North America Professional Employer Organization (PEO) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

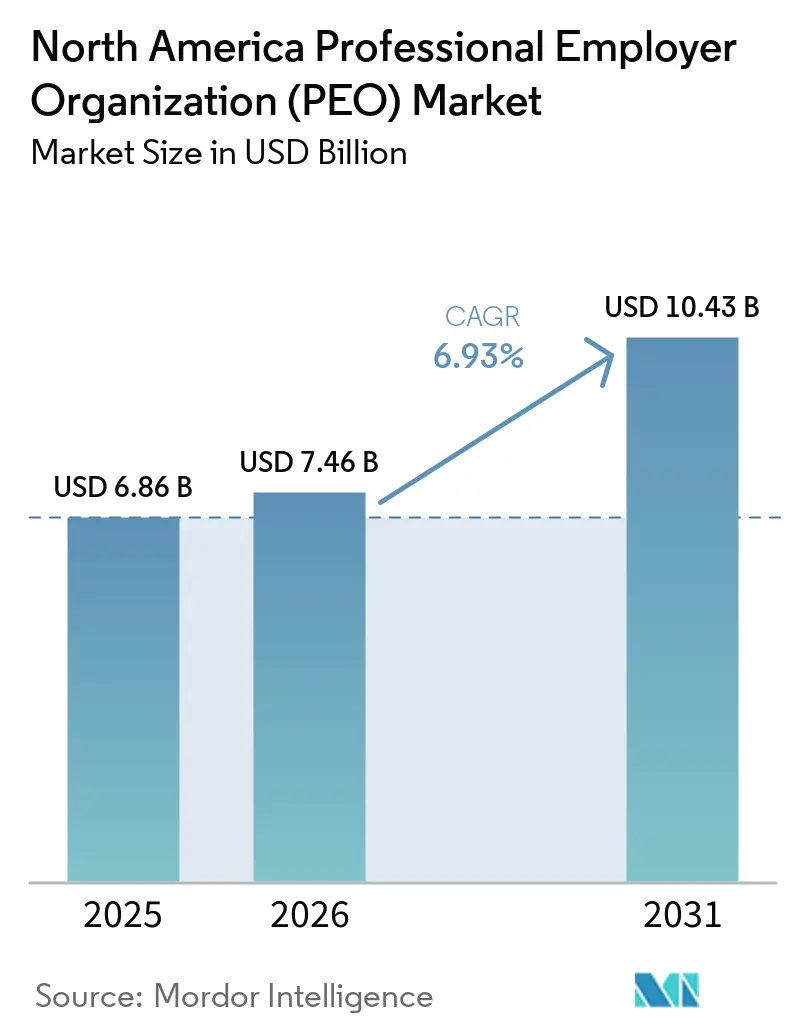

| Base Year Market Size (2025) | USD 6.86 Billion |

| Market Size (2026) | USD 7.46 Billion |

| Market Size (2031) | USD 10.43 Billion |

| Growth Rate (2026 - 2031) | 6.93% CAGR |

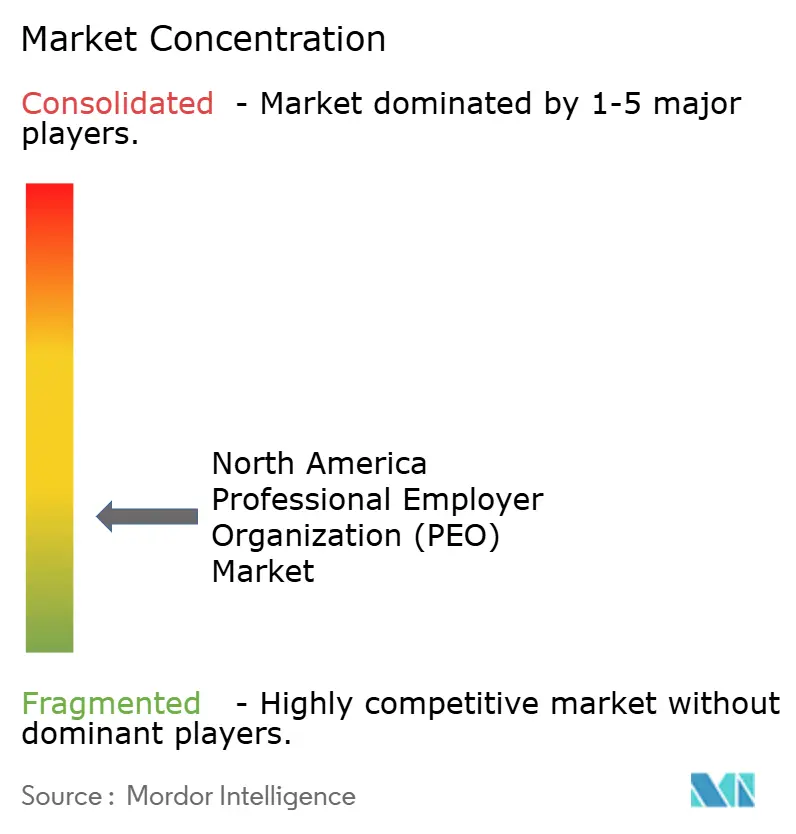

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Professional Employer Organization (PEO) Market Analysis by Mordor Intelligence

The North America professional employer organization (PEO) market size reached USD 6.86 billion in 2025 and is projected to reach USD 10.43 billion by 2031, growing at a CAGR of 6.93% from 2026 to 2031. The North America professional employer organization (PEO) market is expanding as co-employment partnerships are becoming a structural workforce management choice for businesses that cannot absorb payroll complexity, benefits procurement costs, and labor law obligations through internal teams alone. More than 230,000 US businesses already partner with a PEO, including close to 15% of employers with 10 to 499 employees, indicating that adoption has moved well beyond a niche outsourcing decision. Employers are no longer using the North America professional employer organization (PEO) market only for administrative relief, because they are also seeking pooled benefit pricing, litigation risk support, and continuity in compliance execution that are difficult to replicate independently. The North America professional employer organization (PEO) market is also benefiting from a broader shift in how workforce costs are viewed, with payroll, benefits, and compliance now treated as variable, risk-heavy obligations that can be managed through co-employment rather than as fixed internal overhead. Competitive intensity is rising as national platforms, regional consolidators, and technology-led entrants all try to strengthen service breadth, platform integration, and pricing clarity across the North America professional employer organization (PEO) market.

Key Report Takeaways

- By service type, core services accounted for 27.63% of the North America professional employer organization (PEO) market in 2025, while value-added services are projected to expand at a 11.94% CAGR through 2031.

- By business size, SMBs accounted for 58.21% of the market in 2025, while the large business segment is projected to grow at a 9.87% CAGR through 2031.

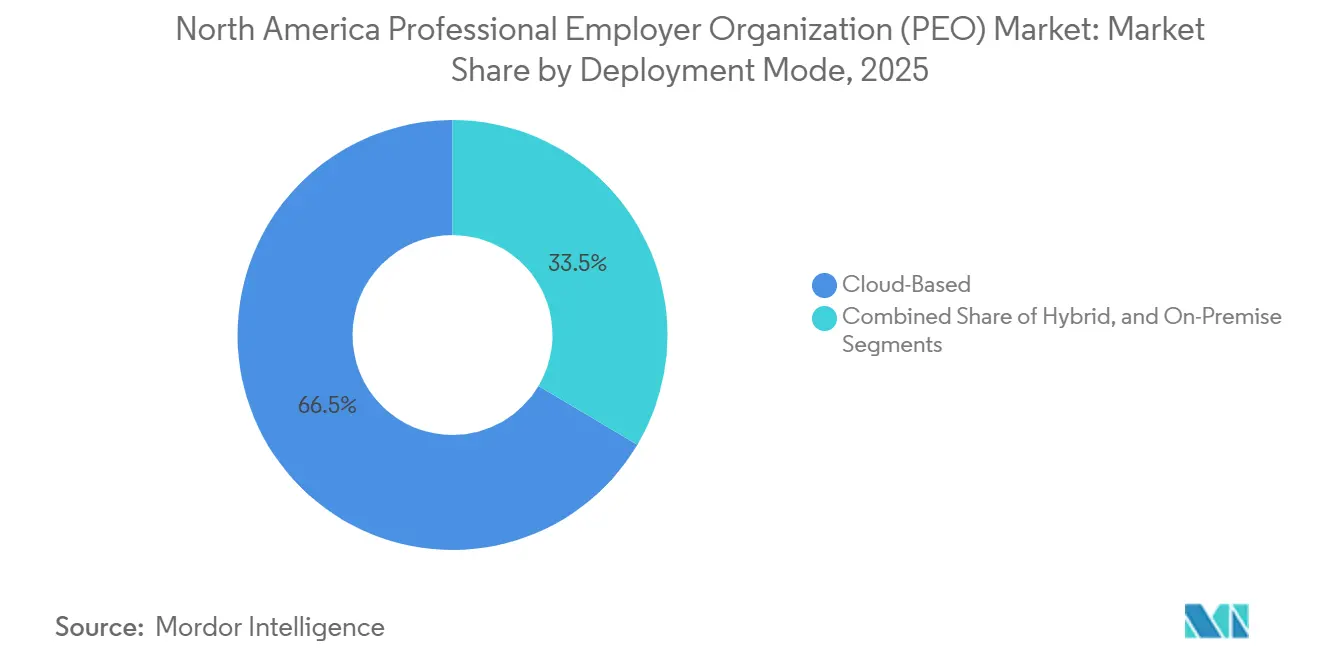

- By deployment mode, cloud-based deployment led with a 66.48% share in 2025, while hybrid deployment is projected to expand at a 10.92% CAGR through 2031.

- By industry vertical, IT and Telecom captured 25.39% share in 2025, while healthcare and life sciences is projected to grow at a 12.00% CAGR through 2031.

- By geography, the United States held 74.11% share of the North America professional employer organization (PEO) market in 2025, while Canada is projected to expand at an 8.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Professional Employer Organization (PEO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing SME Demand For Outsourced Payroll And HR Administration | +2.0% | Global, with concentration in US, especially Florida, California, New York, and Texas | Short term (≤ 2 years) |

| Rising Labor And Tax Compliance Complexity Across North America | +1.7% | North America, concentrated in multi-state US employers and Canadian provincial jurisdictions | Short term (≤ 2 years) |

| Need For Enterprise-Grade Benefits And Retention Support | +1.3% | Global, concentrated in US mid-market | Medium term (2-4 years) |

| Accelerating Adoption Of Cloud-Based HR And Payroll Platforms | +1.0% | Global, with spillover across multinational client workforces | Medium term (2-4 years) |

| Expansion Of State Paid Leave And Pay Data Reporting Requirements | +0.7% | United States, especially multi-state employers in California, Colorado, Connecticut, Delaware, Maine, Maryland, Massachusetts, Minnesota, New Jersey, New York, Oregon, Rhode Island, Washington, and the District of Columbia | Medium term (2-4 years) |

| Heightened I-9, E-Verify, And Immigration Audit Readiness Needs | +0.4% | United States, with early gains in border-adjacent states and dense immigrant labor markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing SME Demand For Outsourced Payroll And HR Administration

Small and medium businesses are treating PEO partnerships as operating needs rather than optional back-office purchases, which is keeping demand broad across the North America professional employer organization (PEO) market. Reported in February 2026, 61% of SMBs outsourced health insurance, 56% outsourced payroll, and 50% outsourced retirement benefits administration, while time savings and stronger focus on core operations ranked ahead of cost reduction in buyer priorities.[1]National Association of Professional Employer Organizations, “New NAPEO Research Highlights Growth and Diversity of PEO Clients,” National Association of Professional Employer Organizations, napeo.org In October 2025, businesses with 50 to 99 employees reached a 15% penetration rate, the highest among the business-size groups covered in the research. The same February 2026 survey found that PEO users reported an 80% business growth rate in 2025 versus 67% for non-users, which helps explain why growth support is now more central to sales conversations than simple administrative savings. Future demand also remains strong, as 87% of non-PEO users said they were interested in using a PEO, indicating that familiarity with the model is increasing and acquisition friction is easing across the North America professional employer organization (PEO) market.

Rising Labor And Tax Compliance Complexity Across North America

Rising labor and tax compliance complexity is making external HR administration more practical for employers operating across multiple jurisdictions, which is supporting the North America professional employer organization (PEO) market. Confirmed that 13 states and the District of Columbia have enacted paid family and medical leave programs, while Delaware's program entered full effect in January 2026 and added another live compliance layer for employers in that state.[2]National Conference of State Legislatures, “State Family and Medical Leave Laws,” National Conference of State Legislatures, ncsl.org California added more pressure through pay data reporting requirements: the California Civil Rights Department set a May 13, 2026, filing deadline for 2025 reports, and Senate Bill 464 strengthened enforcement authority while expanding job-category reporting from 2027 onward. Federal employment obligations also continue to raise the value of structured support, especially where wage-and-hour rules, benefit plan requirements, and the IRS Certified PEO framework all require consistent execution. Employers that expand across US states or Canadian provinces face reporting calendars, tax rules, and leave rules that are difficult to manage without dedicated specialists, which is keeping compliance-led demand durable in the North America professional employer organization (PEO) market.

Need For Enterprise-Grade Benefits And Retention Support

Healthcare cost pressure is widening the gap between what smaller firms can buy on their own and what they can access inside a pooled plan, which is supporting the North America professional employer organization (PEO) market. Milliman estimated in its 2026 Medical Index that employer-sponsored healthcare costs are rising 7.9% in 2026 from 2025, with pharmacy and outpatient facility spending accounting for 69% of the increase. That trend makes pooled master plans more valuable because employers outside a broad benefits pool have limited ability to absorb claims volatility or smooth renewal pressure across a large enrolled base. Reported in February 2026, 67% of SMBs cited hiring difficulties, and 62% cited retention as a major challenge, tying benefit quality directly to workforce stability. The sales case in the North America professional employer organization (PEO) market is therefore moving beyond payroll administration and toward helping employers compete for talent through stronger health coverage, retirement support, and employee experience. This supports demand from firms that may not be large enough to negotiate enterprise-grade benefit structures on their own but still need to compete for skilled labor in tight hiring conditions.

Accelerating Adoption Of Cloud-Based HR And Payroll Platforms

Technology is changing how providers deliver services, improving the competitiveness of the North America professional employer organization (PEO) market against standalone payroll and HR software vendors. Cloud-based deployment already accounted for 66.48% of the market in 2025, indicating that buyers increasingly want payroll, benefits administration, and compliance workflows delivered through scalable digital systems rather than fragmented manual processes. The same shift is visible in vendor strategy, with Vensure launching an AI-powered HR Compliance platform in October 2025 through PrismHR to provide real-time guidance on multi-state labor law changes and a private-label option for service bureau partners. Insperity and Workday announced the general availability of Insperity HRScale in February 2026, combining co-employment delivery with Workday HCM, US payroll, absence management, and time tracking in a pre-configured offering. These moves show that the North America professional employer organization (PEO) market is increasingly being shaped by integration depth, workflow automation, and implementation speed rather than by benefits pricing alone. They also raise switching costs because clients that rely on linked payroll, compliance, benefits, and analytics tools are less likely to separate those functions once they are operating on one platform.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Perceived Loss Of Employer Control Under Co-Employment | -1.4% | Global, strongest in US mid-market and Canada | Short term (≤ 2 years) |

| Price Sensitivity And Low Awareness Among Smaller Buyers | -1.0% | Global, concentrated in US micro-businesses with fewer than 10 employees | Short term (≤ 2 years) |

| Rising Benefit Cost Inflation And PBM Transparency Pressures | -0.8% | North America, with early concentrated impact in high-claims states | Medium term (2-4 years) |

| Contract Exit Friction And CPEO Status Confusion | -0.5% | United States, with early concentrated impact in high-penetration states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Perceived Loss Of Employer Control Under Co-Employment

Co-employment still creates hesitation for some buyers, and this remains a recurring barrier in the North America professional employer organization (PEO) market. Owner-led and mid-market businesses often confuse co-employment with employee leasing, even though the client keeps day-to-day operational control while the provider handles payroll, benefits, and administrative employer functions. That misunderstanding raises concerns around hiring authority, termination decisions, workplace culture, and institutional knowledge, especially where senior management remains directly involved in HR matters. Research has shown that PEO clients are materially less likely to go out of business than comparable non-PEO firms, but that performance advantage does not always remove early objections tied to role clarity.[3]National Association of Professional Employer Organizations, “New NAPEO Survey Shows Small and Mid-Sized Businesses Remain Optimistic but Increasingly Focused on Economic Uncertainty and Cost Pressures,” National Association of Professional Employer Organizations, napeo.org The IRS CPEO framework helps define standards and responsibilities, yet many buyers still need a detailed explanation before they are comfortable with the model. Providers that do not address this clearly at the start often face longer sales cycles and weaker retention in the early stages of engagement.[4]Internal Revenue Service, “About the Voluntary Certification Program for Professional Employer Organizations (CPEOs),” Internal Revenue Service, irs.gov

Price Sensitivity And Low Awareness Among Smaller Buyers

Micro-businesses remain a difficult segment for the North America professional employer organization (PEO) market because cost sensitivity is high and understanding of the model is often limited. Tracking data from 2025 showed that cost remained one of the top factors considered by SMBs evaluating a PEO relationship, even though expertise and time savings carried more weight in final decision-making. Bundled pricing can appear opaque to firms with fewer than 10 employees because they often lack clear benchmarks for comparing payroll, HR, benefits, and compliance support within one offer. Education costs are also higher in this segment because providers must explain the co-employment structure, certification status, benefits differences, and pricing logic before the buyer can judge value. This is one reason tech-native firms are leaning toward per-employee-per-month pricing structures that reduce friction for smaller employers, even though that approach can limit some cross-sell depth later in the relationship. Until awareness improves, the lower end of the North America professional employer organization (PEO) market will remain harder to penetrate than the core SMB segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Are Expanding The Service Mix

Core services accounted for 27.63% of the North America professional employer organization (PEO) market in 2025, making them the foundation of most provider-client relationships. Payroll and tax administration remained the operational anchor because employers still need help with multi-state withholding, direct deposit, quarterly employer tax filings, and year-end reporting. Research in October 2025 showed that member PEOs served more than 4.5 million worksite employees, which helps explain why payroll processing scale remains central to the category. Benefits administration followed closely because pooled plans give smaller employers access to coverage structures that independent procurement often cannot match. Risk, safety, and workers' compensation management also stayed important, especially in industries where claims experience and injury exposure directly affect cost.

Value-added services are projected to grow at an 11.94% CAGR from 2026 to 2031, making them the fastest-expanding service category in the North America professional employer organization (PEO) market. Clients are increasingly asking providers to deliver talent acquisition support, learning platforms, and HR technology tools in addition to payroll and compliance administration. A Q2 2025 Pulse Survey found that 93% of PEOs expected growth in worksite employee count over the next 12 months, which supports the view that client relationships are widening rather than narrowing. VensureHR's launch of Pathway to Care and Wellness in May 2026 is a good example of this shift because it added guided healthcare navigation and benefit support to the broader client relationship. As providers add more tools and employee support layers, switching costs rise, and the revenue opportunity per client deepens across the North America professional employer organization (PEO) market.

By Business Size: SMBs Hold The Base While Large Employers Gain Momentum

SMBs accounted for 58.21% of the North America professional employer organization (PEO) market share in 2025, confirming that smaller employers remain the core customer base. Reported in October 2025, PEO penetration reached 14% among employers with 20 to 499 employees, while the 50 to 99 employee cohort reached 15%, the highest level across the business-size groups covered in its study. This concentration reflects a cost crossover because many firms in this range have already outgrown informal HR management but still lack the scale to justify fully built internal payroll, benefits, and compliance teams. The segment also benefits from pooled purchasing power because a smaller employer can gain access to stronger benefit structures through a PEO than through stand-alone procurement. That combination keeps SMB demand stable and makes this group the operating core of the North America professional employer organization (PEO) market.

The large business segment is projected to grow at a 9.87% CAGR through 2031, which shows that adoption is moving beyond the traditional SMB-only view of the North America professional employer organization (PEO) market. Larger employers are increasingly using the model for specific entities, expansion markets, and business units where compliance complexity is high or where internal systems are not fully standardized. This is especially relevant when companies expand across multiple US states, acquire regional subsidiaries, or enter Canada and Mexico through new legal entities. Insperity HRScale, which became generally available in February 2026, reflects this shift by combining enterprise HCM capabilities with a co-employment delivery structure. The result is a broader addressable base for providers that can serve both high-growth SMBs and more complex employer structures without relying on a single client profile.

By Deployment Mode: Cloud Leads While Hybrid Supports Transition

Cloud-based deployment accounted for 66.48% of the North America professional employer organization (PEO) market in 2025, making it the leading delivery model across payroll, HR administration, and benefits workflows. The preference for cloud systems reflects buyer demand for easier updates, faster onboarding, real-time reporting, and lower dependence on manual intervention. In practical terms, cloud delivery allows providers to process payroll, manage tax filings, update compliance workflows, and support employee self-service across large client bases with greater consistency. That operating model also improves scalability because the provider can add clients without increasing internal headcount at the same rate. For the North America professional employer organization (PEO) market, this creates a direct advantage over fragmented in-house systems and older service structures that depend heavily on manual administration.

Hybrid deployment is projected to expand at a 10.92% CAGR from 2026 to 2031, which makes it the fastest-growing deployment category. Growth is being driven by employers with existing HRIS investments or regulatory requirements that make a full, immediate migration less practical. Large employers, healthcare systems, financial firms, and government-linked organizations often need a phased path that connects cloud applications with legacy infrastructure rather than replacing everything at once. This gives providers a medium-term opportunity to support clients during the migration stage and to deepen platform integration before a full cloud transition is completed. On-premise deployment continues to lose relevance in new engagements, yet it remains present where dedicated infrastructure or specialized controls are still required. That pattern keeps the North America professional employer organization (PEO) market tied to a technology mix in which implementation flexibility matters almost as much as the destination platform itself.

By Industry Vertical: Technology Leads While Healthcare And Life Sciences Accelerate

IT and Telecom accounted for 25.39% of the North America professional employer organization (PEO) market in 2025, making it the largest industry vertical. The segment aligns well with the co-employment model because many technology firms operate across state lines, hire distributed workforces, and rely on competitive benefits to attract skilled employees. Research in October 2025 showed that professional, scientific, and technical services ranked among the largest concentrations of US PEO clients, which supports the strength of this vertical in the regional mix. Employers in this vertical also face strong compliance pressure in states such as California and New York, where reporting and wage rules are more complex. These conditions make the North America professional employer organization (PEO) market especially relevant for firms that need both flexible workforce support and tighter compliance execution.

Healthcare and life sciences are projected to grow at a 12.00% CAGR from 2026 to 2031, making it the fastest-growing vertical in the North America professional employer organization (PEO) market. Research in October 2025 also placed healthcare and social assistance among the four industries with the highest PEO client concentration nationally. This segment combines intense regulation with uneven internal HR capacity, especially among clinical-stage biopharma firms, diagnostic laboratories, and outpatient care networks. Employers in these settings need help with credentialing, training, recordkeeping, and broader compliance workflows that general HR software often cannot support without significant customization. That raises switching costs and makes specialized PEO delivery more valuable over time, which is why healthcare and life sciences are emerging as both a growth segment and a capability test for providers across the North America professional employer organization (PEO) market.

Geography Analysis

The United States accounted for 74.11% of the North America professional employer organization (PEO) market share in 2025, maintaining its dominance as the leading regional demand geography. Reported in October 2025, Florida, California, New York, and Texas represented the largest concentrations of PEO clients nationally, and Florida alone accounted for 18% of all PEO clients. This concentration reflects both dense SMB activity and a high regulatory burden across labor, payroll, and reporting requirements. California continues to stand out because its pay data reporting requirements are becoming more stringent, with Senate Bill 464 signed in October 2025 and the California Civil Rights Department setting a May 13, 2026, deadline for 2025 reports. PEO penetration among US employers with 10 to 499 employees was close to 15% in 2025, suggesting the addressable base for the North America professional employer organization (PEO) market still has room for organic growth without requiring major displacement of incumbents.

Canada is the fastest-growing geography in the North America professional employer organization (PEO) market, with an 8.96% CAGR projected through 2031. The core driver is jurisdictional fragmentation, as employers operating across provinces must manage CPP contributions, Employment Insurance premiums, provincial income tax tables, employer health taxes, and separate employment standards frameworks simultaneously. Ontario, British Columbia, and Quebec each impose different compliance requirements, which increases administrative strain on employers trying to maintain a consistent payroll and HR structure across the country. US-based firms entering Canada often underestimate this complexity at the start, which increases demand for external support during cross-border expansion.

Mexico remains a smaller part of the North America professional employer organization (PEO) market, but it carries strategic importance because nearshoring is driving new workforce administration needs. Manufacturing and technology activity in hubs such as Monterrey and Guadalajara is encouraging US employers to build or duplicate operations there, which increases demand for localized payroll and compliance support. Mexico's regulatory structure does not mirror the traditional US co-employment model, so providers often work through employer-of-record or adjacent service structures that still address payroll, labor administration, and local compliance needs. This means demand is being adjusted to local rules rather than reduced, which gives Mexico a meaningful role in the later stages of regional growth.

Competitive Landscape

The North America professional employer organization (PEO) market remained fragmented in 2026, with more than 500 PEOs operating in the United States alone, even as consolidation accelerated across the mid-tier. Vensure Employer Solutions said in April 2026 that it had completed its 108th acquisition overall and added more than 80,000 worksite employees across 8 deals closed through 2026. That pace shows how acquisitive platforms are using regional deals to buy broker relationships, state-level compliance depth, and operating scale that would take years to build internally. It also shows that the North America professional employer organization (PEO) market remains sufficiently fragmented to support roll-up strategies. The part of the market that remains especially open is the tech-native SMB segment, where smaller employers want transparent pricing, mobile-first onboarding, and direct software integration rather than broker-led sales structures.

Competitive differentiation is increasingly tied to platform capability and workflow depth rather than to benefits pricing alone in the North America professional employer organization (PEO) market. TriNet completed its acquisition of Cocoon in April 2026, adding leave management technology with compliance-first AI workflows, real-time leave tracking, and integrated payroll calculations for SMBs. Insperity HRScale, made generally available in February 2026, demonstrated that enterprise HCM capability can now be delivered within a co-employment model rather than positioned as an alternative to it. CoAdvantage's 2025 merger with PrimePay followed a similar path, combining full-service PEO delivery with payroll and HCM software built for SMBs and franchises.

The competitive field also remains tiered by client type, delivery style, and certification depth across the North America professional employer organization (PEO) market. Large national providers such as Insperity and TriNet compete on brand, integration, and broad benefits scale, while mid-sized regional groups often rely more heavily on local relationships, sector expertise, and acquisition-led growth. Tech-native entrants continue to appeal to smaller employers by reducing pricing friction and simplifying implementation, which gives them room to win accounts that are less responsive to traditional percentage-of-payroll models. Formal credentials are becoming increasingly important as well, because the IRS CPEO framework provides larger, more regulated buyers with a clearer basis for assessing provider quality and role definition. This keeps the market fragmented, but it also creates a clearer separation between scaled, certified operators and smaller firms that compete mainly on local familiarity or narrower service scope.

North America Professional Employer Organization (PEO) Industry Leaders

Vensure Employer Solutions

TriNet Group, Inc.

Insperity, Inc.

CoAdvantage, Inc.

FrankCrum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: VensureHR launched Pathway to Care and Wellness, a guided healthcare navigation program for worksite employees on its master health benefits plan, designed to reduce out-of-pocket expenses through proactive care guidance and Medicare transition support. The program received a Gold Stevie Award for Achievement in Employee Wellbeing Programs, reinforcing VensureHR's strategy of competing on benefits quality alongside its compliance and scale positioning.

- April 2026: Vensure Employer Solutions completed its 108th acquisition overall, closing 8 deals within 2026 to date and adding over 80,000 worksite employees across PEO, payroll, HCM, and staffing-related services. The transactions followed the company's USD 450 million senior secured financing, establishing further M&A capacity as Vensure continued to consolidate mid-tier regional PEOs across the United States.

- April 2026: TriNet completed its acquisition of Cocoon, a market leader in leave management technology specializing in compliance-first AI workflows, real-time leave tracking, and integrated payroll calculations for SMBs. The deal, announced April 9, 2026 and closed April 14, 2026, extends TriNet's leave-of-absence offering with automated compliance tools at a time when multi-state paid leave complexity is intensifying across 13 states plus the District of Columbia.

- March 2026: Allvia, a workforce services platform backed by Trinity Hunt Partners, acquired HR Pals, a provider of outsourced HR administration and employee support services for employers of all sizes. The acquisition built on Allvia's founding partnership with Melita Group and advanced its strategy to develop a scaled HR administration and workforce strategy platform spanning the United States.

North America Professional Employer Organization (PEO) Market Report Scope

The North America Professional Employer Organization (PEO) market refers to service providers and platforms that partner with businesses to manage comprehensive HR functions, including payroll, benefits, compliance, risk management, and workforce administration, while also offering value-added services such as recruitment support, employee learning, and HR technology solutions. Delivered through cloud-based, hybrid, and on-premise models, PEOs cater to both large enterprises and small and medium businesses across industries such as IT and telecom, BFSI, healthcare, manufacturing, retail, government, and others. The core purpose of this market is to enable businesses in the United States, Canada, and Mexico to focus on strategic growth by outsourcing complex HR operations, ensuring compliance, reducing costs, and enhancing employee satisfaction through integrated, technology-enabled HR services.

The North America Professional Employer Organization (PEO) market report is segmented by Service Type (Core Services, [Payroll and Tax Administration, Benefits Administration, HR Operations and Workforce Administration, Regulatory Compliance Management, and Risk, Safety and Workers’ Compensation Management] and Value-added Services [Talent Acquisition and Recruitment Support, Learning and Employee Development, and HR Technology Platforms]), Business Size (Large Business, and Small and Medium Business), Deployment Mode (Cloud-Based, Hybrid, and On-Premise), Industry Vertical (Information Technology and Telecom, Banking, Financial Services and Insurance (BFSI), Healthcare and Life Sciences, Industrial Manufacturing, Retail and E-commerce, and Government and Public Sector), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Core Services | Payroll and Tax Administration |

| Benefits Administration | |

| HR Operations and Workforce Administration | |

| Regulatory Compliance Management | |

| Risk, Safety and Workers Compensation Management | |

| Value-added Services | Talent Acquisition and Recruitment Support |

| Learning and Employee Development | |

| HR Technology Platforms |

| Large Business |

| Small and Medium Business |

| Cloud-Based |

| Hybrid |

| On-Premise |

| Information Technology (IT) and Telecom |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Industrial Manufacturing |

| Retail and eCommerce |

| Government and Public Sector |

| United States |

| Canada |

| Mexico |

| By Service Type | Core Services | Payroll and Tax Administration |

| Benefits Administration | ||

| HR Operations and Workforce Administration | ||

| Regulatory Compliance Management | ||

| Risk, Safety and Workers Compensation Management | ||

| Value-added Services | Talent Acquisition and Recruitment Support | |

| Learning and Employee Development | ||

| HR Technology Platforms | ||

| By Business Size | Large Business | |

| Small and Medium Business | ||

| By Deployment Mode | Cloud-Based | |

| Hybrid | ||

| On-Premise | ||

| By Industry Vertical | Information Technology (IT) and Telecom | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | ||

| Industrial Manufacturing | ||

| Retail and eCommerce | ||

| Government and Public Sector | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the size of the North America professional employer organization (PEO) market?

The North America professional employer organization (PEO) market size reached USD 6.86 billion in 2025 and is projected to reach USD 10.43 billion by 2031 at a 6.93% CAGR from 2026 to 2031.

Which service area is growing the fastest in the North America professional employer organization (PEO) market?

Value-added services are projected to expand at an 11.94% CAGR through 2031 as employers seek recruitment support, learning tools, and HR technology alongside payroll administration.

Which employer group generates the largest demand for PEO services in North America?

SMBs held 58.21% share in 2025, making them the main client base because they need payroll support, benefits access, and compliance help without building full internal HR teams.

Why is healthcare and life sciences becoming an important growth area?

Healthcare and life sciences is projected to grow at a 12.00% CAGR through 2031 because employers in this segment face high compliance demands and need specialized HR workflows.

Which country leads the region and which one is growing the fastest?

The United States led with 74.11% share in 2025, while Canada is projected to record the fastest growth at an 8.96% CAGR through 2031.

How are leading companies differentiating themselves in 2026?

Leading companies are differentiating through acquisitions, leave management technology, healthcare navigation programs, and tighter HCM integration, as shown by Vensure, TriNet, and Insperity.

Page last updated on: