioning centers on technology localization; Goldwind’s Karachi factory delivers tower sections and hub assembly kits, while Siemens Gamesa bundles blade repair and up-tower inspection via remote drones to cut downtime. Oracle Power’s 1.3 GW hybrid cluster and JCM Power’s 240 MW Dhabeji project attracted blended finance from multilateral and commercial sources, signaling lender comfort with cross-border sponsor mixes.

Secondary-market liquidity is improving: Artistic Milliners’ takeover of Tenaga Generasi and UEP Wind’s equity reshuffle in 2024 illustrate evolving asset-rotation models. Regulatory oversight by the Competition Commission of Pakistan mandates pre-merger clearance for any transaction exceeding Rs 1 billion, a process now streamlined through electronic filing introduced in 2024. White-space opportunities abound in offshore, storage-coupled arrays and micro-grid solutions for mining and desalination facilities. These niches could dilute incumbent dominance and further fragment the Pakistan wind energy market over the next five years.

Pakistan Wind Energy Industry Leaders

Vestas Wind Systems A/S

China Three Gorges Corp

United Energy Group Limited

Goldwind International Holdings Ltd

General Electric Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The Pakistan government approved the Sustainable Investment Sukuk Framework, enabling the issuance of approximately Rs 30 billion in green Sukuk to finance renewable energy projects, including wind, solar, hydroelectric, and biomass initiatives that reduce carbon emissions and enhance grid integration, Mettis Global.

- March 2025: Development Finance Institutions, including the International Finance Corporation, the Asian Development Bank, and six other lenders, criticized Pakistan's Ministry of Finance for pressuring renewable energy independent power producers to renegotiate power purchase agreements in a non-consultative manner, warning that unilateral contract revisions could undermine investor confidence and discourage future private investment in wind and solar projects.

- February 2025: International Finance Corporation and Asian Development Bank raised concerns about Pakistan's energy sector negotiations affecting financing dynamics for wind projects, with Development Finance Institutions having invested approximately USD 2.7 billion in Pakistan's power sector over 25 years, and requiring prior written approval for major project document changes, including power purchase agreements.

- January 2025: The World Bank published the Pakistan Development Update, focusing on power sector distribution reforms and the challenges of integrating renewable energy. The update addresses structural issues affecting wind energy deployment and grid modernization requirements for variable renewable resources.

Pakistan Wind Energy Market Report Scope

The Pakistani wind energy market report includes:

By Location

| Onshore |

| Offshore |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| By Location | Onshore |

| Offshore | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System |

Key Questions Answered in the Report

How large is Pakistan’s installed wind capacity in 2026?

It stands at 2,290 MW, with the Pakistan wind energy market expected to reach 4,530 MW by 2031.

What CAGR does Pakistani wind power expect over 2026-2031?

The market is projected to grow at a 14.6% compound annual rate, assuming timely grid and policy execution.

Which province hosts most commercial wind farms?

Sindh dominates due to strong 7-8 m/s coastal winds and existing 500 kV transmission corridors.

Why are 6 MW+ turbines gaining traction in Pakistan?

Larger rotors boost output at low-wind inland sites and lower per-MW balance-of-plant costs, supporting higher returns.

How are corporate PPAs shaping new wind build-out?

Textile exporters lock long-term tariffs below grid prices, driving a 18.8% CAGR in commercial and industrial demand for wind power.

Page last updated on: