Optical Transport Network Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

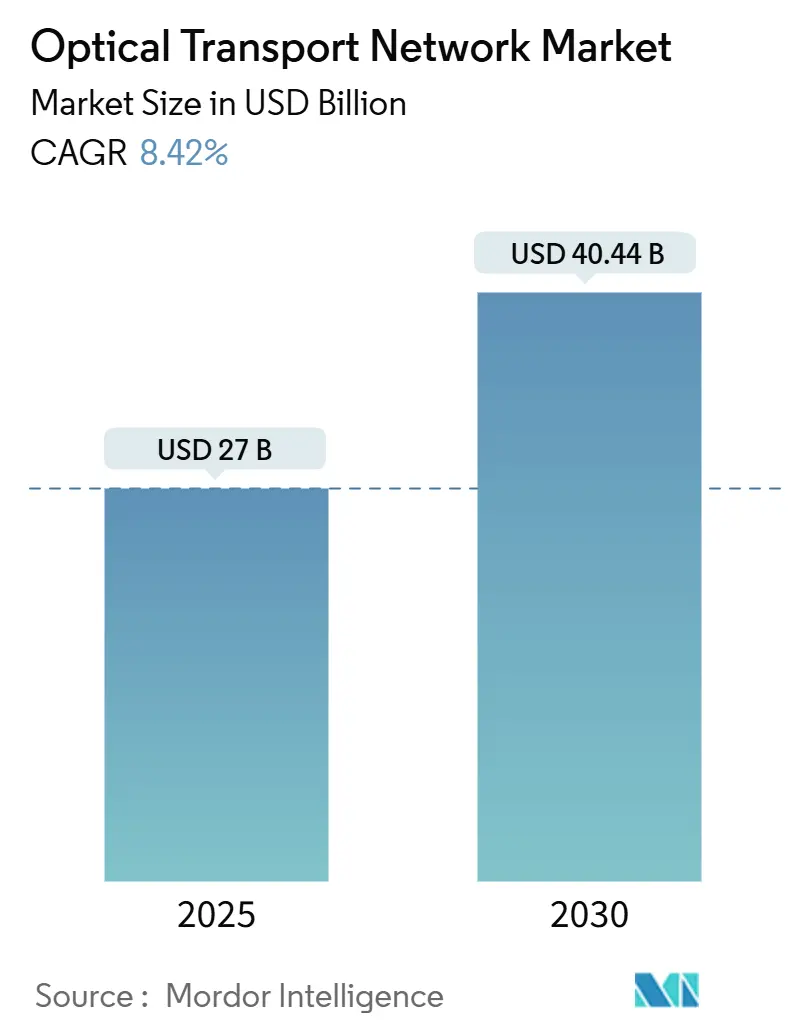

| Market Size (2025) | USD 27 Billion |

| Market Size (2030) | USD 40.44 Billion |

| Growth Rate (2025 - 2030) | 8.42% CAGR |

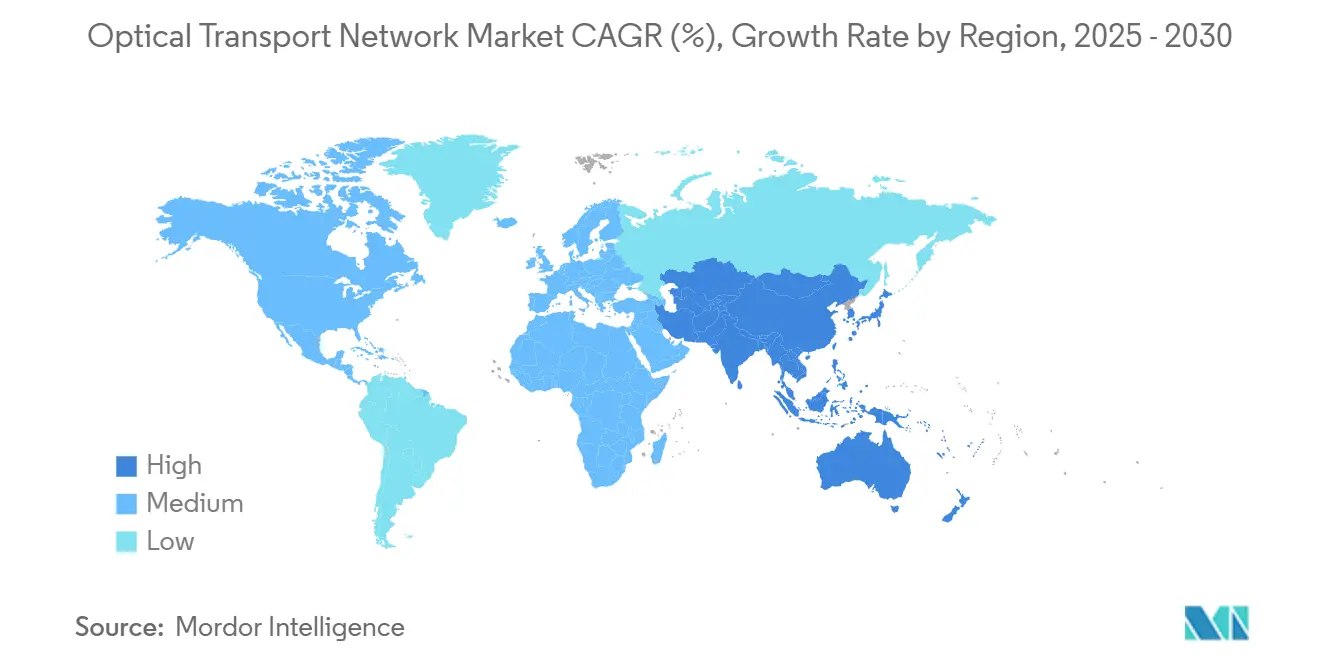

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

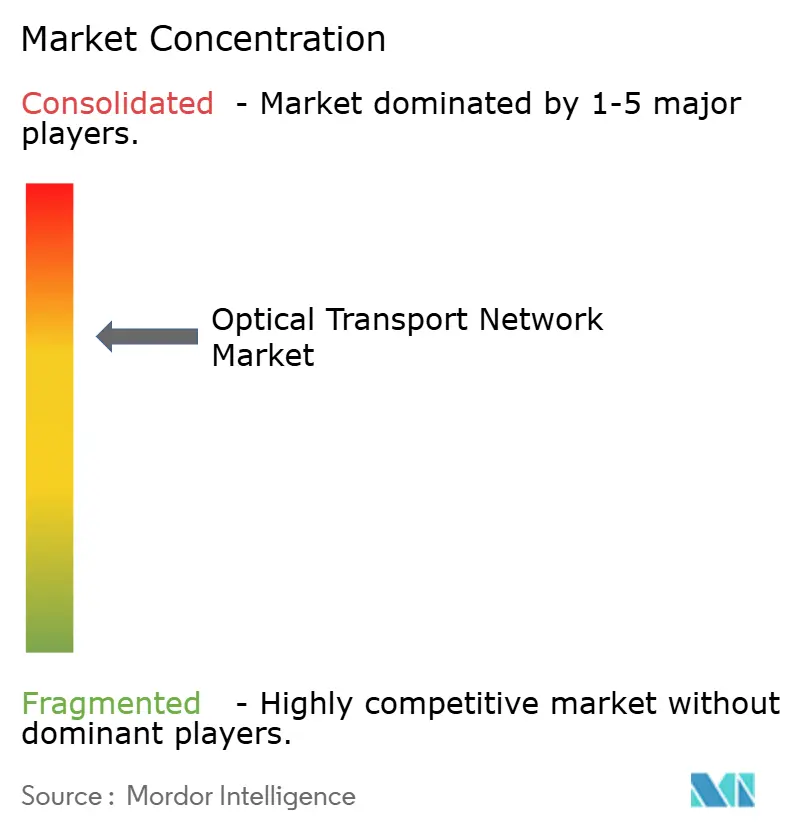

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Optical Transport Network Market Analysis by Mordor Intelligence

The optical transport network market is valued at USD 27 billion in 2025 and is on track to reach USD 40.44 billion by 2030, translating into an 8.42% CAGR. Rising data-center-interconnect bandwidth, the commercialization of 400ZR/ZR+ coherent pluggables, and government-funded fiber rollouts are guiding this expansion. Hyperscalers alone expect to channel USD 215 billion into digital infrastructure in 2025, intensifying demand for high-capacity dense-wavelength-division multiplexing (DWDM) systems. Silicon photonics cost curves are falling after the shift to 6-inch indium-phosphide wafers, while open-line architectures are lowering capital outlays for carriers. Taken together, these forces position the optical transport network market as an essential backbone for artificial-intelligence clusters, cloud interconnects, and broadband inclusion.

Key Report Takeaways

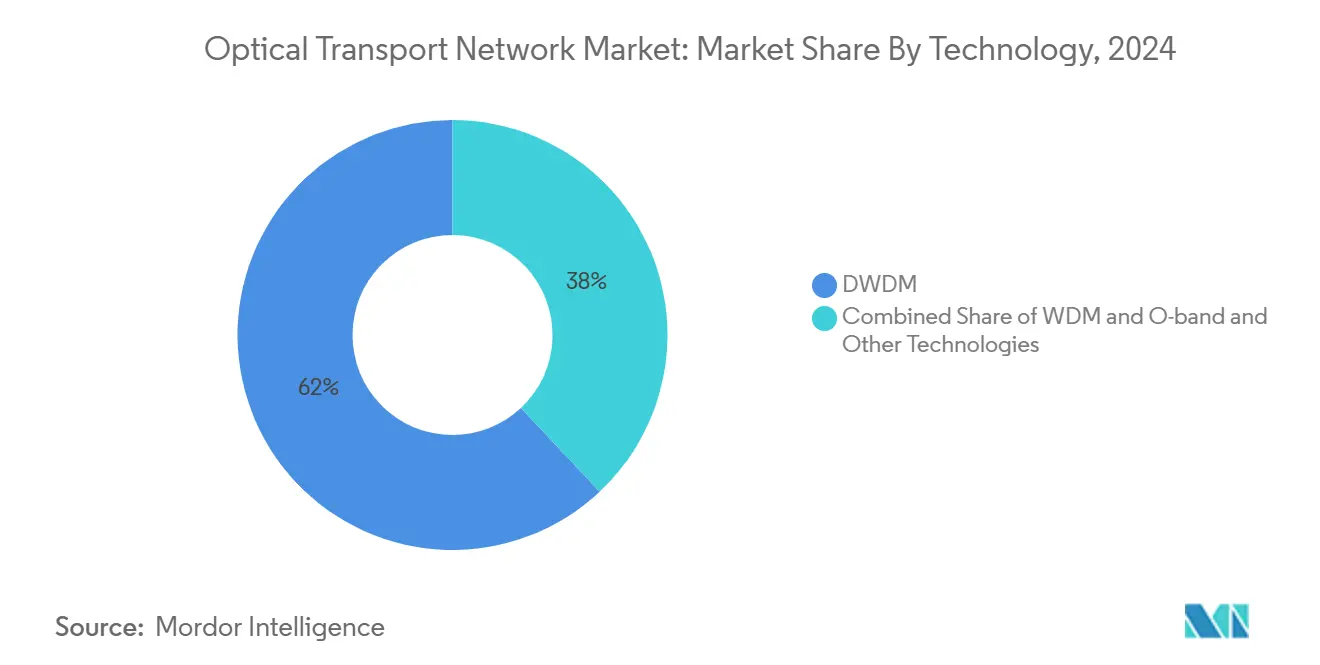

- By technology, DWDM systems led with 62% revenue share in 2024, while 800 G-capable DWDM platforms are projected to grow at a 14.5% CAGR through 2030.

- By offering, components accounted for 54% share of the optical transport network market size in 2024, whereas Edge ROADM components are advancing at a 13.2% CAGR to 2030.

- By end-user vertical, IT and Telecom operators held 48% of the optical transport network market share in 2024, while Cloud and Colocation data centers are expanding at a 17.8% CAGR through 2030.

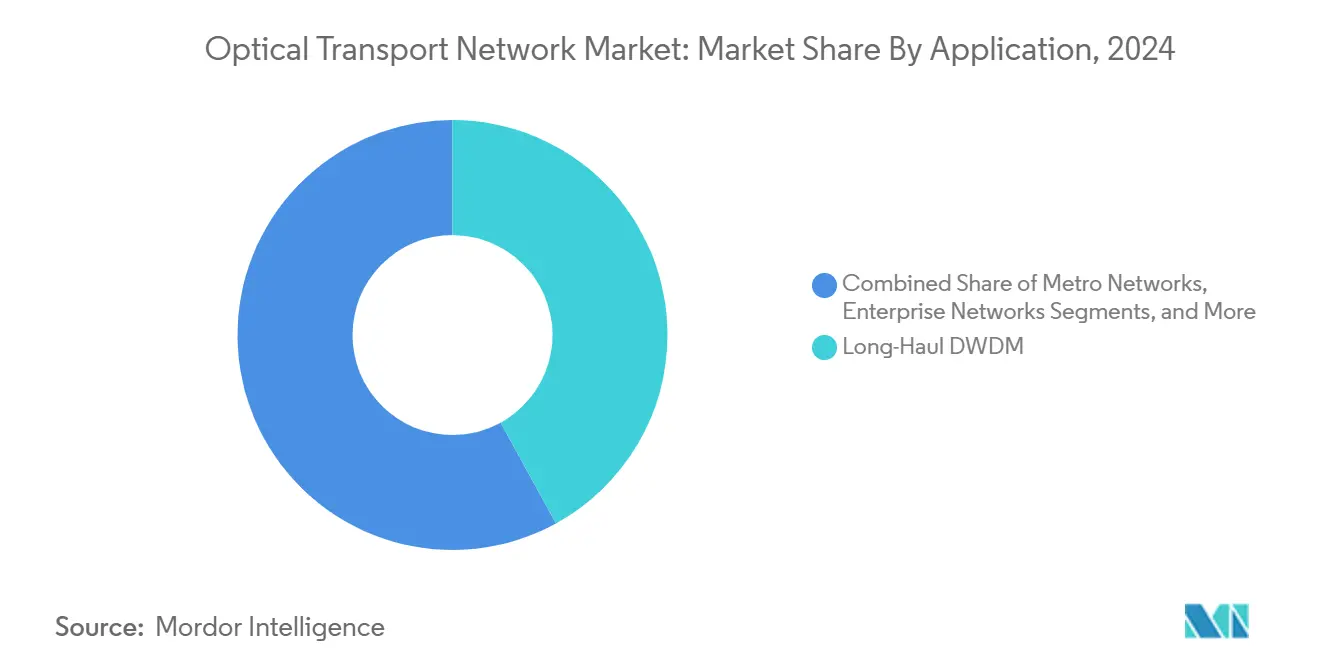

- By application, long-haul DWDM contributed 42% revenue in 2024, and data-center-interconnect is growing at a 15% CAGR between 2025–2030.

- By data rate, the 100–400 Gbit/s segment captured 46% revenue share in 2024, whereas 400–800 Gbit/s links are forecast to rise at a 22% CAGR through 2030.

- By geography, Asia-Pacific dominated with 35% revenue share in 2024 and is poised to expand at a 10.8% CAGR through 2030.

Global Optical Transport Network Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 400 ZR/ZR+ adoption for DCI | +2.1% | Global — APAC and North America lead | Short term (≤ 2 years) |

| Hyperscaler AI-cluster traffic boom | +1.8% | Core in North America and EU, spill-over to APAC | Medium term (2-4 years) |

| Government fibre-backhaul stimulus (US BEAD, EU CEF-2) | +1.4% | North America and EU, selective APAC markets | Medium term (2-4 years) |

| Open-line systems lowering capex | +0.9% | Global — early uptake in North America | Long term (≥ 4 years) |

| Silicon photonics price inflection | +0.7% | Global manufacturing, consumption led by hyperscalers | Long term (≥ 4 years) |

| Under-sea green-field cables (>20 Tb/s) | +0.6% | Trans-Pacific and Trans-Atlantic corridors | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rapid 400 ZR/ZR+ Adoption for DCI

Commercial availability of standardized 400ZR and ZR+ pluggables now lets operators plug coherent optics directly into routers, eliminating standalone transponders and trimming equipment cost. Coherent’s industrial-temperature 100G ZR QSFP28-DCO ships at only 5.5 W power draw, making coherent links viable in edge locations. Operators are logging 20–39% total-cost-of-ownership reductions from IP-optical convergence, and hyperscalers are already redesigning network fabrics to exploit these savings. Ciena’s 1.6T Coherent-Lite and new 448 Gb/s PAM4 optics answer a sixfold rise in DCI throughput expected by 2030. Most short-term gains will materialize in North America and APAC, where hyperscaler campus clusters generate bursty, latency-sensitive traffic.

Hyperscaler AI-Cluster Traffic Boom

Bandwidth tied to machine-learning training clusters is scaling much faster than traditional workloads. Fiber-optical transceiver revenue for AI fabrics is forecast to compound at 30% through 2028, dwarfing the 9% pace for non-AI deployments. Lumen Technologies signed USD 8 billion in new fiber deals during 2024, including a large order with Microsoft that underlines the scale of AI-driven optical demand. Coherent’s 300-port optical-circuit switch and Google’s deployment of similar technology in TPUv4 pods illustrate the architectural shift toward wavelength-selective, reconfigurable fabrics. This driver supports medium-term growth, especially in North America and the European Union as their hyperscale campuses expand.

Government Fibre-Backhaul Stimulus (US BEAD, EU CEF-2)

The USD 42.45 billion US BEAD program has already allocated funds to all states, fast-tracking middle-mile and last-mile projects. In Europe, the CEF Digital initiative and a EUR 350 million European-Investment-Bank loan to Deutsche Glasfaser are channeling capital into rural gigabit networks. Such programs directly lift demand for optical transport equipment, although potential shifts toward technology-neutral rules in US policy could reassign some funds to satellite providers. Public investment has also spurred on-shoring of fiber-optic manufacturing, with 2,500 jobs reshored and 3,200 miles of middle-mile fiber under construction.

Silicon Photonics Price Inflection

Moving from 3-inch to 6-inch indium-phosphide wafers increases die output fourfold and cuts device cost by more than 60%. Coherent’s new fabs in Texas and Sweden anchor this transition, supporting a photonic-integrated-circuit market that could exceed USD 45 billion within the decade. Japan backs similar advances with a 45 billion-yen program involving NTT, Intel, and SK Hynix. Co-packaged-optics modules promise 30% lower power draw and 40% lower cost per bit once manufacturing hurdles are overcome. The resulting cost curve gives hyperscalers enough economic headroom to scale AI networks without breaching power envelopes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capex freeze at Tier-2 telcos (2024–25) | −1.2% | Global — notably Europe and secondary APAC markets | Short term (≤ 2 years) |

| US-China export controls on coherent DSPs | −0.8% | China and aligned markets, ripple effect globally | Medium term (2-4 years) |

| Skilled-labour shortage for fibre installation | -0.6% | North America and EU primarily, emerging in APAC | Long term (≥ 4 years) |

| Supply-chain dependency on InP epitaxy | -0.4% | Global, with concentration risk in specialized foundries | Medium term (2-4 years) |

Source: Mordor Intelligence

Capex Freeze at Tier-2 Telcos (2024–25)

Smaller operators curtailed spending sharply in 2024, with Nokia citing a 23% slide in optical-network revenue because European and Asian customers deferred upgrades. Ciena’s optical revenue also fell to USD 2.64 billion, mirroring tight budgets and low average revenue per user in Europe. Ekinops disclosed a 41% decline in optical-transport sales, underscoring widespread caution. This restraint widens the gap between cash-rich hyperscalers advancing optical rollouts and traditional carriers postponing modernization.

US-China Export Controls on Coherent DSPs

Sanctions affecting germanium and gallium have inflated prices by 75% for germanium, creating a material squeeze for coherent DSPs. Import limitations could trim USD 3.5 billion from US GDP, while additional licensing steps slow Chinese access to leading-edge devices. Suppliers are hastening material substitution—LightPath Technologies is developing BDNL4 chalcogenide glass—and reshoring capacity to North America. Although silicon photonics offers China a route around deep-ultraviolet lithography constraints, global supply chains remain exposed to abrupt policy changes.

Segment Analysis

By Technology: DWDM Dominates Amid 800G Migration

DWDM retained a 62% share of the optical transport network market in 2024, confirming its status as the backbone for long-haul and metro connections. 800G-ready DWDM links are set to grow at 14.5% CAGR to 2030 as operators consolidate traffic from AI clusters and 5G backhaul into fewer wavelengths, boosting spectral efficiency.

Continuous DSP innovation anchors this shift. Ciena’s WaveLogic 6 pushes 1.6 Tb per wavelength, and Nokia’s PSE-6s raises reach at 800G speeds. These breakthroughs keep the optical transport network market moving toward flexible-grid operation, while Infinera’s 83.6 Tbps field test shows the upper ceiling is still rising. Convergence of DWDM and packet-optical functions now guides procurement decisions in both carrier and cloud settings, embedding integrated platforms as default choices.

The next horizon is C + L band expansion and the inclusion of previously unused wavelength windows, as Japan’s 402 Tbps field record revealed. China Broadnet’s Huawei-based 400G OTN deployment underscores high-density switching trends, and C+L integration lifts per-rack capacity to 100 Tbit/s. These moves ensure the optical transport network market remains future-proof as data rates climb beyond 1 Tb per channel.

By Offering: Components Lead Service Evolution

Components accounted for 54% of the optical transport network market size in 2024, led by coherent transceivers, ROADMs, and optical circuit switches. Sales of standardized pluggables are projected to double from USD 600 million in 2024, propelled by multi-vendor interoperability under the 400ZR specification.

Edge-ROADM units grow at a 13.2% CAGR because network disaggregation lets carriers and hyperscalers insert wavelength-selective switching directly at aggregation sites. At the same time, network-design and integration services are pivoting toward intent-based automation, helping customers translate application-level requirements into optical-path provisioning.

Managed network offerings are reviving under bandwidth-as-a-service models that bundle equipment and lifecycle management. Swift rollout of optical platform components, especially colorless-directionless-contentionless (CDC) architectures, is unlocking flexible spectrum allocation. Service providers thus shift operating models away from box-centric procurement to outcome-oriented contracts, realigning internal skill sets around software orchestration.

By End-user Vertical: Cloud Acceleration Reshapes Demand

IT and Telecom incumbents held 48% of the optical transport network market share in 2024, yet cloud and colocation providers now record a 17.8% CAGR through 2030 as AI workloads multiply east–west traffic within and between data centers.

Healthcare networks adopt dual-metro-area architectures to safeguard critical applications, posting annual opex savings above USD 150,000 from optical migrations. Banks are moving high-volume secure traffic onto private optical fabrics, pairing microservices with Kubernetes to lift scalability. Government and defense agencies prioritize EMP-resistant, quantum-safe fiber solutions, while utilities and educational systems use public broadband funds to overhaul campus backbones.

Cross-vertical convergence is clear: carriers are redesigning backbone nodes to support cloud customer requirements, and hyperscalers now lease dark fiber to telecom operators. Optical transport network industry participants thus straddle both service provider and enterprise domains, leveraging integrated roadmaps spanning coherent components, software control, and professional services.

By Application: DCI Emerges as Growth Engine

Long-haul DWDM still made up 42% of 2024 revenue, but data-center-interconnect (DCI) grows at 15% CAGR to 2030, reflecting expanding hyperscale footprints. IP-over-DWDM topologies and standardized 400ZR optics allow direct router connections that bypass traditional transponders, slashing power and capex.

Metro networks are buoyed by 5G densification; South Korea already runs a nationwide 600G backbone across 1,000 km. Enterprises deploy fiber-to-the-office to cut power consumption by 60% while delivering gigabit access. Submarine projects like the 45,000 km 2Africa cable rely on 800G technology, demonstrating that undersea segments are also advancing capacity at pace.

These developments emphasize that the optical transport network market underpins every layer of digital infrastructure, from local campus fabrics to intercontinental subsea routes. Operators therefore align application roadmaps with coherent-pluggable advances, ensuring scalable, low-latency paths for AI, 5G, and ultra-HD video traffic.

Note: Segment shares of all individual segments available upon report purchase

By Data Rate: 400–800 Gbit/s Acceleration Drives Transition

Links operating in the 100–400 Gbit/s range represented 46% of deployments in 2024, but 400–800 Gbit/s lanes are compounding at 22% through 2030 as network owners upgrade line cards and transceivers to meet AI-cluster requirements.

OIF-approved 400ZR and ZR+ standards guarantee interoperability, reducing spares inventory and operational complexity. Beyond 800 Gbit/s, early field trials explore 1.6 T and 1.2 T wavelengths, guided by photonic-integrated-circuit advances and tighter optical packaging. Coherent’s QSFP-DD and OSFP optics for optical-circuit switches point to compact form factors delivering higher radix fabrics.

This data-rate inflection cements a Moore-like cadence in optical throughput, enabling the optical transport network market to maintain cost-per-bit declines even as spectral efficiency rises. Compatibility with legacy fiber and amplifier plants guarantees orderly transitions without wholesale infrastructure rip-and-replace.

Geography Analysis

Optical Transport Network Market in North America

Asia-Pacific controlled 35% of 2024 revenue and is projected to expand at a 10.8% CAGR, the fastest across regions. Chinese authorities selected over 20 cities for 10 G broadband pilots; China Mobile alone serves 272 million broadband lines, with one-third on gigabit tiers. Japan partners NTT and Intel on government-funded optical semiconductors, while South Korea’s K-Network 2030 allocates USD 481 million for 6 G research and low-orbit satellite links. The ALPHA subsea cable, with 18 Tbit/s per fiber pair, fortifies regional interconnectivity.

North America sits on mature infrastructure yet sees renewed momentum as the USD 42.45 billion BEAD program funnels capital into middle-mile construction. Lumen’s USD 8 billion fiber contracts and Zayo’s USD 4 billion long-haul expansion reveal how AI-driven edge compute is reconfiguring route demand. Workforce shortages remain acute: 205,000 additional technicians are needed, spurring training alliances among carriers, vendors, and the Fiber Broadband Association.

Europe balances ambitious digital-sovereignty goals with tight operator cash flow. The European Investment Bank’s EUR 350 million loan to Deutsche Glasfaser targets rural gigabit coverage, while the CEF Digital scheme outlines EUR 200 billion requirements for very-high-capacity networks. Operator ARPU remains muted, so public co-funding remains critical. Orange Poland’s build for 155,000 homes highlights reliance on blended finance. Planned 48-pair subsea links between the UK and mainland Europe will trim latency by up to 5.5 ms for certain routes.

Competitive Landscape

Top Companies in Optical Transport Network Market

The market shows moderate consolidation after Nokia closed its USD 2.3 billion Infinera acquisition in February 2025, forming a 20%-share vendor with complementary DSP roadmaps and expected EUR 200 million synergies by 2027. Huawei reported 22% revenue growth to CNY 860 billion in 2024, offsetting Nokia’s 9% and Ericsson’s 6% declines, indicating divergence between vendor strategies and geographical exposure.

ZTE’s 7.8% revenue gain to RMB 32.97 billion in Q1 2025 stems from public-sector AI demand, while Coherent invests in 6-inch InP fabs to peel cost out of transceiver production. White-space innovators include module makers focused on co-packaged optics and software-defined-networking specialists enabling open-line adoption. Vertical integration resurfaces as a hedge against supply-chain swings in indium-phosphide epitaxy and DSP availability.

Competition also plays out in standards bodies, where multivendor interoperability wins mindshare with hyperscalers. Vendors differentiate via power consumption, component density, and automation hooks rather than proprietary line-rates alone. This realignment ensures buyers can mix-and-match optics, controllers, and software while sustaining differentiated service features.

Optical Transport Network Industry Leaders

-

Nokia Corporation

-

Ciena Corporation

-

Cisco Systems Incorporation

-

Huawei Technologies Co. Ltd

-

Fujitsu Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Nokia completed its USD 2.3 billion acquisition of Infinera, creating a combined optical-networks powerhouse with expected EUR 200 million synergies by 2027.

- February 2025: Meta unveiled Project Waterworth, a 50,000 km subsea cable with 24 fiber pairs linking five continents to anticipate AI growth.

- February 2025: Teset Capital pledged EUR 100 million for a 1,000 km fiber-optic submarine link in the Mediterranean.

- January 2025: center3 activated the 45,000 km 2Africa cable using Ciena’s 800G gear, enhancing Afro-Eurasian connectivity under Saudi Vision 2030.

Global Optical Transport Network Market Report Scope

An optical transport network (OTN) is a high-capacity network that transports optical signals between several sites. OTN networks are perfect for transporting video, audio, and other types of traffic due to their capacity for enormous volumes of data. Many places, like airports, hospitals, and commercial buildings, employ this network to link various regions worldwide.

The Optical Transport Network Market is segmented by technology (WDM, DWDM, and other technologies), by offering (service [network maintenance & support, network design], by component [optical transport, optical switch, optical platform]), by end-user vertical (IT & telecom, healthcare, government, and other end-user verticals), and by geography (North America, Europe, Asia Pacific, the Rest of the World). The report offers market forecasts and size in value (USD) for all the above segments.

| By Technology | WDM | ||

| DWDM | |||

| O-band and Other Technologies | |||

| By Offering | Services | Network Maintenance and Support | |

| Network Design and Integration | |||

| Components | Optical Transport Equipment | ||

| Optical Switch | |||

| Optical Platform/Edge ROADM | |||

| By End-user Vertical | IT and Telecom Operators | ||

| Cloud and Colocation Data Centres | |||

| Government and Defence | |||

| Healthcare | |||

| Banking and Financial Services | |||

| Others (Utilities, Education) | |||

| By Application | Long-Haul DWDM | ||

| Data-Center-Interconnect (DCI) | |||

| Metro Networks | |||

| Enterprise Networks | |||

| By Data Rate / Wavelength | 100-400 Gbit/s | ||

| 400-800 Gbit/s | |||

| Beyond 800 Gbit/s | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| UK | |||

| France | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East | Saudi Arabia | ||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| WDM |

| DWDM |

| O-band and Other Technologies |

| Services | Network Maintenance and Support |

| Network Design and Integration | |

| Components | Optical Transport Equipment |

| Optical Switch | |

| Optical Platform/Edge ROADM |

| IT and Telecom Operators |

| Cloud and Colocation Data Centres |

| Government and Defence |

| Healthcare |

| Banking and Financial Services |

| Others (Utilities, Education) |

| Long-Haul DWDM |

| Data-Center-Interconnect (DCI) |

| Metro Networks |

| Enterprise Networks |

| 100-400 Gbit/s |

| 400-800 Gbit/s |

| Beyond 800 Gbit/s |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| UK | |

| France | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

Key Questions Answered in the Report

What is the current size of the optical transport network market and how fast is it growing?

The optical transport network market is valued at USD 27 billion in 2025 and is estimated to expand to USD 40.44 billion by 2030, reflecting an 8.42% CAGR.

Which technology segment holds the largest share?

DWDM platforms dominated with 62% revenue share in 2024, and migration to 800G wavelengths is pushing this segment forward.

Why is data-center-interconnect growing faster than long-haul applications?

AI workloads and hyperscale cloud expansion are driving east–west traffic, making DCI the fastest-growing application at a 15% CAGR to 2030.

How are government stimulus programs affecting deployment?

US BEAD and EU CEF-2 funding accelerate middle-mile and rural fiber builds, lifting optical equipment demand even in regions with constrained private capital.

What role does silicon photonics play in cost reduction?

Transitioning to 6-inch InP wafers cuts die costs by 60% and boosts output fourfold, allowing operators to scale bandwidth while controlling power and capex.

Which region is expanding the fastest?

Asia-Pacific leads with a 10.8% CAGR through 2030, propelled by large-scale Chinese and Japanese infrastructure investments and record-setting transmission trials.

Page last updated on: June 19, 2025