Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

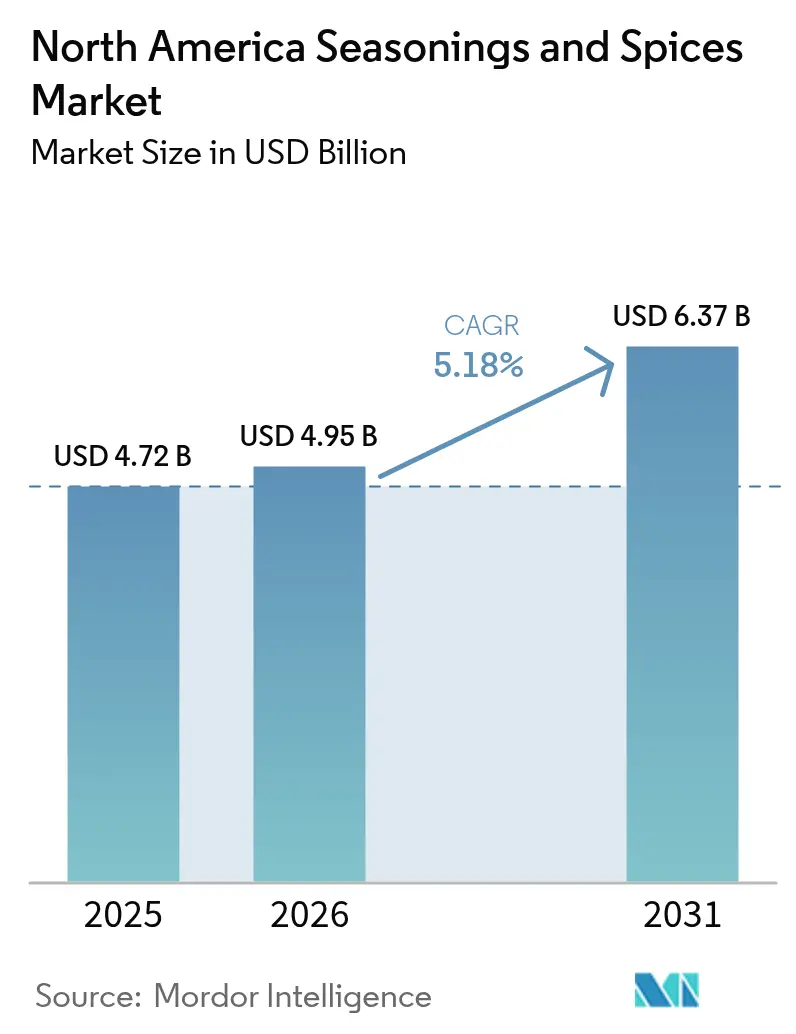

| Base Year Market Size (2025) | USD 4.72 Billion |

| Market Size (2026) | USD 4.95 Billion |

| Market Size (2031) | USD 6.37 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

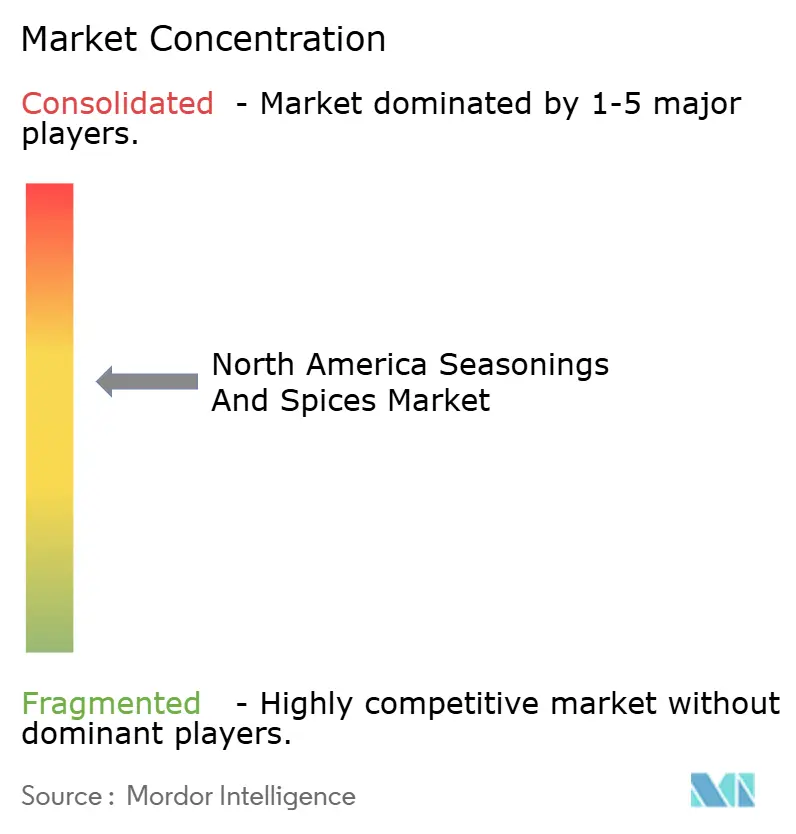

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Seasonings And Spices Market Analysis by Mordor Intelligence

The North America seasonings and spices market size in 2026 is estimated at USD 4.95 billion, growing from 2025 value of USD 4.72 billion with 2031 projections showing USD 6.37 billion, growing at 5.18% CAGR over 2026-2031. Growth in the seasonings and spices segment is being driven by shifting consumption patterns in processed and packaged foods, along with tighter food safety regulations and evolving supply chain structures. Large-scale food manufacturers are prioritizing consistent, high-performance blends that deliver standardized flavor profiles across production batches, while also responding to demand for clean-label and sodium-reduction formulations. Expansion in ready-to-eat, snacks, and convenience meal categories is further accelerating bulk demand. At the same time, stricter controls on pesticide residues, microbial limits, and traceability requirements are increasing compliance complexity, favoring suppliers with advanced quality assurance systems and integrated sourcing networks.

Key Report Takeaways

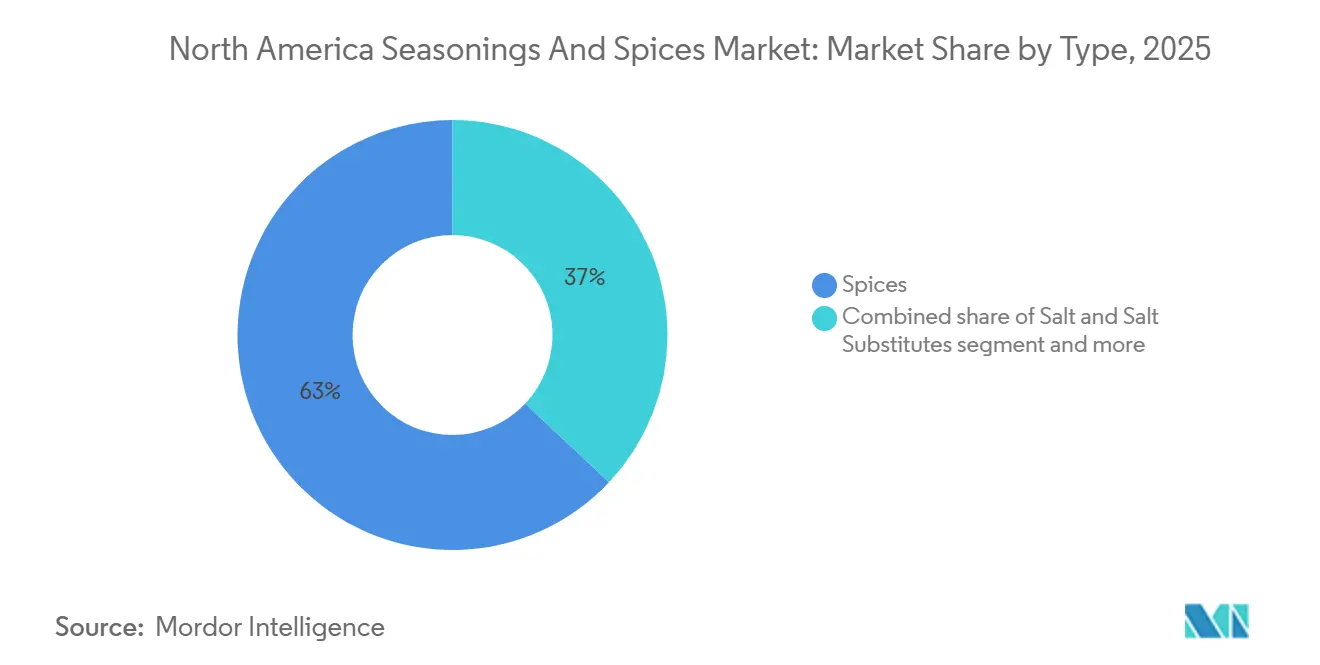

- By type, spices led with 62.98% of North America seasonings and spices market share in 2025 while herbs and seasonings are advancing at a 5.84% CAGR through 2031.

- By category, the conventional segment held 82.95% share of the North America seasoning and spices market size in 2025, while organic products are projected to grow at a 5.62% CAGR to 2031.

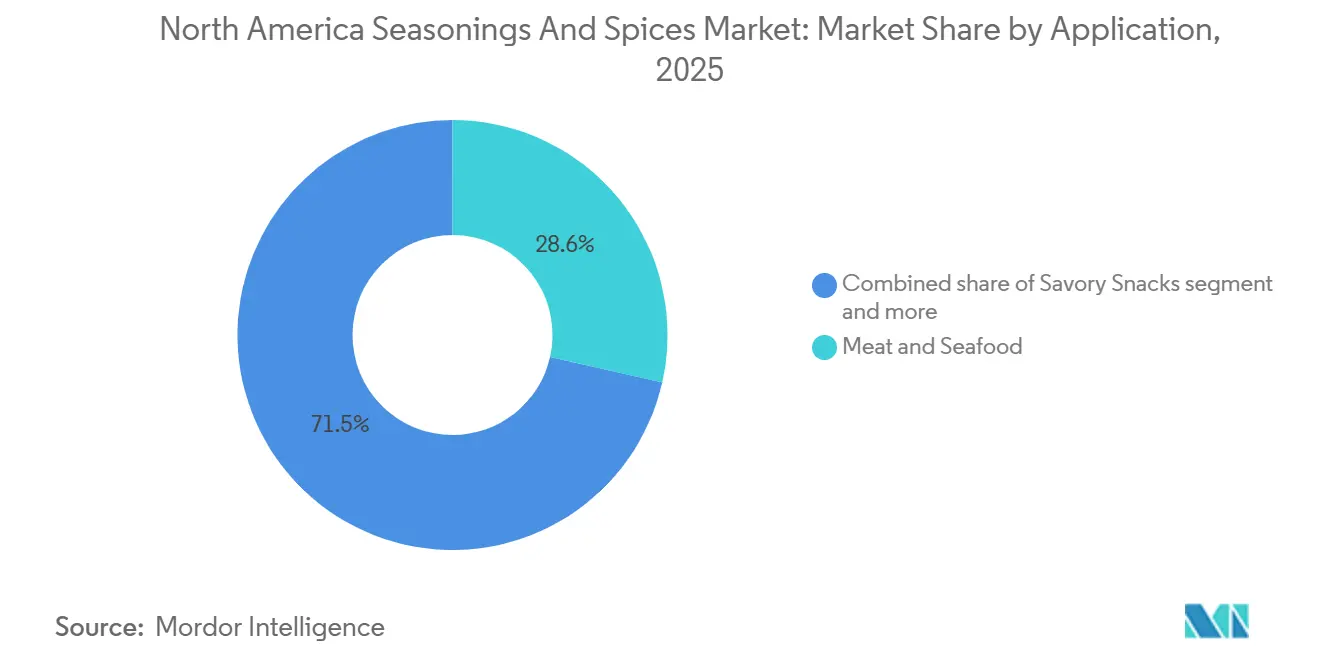

- By application, meat and seafood accounted for a 28.55% share of the North America seasoning and spices market size in 2025, whereas savory snacks are forecast to post a 6.02% CAGR through 2031.

- By geography, the United States commanded 72.55% revenue share in 2025, while Mexico is poised to record the fastest expansion at a 5.89% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Seasonings And Spices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for healthier and higher-quality ingredients | +0.80% | United States coastal metros and Canadian urban hubs | Medium term (2-4 years) |

| Increasing multicultural demographics driving demand for diverse ethnic and global flavors | +0.90% | Toronto, Vancouver, Los Angeles, Houston, Miami | Long term (≥ 4 years) |

| Expansion of the convenience, ready-to-cook, and processed food sectors | +1.00% | United States and Canada, spill-over to northern Mexico | Short term (≤ 2 years) |

| Growing preference for convenient, ready-to-use seasoning blends | +0.70% | United States, Canada, emerging in Mexico City and Monterrey | Medium term (2-4 years) |

| Trending demand for organic and clean-label spices and seasonings | +0.90% | United States and Canada | Medium term (2-4 years) |

| Stronger focus on sustainable and environmentally responsible sourcing practices | +0.50% | Led by United States and Canadian retailers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for healthier and higher-quality ingredients

Premium positioning remains central to differentiation in the spices and seasonings market as food manufacturers and processors face heightened consumer expectations for ingredient authenticity and transparent sourcing. Ethnically diverse eating habits continue to shape product demand, with global regulators like the Food and Drug Administration (FDA)’s Food Safety Modernization Act elevating quality standards and boosting confidence in compliant suppliers. The import of spices in the United States increased from USD 1.64 billion in 2023 to USD 1.98 billion in 2025, underscoring robust industrial use and reliance on international supply chains [1]Source: Trade Map, "Trade Map Database", trademap.org. Robust oversight from agencies such as the Canadian Food Inspection Agency and traceability programs enforced by bodies like India’s Spices Board enhance trust through systematic testing and certification. Industry initiatives on environmentally responsible sourcing further reinforce premium status by reflecting values important to discerning buyers. To justify higher price points, manufacturers increasingly spotlight traceable origin, advanced processing technologies, and improved nutritional or functional benefits. Investments in analytical quality assurance, such as spectroscopy and DNA verification, raise production costs marginally but reduce compliance risks, strengthening end‑market confidence in premium spice ingredients for food manufacturing applications.

Increasing multicultural demographics driving demand for diverse ethnic and global flavors

The growing presence of diverse ethnic populations in the United States and Canada is reshaping demand for seasonings and spices in food manufacturing. Asian communities, particularly South Asian and Chinese households, consistently consume higher amounts of fruits, vegetables, and seafood, while Hispanic households favor meat-based dishes, driving demand for culturally tailored spice blends. Food producers are responding by expanding ethnic product lines and experimenting with fusion flavors that combine traditional tastes with contemporary culinary trends. This shift has created lucrative opportunities for specialty spice importers and regional distributors who leverage strong community connections and deep knowledge of flavor preferences. Ethnic retailers are increasing dedicated shelf space, while co-packing operations in North America are producing localized blends to reduce tariffs and accelerate delivery times. Overall, the market is evolving toward more customized, culturally resonant seasoning solutions that support both mainstream and niche food manufacturing needs.

Expansion of the convenience, ready-to-cook, and processed food sectors

The shift in consumer lifestyles is reshaping meal preparation, prompting food manufacturers to innovate in advanced seasoning systems tailored for ready-to-cook and ready-to-eat applications. Busy households and professionals increasingly seek efficient ways to achieve complex, restaurant-quality flavors at home, driving investment in pre-measured and multifunctional spice blends. Companies like Kerry Group have demonstrated strong growth in the Americas by integrating cutting-edge seasoning technologies, such as Tastesense Salt, which reduces sodium without compromising flavor. Ready-meal and meal-kit segments are rapidly expanding, supported by precise portion-controlled spice solutions that simplify cooking. Protein processors are enhancing per-unit seasoning to deliver diverse global flavor profiles across poultry and meat products. Centralized blending and seasoning hubs now streamline operations for quick-service chains, reducing in-store labor requirements. Regulatory frameworks from the Food and Drug Administration (FDA) provide guidance on seasoning labeling, while clean-label initiatives encourage the use of natural spice extracts, facilitating reformulation without artificial additives. These trends collectively highlight the critical role of sophisticated spice systems in modern food manufacturing.

Growing preference for convenient, ready-to-use seasoning blends

Pre-mixed seasoning solutions are increasingly driving growth in food manufacturing, as producers seek efficient, reliable flavor delivery without manual measurement. Urban-focused production facilities prioritize convenience, supporting dual-income households with ready-to-use formulations that maintain taste quality. Investments in industrial blending lines and advanced packaging technologies are helping extend shelf life while meeting volume demands. E-commerce channels enable direct access to niche and specialty blends that conventional retail may not carry. Meanwhile, foodservice operations favor portion-controlled systems, ensuring consistent flavor across multiple locations. Regulatory frameworks, such as Canadian preventive controls for spice processing, guide safety and compliance in large-scale blend production. Companies respond by developing proprietary recipes that differentiate products while adhering to labeling and ingredient disclosure requirements, supporting both innovation and operational efficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perishability and limited shelf life | -0.40% | Fresh-herb segments in United States and Canada | Short term (≤ 2 years) |

| Regulatory challenges on quality and labeling | -0.50% | Under USMCA harmonization | Medium term (2-4 years) |

| Supply-chain volatility and raw-material swings | -0.60% | India-sourced pepper, turmeric, chili | Short term (≤ 2 years) |

| Adulteration and authenticity concerns | -0.30% | Ground spice categories globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in supply chains and fluctuations in raw material availability

Supply chain challenges continue to strain the food manufacturing spice and seasoning market, pushing up costs and limiting availability, particularly for smaller processors with limited sourcing options. Rising input prices and labor costs have led farmers in major producing regions to cut planted acreage, while unpredictable weather is adding pressure on specialty varieties, even as standard powders and granules remain accessible. In response, industry bodies like the American Spice Trade Association (ASTA) have partnered with logistics groups to secure better freight rates and streamline supply chains. Importers are increasingly diversifying sourcing geographically and investing in advanced inventory management systems to mitigate disruptions, though these measures tie up working capital and add operational complexity. Recent trade policy changes and tariffs have amplified import costs, prompting companies to adopt strategic approaches such as extended stockpiling and tariff-focused planning. These supply pressures are reflected in Food and Agriculture Organization (FAO)’s 2024 global food import bill, which rose 3.6 percent to nearly USD 2.1 trillion, largely driven by a 29.3 percent surge in costs for coffee, tea, cocoa, and spices [2]Source: Food and Agriculture Organization, "FAO Food Outlook", fao.org. Looking ahead, market participants are expected to continue prioritizing resilience and agility in sourcing and logistics to navigate ongoing volatility and secure steady supply for food manufacturing applications.

Increasing concerns over adulteration and authenticity of spices and seasonings

In North America, growing concerns over adulteration and the authenticity of spices and seasonings are driving stringent regulatory requirements that challenge food manufacturers, especially smaller importers and specialty producers. The FDA and Canadian authorities have intensified monitoring for contaminants such as pesticides, heavy metals, ethylene oxide, and undeclared fillers, while demanding robust documentation and testing systems to verify product integrity. Ensuring authenticity through methods like DNA barcoding, NIR analysis, and blockchain traceability requires substantial investment, often feasible only for large processors. These measures are critical to prevent issues such as fraudulent substitution, contamination, or mislabeling, which have led to recalls and delistings in past years. Established companies with strong quality control and compliance infrastructure are able to maintain credibility and retailer trust, whereas new entrants struggle with technical and financial barriers. As a result, retailers are increasingly limiting their supplier base to certified and verifiable partners, emphasizing traceability, purity, and product authenticity in their procurement decisions.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Spices Dominate Traditional Applications

In 2025, traditional spices held a dominant 62.98% share of the North America seasonings and spices market, driven by black pepper, chili, garlic, and mustard. Their widespread integration into meat, seafood, sauces, and ethnic food production underscores their essential role in flavor development. Key spices such as sesame, cinnamon, paprika, and onion continue to support both large-scale food manufacturing and specialty processed products, maintaining market stability even amid fluctuating raw material availability. Processors are increasingly exploring oleoresins and spice extracts to manage cost volatility and ensure consistent flavor quality.

Meanwhile, herbs and blended seasonings are projected to grow at a 5.84% CAGR through 2031, fueled by consumer demand for fresh, natural, and health-oriented flavor solutions in prepared foods. Innovative applications in ready-to-cook and clean-label products are expanding the use of basil, oregano, mint, and other botanicals, while chili and paprika remain popular for visual appeal and bold taste. Manufacturers are increasingly experimenting with less conventional spices, including galangal and za’atar, to diversify flavor offerings and respond to evolving culinary trends in processed and packaged food segments. Urban hydroponic cultivation and improved supply chains are enabling fresher herbs with longer shelf life for industrial applications.

By Category: Organic Acceleration Despite Conventional Dominance

Conventional seasonings and spices continue to dominate the food manufacturing segment, capturing 82.95% of the market in 2025. Their stronghold is supported by well‑developed supply chains that guarantee reliable inventory, cost‑effective pricing that appeals to large buyers, and far‑reaching distribution networks that efficiently serve mainstream production needs. Sterilization practices such as ethylene oxide treatment further extend shelf life, making these products a preferred choice for conventional food processors. Manufacturers also benefit from predictable quality and consistent sensory profiles that help standardize recipes at scale. As a result, conventional offerings remain deeply integrated into industrial kitchens and packaged food production lines, reinforcing their market leadership and cost advantage.

Meanwhile, organic spices are gaining momentum within food manufacturing, projected to grow at a 5.62% CAGR through 2031, driven by rising demand for USDA‑certified ingredients as clean‑label and health‑oriented formulations expand. Health benefits, reduced pesticide residues, and sustainability claims enhance their appeal, allowing manufacturers to sustain premium pricing even amid supply constraints. According to a recent 2025 IFIC consumer survey, about 30% of United States shoppers report that they look for “organic” labels when choosing foods, reflecting meaningful consumer interest in organic attributes [3]Source: International Food Information Council, "IFIC Food and Health Survey", ific.org. However, limited domestic cultivation and certification costs continue to constrain supply, keeping premiums elevated. This tiered market positioning allows food manufacturers to balance cost, quality, and clean‑label appeal while meeting evolving consumer expectations and premium product trends.

By Application: Meat and Seafood Leadership Alongside Savory Snacks Growth

The meat and seafood segment commands a 28.55% share of the North America seasonings and spices market, driven by processors increasing the use of global rubs, marinades, and flavor enhancers. Rising protein consumption among Hispanic communities and strong seafood demand in non-Hispanic Asian populations support sustained growth. Advanced seasoning systems are critical in elevating flavor profiles, masking off-notes, and extending shelf life for protein products. Manufacturers are increasingly experimenting with bold and ethnic flavors, such as smoked paprika, fermented garlic, and citrus blends, to meet evolving consumer palates. This trend is also fueling innovation in ready-to-cook and pre-marinated protein offerings for retail and foodservice channels.

Savory snacks are set to grow at a 6.02% CAGR through 2031 as manufacturers innovate with flavor delivery technologies to meet demand for convenient, restaurant-quality taste experiences. Leading players like Kerry Group’s Americas division have reported notable volume gains, particularly through integrating sophisticated seasoning solutions in chips, puffs, and other snack coatings. Brands are reformulating coatings with natural extracts, reducing sodium while retaining bold flavor appeal. Additionally, the segment benefits from growing consumer preference for on-the-go snacking and premium taste experiences that mimic restaurant or artisanal flavors.

Geography Analysis

The United States accounted for 72.55% of the North American seasoning and spices market in 2025, driven by its expansive food manufacturing sector and a well-established distribution network that supplies both mainstream and niche spice formulations. Manufacturers increasingly cater to health-conscious and sustainability-focused products, including organic and specialty seasonings. Demographic trends, highlighted by USDA data, show non-Hispanic Asian communities consuming more vegetables and seafood, while Hispanic populations favor meat-based formulations. The mature retail and wholesale landscape ensures wide availability of packaged seasonings to both industrial processors and foodservice operators. Growing interest in premium and authentic ingredients supports consistent demand for higher-margin products.

Mexico emerges as the fastest-growing market, expanding at a 5.89% CAGR through 2031, fueled by urbanization, rising disposable incomes, and growth in the food manufacturing and processing sectors. Cities such as Monterrey and Guadalajara see rising industrial spice consumption as new production facilities and meat processing plants scale operations. Exposure to international culinary trends through media and tourism boosts demand for both traditional and exotic seasonings. The market also benefits from improving logistics and retail infrastructure, enhancing distribution of packaged spices to industrial buyers. While organic spice adoption is still limited due to cost sensitivity, government incentives for organic cultivation could increase production capacity after 2026. Overall, Mexico’s industrial base positions it as a key growth driver for the region.

Canada posts a steady growth, underpinned by its regulated food manufacturing sector and predictable industrial demand. CFIA standards enforce strict food safety, labeling, and quality benchmarks, enabling premium seasoning positioning and filtering out substandard imports. Immigration-driven population growth lifts per-capita spice usage above the national average, while private-label organic lines continue to expand with higher margins. Beyond Canada, other North American markets exhibit stable growth, with consistent industrial demand from processors and cross-border trade with the United States supporting supply continuity. Import patterns largely mirror United States sourcing, but freight volatility from India and Southeast Asia drives manufacturers to maintain extended safety stocks, impacting working capital.

Competitive Landscape

The North America seasoning and spices market exhibits a moderate level of concentration, with major players like McCormick, Kerry, Döhler, All Seasonings Ingredients, and Olam controlling a significant portion of supply through vertically integrated sourcing and long-term contracts with processors. These companies leverage operational scale, advanced compliance systems, and continuous innovation to maintain strong market positions, creating high barriers for smaller entrants. Mid-tier manufacturers focus on agile production and niche ethnic flavors, catering to specialized food manufacturers and regional processors. This competitive landscape encourages smaller innovators to target overlooked applications, though regulatory and capital demands remain a challenge.

Opportunities in the market are concentrated in health-conscious and specialty segments, including sodium-reduced, plant-based, and allergen-friendly seasoning solutions. Single-origin and certified organic spices, such as Tellicherry pepper or Kashmiri chili, present premium growth potential, though limited supply can constrain rapid scaling. Some firms are experimenting with controlled-environment farming and local herb cultivation to reduce transportation costs, extend shelf life, and enhance freshness, despite the substantial capital investment required. Consumer demand for clean-label and traceable ingredients further drives investment in specialty and sustainably sourced lines.

Technological adoption is increasingly shaping operational efficiency and product quality. Leading firms are deploying AI-driven demand forecasting, automated blending systems, and real-time supply chain monitoring to optimize production and maintain compliance with FDA and CFIA standards. Strategic initiatives include R&D expansion for novel fermentation-based flavor systems, acquisition of encapsulation technologies to extend shelf life, and QR-code traceability to assure authenticity and transparency for food manufacturers. Collaboration with industry associations and sustainability programs also helps companies meet evolving regulatory and environmental expectations.

North America Seasonings And Spices Industry Leaders

-

McCormick & Company Inc.

-

Olam International

-

Kerry Group PLC

-

Döhler Group

-

All Seasonings Ingredients Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Michigan Potash & Salt Co. announced a new food‑grade salt business in Evart, Michigan that will produce up to 1 million tons of high‑quality salt annually to support domestic food processing and food manufacturing needs, strengthening supply chains and reducing reliance on imports.

- June 2024: Fuchs North America launched the limited-edition “Better Baked Goods” seasoning collection, featuring Apple Lemon, Strawberry Basil, and Brown Sugar blends, designed to enhance baked items and inspire trending flavor innovations.

- April 2024: Kerry launched Tastesense Salt, a sodium reduction solution that delivers salty flavor without adding sodium. This innovation targets the global seasoning and spices market, supporting healthier, low-sodium product development.

North America Seasonings And Spices Market Report Scope

Spices are vegetation products that have an aromatic or pungent taste quality and are used for flavoring while cooking. On the other hand, seasoning is a mixture of several flavoring components, such as sugars, salts, spices, and herbs. The North American seasonings and spices market is segmented by product type into salt and salt substitutes, herbs and seasonings, and spices. The herbs and seasonings covered in the report include thyme, basil, oregano, parsley, and other herbs and seasonings. The spices segment includes pepper, cardamom, cinnamon, clove, nutmeg, and turmeric. The market is segmented by application into bakery and confectionery, soup, noodles and pasta, meat and seafood, sauces, salads and dressings, savory snacks, and other applications. By geography, it is segmented into the United States, Canada, Mexico, and the Rest of North America. For each segment, the market sizing and forecasts are done based on value (USD).

By Type

| Salt and Salt Substitutes | |

| Herbs and Seasonings | Thyme |

| Basil | |

| Oregano | |

| Parsley | |

| Mint | |

| Other Herbs and Seasonings | |

| Spices | Pepper |

| Sesame | |

| Cinnamon | |

| Mustard | |

| Onion | |

| Garlic | |

| Paprika | |

| Chili Pepper | |

| Other Spices |

By Category

| Organic |

| Conventional |

By Application

| Bakery and Confectionery |

| Soup, Noodles, and Pasta |

| Meat and Seafood |

| Sauces, Salads, and Dressing |

| Savory Snacks |

| Other Applications |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Type | Salt and Salt Substitutes | |

| Herbs and Seasonings | Thyme | |

| Basil | ||

| Oregano | ||

| Parsley | ||

| Mint | ||

| Other Herbs and Seasonings | ||

| Spices | Pepper | |

| Sesame | ||

| Cinnamon | ||

| Mustard | ||

| Onion | ||

| Garlic | ||

| Paprika | ||

| Chili Pepper | ||

| Other Spices | ||

| By Category | Organic | |

| Conventional | ||

| By Application | Bakery and Confectionery | |

| Soup, Noodles, and Pasta | ||

| Meat and Seafood | ||

| Sauces, Salads, and Dressing | ||

| Savory Snacks | ||

| Other Applications | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

How large will the North America seasonings and spices market be by 2031?

It is projected to reach USD 6.37 billion by 2031 at a 5.18% CAGR between 2026 and 2031.

Which application segment shows the highest growth?

Savory snacks, as brands reformulate coatings with natural turmeric and chili extracts, are advancing at a 6.02% CAGR through 2031.

Which product type leads current sales?

In 2025, spices held a 62.98% market share, led by growing demand for authentic flavors and ready-to-use blends.

Which geography is expanding the fastest?

Mexico is projected to grow steadily at 5.89% a year through 2031.

Page last updated on: