Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

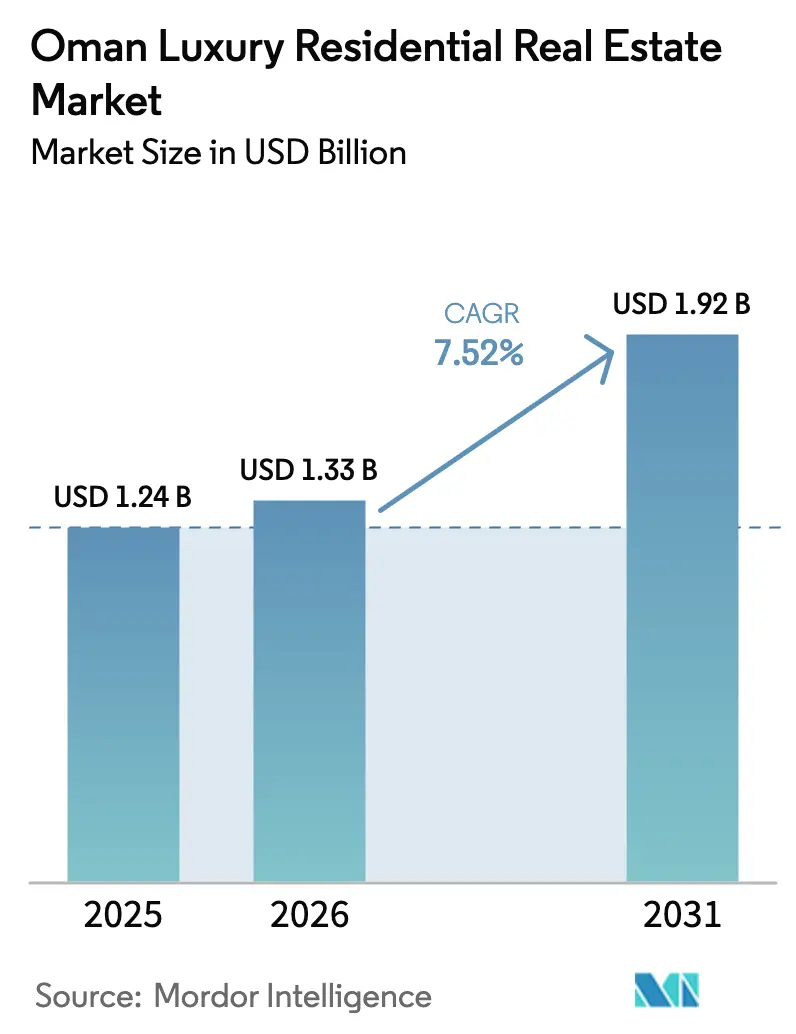

| Base Year Market Size (2025) | USD 1.24 Billion |

| Market Size (2026) | USD 1.33 Billion |

| Market Size (2031) | USD 1.92 Billion |

| Growth Rate (2026 - 2031) | 7.52% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Oman luxury residential real estate market size is expected to grow from USD 1.24 billion in 2025 to USD 1.33 billion in 2026 and is forecast to reach USD 1.92 billion by 2031 at 7.52% CAGR over 2026-2031. Demand is accelerating as Vision 2040 reforms unlock foreign ownership, upscale infrastructure, and zero personal income and capital-gains taxes that improve net returns for affluent purchasers. Villa-led masterplans in Muscat and Dhofar attract Gulf buyers who view Oman as a stable, lifestyle-rich alternative to crowded regional hubs. Developers combine branded hospitality, smart-home technology, and sustainable design to justify premium pricing. The rental slice is still small but growing as expatriate executives seek flexible arrangements while investors chase 6-8% yields in prime districts.

Key Report Takeaways

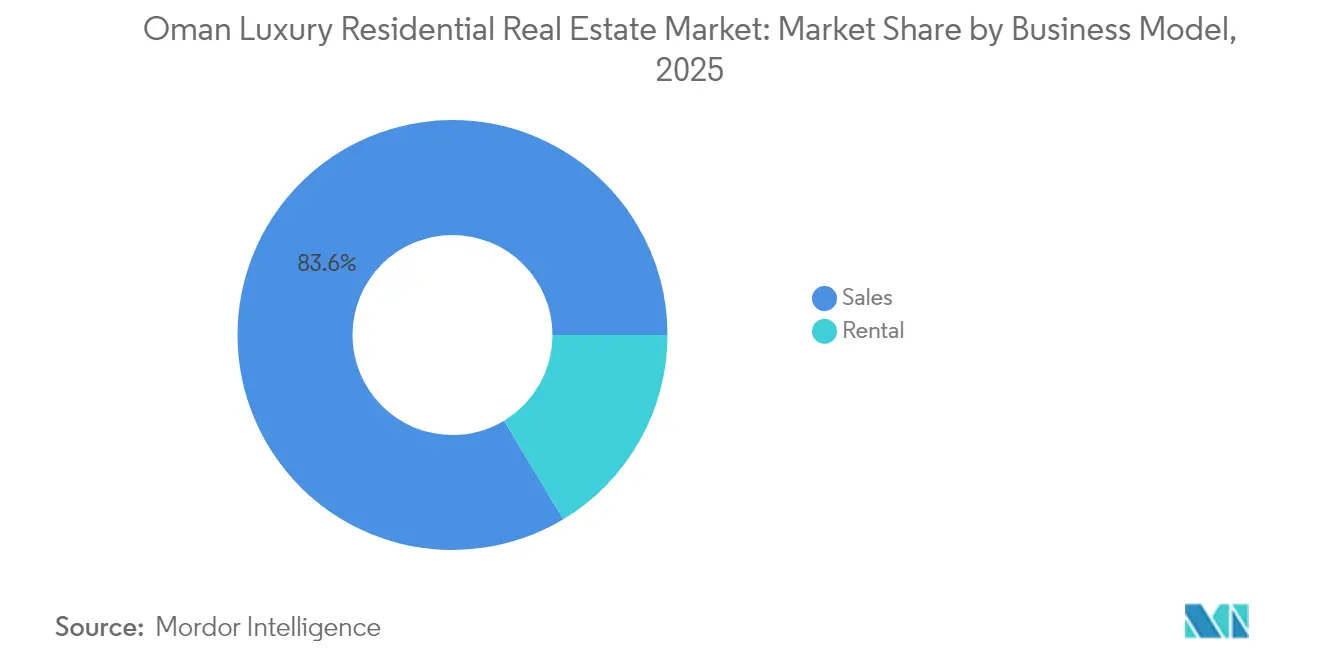

- By business model, sales dominated with an 83.62% share in 2025, and rentals are forecast to expand at an 7.88% CAGR to 2031.

- By property type, villas captured 56.78% of the Oman luxury residential real estate market share in 2025 and are advancing at an 8.14% CAGR through 2031.

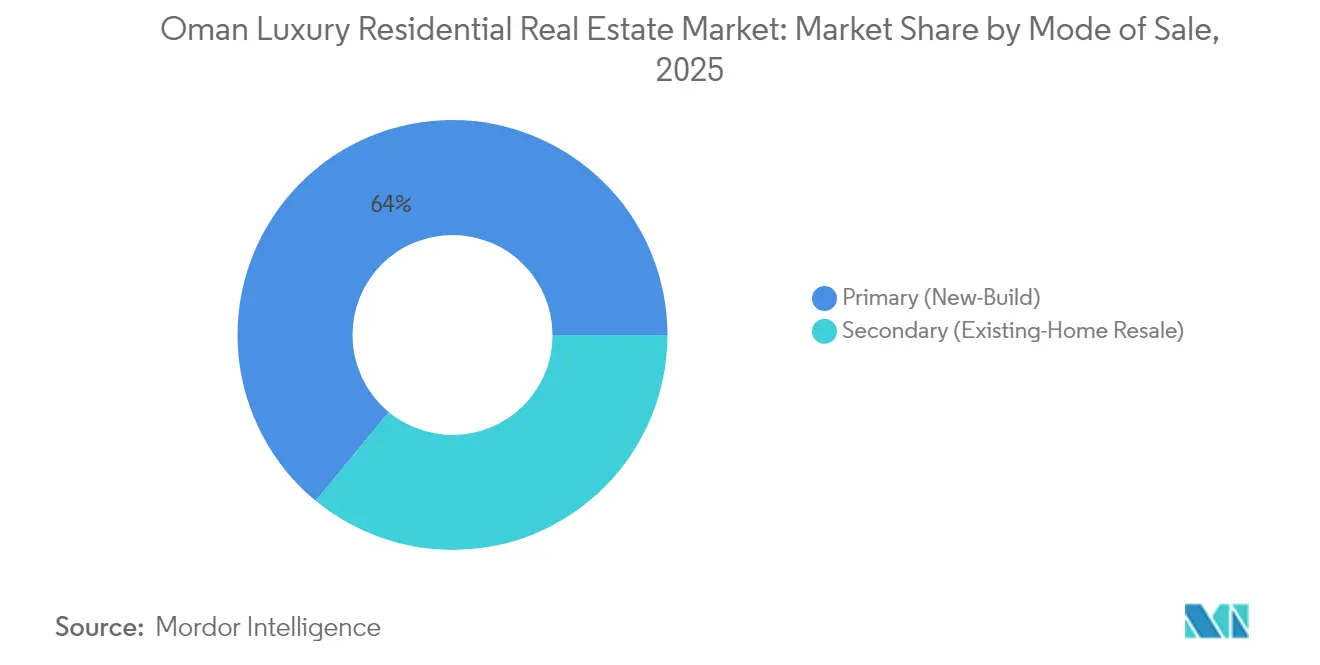

- By mode of sale, primary transactions commanded 64.02% of the Oman luxury residential real estate market size in 2025 and are projected to grow at an 8.05% CAGR between 2026 and 2031.

- By City, Muscat led with 56.15% revenue share in 2025, while Dhofar recorded the highest projected CAGR at 8.62% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Oman Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2040 urban development plans encouraging luxury mixed-use projects | +2.1% | National with flagship sites in Muscat, Salalah, and Al Duqm | Long term (≥ 4 years) |

| Government initiatives allowing foreign ownership in integrated tourism complexes and select zones | +1.8% | National with focus on Muscat and Dhofar tourism zones | Medium term (2–4 years) |

| Rising expatriate and executive population driving demand for premium villas and waterfront residences | +1.5% | Muscat core, spill-over to Dhofar and coastal areas | Short term (≤ 2 years) |

| Strategic location and lifestyle appeal attracting Gulf-based luxury buyers | +1.2% | National with early gains in Muscat, AIDA, and Yiti | Long term (≥ 4 years) |

| Growing preference for gated communities and branded residences with modern amenities | +1.0% | Muscat and emerging enclaves in Dhofar | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government initiatives allowing foreign ownership in integrated tourism complexes and select zones

Revised legislation now lets non-Omani purchase freehold units in integrated tourism complexes without the earlier 49% ceiling, opening a consistent demand channel from Gulf and broader international investors. The policy couples property purchase with long-stay visas, raising the attractiveness of the Oman luxury residential real estate market for portfolio diversification. Sultan Haitham City alone spans 15 million m², assigning explicit quotas for expatriate buyers to stimulate momentum in the primary market. Transparent title registration by the Ministry of Housing and Urban Planning sustains buyer confidence, while targeted zones minimize speculative pressure on legacy neighborhoods. Collectively, these measures add liquidity and accelerate project launches across Muscat and Salalah.

Rising expatriate and executive population driving demand for premium villas and waterfront residences

Skilled expatriates now form the largest cohort within Oman’s 1.81 million foreign residents, and their housing allowances increasingly exceed USD 60,000 per year. Executives in energy, finance, and technology prefer villas in secure, serviced precincts close to international schools and hospitals, fueling absorption of new waterfront stock around Al Mouj and Shatti Al-Qurum. Despite a modest dip in overall expatriate numbers in 2024, the proportion earning above USD 150,000 annually rose, strengthening purchasing power at the top end. Corporate leasing mandates for branded residences create predictable rental cash flows that entice global asset managers. The trend is most visible in Muscat but is spreading to Dhofar, as multinational staff on Salalah logistics projects[1]Maha Al-Balushi, “Statistical Yearbook 2025,” National Centre for Statistics & Information, ncsi.gov.om.

Strategic location and lifestyle appeal, attracting Gulf-based luxury buyers

Oman’s neutrality and pristine coastlines position the Oman luxury residential real estate market as a weekend-home hotspot for UAE and Saudi high-net-worth households. Indian nationals accounted for 30% of all foreign purchases in 2024, followed by British and Emirati buyers, confirming broad cross-border pull. Natural enclaves like Jabal al Akhdar offer mountain climates unmatched in the Gulf, diversifying luxury propositions beyond seafront living. Road upgrades that cut the Muscat–Dubai drive to under four hours have widened the catchment for secondary-home buyers. Environmental protections embedded in project approvals reassure eco-minded investors, reinforcing Oman’s brand as authentic, low-density luxury.

Growing preference for gated communities and branded residences with modern amenities

Affluent households gravitate to gated precincts like Trump Signature Villas at AIDA, where USD 200 million in resort amenities complements strict access control. Hospitality-branded projects such as Nobu Residences Muscat bundle concierge, wellness, and dining, adding service premiums of 15–20% over unbranded peers. Developers integrate solar panels, EV chargers, and AI-enabled security, aligning with global luxury benchmarks. This convergence of real estate and hospitality blurs lines between ownership and experience, lengthening average holding periods among investors who perceive both lifestyle and income upside[2]Yusif Al-Abri, “Omran 2025 Hospitality & Real Estate Pipeline,” Oman Tourism Development Company, omran.om.

Restraints Impact Analysis*

| Restraints | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Relatively small luxury buyer base limiting overall market depth | -1.3% | National with constraints in secondary cities | Medium term (2–4 years) |

| High construction costs and dependence on imported materials raising project pricing | -0.9% | National with higher impact on coastal and mountain sites | Short term (≤ 2 years) |

| Economic reliance on oil revenues creating volatility in luxury housing demand | -0.8% | National with spillover to expatriate sectors | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Relatively small luxury buyer base, limiting overall market depth

Oman’s population of 5.3 million hosts a narrower pool of ultra-high-net-worth individuals than Dubai or Riyadh, capping absorption for very large villa inventories. Projects in Musandam or interior cities must therefore stage releases in tranches to match demand velocity. Omanization policies that slowly reduce expatriate headcount could further shrink the executive tenant base, prompting developers to pivot toward regional investors. The thinner pipeline of million-dollar deals elongates sales cycles for projects priced above USD 2 million. Targeted marketing through GCC brokerage networks partly mitigates this structural restraint.

High construction costs and dependence on imported materials are raising project pricing

Up to 70% of steel, cement, and finishing items for luxury schemes still arrive by sea from Asia, exposing budgets to shipping delays and currency volatility. Global commodity inflation lifted average villa construction costs by 9% in 2024, forcing some developers to revise price lists mid-cycle. Coastal and mountain sites face additional logistics expenses that can add USD 60 per square meter to build costs. Although local suppliers are scaling capacity, near-term reliance on imports persists for specialized marble, fixtures, and smart-home systems. Developers respond with value engineering and bulk procurement to defend margins without diluting luxury standards[3]Khalid Al-Hinai, “Quarterly Construction Materials Price Index Q4 2024,” Ministry of Commerce, Industry & Investment Promotion, moci.gov.om.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Sales dominance with rental growth acceleration

Sales accounted for 83.62% of the Oman luxury residential real estate market in 2025 as buyers secured assets to capture future capital gains and tax-free resale benefits. Rental demand, however, is expected to grow 7.88% annually through 2031 as multinational firms relocate executives into Muscat’s financial district. Zero property tax and 6–8% gross yields encourage investors to purchase villas specifically for high-end leasing. Combined, these factors widen product diversity and deepen liquidity during market cycles.

Primary transactions dominate because developers offer phased payment plans and off-plan discounts that favor early entry. Meanwhile, the rental slice benefits from branded residences that provide professional tenant management, creating hands-off income for non-resident owners. The interplay between both models anchors the Oman luxury residential real estate market, ensuring that supply remains aligned with fluctuating ownership and occupancy preferences over the forecast horizon.

By Property Type: Villas lead market share and growth

Villas secured 56.78% market share in 2025 and are set to grow at an 8.14% CAGR, reflecting cultural preference for privacy, gardens, and multi-generational layouts. Three-bedroom waterfront homes along Al Mouj regularly achieve USD 1 million plus selling prices, underlining sustained depth in the premium bracket. Apartments appeal to young professionals seeking lock-and-leave convenience and stand to benefit from mixed-use vertical communities such as Al Khuwair Downtown.

Luxury villa projects now standardize smart-home control, solar rooftops, and shaded outdoor spaces to address climate concerns. Apartments increasingly integrate hospitality layers, blending serviced living with owner occupancy. These intertwined offers keep the Oman luxury residential real estate market size balanced between high-ticket villa revenue and higher-velocity apartment turnover, allowing developers to hedge against buyer preference shifts.

By Mode of Sale: Primary market strength with future resale potential

Primary sales represented 64.02% of the Oman luxury residential real estate market in 2025, supported by government land grants and joint ventures that de-risk early-phase funding. Buyers often lock units two to three years before completion, capturing first-mover pricing while developers secure forward funding. Secondary transfers, although smaller today, are anticipated to rise as projects like Al Mouj and AIDA mature and early investors capitalize on value appreciation.

Regulated escrow systems safeguard off-plan payments, reinforcing confidence in primary booking. Improved digital title platforms make resale faster and cheaper, which will help the secondary layer evolve into a vital liquidity valve. In tandem, the two channels strengthen the overall health of the Oman luxury residential real estate market by supporting both new supply and efficient recycling of built stock.

Geography Analysis

Muscat held 56.15% of the overall value in 2025, leveraging political status, multinational headquarters, and international schools to anchor premium demand. Landmark schemes such as Al Khuwair Downtown and Sultan Haitham City collectively exceed USD 5 billion in committed spend and broaden the urban luxury corridor from Seeb to Qurum. Branded giants like Nobu Residences Muscat and Trump International Oman inject global cachet, further lifting Muscat’s profile among cross-border investors. The capital’s mature utility grid and four major international hospitals underpin sustained absorption even during regional economic swings.

Dhofar is the fastest growing with an 8.62% CAGR, catalyzed by the USD 85.8 billion Vision 2040 allocation funding New City Salalah’s 7.3 km² waterfront blueprint. The unique Khareef monsoon transforms the landscape into lush greenery for three months, offering a climate hedge that is rare in the Gulf. Public spending on promenades, cultural hubs, and climate-resilient drainage reassures luxury buyers about long-term asset stability. Investor interest is also strong among wellness-focused Europeans who favor Salalah’s cooler summers over inland desert heat.

Musandam and the rest of Oman contribute niche volume but meaningful brand diversification. Musandam’s fjord-like inlets host USD 100 million resort-linked villas managed by Club Med, targeting ultra-high-net-worth buyers seeking privacy and maritime recreation. Al Duqm’s economic zone expansion attracts executive rentals anchored to logistics firms, while Jabal al Akhdar presents mountain villas at 2,400 meters that command wellness premiums. Together, these peripheral areas enrich the Oman luxury residential real estate market by spreading balance-of-payments benefits beyond the capital.

Competitive Landscape

The Oman luxury residential real estate market remains moderately fragmented. Local stalwarts such as AL Mouj Muscat, Tibiaan Properties, and Muriya compete alongside international entrants Dar Global, Emaar Hospitality, and Anantara. Partnerships blend global design language with local land access, evidenced by Dar Global’s alliance with the Trump Organization for Trump International Oman.

Amenity escalation is the primary competitive weapon. Developers add yacht marinas, signature golf courses, and wellness clinics rather than price discounts. Technology differentiation is rising; newer projects integrate AI-enabled energy controls and blockchain title verification to woo tech-savvy purchasers. Sustainability is becoming a distinct arena as carbon-neutral building methods transition from marketing pitch to permit prerequisite.

Competitive gaps persist in mountain retreats, eco-resorts, and mid-sized branded residences priced between USD 500,000 and USD 800,000. Firms that can master prefab modular systems may compress build times and gain pricing power against cost inflation. Overall, healthy rivalry spurs innovation without driving destructive discounting, keeping margins stable, and elevating project quality across the Oman luxury residential real estate market.

Oman Luxury Residential Real Estate Industry Leaders

AL Mouj Muscat

Tibiaan Properties

Saraya Bandar Jissah

Savills Oman

Dar Global

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The Ministry of Housing and Urban Planning unveiled the New City Salalah waterfront masterplan, covering 7.3 km² with 12,000 residential units for 60,000 residents, emphasizing climate resilience within the USD 85.8 billion Vision 2040 framework.

- July 2024: Dar Global launched Marriott Residences in AIDA, a USD 100 million shoreline community of 224 branded apartments slated for Q4 2027 handover under Marriott management.

- June 2024: Dar Global confirmed the USD 500 million Trump International Oman at AIDA target opening in Dec 2028, featuring a 140-key hotel, luxury villas, and an 18-hole golf course.

- June 2024: The Ministry of Housing and Urban Planning signed 35 agreements for Sultan Haitham City, allocating USD 2.6 billion to phase 1 across 5 million m² for 39,000 residents and 7,000 homes.

Oman Luxury Residential Real Estate Market Report Scope

The Oman Luxury Residential Real Estate Market is segmented by Type (Apartments and Condominiums, Villas, and Landed Houses), and by Key Cities (Muscat, Dhofar, Musandam, and the rest of Oman). The report offers market size and forecasts for the Oman Luxury Residential Real Estate Market in value (USD Billion) for all the above segments. The report offers market size and forecasts for the Oman Luxury Residential Real Estate Market in value (USD Billion) for all the above segments.

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Key Questions Answered in the Report

How fast is the Oman luxury residential real estate market expected to grow between 2026 and 2031?

The market is forecast to expand at a 7.52% CAGR, lifting value from USD 1.33 billion in 2026 to USD 1.92 billion by 2031.

Which segment currently commands the largest share of luxury transactions in Oman?

Sales transactions dominate with an 83.62% share in 2025, reflecting buyer preference for direct ownership and tax-free gains.

Why are villas outperforming apartments in Oman’s premium sector?

Villas offer privacy, outdoor space, and multi-generational layouts favored by Gulf families and expatriate executives, resulting in a 56.78% share and the fastest growth within the market.

What makes Dhofar the fastest-growing luxury region in the country?

The USD 85.8 billion Vision 2040 commitment to New City Salalah, plus Dhofar’s unique monsoon climate, drives an 8.62% CAGR in luxury demand.

Page last updated on: