Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

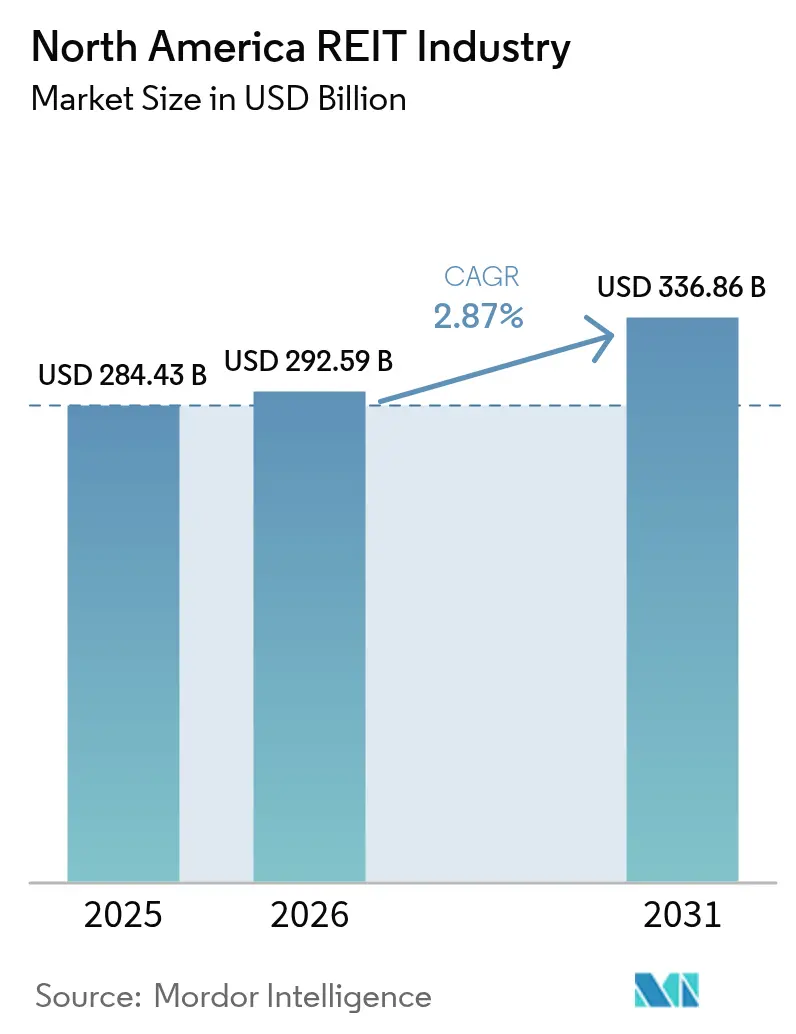

| Base Year Market Size (2025) | USD 284.43 Billion |

| Market Size (2026) | USD 292.59 Billion |

| Market Size (2031) | USD 336.86 Billion |

| Growth Rate (2026 - 2031) | 2.87% CAGR |

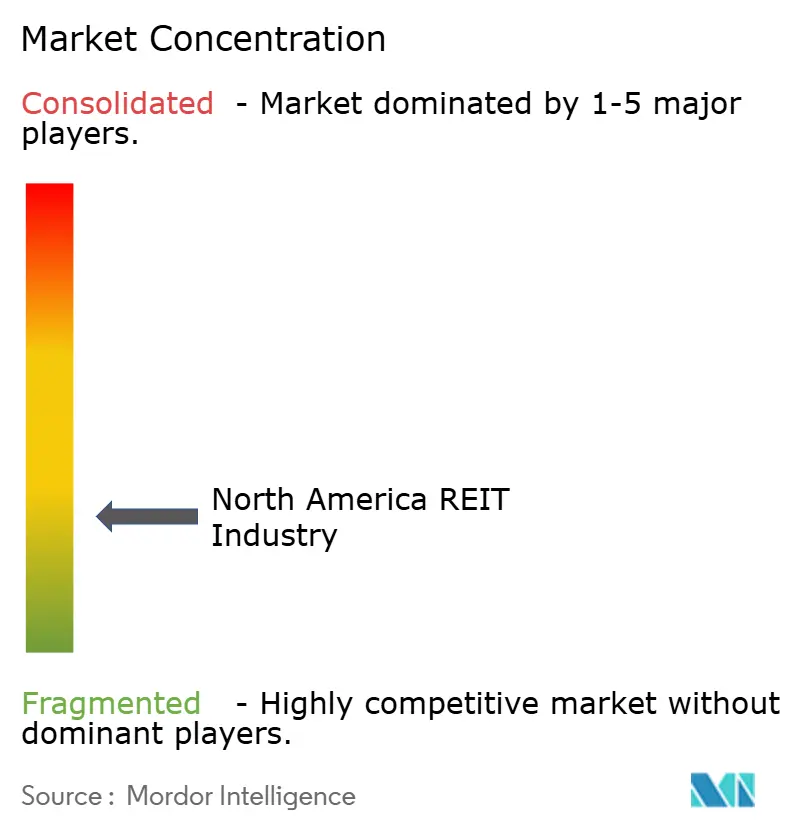

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America REIT Industry Analysis by Mordor Intelligence

The North America REIT Industry market size in 2026 is estimated at USD 292.59 billion, growing from 2025 value of USD 284.43 billion with 2031 projections showing USD 336.86 billion, growing at 2.87% CAGR over 2026-2031.

Sustained growth reflects the sector’s maturity, supportive monetary policy expectations, and a balanced exposure to industrial, residential, and technology-linked real estate. Industrial REITs remain the largest allocation, residential platforms record the fastest expansion, and data-center operators benefit from persistent digital-infrastructure demand. Fundraising pipelines have reopened as investors anticipate lower policy rates, even though refinancing risks tied to commercial mortgage-backed securities (CMBS) remain elevated. Portfolio managers respond by rotating capital away from challenged office assets toward last-mile logistics, single-family rentals, and hyperscale data centers, while hybrid REIT structures gain attention for their flexibility in deploying both equity and debt capital.

Key Report Takeaways

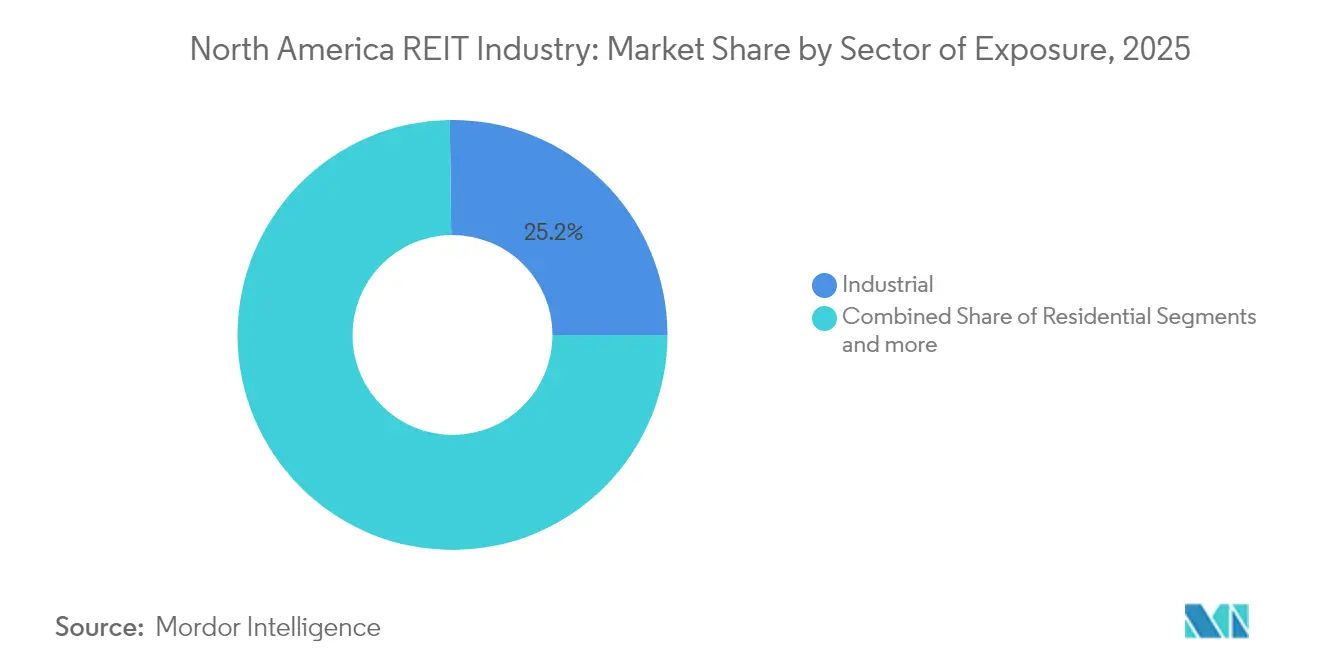

- By sector of exposure, industrial REITs led with 25.20% North America REIT market share in 2025, while residential REITs are forecast to expand at a 5.05% CAGR to 2031.

- By REIT structure, equity vehicles held 86.20% of the total market capitalization of the North America REIT market in 2025; hybrid structures record the highest projected CAGR at 3.62% through 2031.

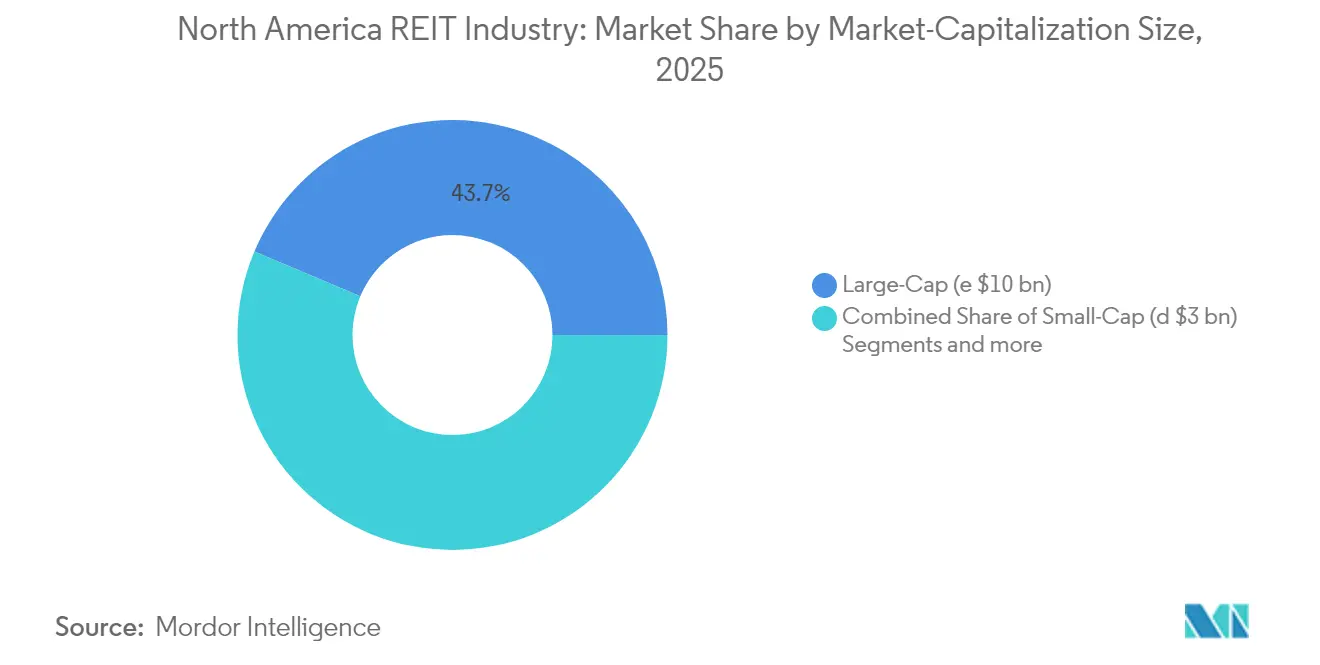

- By market-capitalization size, large-cap platforms accounted for 43.65% of the North America REIT market size in 2025, yet small-cap operators carry a 4.45% CAGR outlook to 2031.

- By country, United States entities controlled 90.15% of the North America REIT market in 2025, whereas Mexico is advancing at a 5.62% CAGR on the strength of nearshoring-driven industrial demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America REIT Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fed rate-cut expectations reinvigorating fundraising pipelines | +0.8% | North America | Short term (≤ 2 years) |

| Demand surge for last-mile logistics assets | +0.6% | US core markets, Canada urban centers | Medium term (2-4 years) |

| AI-led hyperscale data-center absorption | +0.5% | Northern Virginia, Texas, California | Long term (≥ 4 years) |

| Resilient rent growth in single-family rental portfolios | +0.4% | US Sunbelt, select Canadian markets | Medium term (2-4 years) |

| Institutional capital rotation from office to alternative sectors | +0.3% | North America | Medium term (2-4 years) |

| Tokenization of fractional REIT units on blockchain exchanges | +0.2% | Global, early adoption in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fed Rate-Cut Expectations Reinvigorating Fundraising Pipelines

Monetary policy easing forecasts lower borrowing costs, improving net operating income margins for leveraged platforms. Equity issuance volumes rose markedly in late 2024, unlocking capital for development and acquisitions. The USD 150.9 billion CMBS maturity wall scheduled for 2025 poses risk for highly leveraged peers but offers well-capitalized REITs discounted buying opportunities [1]CBRE Investment Management, “North America Real Estate Outlook 2025,” cbre.com. Issuers with strong balance sheets can refinance or opportunistically acquire assets before wider market repricing sets in. The policy backdrop, therefore, acts as both a catalyst and a filter, rewarding disciplined capital allocators.

Demand Surge for Last-Mile Logistics Assets

In 2024, e-commerce was responsible for over half of the growth in US retail sales, driving significant changes in fulfillment strategies. Companies are prioritizing facilities located near densely populated consumer areas, with urban infill warehouses achieving rental rates 15% higher than traditional distribution centers. Despite residual excess capacity from pandemic-era expansions, inventory restocking initiatives and supply-chain resilience programs are fueling additional demand. Prologis research projects a requirement for an extra 250–350 million sq ft of logistics space by 2030 to meet these evolving needs [2]Prologis Research, “E-commerce and Logistics Real Estate,” prologis.com . Real estate investment trusts (REITs) with zoning entitlements in land-constrained metropolitan markets are leveraging their strategic positioning to maintain pricing power. These portfolios are also benefiting from consistently high occupancy rates, reflecting the growing demand for well-located logistics facilities.

AI-Led Hyperscale Data-Center Absorption

The growing demand for high-density server halls, driven by artificial intelligence workloads, is significantly increasing power requirements and placing immense pressure on regional electricity grids. Major data center markets, including Northern Virginia, Dallas, and Silicon Valley, are experiencing extended delays, with multi-year waitlists for utility interconnections becoming a widespread issue. Operators with legacy power contracts and strategically located land are capitalizing on their advantageous positions by pre-leasing capacity at premium rates, thereby strengthening their market standing. Joint-venture investments, such as Equinix’s USD 15 billion hyperscale program, are enabling rapid expansion to address the surging demand for data center infrastructure [3]Equinix, “Equinix and Partners Commit USD 15 Billion to Hyperscale Program,” equinix.com . However, grid constraints are not only creating operational challenges but are also raising substantial barriers to entry for new players. These limitations are further consolidating the competitive advantage of established operators in the market.

Institutional Capital Rotation from Office to Alternative Sectors

In 2024, the national office vacancy rate rose to 1.9%, driving capital allocators to focus on data centers, life-science laboratories, and self-storage facilities. Non-office asset classes now constitute 60% of the total market capitalization of public Real Estate Investment Trusts (REITs) [4]Nareit, “Capital Markets Update 2025,” nareit.org . The valuation disparity between sectors has grown, with alternative-sector REITs trading at or above their net-asset values while office-focused REITs continue to trade at significant discounts. Canadian pension funds, which have historically been among the largest investors in the US real estate market, are shifting their investment strategies. These funds are increasingly prioritizing healthcare and logistics properties over traditional office buildings. This trend underscores a broader reallocation of capital within the real estate market, reflecting changing investor preferences and market dynamics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated refinancing wall amid tapering CMBS appetites | -0.7% | North America | Short term (≤ 2 years) |

| Work-from-home pressure on CBD office occupancy | -0.5% | Major metropolitan areas | Medium term (2-4 years) |

| Legislative scrutiny of housing REIT rent escalations | -0.3% | US federal and state levels | Medium term (2-4 years) |

| Grid-capacity bottlenecks are delaying data-center developments | -0.2% | Northern Virginia, Texas, California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Refinancing Wall Amid Tapering CMBS Appetites

Commercial mortgage-backed securities (CMBS) investors are pushing for wider credit spreads, which is reducing loan proceeds and increasing refinancing costs for maturing loans. Approximately USD 4.70 trillion in commercial real estate debt is expected to require refinancing by 2028, heightening the risk of financial distress for highly leveraged office and retail properties. Real estate investment trusts (REITs) with investment-grade credit ratings and staggered debt maturities are better positioned to manage these challenges. However, REITs that rely heavily on floating-rate debt are likely to face significant financial pressure. These entities may need to resort to issuing dilutive equity or selling assets to meet their obligations. The refinancing wave underscores the growing divide between financially stable REITs and those with weaker balance sheets.

Work-From-Home Pressure on CBD Office Occupancy

Structural vacancies in legacy downtown towers are rising as permanent hybrid work arrangements continue to influence tenant behavior. Businesses are increasingly seeking energy-efficient and amenity-rich spaces, leaving class B and C buildings struggling to remain competitive. This shift is driving shorter lease terms and higher concessions, which are negatively impacting net operating income. Although headline rents are showing signs of stabilization, property owners are still facing financial challenges. The elevated costs of asset repositioning or converting buildings for residential purposes are further delaying recovery efforts. These trends highlight the necessity for strategic investments to align with changing market demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector of Exposure: Industrial Leadership Drives Allocation

Industrial facilities captured 25.20% of the North America REIT market share in 2025. The segment benefits from resilient supply-chain re-engineering, e-commerce fulfilment, and reshoring that lift warehouse absorption in port-proximate and inland hubs. Vacancy rates in tier-one logistics corridors have remained below 4% since 2023, underpinning rent growth outperformance. Capital recycling focuses on acquiring infill last-mile assets even at compressed yields, reflecting confidence in long-term demand durability. Data-center, healthcare, and self-storage niches continue to draw incremental capital, yet industrial remains the anchor allocation for diversified portfolios.

Residential REITs post the fastest expansion at a 5.05% CAGR through 2031, propelled by affordability constraints, rising household formation in the Sunbelt, and demographic aging bolstering senior housing. The North America REIT market size for residential platforms is projected to advance faster than any other property type as build-to-rent pipelines grow. Occupancy above 95% and steady same-property rent gains support dividend visibility. Legislative oversight poses a medium-term risk, though diversified rent affordability programs help sustain community engagement. Retail and office allocations remain under strategic review, with necessity-based retail holding steady while discretionary apparel centers lag footfall recovery.

By REIT Structure: Equity Dominance with Hybrid Innovation

Equity vehicles controlled 86.20% of capitalization in 2025, offering investors transparent ownership of physical assets and inflation-hedged cash flows. Tax-advantaged status underpins stable dividend policies, attracting long-only funds seeking yield replacement relative to fixed income. The North American REIT market continues to favor equity formats for their alignment with direct real-estate fundamentals. Hybrid REITs, blending property ownership with structured lending, post a 3.62% CAGR as sponsors monetize underwriting expertise during credit cycles. Mortgage-only REITs remain a minority, navigating spread volatility and stricter risk-retention standards.

Hybrid strategies enable businesses to diversify revenue streams, mitigate earnings volatility, and enhance flexibility in capital allocation. Prominent examples include platforms integrating data-center development with preferred-equity investments or combining net-lease acquisition pipelines with mezzanine loan support. These approaches are helping to bridge historical valuation gaps between hybrid strategies and traditional equity investments as investor awareness improves. The narrowing of these valuation discounts reflects a growing understanding of the benefits offered by hybrid models. However, achieving broader inclusion in major indices requires companies to maintain high standards of governance transparency. Additionally, a well-structured and clear balance sheet remains a critical prerequisite for such inclusion.

By Market-Capitalization Size: Large-Cap Stability versus Small-Cap Upside

In 2025, large-cap entities represented 43.65% of market capitalization, leveraging their liquidity advantages and extensive index inclusion. Their operational scale enables cost efficiencies in procurement, access to favorable debt terms, and geographic diversification, which collectively support stable dividend distributions. These entities dominate the North American REIT market, offering defensive investment characteristics that appeal to institutional investors such as pension funds and sovereign wealth funds. Their ability to maintain consistent performance underpins their attractiveness to risk-averse investors seeking reliable returns. Mid-cap REITs, in contrast, provide a blend of growth potential and yield, often focusing on specialized segments like medical office spaces or manufactured housing. This strategic focus allows mid-caps to cater to niche demands while balancing risk and return for investors.

Small-cap REITs are forecasted to grow at a 4.45% CAGR through 2031, driven by specialist managers who reposition underperforming assets and explore untapped geographic markets. These entities often trade at valuation discounts relative to their net-asset value, primarily due to limited analyst coverage, which creates opportunities for potential re-rating. Their smaller scale and focused strategies make them attractive targets for acquisition by larger peers, highlighting ongoing consolidation trends in the market. This dynamic provides small-cap REITs with an additional pathway for value realization, enhancing their appeal to investors. The segmentation of REITs by size offers a diverse range of risk-return profiles, enabling investors to align their portfolios with specific strategic objectives. Overall, the size-based segmentation reflects the varying growth trajectories and investment opportunities across the REIT market.

Geography Analysis

The United States anchors the North American REIT market with a 90.15% share and a 2.85% CAGR outlook through 2031. Regulatory clarity, broad tenant demand, and robust public equity liquidity continue to attract domestic and offshore investors. Industrial hubs in Dallas-Fort Worth, Los Angeles, and Atlanta enjoy low vacancies, while Sunbelt multifamily assets benefit from in-migration. Federal tax rules and well-established REIT governance codes further reinforce the country’s dominance. Yet the USD 150.9 billion CMBS maturity cliff in 2025 signals heightened refinancing vigilance across all property types.

Mexico records the fastest 5.62% CAGR thanks to supply-chain realignment that channels manufacturing toward cost-effective, US-proximate industrial parks. FIBRA vehicles have capitalized on this trend by expanding portfolios near Monterrey and Tijuana and by pre-leasing space to automotive and electronics tenants. Peso strength relative to the US dollar enhances effective rental growth when translated for foreign investors. Government infrastructure spending on highways and ports supports ongoing expansion. Currency volatility and distinct regulatory frameworks nonetheless require specialized asset-management capabilities.

Canada offers diversification through exposure to Toronto and Vancouver multifamily, Calgary energy-linked offices, and Montréal tech-enabled industrial parks. Currency movements historically act as a hedge against US dollar shifts, stabilizing total returns. Development is constrained by limited zoned land and lengthy entitlement processes, supporting rent growth even in slower GDP cycles. Foreign-buyer taxes and transaction-cost frictions persist but have not deterred pension funds from maintaining significant domestic allocations. The combined regional profile allows portfolio managers to blend high-growth Mexican assets with stable US and Canadian cash-flow streams within the North America REIT market.

Competitive Landscape

The North America REIT market remains moderately fragmented, with the five largest platforms controlling one-third of capitalization. Diversification by property type and geography lowers direct rivalry, yet competition intensifies within high-growth niches such as data centers and single-family rentals. Operators with investment-grade balance sheets can access unsecured debt at significantly tighter spreads compared to their high-yield counterparts, providing them with a competitive edge in acquisitions during periods of credit stress. Technology deployment in leasing analytics, energy management, and tenant engagement differentiates performance, particularly where AI-based tools optimize portfolio decisions.

Strategic transactions highlight scale benefits. Healthpeak Properties merged with Physicians Realty Trust to create a medical-office leader, while Blackstone’s acquisition of Retail Opportunity Investments Corp shows private-equity support for well-located necessity retail. Realty Income’s creation of a private core-plus fund expands fee revenue and deepens institutional relationships. Capital-raising innovations include green bonds tied to LEED-certified developments and pilot blockchain tokenizations that broaden investor reach. Competitive positioning, therefore, hinges on capital access, technology adoption, and disciplined portfolio rotation within the evolving North America REIT market.

North America REIT Market Leaders

Prologis Inc.

American Tower Corporation

Equinix Inc.

Crown Castle Inc.

Simon Property Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cottonwood Communities finalized its merger with RealSource Properties, adding scale to its single-family rental portfolio across key Sunbelt markets.

- June 2025: Macerich purchased Crabtree Valley Mall in Raleigh, North Carolina, for USD 290 million, strengthening its footprint in high-growth Southeastern metros.

- April 2025: Realty Income introduced a private core-plus real-estate fund, giving institutional investors direct access to its net-lease acquisition pipeline and adding a new fee-based revenue stream for shareholders.

- January 2025: Kimco Realty expanded its Florida presence through the acquisition of multiple grocery-anchored neighborhood centers, capitalizing on population inflows to the state.

North America REIT Industry Report Scope

An understanding of the North America REIT industry, regulatory environment, REITs and their business models, along with detailed market segmentation, product types, revenues and dividends, current market trends, changes in market dynamics, and growth opportunities. In-depth analysis of the market size and forecast for the various segments.

By Sector of Exposure

| Retail |

| Industrial |

| Office |

| Residential |

| Diversified |

| Other Sectors |

By REIT Structure

| Equity REITs |

| Mortgage REITs |

| Hybrid REITs |

By Market-Capitalization Size

| Large-Cap (≥ US $10 bn) |

| Mid-Cap (US $3–10 bn) |

| Small-Cap (≤ US $3 bn) |

By Country

| United States |

| Canada |

| Mexico |

| By Sector of Exposure | Retail |

| Industrial | |

| Office | |

| Residential | |

| Diversified | |

| Other Sectors | |

| By REIT Structure | Equity REITs |

| Mortgage REITs | |

| Hybrid REITs | |

| By Market-Capitalization Size | Large-Cap (≥ US $10 bn) |

| Mid-Cap (US $3–10 bn) | |

| Small-Cap (≤ US $3 bn) | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current size of the North America REIT market?

The market is valued at USD 292.59 billion in 2026 and is forecast to reach USD 336.86 billion by 2031.

Which sector holds the largest share in the North America REIT market?

Industrial assets lead with 25.20% market share in 2025, reflecting strong e-commerce and supply-chain demand.

Which segment is growing fastest within the North America REIT market?

Residential REITs post the fastest 5.05% CAGR outlook, driven by housing affordability challenges and build-to-rent development.

How does monetary policy influence the North American REIT market growth?

Anticipated Federal Reserve rate cuts reduce borrowing costs, revive equity issuance, and support acquisition pipelines, adding an estimated 0.8% to forecast CAGR.

Why are data-center REITs attracting investor interest?

AI-related workloads are doubling energy demand, and operators with secured power contracts can pre-lease space at premium rates, creating strong cash-flow visibility.

Which geography outside the United States shows the strongest REIT growth?

Mexico advances at a 5.62% CAGR through 2031 as nearshoring drives industrial leasing along key manufacturing corridors.

Page last updated on: