Oilfield Equipment Rental Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

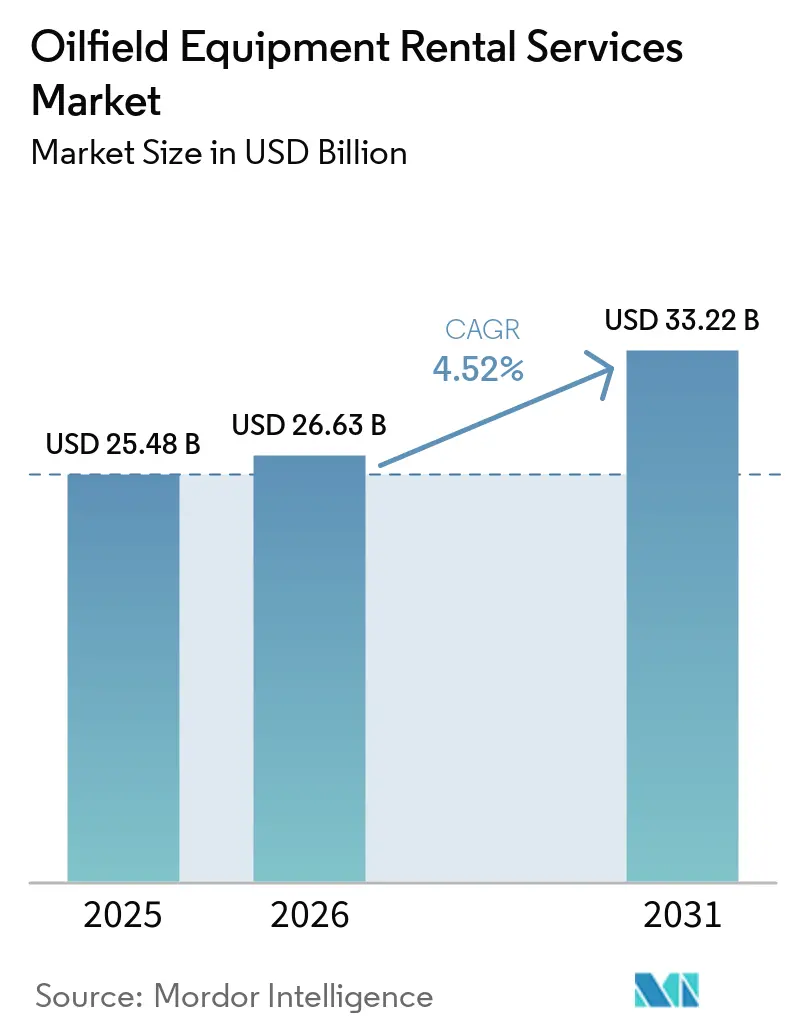

| Market Size (2026) | USD 26.63 Billion |

| Market Size (2031) | USD 33.22 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oilfield Equipment Rental Services Market Analysis by Mordor Intelligence

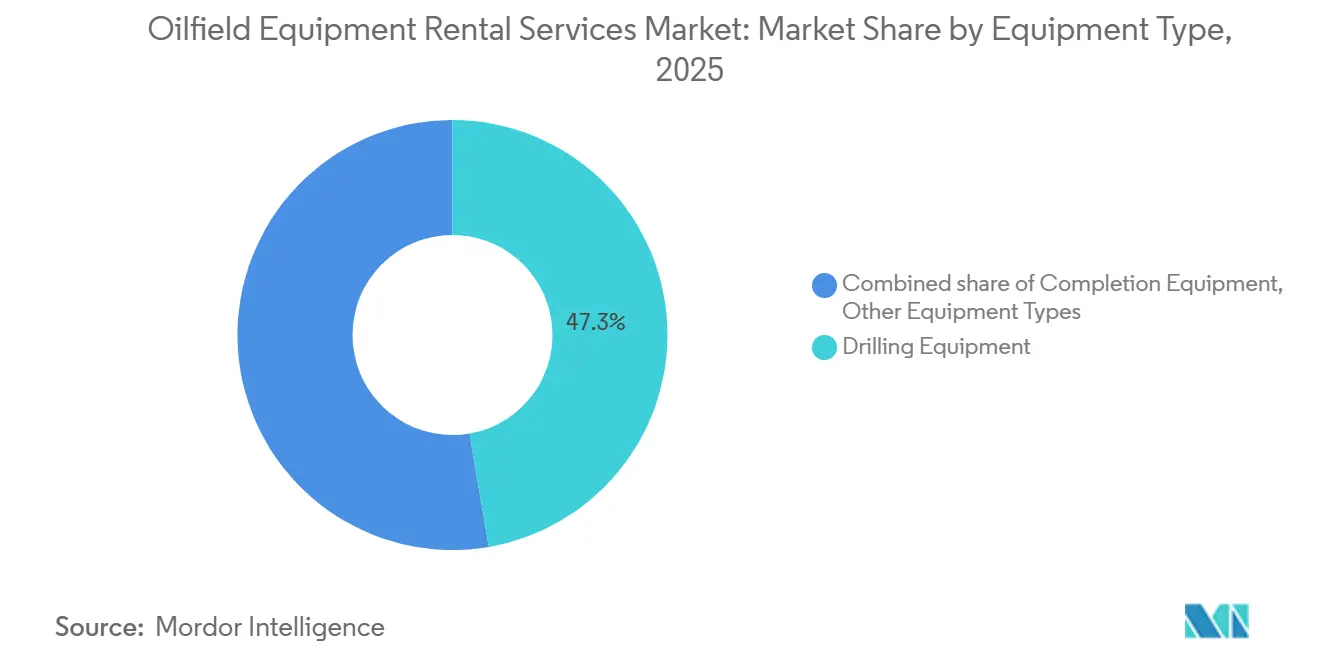

The Oilfield Equipment Rental Services Market size is expected to grow from USD 25.48 billion in 2025 to USD 26.63 billion in 2026 and is forecast to reach USD 33.22 billion by 2031 at 4.52% CAGR over 2026-2031. Uptake is strongest among exploration-and-production (E&P) companies that favor capital-light operating models, choosing to lease drilling rigs, pressure-pumping fleets, and completion tools rather than own them outright. North America supplied 38.5% of global 2025 revenue, yet Asia-Pacific is forecast to be the fastest growing region on the back of China’s unconventional resource push and India’s import-substitution program.[1]Company press office, “CNPC Launches Seven-Year Action Plan,” China Daily, chinadaily.com.cn Drilling equipment captured nearly half of 2025 turnover, while completion equipment is advancing quickly as modular frac systems become the norm.[2]Product sheet, “Leucipa Automated Well Construction,” Baker Hughes, bakerhughes.com Offshore demand, though smaller than onshore, is accelerating as Petrobras, BP, and ADNOC green-light multibillion-dollar deep-water developments that require long-cycle rental contracts for rigs and subsea hardware.[3]Corporate press release, “Petrobras Approves USD 5.8 Billion Investment,” Petrobras, petrobras.com.br Competitive intensity remains elevated, with the five largest integrated providers holding about 40% of revenue while dozens of regional specialists battle on logistics and price.[4]IR presentation, “Fourth-Quarter 2025 Results,” Schlumberger, slb.com

Key Report Takeaways

- By equipment type, drilling equipment led with 47.3% of 2025 revenue; completion equipment are projected to expand at a 5.2% CAGR through 2031.

- By location, onshore led with 68.9% of 2025 revenue; offshore are projected to expand at a 5% CAGR through 2031.

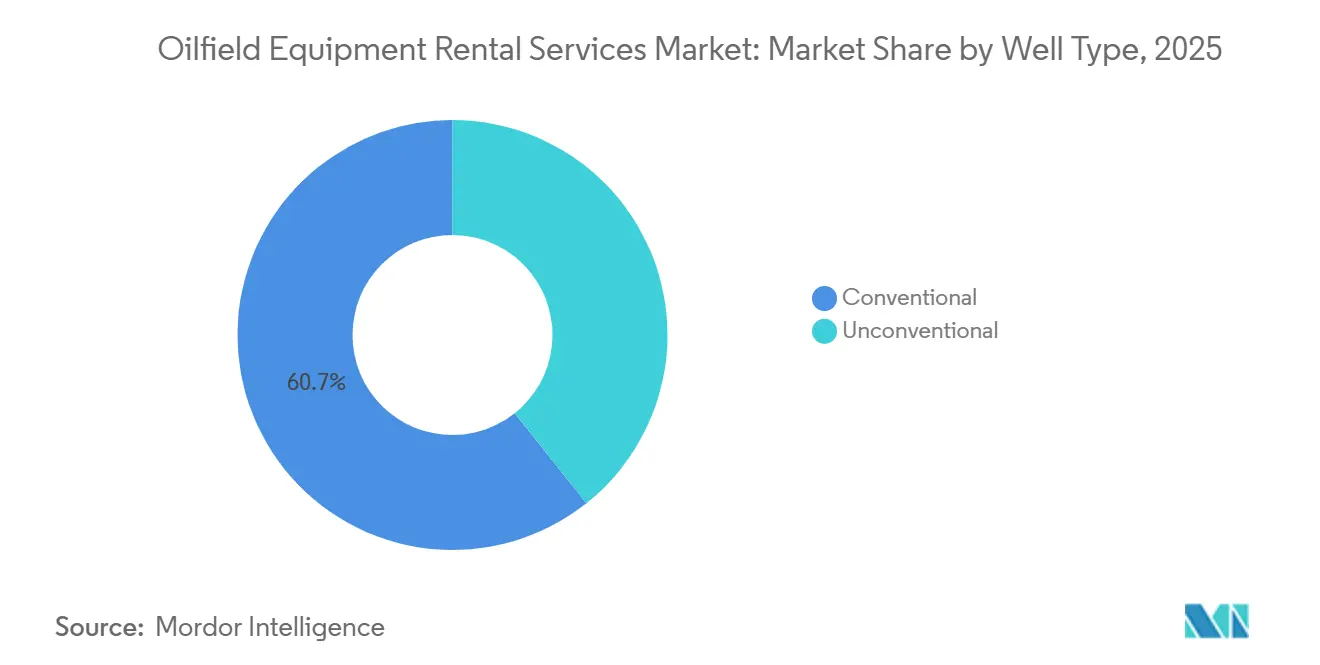

- By well type, conventional wells commanded 60.7% of 2025 revenue, while unconventional activity is advancing at a 5.7% CAGR to 2031.

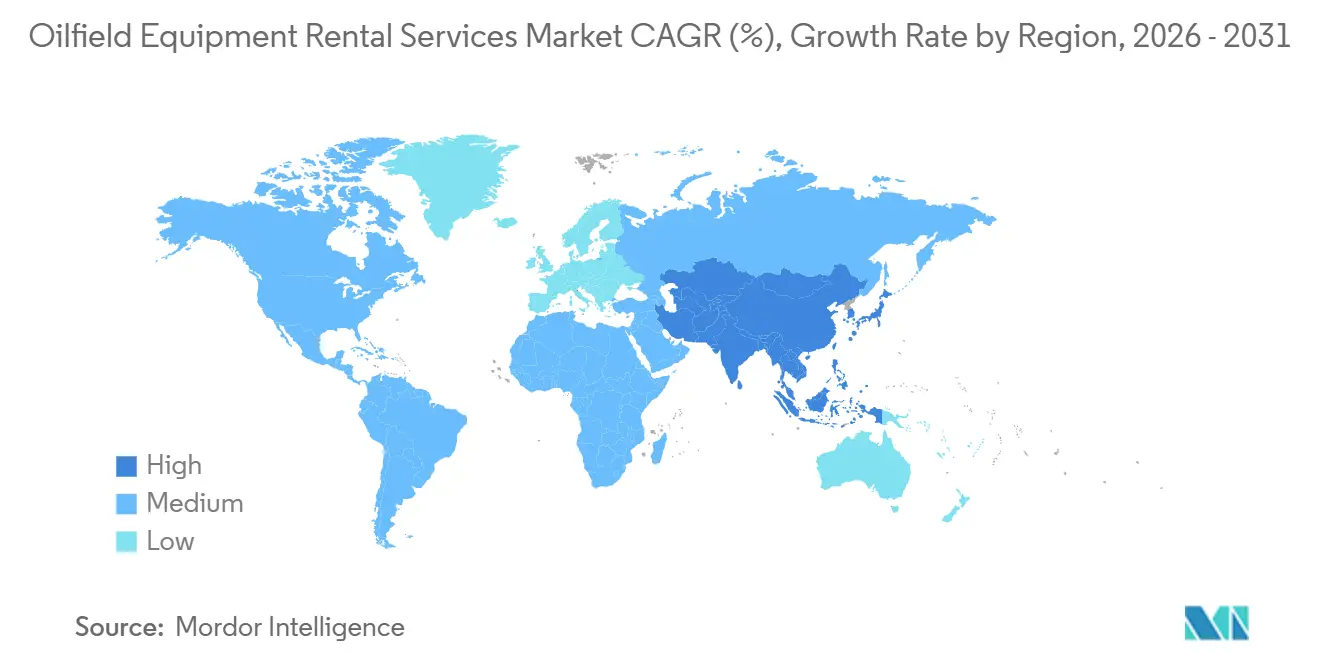

- Geographically, North America held 38.5% of 2025 turnover, whereas Asia-Pacific is forecast to register a 5.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oilfield Equipment Rental Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising shale & tight-oil drilling activity | +0.9% | North America (Permian, Eagle Ford, Bakken); emerging in Argentina Vaca Muerta | Medium term (2–4 years) |

| Offshore deep-water CAPEX rebound | +0.8% | South America (Brazil pre-salt), North America (Gulf of Mexico), Europe (Norway), Middle East & Africa (Guyana, Namibia) | Long term (≥ 4 years) |

| Cap-ex-lite preference among E&Ps | +0.7% | Global, with strongest adoption in North America shale and Asia-Pacific NOCs | Short term (≤ 2 years) |

| Ageing global rig fleet replacements | +0.5% | Global; acute in Middle East jackup markets and North Sea harsh-environment units | Medium term (2–4 years) |

| Modular well-site automation rental demand | +0.4% | North America, Middle East, Asia-Pacific | Medium term (2–4 years) |

| Low-carbon electrified rental fleets | +0.3% | North America, Europe (Norway, UK) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Shale & Tight-Oil Drilling Activity

Horizontal drilling in the Permian and Eagle Ford continues to shorten well cycles, enabling more wells per rig-year even with a lower total rig count. Modular rental equipment, pressure-pumping spreads, wireline units, and coiled-tubing systems supports simulfrac and trimulfrac operations that fracture multiple wellbores at once, sustaining utilization despite commodity volatility. YPF and Shell increased investment in Argentina’s Vaca Muerta, importing North American rental fleets to accelerate development.

Offshore Deep-Water CAPEX Rebound

Petrobras approved USD 5.8 billion for two pre-salt hubs that will each require multi-year drillship campaigns. BP’s Tiber-Guadalupe project in the Gulf of Mexico demands 20,000-psi subsea architectures supplied almost entirely on a rental basis. Transocean’s 2025 contract wins added USD 2.3 billion to backlog, signaling durable offshore rental demand.

Cap-Ex-Lite Preference Among E&Ps

Schlumberger’s asset-light leasing model produced USD 9.2 billion in fourth-quarter 2025 revenue as operators shifted fixed capital to variable operating expenses. India’s ONGC moved 30% of its land-rig fleet to rental agreements to free funds for offshore exploration.

Ageing Global Rig Fleet Replacements

With a median offshore-rig age of 22 years, operators are retiring older units and leasing modern, high-spec rigs that meet stricter safety and automation standards. Equinor’s harsh-environment Rosebank program specifies post-2010 semisubs, narrowing the pool of qualified rental assets.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility | -0.6% | Global, with highest sensitivity in North America shale and offshore frontier basins | Short term (≤ 2 years) |

| Stricter environmental regulations | -0.4% | North America (EPA methane rules), Europe (EU taxonomy), Middle East (flaring bans) | Medium term (2–4 years) |

| Margin compression from price wars | -0.3% | North America pressure-pumping sector, Middle East jackup dayrates | Short term (≤ 2 years) |

| Supply-chain shortages for HPHT parts | -0.2% | Offshore deepwater markets (Gulf of Mexico, Brazil, West Africa, North Sea) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Volatility

Brent spiked to USD 103-118 per barrel after the temporary Strait of Hormuz closure in early 2026, then fell below USD 82 within weeks, prompting E&Ps to delay rig reactivations and squeeze discretionary budgets. U.S. land rig activity slipped 4% month-over-month in February 2026 despite the brief price rally.

Stricter Environmental Regulations

The U.S. EPA’s Methane Emissions Reduction Program mandates quarterly leak surveys and introduces a Waste Emissions Charge rising to USD 1,500 per metric ton in 2026, lifting rental-fleet operating costs by 8-12%. Norway now requires net-zero Scope 1 rig emissions by 2030, accelerating demand for electrified jackups powered via shore grid.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Drilling Dominates, Completion Accelerates

Drilling equipment captured 47.3% of 2025 revenue, reflecting multi-year rig-rental contracts that underpin large capital programs. The oilfield equipment rental services market size for completion equipment is projected to expand at a 5.2% CAGR, outpacing aggregate growth as simulfrac operations multiply. Helmerich & Payne’s FlexRig platform trimmed total-depth times by 30% in West Texas, illustrating how high-spec rentals justify premium dayrates.

Production and intervention tools, workover rigs, artificial-lift systems, and well-test packages serve mature fields and rotate through shorter rental cycles. Weatherford booked USD 1.8 billion in 2025 artificial-lift rentals, with electric submersible pumps representing 60% of segment sales.

By Location: Onshore Leads, Offshore Gains Momentum

Onshore environments supplied 68.9% of 2025 turnover thanks to shale activity and Middle Eastern development drilling. Offshore contracts, however, are set to grow at a 5.0% CAGR as Petrobras, BP, and ADNOC execute large deep-water programs that lock in long-cycle dayrates. Transocean’s backlog reached USD 2.3 billion in 2025 as dayrates for ultra-deepwater drillships approached USD 500,000, underscoring the premium offshore segment of the oilfield equipment rental services market share.

By Well Type: Conventional Holds Share, Unconventional Surges

Conventional wells still account for 60.7% of utilization, mainly in the Middle East and offshore basins. Yet unconventional activity is expanding at a 5.7% CAGR, supported by horizontal-rig fleets optimized for pad drilling. FlexRigs deliver faster cycles, keeping rental demand resilient even when rig counts stagnate.

Geography Analysis

North America generated 38.5% of 2025 revenue, anchored by the Permian Basin and Gulf of Mexico. Despite a land-rig count well below the 2019 peak, operators completed more wells by using simulfrac techniques that intensify rental-equipment turnover. BP’s Tiber-Guadalupe sanction locks in ultra-deepwater drillship and subsea rentals through 2031.

Asia-Pacific is forecast to grow at a 5.9% CAGR through 2031 as China’s seven-year unconventional plan calls for 120 additional drilling rigs most of them leased and India’s ONGC channels savings from onshore fleet rentals into offshore exploration. Petronas awarded six jackup charters in 2025, signaling a rebound for Southeast Asian shallow-water rentals.

Europe shows mixed dynamics. Norway continues to approve projects AkerBP’s Johan Castberg and Equinor’s Rosebank requiring harsh-environment semisubs leased from a narrow supplier base. In contrast, UK investment is cooling under higher taxes, dampening future demand for rental assets.

South America’s momentum is dominated by Brazil. Petrobras’ SEAP hubs and BW Energy’s Maromba field will each consume multiple drillships and subsea packages under long-term rentals. Argentina’s Vaca Muerta continues to import frac and drilling rentals from North America.

The Middle East and Africa remain resilient. ADNOC Drilling operated 118 units at end-2025, much of it leased, while Saudi Aramco’s budget focuses on gas, leaving upstream drilling to third-party rental providers. Nigeria and Namibia are bright spots for deep-water rentals as new discoveries move toward appraisal.

Competitive Landscape

Market concentration is moderate. Schlumberger, Halliburton, and Baker Hughes together captures significant share of global rental revenue, leveraging global scale, automation technology, and compliance expertise. Schlumberger’s asset-light model exemplifies the shift toward performance-based leasing. Halliburton, meanwhile, is rolling out its FloConnect digital ecosystem across Latin America after successful North American deployments.

Technology differentiation is widening. Baker Hughes’ Leucipa platform couples autonomous pipe handling with predictive maintenance, reducing invisible lost time by one-quarter during Permian trials. Smaller challengers such as Expro and Integrated Well Services target mobility advantages, offering containerized packages that mobilize in 48 hours.

Environmental compliance is a growing moat. U.S. methane rules raise operating costs but favor large providers that can amortize monitoring gear across extensive fleets, while Norway’s net-zero rig mandate accelerates demand for electrified rigs such as Patterson-UTI’s EcoCell platform.

Oilfield Equipment Rental Services Industry Leaders

Schlumberger Limited

Halliburton Company

Baker Hughes Company

Weatherford International

Superior Energy Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Transocean secured a 5-year, USD 1.2 billion charter with Petrobras for the Deepwater Atlas drillship in the Santos Basin pre-salt.

- January 2026: Schlumberger reported USD 9.2 billion in Q4 2025 revenue, buoyed by rental agreements, and acquired a Norwegian subsea-services firm for USD 320 million.

- December 2025: The Toro Company completed its acquisition of Tornado Infrastructure Equipment Ltd., a Calgary-based hydrovac excavation solutions manufacturer. This acquisition strengthens The Toro Company’s construction portfolio, including oilfield equipment rental services, and enhances its market presence. Tornado’s expertise complements existing brands like Ditch Witch, reinforcing leadership in underground construction and energy markets.

- February 2025: Valaris won a 3-year, USD 540 million contract from BP for jackup VALARIS 249 in the UK North Sea.

Global Oilfield Equipment Rental Services Market Report Scope

Oilfield equipment rental services offer temporary and cost-efficient access to specialized machinery, including drilling tools, pressure control units, and pumps, utilized in oil and gas exploration, extraction, and maintenance. These services enable operators to lease high-cost, short-term assets instead of purchasing them, providing operational flexibility and lowering capital expenditure.

The Oilfield Equipment Rental Services Market is segmented into equipment type, location, well type, and geography. By equipment type, the market is segmented into drilling equipment, production and intervention equipment, completion equipment, and other equipment types. By location, the market is segmented into onshore and offshore. By well type, the market is segmented into conventional and unconventional wells. The report also covers the market size and forecasts for the oilfield equipment rental services market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Drilling Equipment |

| Production and Intervention Equipment |

| Completion Equipment |

| Other Equipment Types |

| Onshore |

| Offshore |

| Conventional |

| Unconventional |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Norway |

| United Kingdom | |

| Russia | |

| Netherlands | |

| Germany | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Iran | |

| Nigeria | |

| South Africa | |

| Rest of Middle East and Africa |

| By Equipment Type | Drilling Equipment | |

| Production and Intervention Equipment | ||

| Completion Equipment | ||

| Other Equipment Types | ||

| By Location | Onshore | |

| Offshore | ||

| By Well Type | Conventional | |

| Unconventional | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Norway | |

| United Kingdom | ||

| Russia | ||

| Netherlands | ||

| Germany | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Iran | ||

| Nigeria | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the oilfield equipment rental services market be by 2031?

The oilfield equipment rental services market size is forecast to reach USD 33.22 billion by 2031.

Which equipment segment is growing fastest?

Completion equipment is projected to grow at a 5.2% CAGR, the quickest among all categories.

Why are E&Ps shifting to rental models?

Leasing converts fixed capital into variable costs, offering flexibility amid commodity-price swings and regulatory uncertainty.

Which region will expand the quickest through 2031?

Asia-Pacific is expected to post the highest regional CAGR at 5.9%, driven by unconventional programs in China and India.

How are environmental rules influencing rental demand?

Methane-leak regulations in the United States and net-zero mandates in Norway are accelerating investment in electrified and low-emission rental fleets.

Page last updated on: