Outsourced Semiconductor Assembly And Test (OSAT) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

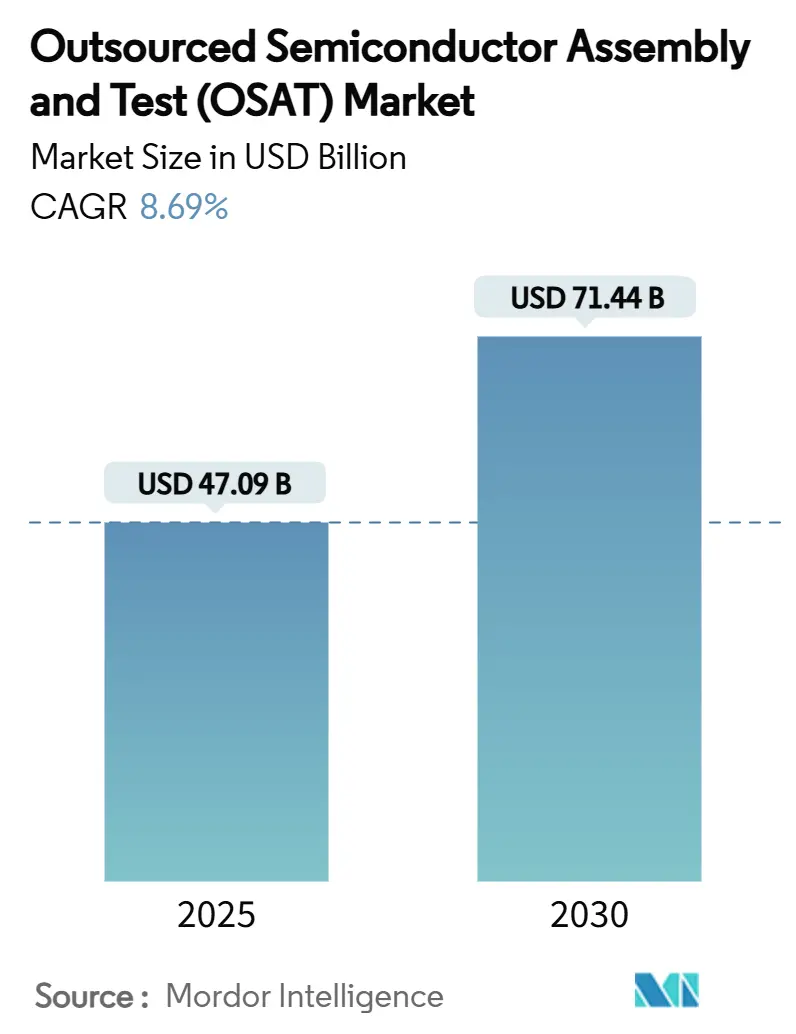

| Market Size (2025) | USD 47.09 Billion |

| Market Size (2030) | USD 71.44 Billion |

| Growth Rate (2025 - 2030) | 8.69% CAGR |

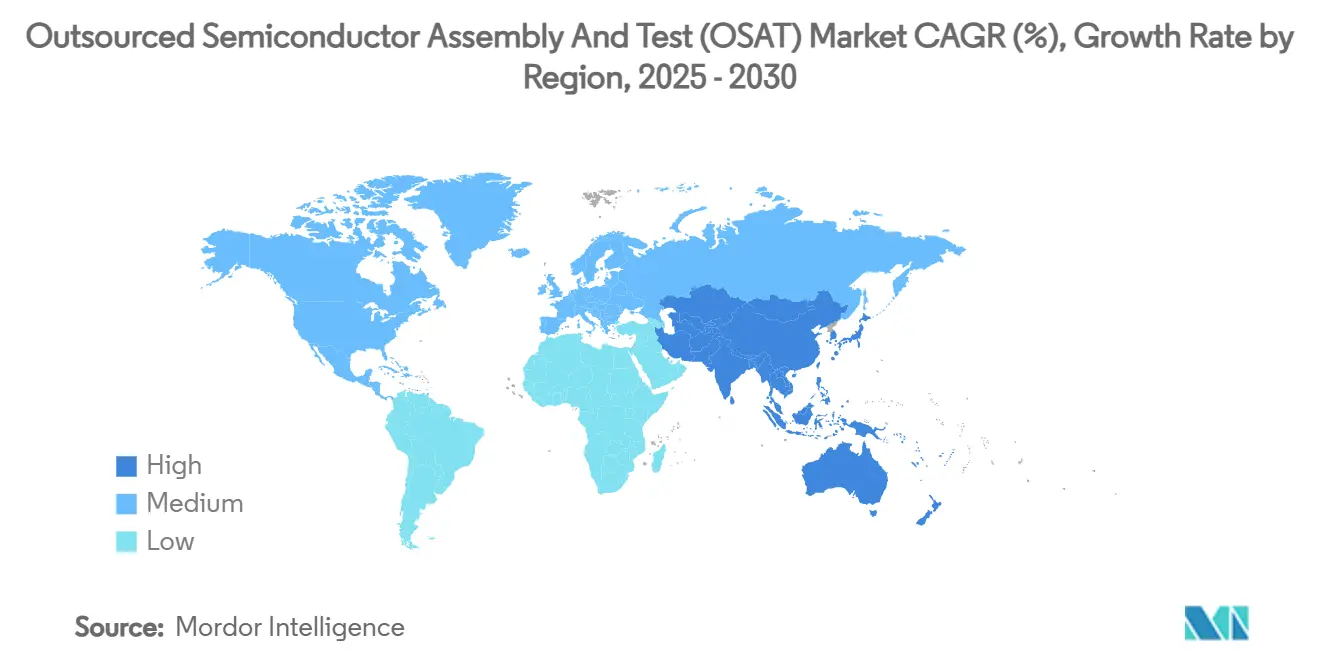

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

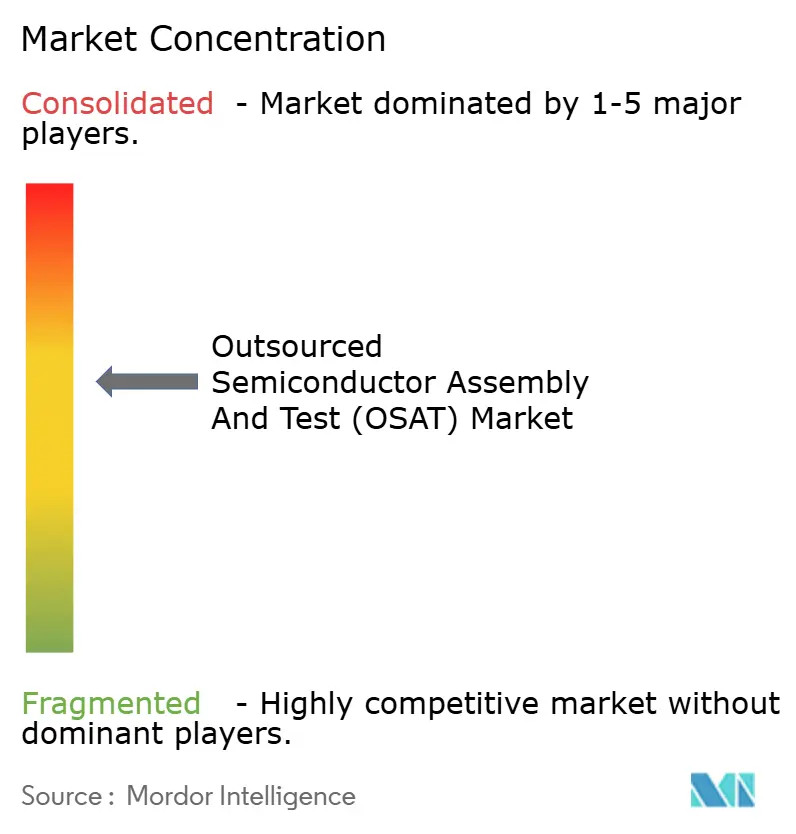

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Outsourced Semiconductor Assembly And Test (OSAT) Market Analysis by Mordor Intelligence

The outsourced semiconductor assembly and test market size reached USD 47.09 billion in 2025 and is forecast to attain USD 71.44 billion by 2030, advancing at an 8.69% CAGR. Sustained progress in artificial intelligence, high-performance computing, and automotive electrification raised demand for advanced packages and safety-critical test flows, thereby widening the total addressable opportunity for specialized backend service providers. Asia-Pacific suppliers preserved pricing leverage owing to mature ecosystems, yet policy-driven capacity build-outs in North America and Europe began to reshape global supply allocation. Hybrid chiplet architectures elevated the importance of heterogeneous integration, motivating strategic investments in fan-out wafer-level and 2.5D/3D platforms. Meanwhile, tighter trade controls and sustainability mandates encouraged customers to shift part of the workload to geographically diversified sites that can demonstrate lower energy use per unit throughput. As foundry capacity remained strained, fab-lite semiconductor companies continued to outsource backend steps, reinforcing the structural relevance of the outsourced semiconductor assembly and test market in the next planning cycle.

Key Report Takeaways

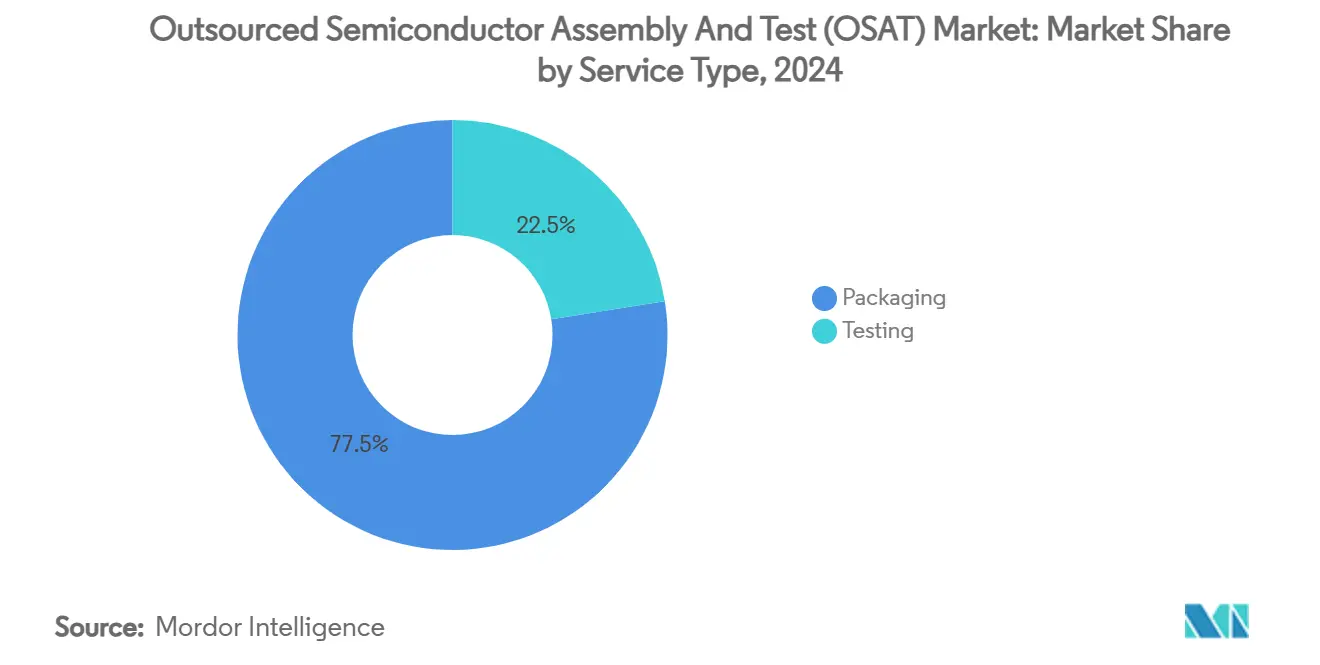

- By service type, packaging accounted for 77.5% revenue in 2024; testing is forecast to rise at a 10.8% CAGR to 2030.

- By packaging type, ball grid array held 24.3% of outsourced semiconductor assembly and test market share in 2024, while fan-out wafer-level packaging is projected to expand at an 11.5% CAGR through 2030.

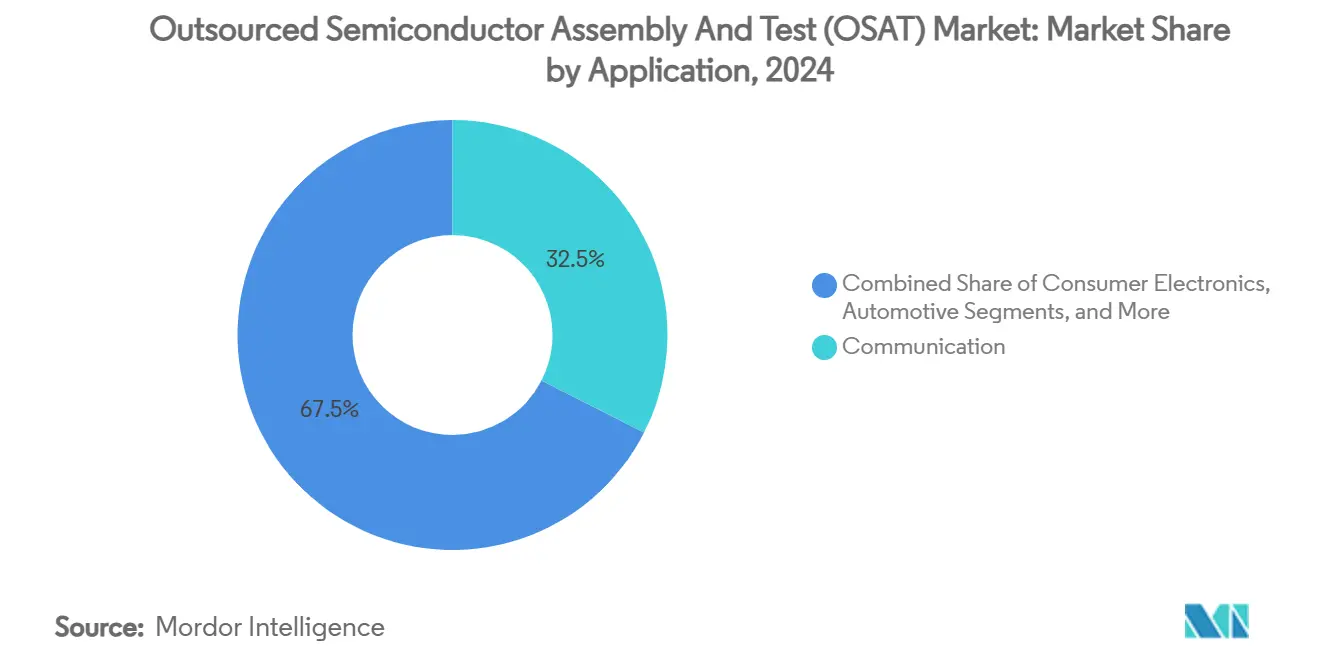

- By application, communication led with 32.5% revenue share in 2024; automotive is advancing at a 13.4% CAGR to 2030.

- By technology node, legacy nodes (≥28 nm) represented 46.3% of the outsourced semiconductor assembly and test market size in 2024; sub-5 nm nodes are growing at a 15.1% CAGR through 2030.

- By geography, Asia-Pacific commanded 73.5% revenue in 2024; its 9.6% CAGR through 2030 reflects persistent leadership despite diversification moves.

Global Outsourced Semiconductor Assembly And Test (OSAT) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring semiconductor content per vehicle | +1.8% | Global, with concentration in Germany, Japan, the US, and China | Medium term (2-4 years) |

| 5G-led demand for advanced RF packages | +1.2% | Global, with early adoption in South Korea, China, US | Short term (≤ 2 years) |

| AI/HPC chiplet architectures needing heterogeneous integration | +2.1% | Global, with concentration in Taiwan, the US, and China | Medium term (2-4 years) |

| Foundry capacity shortages driving fab-lite outsourcing | +1.5% | Global, with spillover effects in Southeast Asia | Short term (≤ 2 years) |

| U.S. CHIPS and EU Chips Acts incentivising local OSAT build-out | +0.9% | North America and EU, with supply chain effects in Asia | Long term (≥ 4 years) |

| Sustainability mandates are pushing wafer-level fan-out adoption | +0.7% | Global, with regulatory leadership in the EU, California | Medium term (2-4 years) |

Source: Mordor Intelligence

Soaring Semiconductor Content Per Vehicle

Automotive OEMs transitioned toward software-defined platforms, lifting semiconductor bill-of-materials per car and intensifying demand for high-reliability packages. Volkswagen Group’s traction inverter partnership with onsemi highlighted the rising adoption of silicon carbide devices that need thermally robust power packages.[1]onsemi, “Volkswagen Group Selects onsemi Silicon Carbide Traction Inverter,” onsemi.com Imec’s Automotive Chiplet Program, supported by ASE, BMW, and Bosch, illustrated cross-value-chain alignment on standardized chiplet packaging for functional safety compliance. OSAT providers that qualify to AEC-Q100 and ISO 26262, therefore, captured new design wins and secured multiyear capacity reservations with electric-vehicle suppliers.

5G-Led Demand for Advanced RF Packages

Commercial 5G base-station roll-outs moved the radio front-end into millimetre-wave territory, necessitating low-loss substrates, conformal shielding, and compact SiP footprints. Finwave Semiconductor’s E-mode MISHEMT integration at GlobalFoundries signalled commercial deployment of novel gallium-nitride devices that require specialised RF packaging, with mass qualification targeted for 2026. The pipeline for 6G testbeds already incorporates co-packaged optics, urging OSAT firms to expand mixed-signal assembly capabilities and advanced thermal solutions.

AI/HPC Chiplet Architectures Needing Heterogeneous Integration

As monolithic die scalability reached economic limits, chiplet partitioning prevailed across AI accelerators and data-centre CPUs. ASE’s VIPack platform demonstrated active-silicon bridges and hybrid bonding routes that enable efficient chiplet integration while shortening time-to-yield. Intel’s EMIB and Foveros offerings positioned foundry services in direct competition, yet many fab-less customers continued to leverage independent OSAT houses for volume production verification. The outsourced semiconductor assembly and test market widened because multi-die modules required specialised reliability tests such as thermal-coupled structural analysis that only a handful of vendors currently provide.

Foundry Capacity Shortages Driving Fab-Lite Outsourcing

Global foundry utilisation stayed elevated despite record capital expenditure, pushing device makers to adopt fab-lite models in which backend operations are fully outsourced. SEMI projected USD 400 billion in 300 mm equipment spending through 2027, yet near-term supply-demand imbalance persisted, sending further assembly volumes to Southeast Asian OSAT clusters. Equipment suppliers forecast 34.9% growth in assembly-tool sales for 2025, underscoring the urgent need for incremental backend capacity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vertical integration by leading foundries and IDMs | -1.4% | Global, with concentration in Taiwan, South Korea, US | Medium term (2-4 years) |

| Cap-ex intensity and long equipment lead times | -0.8% | Global, with particular impact on emerging markets | Short term (≤ 2 years) |

| Geopolitical export controls on advanced tools | -0.6% | Global, with a focus on China-US technology restrictions | Medium term (2-4 years) |

| Skilled-labour shortages in advanced packaging engineering | -0.5% | Global, with acute impact in developed markets | Long term (≥ 4 years) |

Source: Mordor Intelligence

Vertical Integration by Leading Foundries and IDMs

TSMC’s Wafer Manufacturing 2.0 strategy integrated packaging and testing flows, offering turnkey services that reduced addressable volume for stand-alone OSAT companies. Samsung pursued a similar path, while Intel grew its foundry services to include advanced interposers. These moves compressed third-party share in high-margin segments and obliged OSAT firms to double down on niches such as automotive safety or photonics.

Cap-Ex Intensity and Long Equipment Lead-Times

A new advanced packaging line can require USD 100-200 million and 12-18 months for tool delivery, hurdles that deter smaller entrants. ASMPT’s FY 2023 revenue decline illustrated cyclical headwinds that constrained reinvestment capacity during downturns. Emerging locations in India and Vietnam faced even steeper procurement cycles because Japanese material suppliers prioritised long-standing customers, slowing competitive catch-up.

Segment Analysis

By Service Type: Testing Momentum Accelerates on AI Validation

Testing captured a 10.8% CAGR forecast for 2025-2030, a pace outstripping packaging’s expansion yet starting from a smaller base. AI and high-performance computing designs demanded system-level test coverage that verifies chiplet interconnect latency, dynamic thermal throttling, and deep-learning workload performance under varied voltages. The outsourced semiconductor assembly and test market responded by integrating adaptive machine-learning algorithms in automatic test equipment, cutting test time while improving fault isolation.

Packaging retained 77.5% of 2024 revenue, but its composition evolved toward fan-out panel-level, 2.5D interposer, and co-packaged optics lines. As customers consolidated suppliers, OSAT groups bundled turnkey offerings that merge fixture design, final test, and logistics. Advantest secured its sixth consecutive leadership in assembly test equipment after adding AI-enabled analytics to its V93000 series.[2]Advantest Corporation, “Advantest Ranks Global #1 in Assembly Test Equipment Supplier,” advantest.com

Note: Segment shares of all individual segments available upon report purchase

By Packaging Type: Fan-Out WLP Captures Advanced-Node Designs

Ball grid array technology maintained a 24.3% share in 2024 by serving mainstream consumer and industrial platforms that value mechanical robustness. However, fan-out wafer-level packages expanded at 11.5% CAGR as mobile processors and AI accelerators transitioned to high-density redistribution layers. This trend strengthened the outsourced semiconductor assembly and test market because only a limited pool of vendors can process larger panel formats without yield drift.

ASE’s USD 200 million panel-level expansion to 310 mm × 310 mm glass panels illustrated a cap-ex commitment toward cost-effective, large-area builds. Through-silicon-via and through-glass-via variants proliferated in high-bandwidth memory stacks. FC-BGA substrates benefited from advanced node adoption, bridging the gap between organic laminates and silicon interposers for networking ASICs.

By Application: Automotive Electrification Spurs Packaging Innovation

Communication systems dominated with 32.5% revenue in 2024, reflecting sustained 5G macro rollout and handset refresh demand. Yet electrified powertrains and ADAS modules pushed automotive to the top of the growth tables at a 13.4% CAGR. The outsourced semiconductor assembly and test market size for automotive modules is projected to eclipse USD xx billion by 2030 (specific value not disclosed), supported by long-term supply agreements that guarantee capacity for silicon carbide and radar chips.

onsemi’s acquisition of Qorvo’s silicon-carbide JFET portfolio for USD 115 million underscored the race to secure differentiated power devices. Industrial smart-factory projects and edge AI also raised backend demand, but their shares remained lower than the mobility and communication segments.

By Technology Node: Advanced Nodes Outpace Legacy but Dual Track Persists

Legacy geometries ≥28 nm still composed 46.3% of the outsourced semiconductor assembly and test market size in 2024, serving analog, power management, and automotive microcontrollers. They retained sticky share due to mature tooling and extended product lifecycles. In parallel, sub-5 nm nodes grew at 15.1% CAGR, driven by AI training accelerators, premium smartphones, and data-centre CPUs.

Siemens released Tessent Hi-Res Chain test software to curb yield loss at 5 nm and below, showcasing that backend test innovation must match front-end scaling. OSATs, therefore, built cleanroom zones with finer contamination control and advanced lithography debonding flows to handle ultra-thin dies that conventional package lines cannot sustain.

Geography Analysis

Asia-Pacific retained 73.5% share of outsourced semiconductor assembly and test market revenue in 2024 and posted a 9.6% CAGR outlook through 2030. Taiwan, China, and South Korea anchored the cluster owing to proximity to foundries and substrate makers, yet escalating trade frictions prompted diversification into Malaysia, Vietnam, and the Philippines. India accelerated incentive programmes, endorsing Kaynes Technology’s USD 413 million plant in Gujarat and Tata Electronics’ USD 3 billion Assam package-test complex.[3]Evertiq, “Indian Government Approves Kaynes’ USD 413 Million Chip Plant,” evertiq.com

North America regained strategic weight following the CHIPS Act funding. Amkor broke ground on an advanced packaging facility in Arizona designed to supply domestic automotive and AI customers. Texas Instruments earmarked USD 60 billion for multiple wafer fabs and corresponding backend capacity, while SkyWater’s USD 93 million acquisition of Infineon’s Austin fab added sovereign redundancy.

Europe moved from niche R&D toward scaled production. Silicon Box obtained EU approval for a EUR 1.3 billion (USD 1.47 billion) panel-level plant in Italy, targeting >100 million SiP units per year. Thales, Radiall, and Foxconn explored a French OSAT alliance to serve defence and aeronautics users. Onsemi committed USD 2 billion to a silicon-carbide line in the Czech Republic, assuring local supply for e-mobility projects. The Middle East and Africa remained an emerging frontier, with Israel and the UAE assessing policy frameworks to attract backend investors.

Competitive Landscape

The top three suppliers—ASE Technology, Amkor Technology, and JCET—held roughly 45-50% of revenue in 2024, indicating moderate concentration. ASE reported NT$595.410 billion (USD 18.6 billion) revenue, buoyed by AI and communication orders despite margin pressure.[4]StockTitan, “ASE Technology Reports Mixed Q4 Results,” stocktitan.net Amkor pursued regional diversification through its Arizona site and a joint project with GlobalFoundries in Portugal, aimed at European automakers. JCET secured record revenue after deepening automotive engagements and expanding SiP capacity in Jiangsu.

Competition is intensifying as foundries integrate backend offerings. TSMC’s 3DFabric positioned the firm as a one-stop advanced-packaging supplier, challenging OSAT pricing power. OSAT groups are countering by investing in heterogeneous integration, photonics, and automotive safety packages. Government subsidies also lowered entry barriers for newcomers in India and Vietnam, who leverage strategic partnerships to fast-track technology transfer.

Strategic moves included ASE’s cooperation with TSMC on panel-level processes, Amkor’s CHIPS Act grant that anchored domestic US capacity, and SkyWater’s purchase of Infineon’s Austin factory to broaden prototype-to-production pathways. Players are shifting from cost competition toward differentiated value propositions such as co-packaged optics assembly, machine-learning-driven test optimisation, and circular-economy material flows.

Outsourced Semiconductor Assembly And Test (OSAT) Industry Leaders

-

ASE Technology Holding Co. Ltd

-

Amkor Technology Inc.

-

Powertech Technology Inc.

-

ChipMOS Technologies Inc.

-

King Yuan Electronics Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: TSMC and ASE intensified panel-level packaging race; ASE invested USD 200 million in 310 mm×310 mm panels for AI chips.

- July 2025: SkyWater acquired Infineon’s Austin plant for USD 93 million to bolster US sovereignty.

- June 2025: Texas Instruments announced USD 60 billion for seven US fabs, the largest domestic commitment on record.

- May 2025: Thales, Radiall, and Foxconn started talks for a French OSAT site, surpassing EUR 250 million.

Global Outsourced Semiconductor Assembly And Test (OSAT) Market Report Scope

OSAT companies offer third-party integrated circuit (IC) packaging and test services. These companies provide packaging for silicon devices made by foundries and test the devices before shipping. They focus on offering innovative packaging and test solutions for semiconductor companies in well-established markets, such as communications, consumers, and computing, as well as emerging markets, such as automotive electronics, the Internet of Things (IoT), and wearable devices.

The outsourced semiconductor assembly and test services (OSAT) market is segmented by service type (packaging and testing), type of packaging (ball grid array packaging, chip-scale packaging, stacked die packaging, multi-chip packaging, and quad flat and dual-inline packaging [only qualitative analysis is included]), application (communication, consumer electronics, automotive, computing and networking, industrial, and other applications), and geography (United States, China, Taiwan, South Korea, Malaysia, Singapore, Japan, and Rest of the World). The report includes market forecasts and size in value in USD for all the above segments.

| By Service Type | Packaging | |||

| Testing | ||||

| By Packaging Type | Ball Grid Array (BGA) | |||

| Chip-Scale Package (CSP) | ||||

| Quad Flat / Dual-Inline (QFP/DIP) | ||||

| Multi-Chip Module (MCM) | ||||

| Wafer-Level Packaging (WLP) | ||||

| Fan-Out Packaging (FO-WLP / FO-BGA) | ||||

| System-in-Package (SiP) | ||||

| Through-Silicon Via (2.5D/3D TSV) | ||||

| Flip-Chip (FC-BGA / FC-CSP) | ||||

| By Application | Communication | |||

| Consumer Electronics | ||||

| Automotive | ||||

| Computing and Networking | ||||

| Industrial | ||||

| Other Applications | ||||

| By Technology Node | ≥28 nm | |||

| 16/14 nm | ||||

| 10/7 nm | ||||

| 5 nm and below | ||||

| Legacy (90-65 nm) | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| France | ||||

| United Kingdom | ||||

| Italy | ||||

| Netherlands | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Taiwan | ||||

| South Korea | ||||

| Japan | ||||

| Singapore | ||||

| Malaysia | ||||

| India | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | Israel | ||

| United Arab Emirates | ||||

| Saudi Arabia | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Rest of Africa | ||||

| Packaging |

| Testing |

| Ball Grid Array (BGA) |

| Chip-Scale Package (CSP) |

| Quad Flat / Dual-Inline (QFP/DIP) |

| Multi-Chip Module (MCM) |

| Wafer-Level Packaging (WLP) |

| Fan-Out Packaging (FO-WLP / FO-BGA) |

| System-in-Package (SiP) |

| Through-Silicon Via (2.5D/3D TSV) |

| Flip-Chip (FC-BGA / FC-CSP) |

| Communication |

| Consumer Electronics |

| Automotive |

| Computing and Networking |

| Industrial |

| Other Applications |

| ≥28 nm |

| 16/14 nm |

| 10/7 nm |

| 5 nm and below |

| Legacy (90-65 nm) |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Taiwan | |||

| South Korea | |||

| Japan | |||

| Singapore | |||

| Malaysia | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Israel | |

| United Arab Emirates | |||

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the outsourced semiconductor assembly and test market?

The outsourced semiconductor assembly and test market stood at USD 47.09 billion in 2025 and is projected to reach USD 71.44 billion by 2030.

Which region leads the outsourced semiconductor assembly and test market?

Asia-Pacific led with 73.5% revenue share in 2024, supported by mature supply chains and proximity to foundries.

Why is fan-out wafer-level packaging growing so quickly?

Fan-out wafer-level packaging offers compact form factors and high-density interconnects required by AI accelerators and mobile processors, driving an 11.5% CAGR through 2030.

How are automotive trends influencing OSAT services?

Rising semiconductor content per vehicle and the shift to electric powertrains pushed automotive-focused packaging and testing demand at a 13.4% CAGR, creating long-term contracts for safety-qualified OSAT providers.

What risks could slow market expansion?

Vertical integration by large foundries and high capital expenditure requirements may trim third-party growth, potentially shaving 1.4% from forecast CAGR over the medium term.

Page last updated on: July 11, 2025