Outdoor Lighting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.32 Billion |

| Market Size (2031) | USD 23.72 Billion |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

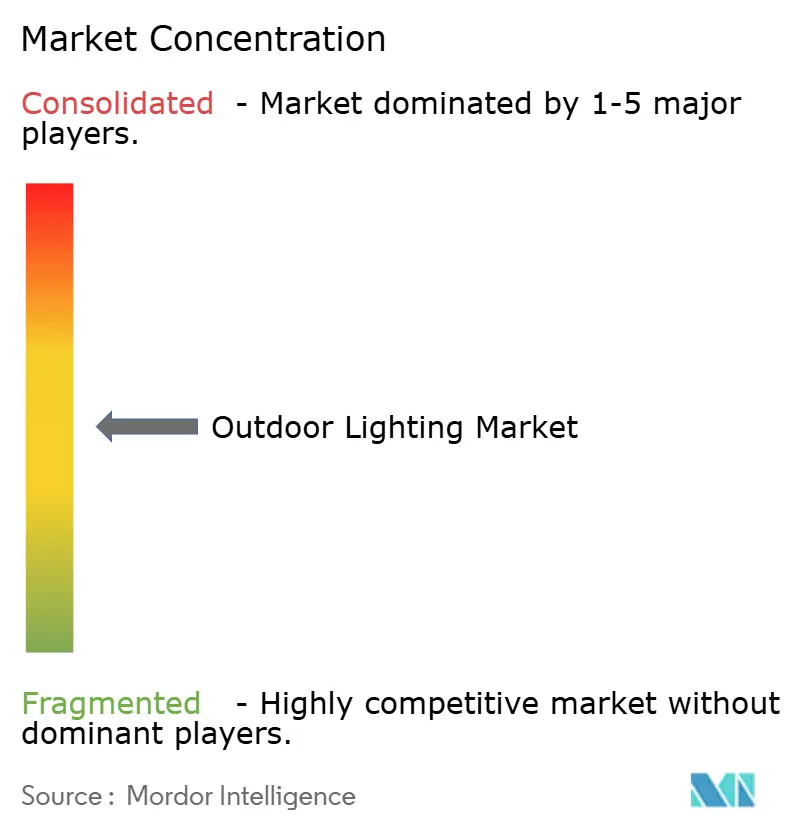

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Outdoor Lighting Market Analysis by Mordor Intelligence

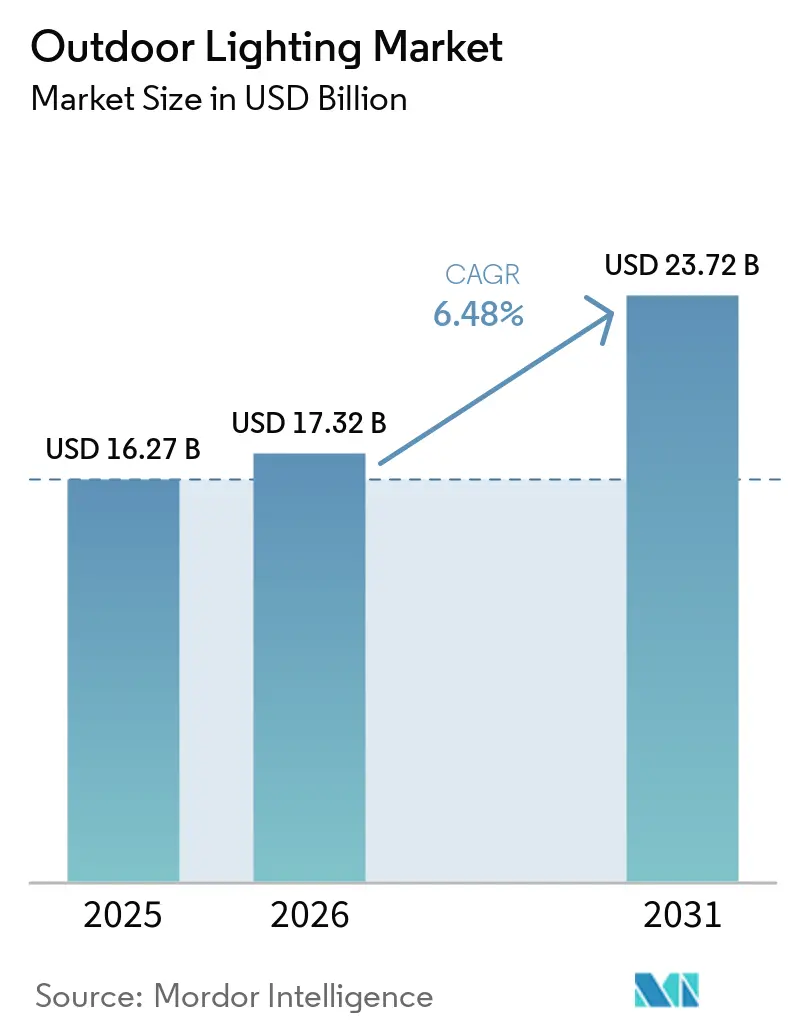

The outdoor lighting market size is projected to expand from USD 16.27 billion in 2025 and USD 17.32 billion in 2026 to USD 23.72 billion by 2031, registering a CAGR of 6.48% between 2026 and 2031. The outdoor lighting market is expanding as cities grow and invest in smart city infrastructure. Governments and municipalities are replacing older fixtures with energy‑efficient LED systems to cut costs and meet sustainability goals. The shift to connected lighting powered by IoT, motion sensors, and remote monitoring is improving uptime, reducing maintenance costs, and strengthening demand[1]Signify, “Connected Light Points Update,” Signify, signify.com. At the same time, homeowners are putting more emphasis on outdoor aesthetics for gardens, patios, and landscapes, which supports decorative and architectural lighting. New and upgraded infrastructure across highways, public spaces, and commercial areas also adds to demand. Product roadmaps continue to reflect interest in solar‑powered lighting, adaptive controls that adjust to conditions, and solutions aligned with carbon‑reduction targets, which together support long‑term growth.

Key Report Takeaways

- By product type, decorative lighting led with a 38.82% revenue share in 2025, while deck and patio lighting is projected to be the fastest-growing category at an 8.47% CAGR through 2031.

- By light source, LED technology held 68.36% share in 2025, and other light sources posted the highest growth outlook at 7.39% CAGR.

- By installation type, new installations accounted for 66.61% in 2025, while retrofit and replacement projects are expanding at 8.14% CAGR.

- By application, commercial use cases captured 65.53% of the market in 2025, and residential is the fastest-growing segment at a 7.10% CAGR.

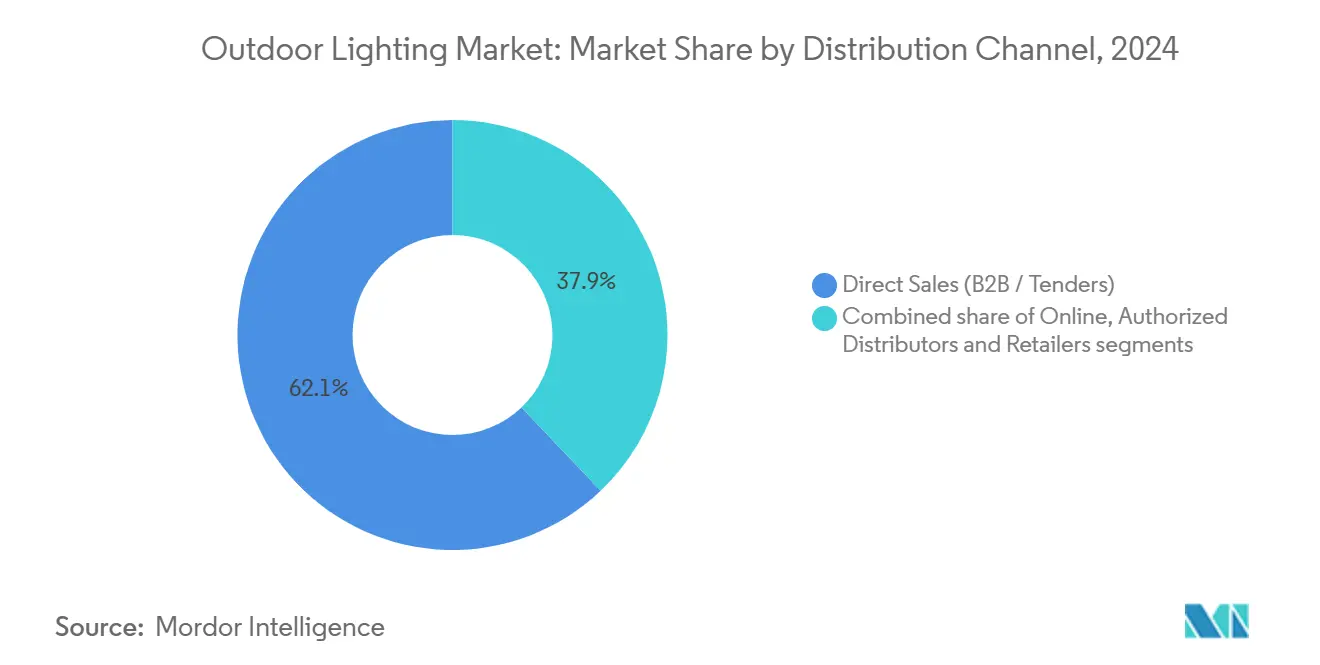

- By distribution channel, direct B2B sales retained 62.13% share in 2025, while online and direct-to-consumer channels are growing at 9.27% CAGR.

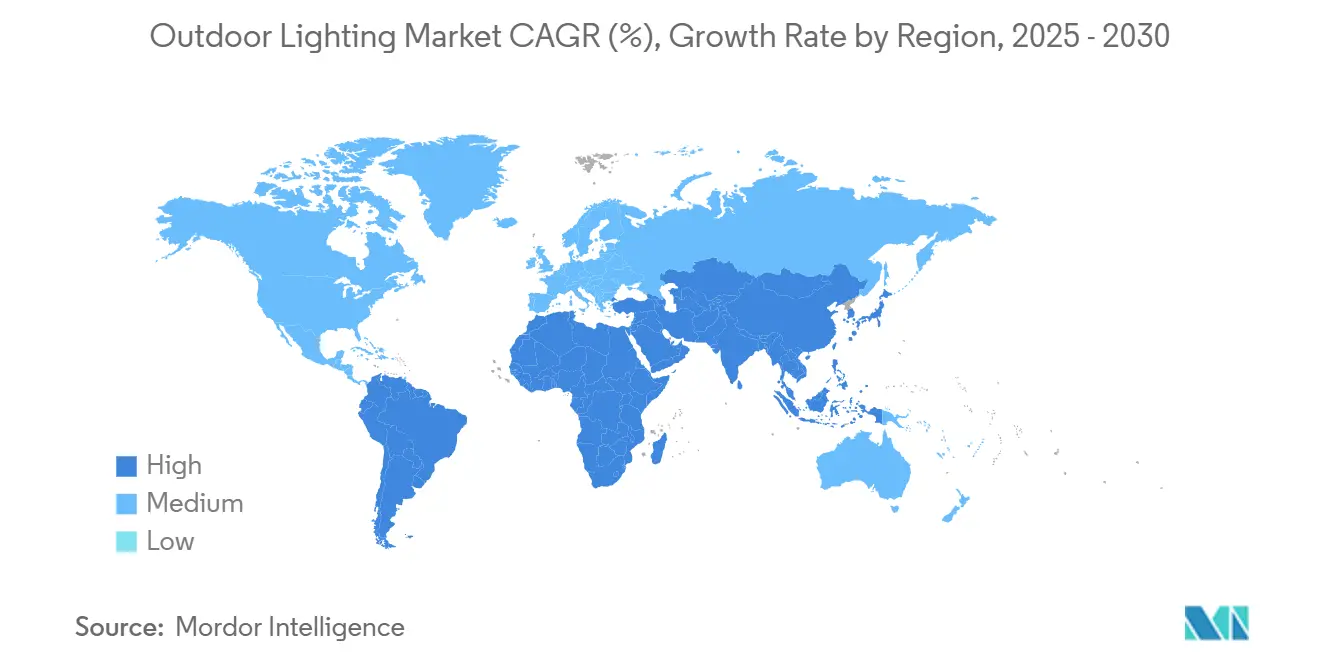

- By geography, North America led the outdoor lighting market with 37.85% share in 2025, and Asia-Pacific is the fastest-growing region with an 8.92% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Outdoor Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urbanization and Infrastructure Development | +1.3% | Global, with early gains in Asia-Pacific core cities, North America | Medium term (2-4 years) |

| Growing Demand for Energy-Efficient LED Solutions | +1.4% | North America, EU, Asia-Pacific | Short term (≤ 2 years) |

| Smart City Initiatives and IoT Integration | +1.1% | Global, spill-over to emerging markets | Medium term (2-4 years) |

| Rising Focus on Safety and Security | +0.9% | North America, EU, select Middle East markets | Medium term (2-4 years) |

| Government Support and Energy Efficiency Mandates | +1.2% | North America, EU, Middle East, Asia-Pacific | Short term (≤ 2 years) |

| Declining LED Prices and Technological Advancements | +0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Infrastructure Development

Cities are shifting from static grid-tied systems to modular, software-defined lighting that scales with growth and strengthens asset control. In March 2026, Los Angeles approved a two-year plan to deploy up to 60,000 solar roadway and area lights, the city’s largest single lighting investment, to address a backlog of 32,000 service requests and rampant wire theft that strained maintenance budgets. Hyderabad, India authorized an INR 1,340 crore (USD 161.4 million) program to modernize 760,000 streetlights with a Centralized Control and Monitoring System, performance-based penalties, and device-level tracking to lock in uptime and accountability. Pittsburgh combined Rescue Plan funds and bond proceeds to upgrade more than 35,000 fixtures with wireless management and illuminance analytics to cut energy use and reduce light spill. These actions reflect a pragmatic path for rapidly urbanizing regions that must combine new coverage, lifecycle savings, and measurable service levels. Hong Kong Trade Development Council sentiment data highlights India, ASEAN, and the Middle East as among the most promising near-term demand pools for suppliers aligned with public-infrastructure pipelines. Concentration of LED component manufacturing in Asia continues to underpin the scaling of such projects.

Growing Demand for Energy-Efficient LED Solutions

Minimum-efficacy rules and fast paybacks make LED the default across exterior categories. New York City’s 2025 Energy Conservation Code, effective March 2026, tightened lighting power density and made high-efficacy LED systems the practical path to compliance for most nonresidential interiors and exterior lighting[2]LightNOW Editors, “NYC 2025 Energy Conservation Code Highlights,” LightNOW, lightnowblog.com. California’s Title 24 updates in 2026 widened daylight-responsive coverage and required continuous dimming for multilevel control, pushing site and parking applications to networked LEDs with granular control. LED systems typically deliver 100–150 lumens per watt and can reduce energy use by 75–80% compared with legacy lamps, with smart controls further improving performance through scheduling, occupancy, and daylighting. A county-wide upgrade in West Sussex will convert 64,000 streetlights to LED and connect them to a remote monitoring platform, with annual savings projected at 10.7 million kWh and 1,633 tons of CO₂. Retrofit programs that reuse existing housing can preserve capital while harvesting energy savings, as shown by insert-based LED upgrades that recorded 45–51% reductions at scale.

Smart City Initiatives and IoT Integration

Outdoor lighting is becoming a digital platform that supports multiple municipal services. Signify reported 167 million connected light points at the end of 2025, up from 145 million a year earlier, underscoring the mainstreaming of connected luminaires and controls. Hyderabad’s citywide rollout embeds centralized monitoring, data capture, and enforcement tools, making uptime and service metrics integral to procurement and vendor management. Papendrecht, the Netherlands, demonstrated how LiDAR units mounted on lighting poles can replace multiple thermal cameras to monitor busy roundabouts, reduce pole counts, and improve detection of faster personal mobility devices. Pittsburgh is upgrading 35,000 fixtures to enable wireless management and advanced reporting to track real-time lighting conditions. TVilight’s CityManager deployments show how streetlights can be monitored and dimmed individually and also serve as hubs for air-quality and safety sensors, which introduces recurring software revenue for vendors. Municipalities in the Gulf have adopted remote management and programmable color for bridges and landmark structures, linking lighting with civic identity and sustainability goals.

Rising Focus on Safety and Security

Lighting upgrades are addressing crime, traffic risks, and public expectations for comfort. Los Angeles prioritized solar streetlights to eliminate vulnerable copper runs and close service gaps that had created dark zones, improving nighttime visibility for residents and road users. Security lighting products, especially LED flood and spot fixtures, are now specified with motion sensing and connectivity to deliver alerting and adaptive dimming for safer perimeters. West Sussex has paired LEDs with remote monitoring to shorten fault-to-fix cycles, which supports public safety outcomes and operational savings. Municipal projects in the Middle East are emphasizing improvements in visibility along high-traffic corridors and campuses, with authorities citing reduced maintenance and energy use as additional benefits. Warm-white color temperatures in the 2700K–3000K range are gaining traction because they support perceived safety and comfort while also aligning with many dark-sky standards. Institutional buyers continue to specify pathway and step lighting that meets accessibility requirements, which sustains steady retrofit activity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Installation and Retrofit Costs | -0.8% | Global, pronounced in cost-sensitive emerging markets | Short term (≤ 2 years) |

| Light Pollution and Environmental Concerns | -0.5% | North America, Western EU, select Asia-Pacific markets | Medium term (2-4 years) |

| Regulatory Compliance Pressures | -0.4% | North America, EU, Asia-Pacific | Medium term (2-4 years) |

| Supply Chain Vulnerabilities (e.g., Raw Material Price Fluctuations) | -0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Initial Installation and Retrofit Costs

Full smart-lighting projects can carry premium costs for controllers, gateways, and central software, stretching municipal budgets. Even straightforward conversions show the scale at play, such as a four-year West Sussex upgrade of 64,000 roadway fixtures for an estimated USD 30.7 million. Some owners offset this with policy tools and incentives, such as Portland’s dedicated funding for high-crash corridors and the U.S. 179D tax deduction, which compresses paybacks for large campuses and commercial properties. Nonetheless, long payback periods on fully networked systems and grant caps that limit project size can slow adoption in cash-constrained municipalities. Residential buyers face a similar hurdle for premium outdoor packages with smart features and solar storage, which can delay uptake in price-sensitive segments. Transaction frictions also increase costs, as many cities must define interoperability requirements and vet multi-vendor control stacks before awarding contracts.

Light Pollution and Environmental Concerns

Dark-sky compliance is pushing specifiers toward warmer color temperatures, full cutoffs, and after-hours dimming. Concerns over skyglow and glare have led many authorities to favor 2700K–3000K designs that balance safety and comfort while protecting nocturnal environments. This often adds design time, involves new photometric constraints, and can result in different fixture selections for ecologically sensitive or residential zones. Circularity and stewardship expectations are also rising, with extended producer responsibility frameworks and remanufacturing programs gaining momentum among leading suppliers. Municipalities in markets with tight standards are now procuring with lifecycle performance and end-of-life handling in scope, which increases vendor requirements. Off-grid programs in resource-constrained regions naturally limit over-illumination but introduce their own system design and maintenance considerations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Aesthetic Premium Drives Decorative Segment Growth

Decorative lighting led the category with 38.82% in 2025 as hospitality, campuses, and residential settings used designer forms and finishes to extend exterior experiences. The fastest-growing deck and patio segment is advancing at 8.47% CAGR, supported by residential upgrades where layered task, ambient, and accent lighting elevate outdoor living. Post and wall lights serve as both architectural accents and pathway illumination, while HoReCa venues specify IP-rated fixtures that balance visual appeal with weather resilience. Security lighting benefits from motion-activated controls and low-glare optics that tune output to activity while maintaining visual comfort. Warm-color garden and bollard fixtures continue to win in residential projects due to comfort and curb appeal requirements for evening use.

Demand in this segment reflects the outdoor lighting market's trend toward connected, low-maintenance, and curb-appeal solutions that enhance perceived safety and property value. Institutional buyers focus on vandal resistance and compliance with accessibility requirements in pathways and steps to reduce incidents and liability. In premium applications, high-CRI options help hospitality and public spaces maintain color fidelity for facades, landscaping, and art. The outdoor lighting market is also adopting formats for faster installation and serviceability, enabling projects to close faster with fewer site disruptions. Where data points are available, designers are aligning with dark-sky principles to control uplight while preserving ambiance.

By Light Source: LED Dominance Amid Emergent Alternative Technologies

LED technology captured 68.36% of the light source mix in 2025, reflecting superior efficacy, long life, and mature price points that continue to displace legacy lamps. Other light sources posted a 7.39% CAGR through 2026-2031 outlook from a smaller base, finding roles in specialty niches where LEDs have technical or aesthetic constraints. Regulatory phase-outs have accelerated the decline of fluorescent lamps, while new LED forms that emulate warm filament tones have further reduced demand for incandescent and halogen. In high-lumen stadium and long-throw applications, LEDs continue to expand their share as optical design, thermal management, and lumen density improve. OLED and laser-based solutions remain limited to specific design or performance briefs due to cost and reliability constraints in exterior settings.

With controls standardizing on interoperable protocols, planners can mix LED luminaires across brands while maintaining unified management layers that support reporting and optimization. The outdoor lighting market is also seeing better integration between luminaires and sensors to capture traffic, occupancy, and environmental data for municipal analytics. Field-serviceable components and modular drivers are helping large owners reduce downtime and carry fewer spares. As energy codes ratchet up, fixture efficacy and controllability will remain the main reasons LED technology maintains its dominance. Continued maturity in the LED ecosystem provides both buyers and integrators with stable performance and support baselines.

By Installation Type: Retrofit Economics Accelerate Replacement Cycle

New installations accounted for 66.61% in 2025, supported by greenfield developments, district-scale smart-city zones, and off-grid or hybrid solar projects that avoid trenching and grid tie-ins. Retrofit and replacement are the fastest-growing installation paths, with a 8.14% CAGR, as high-pressure sodium and metal halide fixtures approach the end of life and owners pursue cost and carbon reductions. Insert retrofits that reuse legacy housings have cut energy use by up to half in municipal pilots while reducing capital and e-waste. West Sussex’s program pairs LEDs with remote monitoring and expects multi-decade maintenance and energy savings, with rapid lamp-replacement cycles measured in minutes per location during rollout. Hyderabad’s tender structure ties payments to performance and data capture to ensure lighting uptime and serviceability.

New installs emphasize platforms and pathways that integrate future data applications at marginal added cost, which aligns with how the outdoor lighting market is becoming a sensor network at the edge. Retrofit projects often proceed in phases around budget and staffing constraints, which increases demand for controls that coexist with legacy devices. Large campuses and parking assets are tapping utility programs and 179D to tighten paybacks, with case studies showing strong outcomes when scope aligns with code and incentive structures. For theft-prone corridors, solar lighting is being piloted to eliminate susceptible copper runs. The outdoor lighting market's momentum here should hold as owners refresh older stock and integrate controls to improve visibility and accountability.

By Application: Commercial Scale Meets Residential Customization

Commercial applications represented 65.53% in 2025 across hospitality, retail, education, healthcare, sports, and cultural sites, where energy, visibility, and code compliance drive specification. Residential is the fastest-growing use case, with a 7.10% CAGR through 2026-2031, as homeowners upgrade landscapes, decks, and facades with warm, low-voltage LEDs and app-based controls. In commercial settings, integrated control stacks that connect lighting with building management, AV, and sustainability reporting are gaining traction. Sports and recreation projects prioritize glare control, instant-on capability, and broadcast-ready photometrics to upgrade user experience and reduce maintenance. Healthcare and campus environments are aligning exterior lighting with human-centric design to balance comfort and wayfinding.

The DIY segment is thriving through e-commerce channels, while professionally installed systems drive larger per-project value through design services and warranties. Smart-home integration across major platforms is improving ease of use, with consumer lines showing steady demand even where professional sales fluctuate. In institutional spaces, vandal-resistant, dark-sky-compliant products anchor long-term performance and reduce nuisance issues. As budgets spread across safety, ambiance, and sustainability, the outdoor lighting market provides targeted mixes of decorative, pathway, and security lighting to meet site goals. Commercial pathways continue to leverage incentives and controls to shorten paybacks and document performance.

By Distribution Channel: Direct Sales Lead as D2C Accelerates

Direct B2B channels and tenders captured 62.13% in 2025, reflecting municipal procurement and specification-led commercial projects that favor proven vendors and lifecycle-value bids. Online and D2C sales are the fastest-growing, with a 9.27% CAGR, as residential customers, small contractors, and showroom hybrids increasingly rely on digital discovery and fulfillment. Municipal tenders such as Hyderabad’s ₹1,340 crore (USD 161.4 million) program and West Sussex’s £24 million (USD 30.7 million) program underscore how processes, warranties, and data requirements shape award decisions. Electrical distributors provide financing and technical support to contractors, while agency networks influence specifications during renovation and new-build cycles.

On the consumer side, omnichannel strategies have taken hold across exhibitors and buyers, and some brands operate purely online with policies tailored to reduce friction in selection and returns. D2C sellers lean on design tools, video tutorials, and chat-based consultations to approximate in-store experiences and drive conversion. Marketplaces consolidate selection and price comparison, which can pressure margins and brand differentiation for commodity categories. The outdoor lighting market is evolving, packaging for parcel carriers, and smart products are simplifying setup to encourage DIY adoption. Professional e-commerce wholesalers support small contractor workflows with U.S.-based inventory and low minimums to keep projects on schedule.

Geography Analysis

North America led with 37.85% in 2025 as federal incentives, strong municipal pipelines, and mature distribution supported steady demand. Los Angeles approved the largest lighting investment in its history to deploy up to 60,000 solar streetlights that tackle theft and service backlogs. Pittsburgh set aside USD 15 million to manage more than 35,000 fixtures with wireless controls and enhanced reporting. Portland dedicated USD 37 million from a voter-backed fund specifically for LED streetlighting on high-crash corridors and powers the load with renewable energy. Commercial retrofits benefit from the 179D deduction, which has enabled large projects to pass payback hurdles through stacked incentives. Regional manufacturing footprints reduce tariff exposure and buffer logistics for United States-bound products.

Asia-Pacific is the fastest-growing region, with a 8.92% CAGR driven by smart-city spending, urban migration, and expanding residential investment. Hyderabad’s 760,000-light program couples centralized monitoring, fines for downtime, and complete asset traceability to enforce service levels. Manufacturing and packaging bases across Asia underpin cost and volume advantages for global projects during competitive tenders. Market sentiment surveys identify India, ASEAN, and the Middle East as priority destinations for suppliers growing footprints beyond incumbent regions. Municipalities in the Gulf are implementing remote management and multi-color systems for bridges and gateways while meeting sustainability targets. Cities like Amman are replacing thousands of lights with smart LEDs that support remote intensity control and fault reporting.

Europe shows steady activity as energy-efficiency rules and circularity ambitions steer procurement to LEDs and remanufacturable designs. West Sussex’s four-year program will replace 64,000 fixtures and integrate a monitoring system with expected long-term maintenance and energy benefits. Insert-based retrofits in Denmark reuse aluminum housings to cut both energy and embodied emissions at favorable returns. Phase-outs of legacy lamps accelerate commercial and industrial conversions that improve controls readiness. Some vendors are localizing assembly to shorten times and limit tariff exposure while upstream components remain globally sourced.

Middle East and Africa (MEA) spans advanced smart-city deployments and large-scale solar programs that improve electrification. Abu Dhabi City Municipality upgraded bridge lighting with remote management and programmable color for civic events, while meeting sustainability criteria. In Oman, Muscat Hills combined LED performance with RF mesh controllers and a central platform to improve reliability and save energy. Ghana’s program to deploy tens of thousands of solar streetlights aims to reduce peak loads and relieve grid pressure. Sub-Saharan markets often emphasize off-grid and hybrid systems to avoid trenching and reduce reliance on diesel. In contrast, GCC markets align more closely with codes and standards adopted from global best practice. South Africa’s load-shedding challenges are creating niches for off-grid public lighting with local maintenance capacity.

South America shows modest growth as urban retrofits progress where funding and stability allow. Brazilian cities leverage national programs and multilateral finance to expand LED streetlighting in high-crime districts. Chile integrates solar streetlights for remote and mining-adjacent communities with high solar resources. Macroeconomic volatility in some markets has slowed municipal procurement, though pockets of private demand persist in commercial districts. Fragmented standards and local-content policies complicate cross-border supply chains and specifications. The outdoor lighting market remains opportunity-rich, with safety, power costs, and reliability gains aligning with access to funding.

Competitive Landscape

Global incumbents such as Signify, Acuity Brands, ams OSRAM, and Zumtobel anchor coverage with broad portfolios, distribution depth, and integrated controls. Signify initiated a USD 192.6 million cost-reduction program affecting 900 roles in January 2026 to protect profitability after a year of softer demand and pricing pressure in parts of Europe. The company’s long-term sustainability program targets cumulative energy savings for customers and a bigger share of circular revenues by 2030 through remanufacturing and service-led offers[3]Signify Press Office, “Cost Reduction Program and Sustainability Goals,” Signify, signify.com. Acuity Brands expanded total revenue in fiscal 2025 to USD 4.3 billion, while lighting grew modestly organically and platform adjacencies drove stronger gains. Its strategy integrates building controls, sustainability software, and AV control platforms to frame lighting within a larger intelligent space stack[4]Acuity Brands Investor Relations, “FY2025 Results and Strategy,” Acuity Brands, acuitybrands.com.

Software-led revenue is rising as municipalities and enterprises seek monitoring, analytics, and lifecycle services. TVilight’s CityManager highlights the shift from point hardware to fleet management and third-party integrations on lighting networks. Retrofit specialists like Luxega demonstrate how insert-based solutions unlock circular benefits and bypass full fixture replacements with strong energy reductions. Solar-focused players in off-grid segments are expanding in regions where trenching and grid interconnect are impractical or cost-prohibitive. Manufacturers that standardize on open protocols such as D4i, DALI-2, TALQ, and Zhaga reduce lock-in concerns and maintain specification pull.

Channel dynamics remain important for reach and service delivery. Brands that maintain strong agency networks and distributor relationships protect their specification positions and provide after-sales support for public-sector and corporate buyers. Domestic manufacturing bases support lead-time reliability and tariff resilience for North American demand. Consumer-facing lines in smart outdoor lighting held up for leaders even as broader professional categories softened under price pressure. Partnerships that link lighting with sports, events, and venue experiences continue to raise brand equity in performance and connected capabilities. Vendors with credible cybersecurity and circular credentials stand out in municipal tenders that price lifecycle compliance alongside capital cost.

Outdoor Lighting Industry Leaders

Signify (Philips Lighting)

Acuity Brands Lighting

Hubbell Lighting

ams OSRAM

Cooper Lighting Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Signify launched “Brighter Lives, Better World 2030,” targeting 60 TWh cumulative customer energy savings, 35% portfolio CO₂ intensity reduction, and growth in circular revenues to 27.5% of sales by 2030 for professional customers in Europe.

- March 2026: Los Angeles announced a two-year initiative to repair and replace up to 60,000 solar-powered streetlights, the city’s largest investment in lighting infrastructure, to resolve 32,000 outstanding service requests and deter wire theft.

- March 2026: West Sussex County Council began a four-year, USD 30.7 million program to replace around 64,000 streetlights with LEDs and smart control nodes connected to a Remote Monitoring System, with annual savings projected at 10.7 million kWh and 1,633 tons of CO₂.

Global Outdoor Lighting Market Report Scope

| Decorative lighting | |

| Post lights | |

| Wall lights | Hanging lights |

| Chandeliers | |

| Others (flush mounts, etc.) | |

| Path & step lights | |

| Deck & patio lights | |

| Garden lights | |

| Security lighting | |

| Flood & spotlights | |

| Bollard | |

| Others (rope lights, string lights, etc.) |

| LED |

| Fluorescent |

| Incandescent |

| Halogen |

| Other Light Sources (HID, OLED, laser, etc.) |

| New Installations |

| Retrofit / Replacement |

| Residential |

| Commercial (HoReCa, Sports centers, Healthcare, Retail, Institutional, and Others (galleries/museums, corporates, etc.)) |

| Direct Sales (B2B / Tenders) |

| Online / D2C |

| Authorized Distributors & Retailers |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product Type | Decorative lighting | |

| Post lights | ||

| Wall lights | Hanging lights | |

| Chandeliers | ||

| Others (flush mounts, etc.) | ||

| Path & step lights | ||

| Deck & patio lights | ||

| Garden lights | ||

| Security lighting | ||

| Flood & spotlights | ||

| Bollard | ||

| Others (rope lights, string lights, etc.) | ||

| By Light Source | LED | |

| Fluorescent | ||

| Incandescent | ||

| Halogen | ||

| Other Light Sources (HID, OLED, laser, etc.) | ||

| By Installation Type | New Installations | |

| Retrofit / Replacement | ||

| By Application | Residential | |

| Commercial (HoReCa, Sports centers, Healthcare, Retail, Institutional, and Others (galleries/museums, corporates, etc.)) | ||

| By Distribution Channel | Direct Sales (B2B / Tenders) | |

| Online / D2C | ||

| Authorized Distributors & Retailers | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the outdoor lighting market size and growth outlook through 2031?

The outdoor lighting market size is USD 16.27 billion in 2025 and is projected to reach USD 23.72 billion by 2031 at a 6.48% CAGR.

Which region leads, and which grows the fastest, in outdoor lighting?

North America leads with 37.85% in 2025, while Asia-Pacific is the fastest-growing region at 8.92% CAGR through 2026-2031.

Which applications dominate demand in outdoor lighting?

Commercial use cases account for 65.53% in 2025, with residential growing the fastest as homeowners invest in smart, warm, and low-voltage exterior lighting.

What is driving the rapid shift to connected LEDs in outdoor lighting?

Energy codes, tax incentives, and IoT platforms are the main drivers, with 167 million connected light points reported by the end of 2025 and strong municipal programs underway.

How are cities funding large-scale outdoor lighting upgrades?

Cities use a mix of federal or state grants, tax deductions like 179D, and dedicated local funds, such as Portland’s PCEF allocation, to LED streetlighting.

Page last updated on: