Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

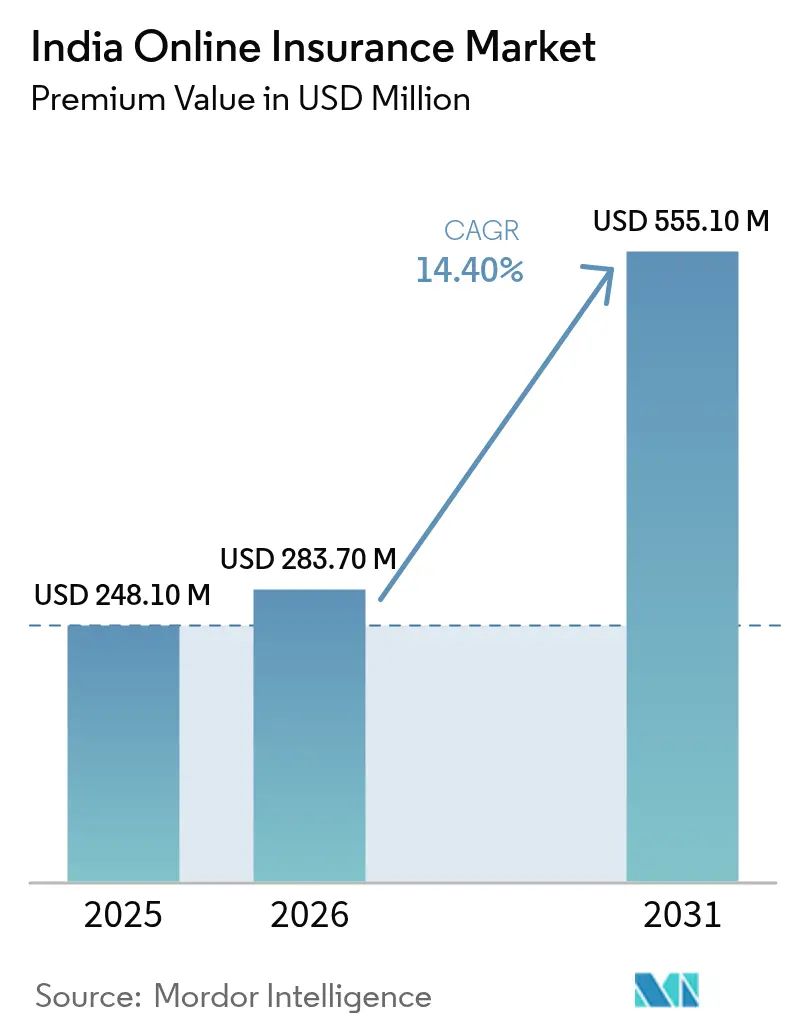

| Base Year Market Size (2025) | USD 248.10 Million |

| Market Size (2026) | USD 283.70 Million |

| Market Size (2031) | USD 555.10 Million |

| Growth Rate (2026 - 2031) | 14.40% CAGR |

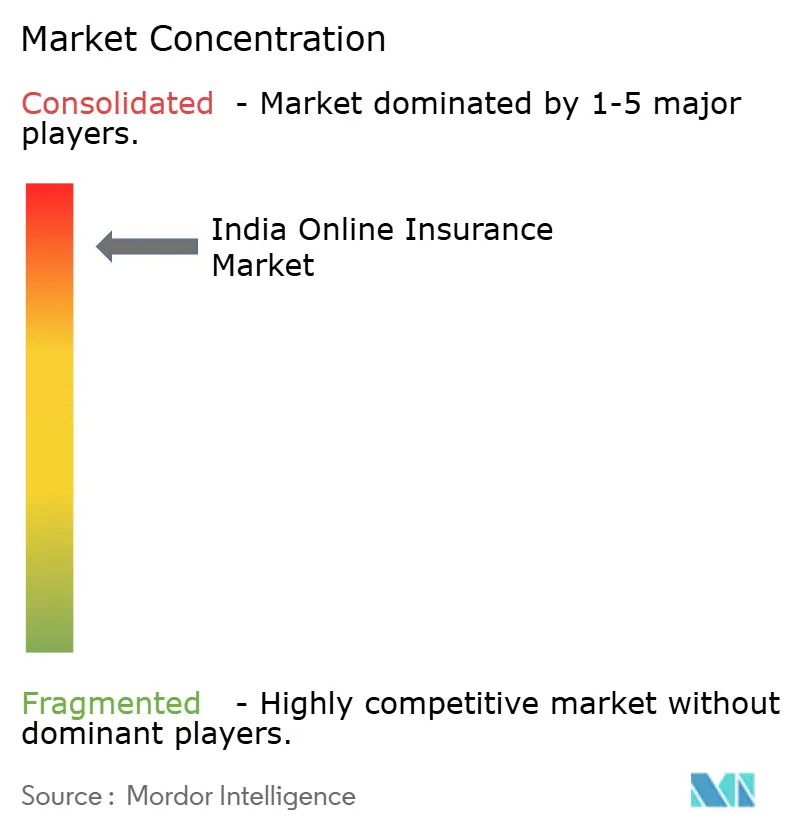

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Online Insurance Market Analysis by Mordor Intelligence

The India Online Insurance Market size in terms of premium value is projected to expand from USD 248.10 million in 2025 and USD 283.70 million in 2026 to USD 555.10 million by 2031, registering a CAGR of 14.40% between 2026 to 2031.

The online insurance market in India is experiencing rapid growth, transforming from a backup channel into a primary avenue for purchasing and managing policies. This growth reflects a shift toward digital-native purchase and renewal journeys, where low-friction payments, faster product filing, and platform-led distribution increasingly shape consumer behavior[1]IRDAI, “Consolidated & Gazette Notified Regulations,” Insurance Regulatory and Development Authority of India, irdai.gov.in. India’s broader protection gap continues to be a structural catalyst for online channels, with the country positioned among the fastest-growing global insurance ecosystems in 2026. Payment innovations like UPI AutoPay and the launch of Bima-ASBA reduce refund disputes and renewal lapses, anchoring mobile-first acquisition and retention. At the same time, regulatory enablers such as Use-and-File and an expanded sandbox framework compress time-to-market for digital-first covers and riders, which fosters iteration in wellness, micro-duration, and device-linked protection. With insurers and partners increasingly leveraging telematics, consented data, and standardized claims rails, the India online insurance market is entering a more scalable phase of digital distribution and servicing in 2026.

Key Report Takeaways

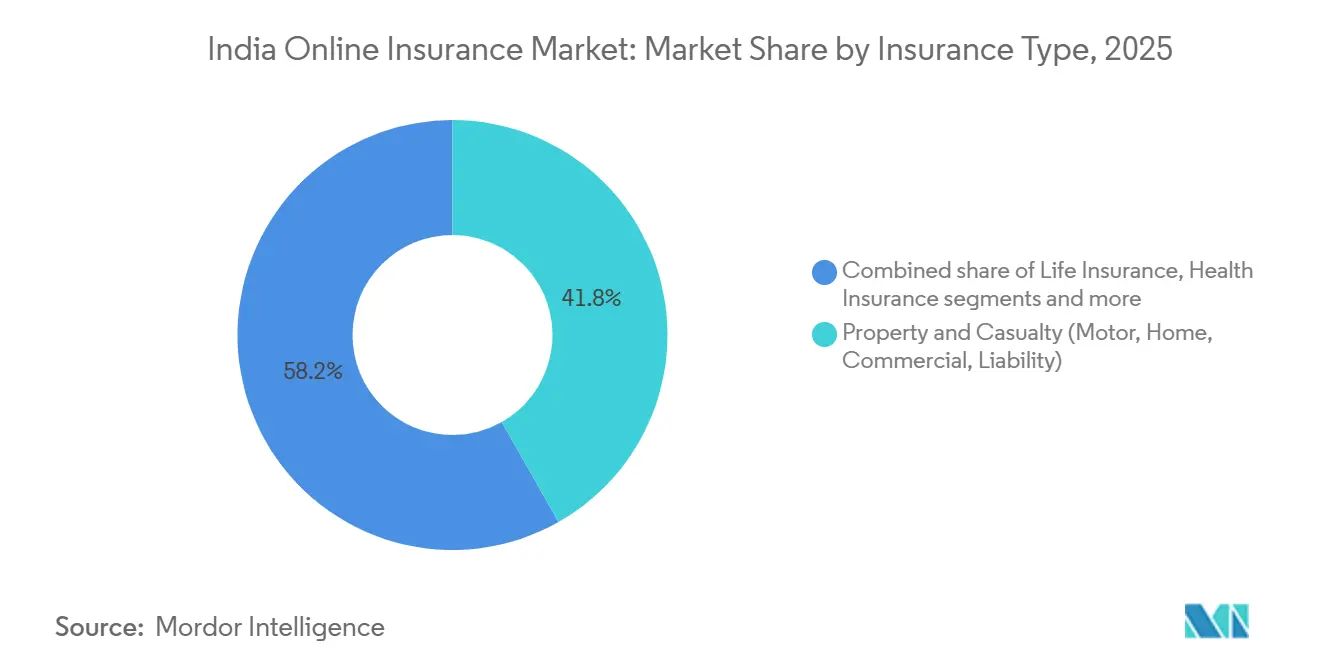

- By insurance type, the India online insurance market was led by property and casualty at 41.8% revenue share in 2025, while specialty lines are projected to expand at a 15.6% CAGR to 2031.

- By customer segment, the India online insurance market saw retail and individual customers hold 71.4% share in 2025, and the SME or commercial segment is forecast to grow at a 15.1% CAGR through 2031.

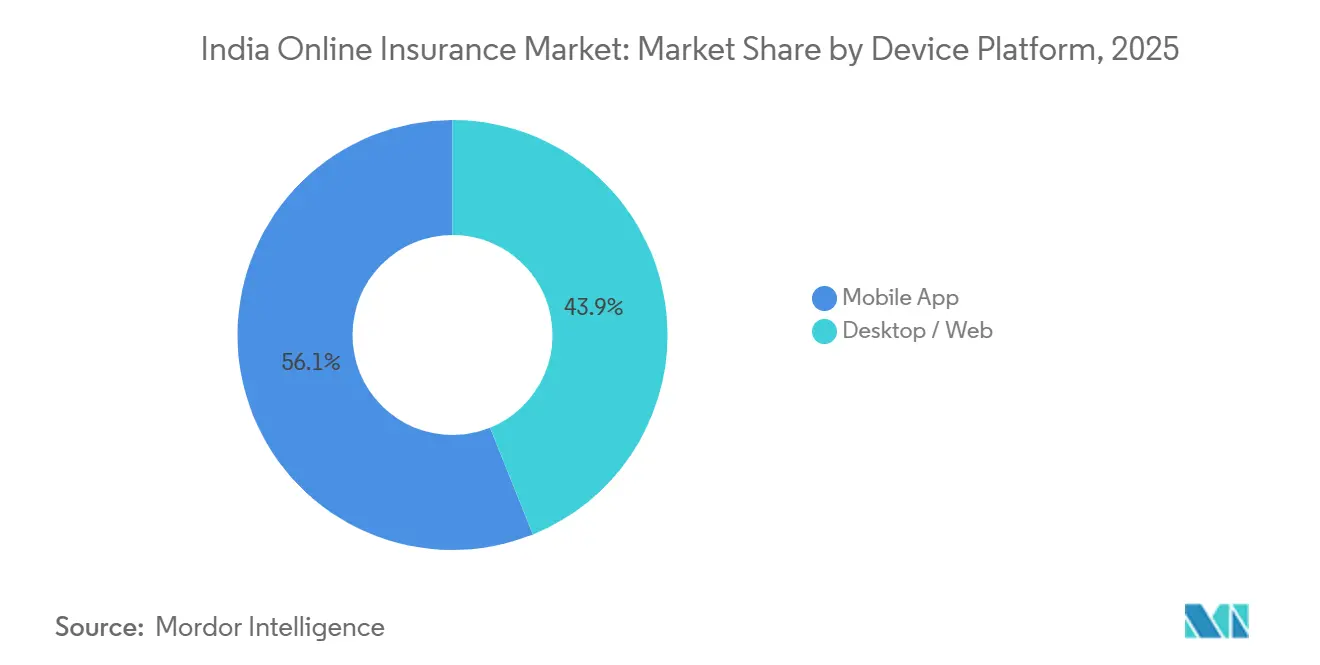

- By device platform, the India online insurance market registered mobile app as the largest channel with 56.1% share in 2025 and the fastest trajectory at a projected 17.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Online Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UPI AutoPay and Bima-ASBA reduce premium payment friction and drop-offs in online journeys | +2.8% | National, with early gains in metro clusters and rapid spread to tier-2 and tier-3 hubs | Short term (≤ 2 years) |

| Use-and-File and sandbox reforms compress product launch cycles for digital-first covers and riders | +2.1% | National, especially insurtech corridors such as Bengaluru, Pune, and Hyderabad | Medium term (2-4 years) |

| Usage-based motor add-ons enable app-led telematics and personalized pricing | +1.9% | Urban metros and highway corridors, with spillover to tier-2 state capitals | Medium term (2-4 years) |

| Embedded insurance via fintech and e-commerce expands low-ticket, context-led online adoption | +2.4% | National, concentrated in e-commerce and digital-first banking zones | Short term (≤ 2 years) |

| NHCX-enabled cashless claims improve trust and conversion for digitally purchased health covers | +1.7% | National, top-tier hospital networks first, slower rural integration | Long term (≥ 4 years) |

| Account Aggregator and CKYC reduce underwriting TAT for retail and SME digital policies | +1.5% | Metros and tier-1 cities, gradual MSME ecosystem reach | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

UPI AutoPay and Bima-ASBA Reduce Premium Payment Friction and Drop-Offs in Online

Journeys IRDAI mandated the rollout of Bima-ASBA for life and health policies, enabling a consent-first process where premiums are blocked in the customer’s account and released only after issuance or unblocked within stipulated timelines if issuance does not occur. Insurers and distributors report improved trust and fewer refund-related disputes because the mechanism removes premature debits from the customer journey. UPI AutoPay continues to gain traction for recurring premiums, and the payments ecosystem has introduced higher per-transaction limits for relevant use cases to support insurance renewals at scale. APIs from leading payment players integrate with insurer and aggregator apps, which reduces manual follow-ups and curbs renewal lapses for digitally purchased policies. The combined effect is a lower-cost, automated premium collection flow that sustains retention in the India online insurance market and simplifies first-time buying decisions on mobile.

Use-and-File and Sandbox Reforms Compress Product Launch Cycles for Digital-First Covers or Riders

Regulatory reforms have accelerated the product pipeline by allowing Use-and-File for certain health insurance products and by enlarging the sandbox scope to invite broader innovation and operational efficiency proposals. The Use-and-File framework cuts time-to-market by enabling launches that adhere to design and transparency norms without waiting for prior approval, which is well-suited for app-native features and micro covers. The expanded sandbox permits controlled pilots across channels and partners, which supports embedded distribution experiments and new underwriting workflows. Insurers and insurtechs are now able to iterate faster on contextual riders and wellness-linked add-ons, which strengthens product-market fit in digital channels. These changes underpin a more agile product cadence in the Indian online insurance market and have encouraged carriers to prioritize mobile-first features in their launch roadmaps.

Usage-Based Motor Add-Ons Enable App-Led Telematics and Personalized Pricing

By 2026, several general insurers had introduced app-linked Pay-As-You-Drive and Pay-How-You-Drive options that factor mileage and driving behavior into pricing, supported by smartphone sensors and optional in-vehicle devices. Telematics-based add-ons encourage safer driving by offering premium benefits to low-risk users, and they create a more transparent linkage between behavior and cost[2]Shriram General Insurance, “AI and Telematics Shaping Car Insurance Premiums in India,” Shriram General Insurance, shriramgi.com. Insurers use app telemetry to reduce investigation overheads for minor claims and to increase straight-through approvals where data corroborates the event. This approach strengthens underwriting discipline while enhancing customer experience in channel journeys that start and finish on mobile. As a result, telematics has become a visible differentiator in the India online insurance market for motor lines.

Embedded Insurance via Fintech and E-Commerce Expands Low-Ticket, Context-Led Online Adoption

Embedded insurance is scaling inside checkout flows for travel, mobility, electronics, and payments apps, which reduces clicks between discovery and purchase and encourages first-time adoption. The ubiquity of real-time digital payments has created frequent micro-moments to place one-tap protection offers with clear benefits and instant policy documents. Account Aggregator rails help partners personalize offers with consented data, which improves conversion while keeping turnaround times to minutes. The resulting low-ticket and short-duration covers add breadth to customer portfolios and build trust for higher-value purchases over time. These embedded rails reinforce mobile-first behavior and help widen access in the India online insurance market across urban and rising digital hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Physical medical underwriting for high-sum insured or term products limits straight-through digital conversion | -1.8% | National, acute in semi-urban and rural zones with limited tele-underwriting infrastructure | Long term (≥ 4 years) |

| Digital fraud and identity misuse elevate AML or KYC friction and operating costs | -2.3% | Metros and tier-1 cities with high digital transaction volumes | Medium term (2-4 years) |

| DPDP Act consent and purpose-limitation curb behavioral targeting and cross-sell without robust consent rails | -1.4% | National, especially for data-heavy digital players | Short term (≤ 2 years) |

| Uneven NHCX and hospital IT integration outside top networks constrains cashless claim STP at scale | -1.1% | Tier-2 and tier-3 cities and rural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Physical Medical Underwriting for High-Sum Insured or Term Products Limits Straight-Through Digital Conversion

High-value term and critical illness policies still require in-person or supervised medical checks for risk selection, which reduces the share of fully automated issuance online. Diagnostic infrastructure and scheduling capacity are uneven outside major metros, which introduces delays and increases drop-offs for complex policies. Insurers have continued to digitize documentation and appointment booking, but the last-mile examination remains offline for high sums insured. The regulator has also emphasized robust underwriting and compliance, which limits shortcuts for high-ticket issuance in digital flows. These constraints keep portions of the India online insurance market hybrid in nature for large-cover products.

Digital Fraud and Identity Misuse Elevate AML or KYC Friction and Operating Costs

Cyber threats and identity abuse have raised the need for stronger fraud monitoring and security programs across insurers and intermediaries. IRDAI has issued governance and control expectations on information and cybersecurity, as well as fraud monitoring, which require timely incident escalation and board oversight. To comply and manage risk, insurers deploy multi-layered KYC and transaction risk controls that include device fingerprinting, behavioral analytics, and real-time database checks. These measures protect customers and the system, but can introduce friction that affects conversion and adds cost to digital acquisition. This evolving control stack is now a core consideration in customer journey design in the Indian online insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Specialty Lines Surge on Cyber and Pet Demand, While Motor Anchors Volume

Property and Casualty accounted for 41.8% of the India online insurance market share in 2025, while Specialty Lines are projected to record a 15.6% CAGR to 2031 as digital purchase intent for niche protection expands. Motor remains the anchor for P&C in online channels, supported by usage-based add-ons that connect pricing to how and how much a vehicle is driven. App-based telematics and optional in-vehicle sensors have created new data points for underwriting and claims automation, which strengthens customer acceptance of online motor purchases. Life products benefit from digital pre-issuance workflows and more agile filing pathways, which help carriers launch updated variants faster for online shoppers. In health, digital buying is advancing alongside standardized claims rails like NHCX, which fosters trust in cashless approvals over time[3]National Health Authority, “NHCX Platform and Claims Exchange,” National Health Authority, hcxbeta.nha.gov.in.

Specialty Lines draw momentum from enterprise digitization and app-based lifestyles, which is visible in rising online interest for cyber, pet, travel, and marine covers. Cyber protection continues to gain visibility with policy add-ons and SME offerings marketed through digital partners. Pet insurance has expanded its product shelf, with new retail-focused offerings routed through digital channels to simplify discovery and enrollment. Travel insurance remains a leading embedded use case because checkout placement reduces friction and shortens time to bind. As carriers refine digital onboarding and strengthen claims infrastructure, Specialty Lines are well positioned to contribute a greater share to the India online insurance market by 2031.

By Customer Segment: Retail Dominance Persists, but SME or Commercial Sprint on Lending-Linked Covers

Retail and Individual customers held 71.4% in 2025, underscoring the online channel’s strength in everyday protection and renewal journeys. Aggregators and embedded partners enable retail discovery at scale, while app-first journeys improve renewal compliance through consented, recurring payment mandates. Mobile design and vernacular interfaces continue to expand reach across digital hubs, which sustains retail-led volumes in the India online insurance market. Health and motor remain leading retail purchase categories because standardized coverage, app support, and e-KYC keep journeys predictable and quick. Retail adoption also benefits from faster product iteration made possible by Use-and-File in health and wider sandbox permissions for pilots.

SME or Commercial shows the fastest trajectory with a 15.1% CAGR outlook, catalyzed by loan-linked protection and Account Aggregator data that compress underwriting timeframes. AA frameworks let insurers, with consent, access financial records to tailor premiums and coverage at the point of credit decision, which increases attach rates[4]Sahamati, “From Consent to Cover,” Sahamati, sahamati.org.in.SME owners also access digital storefronts that aggregate business covers, which reduces dependence on broker-led offline cycles. For large corporations, online enrollment and benefit administration via APIs are increasing, though broker-led negotiation and consulting remain important for group programs. Together, these shifts broaden the customer base for the India online insurance market while balancing high-volume retail with faster-growing SME demand.

By Device Platform: Mobile App Dominates as Recurring Premiums Shift to Consent-Led Flows

Mobile App commanded 56.1% share of the India online insurance market size in 2025 and is projected to expand at a 17.1% CAGR to 2031 as smartphone-first design and instant payment mandates remove friction. UPI AutoPay adoption continues to rise for renewals, which supports lapse reduction and predictable cash flows for insurers operating digital books. App interfaces now consolidate purchase, endorsements, claims initiation, and document access, which lowers service costs and reduces policyholder effort. Digital servicing and claims status visibility further improve satisfaction for mobile-first users. These elements create a sustained channel advantage for the India online insurance market as more users transact and renew on mobile.

Desktop and Web continue to serve high-involvement purchases where customers compare detailed benefits, evaluate long-tail riders, and coordinate with family or advisors before binding. Insurers and aggregators maintain synchronized journeys across devices to avoid drop-offs when users switch from research on a large screen to final purchase on mobile. This omnichannel coherence is essential to large-cover life or commercial policies, where due diligence and documentation take longer. With autopay and e-KYC integrated across channels, users can complete pending steps on the device of choice without starting over. The mix ensures the India online insurance market meets both quick buys and considered purchases with consistent experiences.

Geography Analysis

Metropolitan clusters account for a large share of digital premiums due to dense fintech ecosystems, higher smartphone use, and early adoption of consented payments for renewals. Concentrated insurer and distributor presence in hubs such as Mumbai and Bengaluru supports faster rollouts of telematics add-ons and mobile-first journeys. App-based flows take root first in these regions, which sets benchmarks in claims service time and renewal completion. These metros remain anchor markets for the India online insurance market, especially for motor, health, and life rider experimentation.

Tier-2 and tier-3 cities are the next growth frontier for digital acquisition as account aggregator data and embedded distribution improve underwriting and attach rates for protection. Regulatory programs focused on inclusion and digital rails also encourage product availability and service standardization in smaller cities. Ongoing NHCX onboarding across providers and payers lays the groundwork for wider cashless claim adoption, which drives trust in online health purchases beyond metros. As claims processing gets more uniform across networks, digitally purchased policies become easier to use for customers in rising digital hubs. These shifts expand the addressable base for the India online insurance market across multiple product lines.

Rural penetration remains an opportunity for digital models that combine assisted onboarding with mobile-first servicing and claims coordination. Vernacular UX, one-tap consent, and recurring mandates help first-time buyers manage renewals and claims with fewer in-person visits. As hospitals and insurers in smaller towns integrate with NHCX, more policyholders will experience faster approvals and discharge, which raises satisfaction. With embedded protection present in commerce and mobility apps that are already familiar in rural markets, entry barriers are further lowered for short-duration and micro-ticket covers. Together, these elements advance inclusion while growing the India online insurance market beyond urban concentration.

Competitive Landscape

Distribution in the Indian online insurance market is concentrated around major aggregators that integrate dozens of insurers and hundreds of plans onto unified mobile and web experiences. This aggregation reduces search costs for consumers and gives carriers a digital shelf to test and refine product variants more quickly. Embedded partners in e-commerce and fintech add incremental reach by placing one-tap offers inside high-frequency purchase journeys. Payment innovations like UPI AutoPay strengthen renewal retention and improve the economics of digital books as portfolios mature. This ecosystem structure favors participants that excel in acquisition efficiency, claims speed, and compliance-by-design.

On the carrier side, product and process digitization continue to advance, with motor telematics and app-first claims submission gaining traction. Health insurers and partners are integrating with NHCX to standardize claims exchange, and each onboarding milestone reduces friction for cashless approvals. Regulatory sandbox permissions encourage targeted pilots in embedded distribution, parametric triggers, and API-led onboarding that can later scale system-wide. Identity, AML, and fraud controls are also a source of competitive advantage as firms balance drop-off risk against security obligations in digital flows. These moves define performance gaps among carriers and distributors across the India online insurance market.

Strategic partnerships and ownership changes also reshape capacity and capability. Zurich’s acquisition of a majority stake in an Indian general insurer adds global expertise to local operations and raises competitive intensity. Allianz completed a major realignment of its India ventures and announced a reinsurance joint venture with a domestic financial services partner, which signals new types of platform partnerships. As these shifts proceed, participants are investing in mobile-first journeys, embedded rails, and standardized claims to differentiate in the India online insurance market.

India Online Insurance Industry Leaders

Policybazaar

Acko General Insurance

ICICI Lombard

HDFC Life

Bajaj Allianz General Insurance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Allianz and Jio Financial Services announced binding agreements to form a domestic reinsurance joint venture and non-binding agreements toward new general and life insurance ventures.

- June 2025: Zurich acquired a 70% stake in Kotak General Insurance after regulatory approval, adding global scale to India general insurance operations.

- June 2025: Central Bank of India acquired a minority stake in Future Generali India Insurance to strengthen bancassurance distribution plans.

- February 2025: IRDAI mandated Bima-ASBA for life and health policies with UPI One-Time Mandate, enabling premium blocking and time-bound release to reduce refund disputes.

India Online Insurance Market Report Scope

Online insurance, also known as digital insurance or e-insurance, refers to buying insurance policies through online channels, typically via the internet or mobile apps. The Indian online insurance market, by type, includes life insurance, motor insurance, health insurance, and other insurance. The report offers market size and forecasts for the online insurance market in India in value (USD) for all the above segments.

By Insurance Type

| Life Insurance |

| Health Insurance |

| Property & Casualty (Motor, Home, Commercial, Liability) |

| Specialty Lines (Cyber, Pet, Marine, Travel) |

By Customer Segment

| Retail / Individual |

| SME / Commercial |

| Large Enterprise / Corporate |

By Device Platform

| Mobile App |

| Desktop / Web |

| By Insurance Type | Life Insurance |

| Health Insurance | |

| Property & Casualty (Motor, Home, Commercial, Liability) | |

| Specialty Lines (Cyber, Pet, Marine, Travel) | |

| By Customer Segment | Retail / Individual |

| SME / Commercial | |

| Large Enterprise / Corporate | |

| By Device Platform | Mobile App |

| Desktop / Web |

Key Questions Answered in the Report

What is the current size and growth outlook for the India Online Insurance Market to 2031?

The India online insurance market size is expected to increase from USD 248.1 million in 2025 to USD 283.7 million in 2026 and reach USD 555.1 million by 2031 at a 14.4% CAGR over 2026-2031.

Which product categories lead online adoption in India and which are growing the fastest?

Property and Casualty leads online adoption with 41.8% share in 2025, while Specialty Lines are set to grow the fastest with a 15.6% CAGR to 2031.

How is the channel mix evolving between mobile apps and desktop for digital policy purchase and renewals?

Mobile App is the largest and fastest channel with a 56.1% share in 2025 and a projected 17.1% CAGR, supported by UPI AutoPay for recurring premiums.

What regulatory changes are most important for India’s digital insurance growth in 2026?

Use-and-File for health and a broader regulatory sandbox accelerate launches and pilots, while Bima-ASBA reduces payment friction for online issuance.

How are data and consent rails improving digital underwriting and claims?

Account Aggregator consented data shortens SME and retail underwriting, while NHCX standardizes cashless health claims to build trust in online purchases.

What are the main operational challenges that could slow online conversion in India?

High-sum medical underwriting often requires in-person tests and stronger digital fraud controls add KYC layers, which can introduce friction in online flows.

Page last updated on: