South America Digital Workplace Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

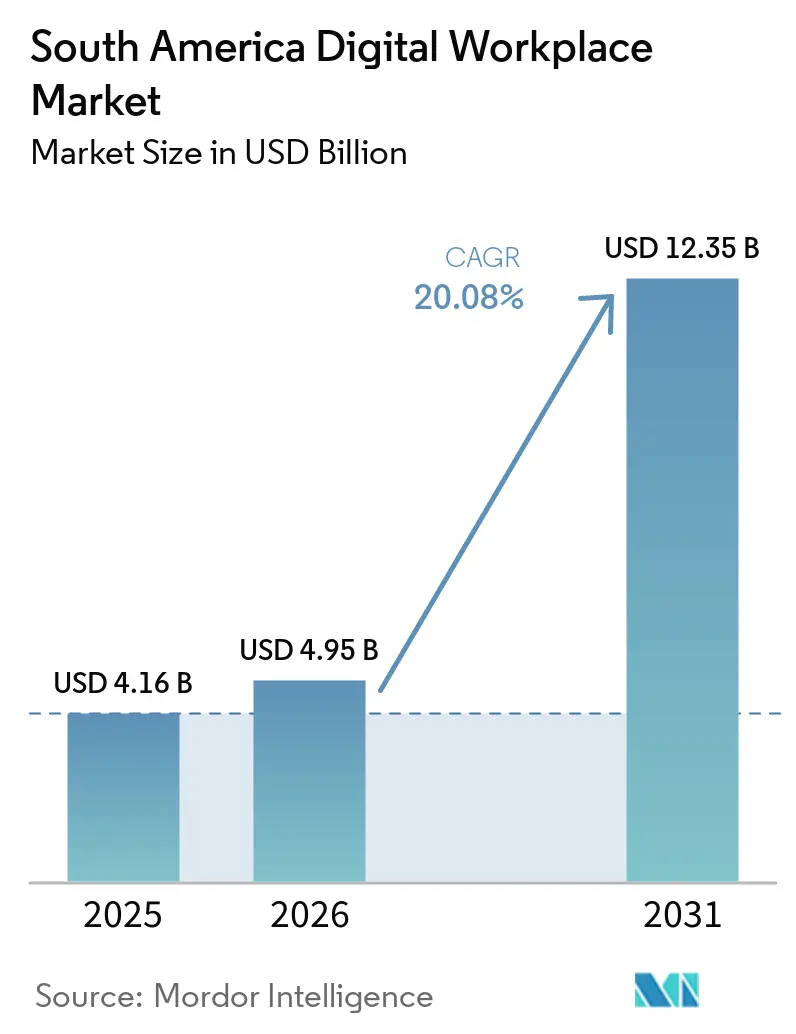

| Base Year Market Size (2025) | USD 4.16 Billion |

| Market Size (2026) | USD 4.95 Billion |

| Market Size (2031) | USD 12.35 Billion |

| Growth Rate (2026 - 2031) | 20.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Digital Workplace Market Analysis by Mordor Intelligence

The South America digital workplace market size was valued at USD 4.16 billion in 2025 and estimated to grow from USD 4.95 billion in 2026 to reach USD 12.35 billion by 2031, at a CAGR of 20.08% during the forecast period (2026-2031). The South America digital workplace market is expanding as hybrid work remains embedded in enterprise operating models across the region, which keeps collaboration, endpoint, and workflow tools tied to recurring modernization budgets. The market is also benefiting from the overlap between cloud migration and workplace platform refresh cycles, because enterprises increasingly treat collaboration, identity, analytics, and employee experience tools as one connected stack rather than separate purchases. Artificial intelligence is becoming a practical buying trigger rather than a trial feature, which is driving demand for copilots, governance controls, and workflow orchestration within workplace suites. Local cloud infrastructure buildouts in large South American economies are reducing earlier barriers tied to latency and data residency, which supports deeper adoption in regulated sectors. Competition remains active across software vendors, hyperscalers, managed service providers, and regional integrators, while integration with legacy applications, talent shortages, and uneven regulatory conditions still slow full deployment in parts of the region.

Key Report Takeaways

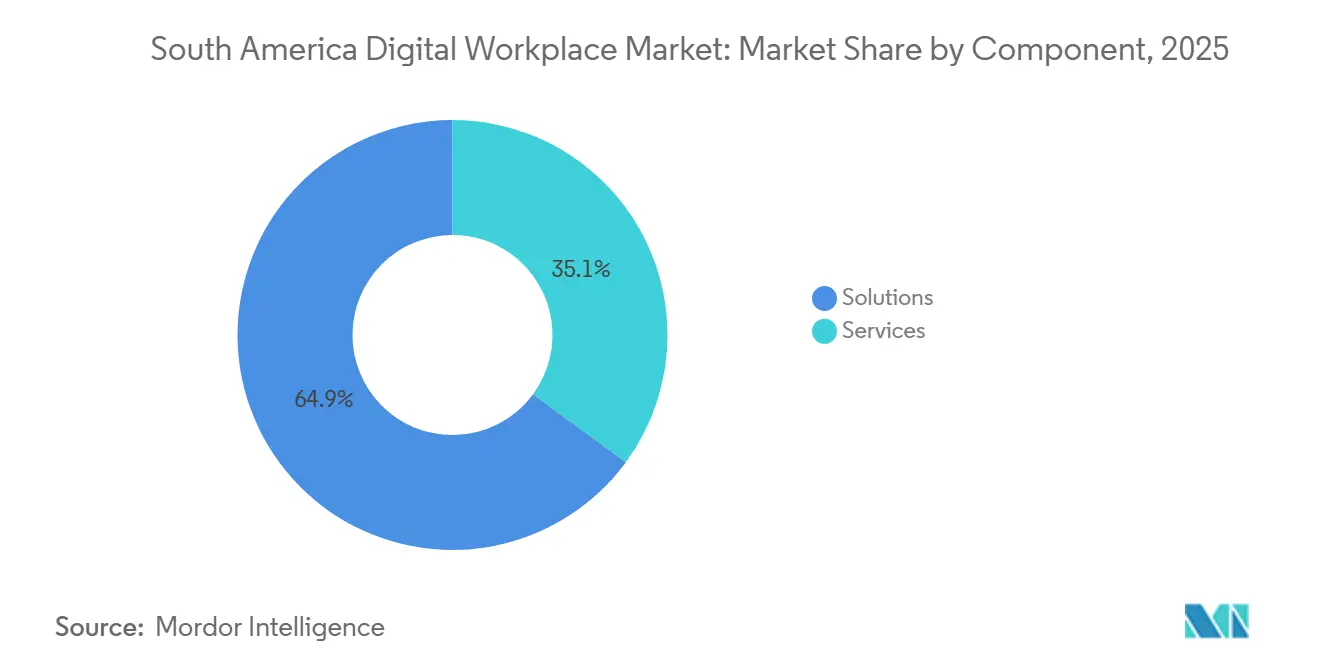

- By component, solutions held 64.93% of the South America digital workplace market share in 2025, while solutions are projected to expand at a 20.48% CAGR through 2031.

- By deployment mode, cloud held a 58.32% share in 2025, and is projected to grow at a 20.64% CAGR through 2031.

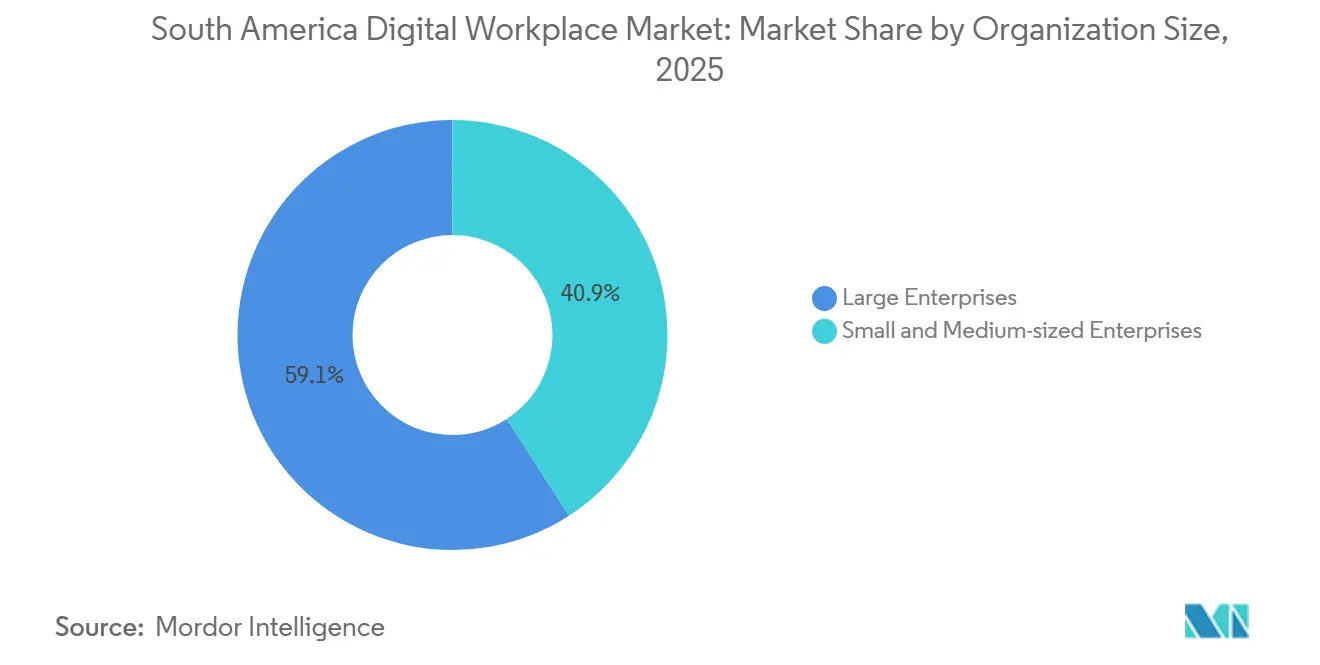

- By organization size, large enterprises accounted for 59.12% of the market share in 2025, while SMEs are projected to record the fastest CAGR of 20.51% through 2031.

- By end-user industry, BFSI led with 22.48% share in 2025, while healthcare is projected to advance at a 22.06% CAGR through 2031.

- By geography, Brazil led with 47.28% of regional revenue in 2025, while Colombia is projected to record the fastest CAGR at 21.11% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Digital Workplace Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Hybrid Work Adoption in Enterprise Operations | +4.2% | Brazil, Argentina, Chile primary, Colombia, Rest of South America secondary | Short term (≤ 2 years) |

| Cloud Migration of Collaboration and Virtual Workspace Stacks | +3.9% | Brazil, Chile primary, Colombia, Argentina secondary | Medium term (2-4 years) |

| AI-Assisted Employee Experience and Workflow Orchestration | +3.5% | Brazil primary, Colombia, Chile secondary | Medium term (2-4 years) |

| Security-First Endpoint and Identity Management Prioritization | +2.8% | Brazil, Chile, Colombia primary, all geographies secondary | Medium term (2-4 years) |

| Expansion of Managed Digital Workplace Outsourcing | +1.6% | Brazil primary, Argentina, Chile secondary | Medium term (2-4 years) |

| Localization Pressure From Data Residency and Sovereignty Rules | +1.4% | Brazil primary, Argentina, Colombia secondary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Hybrid Work Adoption in Enterprise Operations

Hybrid work has moved from a temporary arrangement to a more stable operating model for many enterprises in the region, keeping the South America digital workplace market closely linked to everyday workflow decisions rather than one-time emergency spending. The demand effect extends beyond collaboration software alone, because employers need secure access, managed devices, identity controls, workflow documentation, and policy tracking for staff who move between home, branch, and central-office settings. This operating model also underscores the importance of platforms that connect communication, file access, approvals, and basic employee support within a single system, which helps explain the continued platform consolidation across the South America digital workplace market. Formal remote and hybrid work rules in major economies are also pushing employers toward systems that can consistently support records, approvals, and governance across teams. That requirement underscores the value of integrated workplace platforms over isolated tools, especially when employers must manage distributed staff, sensitive data, and recurring compliance tasks. As a result, hybrid work is not only expanding seat counts in the South America digital workplace market, but also widening the capabilities buyers expect from each deployment.

Cloud Migration of Collaboration and Virtual Workspace Stacks

Cloud migration remains a central growth force in the South America digital workplace market because workplace platforms are easier to scale when collaboration, storage, identity, and security controls sit on shared cloud infrastructure. Microsoft announced a BRL 14.7 billion (USD 2.9 billion) investment over 3 years in cloud and AI infrastructure in Brazil, reflecting long-term confidence in regional enterprise demand and local service capacity.[1]Microsoft, “Microsoft Announces 14.7 Billion Reais Investment Over Three Years in Cloud and AI Infrastructure,” Microsoft News Center Brasil, news.microsoft.com The practical effect of investments like this is that enterprises face fewer barriers tied to latency, resilience, and data locality when moving core workplace functions into cloud environments. That shift matters in the South America digital workplace market because buyers often refresh collaboration, analytics, workflow, and employee service tools at the same time once the base infrastructure question becomes easier to solve. Cloud migration also supports broader vendor participation, as enterprises can mix large platform suites with specialized tools rather than relying on a single on-premises architecture. Over the next few years, this pattern should keep cloud-led contracts at the center of the South America digital workplace market, especially in countries where local infrastructure has become more credible for regulated use cases.

AI-Assisted Employee Experience and Workflow Orchestration

Artificial intelligence is now shaping enterprise workplace spending more directly, and this is becoming one of the clearest demand drivers in the South America digital workplace market. SAP reported in 2025 that 55% of South American decision-makers planned to increase AI investment over 2024 levels, with Brazil leading the region at 62%, indicating that workplace AI budgets are broadening rather than remaining in pilot mode. SAP also reported that 96% of companies in South America planned to train their entire workforce on AI adoption tools, while 94% treated AI proficiency as an important hiring criterion, pointing to a region-wide shift from experimentation to daily use. The Linux Foundation found in 2025 that more than two-thirds of organizations in Latin America were already reporting productivity gains from AI, with more than 40% reporting process automation and cost reductions, reinforcing the business case for AI-enabled workplace platforms. In the South America digital workplace market, that means buyers are more willing to pay for copilots, automation layers, and workflow intelligence that sit inside the broader workplace stack. It also means vendors that can combine AI usefulness with governance, identity, and data control are better placed to win larger and longer contracts in the South America digital workplace market.

Security-First Endpoint and Identity Management Prioritization

Security has become a built-in part of workplace buying decisions, keeping the South America digital workplace market tied to endpoint protection and identity governance as much as to collaboration features. Enterprises in the region are managing larger device fleets, more remote access points, and greater sensitivity to employee and customer data, which makes secure workplace access a core design requirement. This shift favors providers that can package endpoint visibility, identity management, and productivity tools within a single environment rather than treating security as a separate add-on. Microsoft reported in 2026 that TIM Brasil deployed Microsoft Defender XDR to secure around 12,000 endpoints in under 20 days, demonstrating how large buyers are moving toward identity-led, integrated workplace security models. The example matters for the South America digital workplace market because it shows that workplace modernization projects increasingly deliver security outcomes from the start, especially in large enterprises with distributed users and complex device estates. As this pattern spreads, the South America digital workplace market should continue to reward vendors that can combine collaboration, access control, and threat visibility within a single operating model.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Application Integration Complexity | -2.1% | Brazil, Argentina primary, Chile, Colombia secondary | Medium term (2-4 years) |

| Skills Shortage in Workplace Digitalization and Endpoint Security | -1.8% | Brazil primary, Colombia, Argentina, Chile secondary | Long term (≥ 4 years) |

| Fragmented Cross-Border Compliance Requirements | -1.1% | All South American geographies | Long term (≥ 4 years) |

| Limited Rural Connectivity and Uneven Network Quality | -0.9% | Rest of South America primary, rural Brazil, Colombia secondary | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Application Integration Complexity

Legacy application integration remains one of the main restraints on the South America digital workplace market because many enterprises still run older HR, payroll, document, and line-of-business systems that were not built for modern cloud workflows. Even when companies want to deploy new collaboration, automation, or employee service tools, they often need middleware, custom interfaces, or phased migration plans before new platforms can work with existing data and approval flows. This slows implementation, raises project costs, and makes buyers more cautious about large-scale rollouts, especially when workplace programs touch sensitive employee records or regulated processes. The problem is more serious in large organizations where several systems have been layered over time, which limits how quickly the South America digital workplace market can convert strong demand into completed deployments. It also shifts spending toward longer service engagements, because vendors must solve data mapping, access control, and process redesign before the customer can use the full platform value. As a result, the South America digital workplace market continues to grow strongly, but integration complexity still delays adoption speed and margin realization across many enterprise projects.

Skills Shortage in Workplace Digitalization and Endpoint Security

Talent shortages continue to slow parts of the South America digital workplace market because advanced workplace environments need specialists in endpoint security, identity design, AI governance, automation, and digital employee experience. SAP reported in 2025 that 26% of South American companies viewed the shortage of a skilled AI workforce as a significant barrier, confirming that demand for digital capability is rising faster than the available talent.[2]SAP, “Artificial Intelligence in the Corporate World, Regional Report,” SAP News Latin America, news.sap.com The Linux Foundation also found that 84% of employers planned to upskill their workforce to address rising digital skills demand, which shows that companies are responding, but that response still takes time to affect delivery capacity. In practical terms, this means organizations may buy new platforms before they have enough internal skill to configure governance, manage change, or optimize automation at scale. The result is longer vendor dependence, slower feature adoption, and a wider gap between installed technology and realized productivity in the South America digital workplace market. Until deeper local skill pools develop in security, AI operations, and workplace engineering, this talent constraint will remain a meaningful brake on the South America digital workplace market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Architecture Shapes Platform Consolidation

Solutions captured 64.93% of the South America digital workplace market in 2025, indicating that buyers still place the greatest weight on core software platforms that unify communication, files, workflows, and employee-facing tools. This lead also reflects the way enterprise customers now prefer fewer strategic suites rather than scattered point tools that create separate logins, support, and governance burdens. In the South America digital workplace market, this pattern supports vendors that can combine collaboration, productivity, analytics, and automation within a single commercial model. SAP reported in 2025 that 55% of South American decision-makers planned to increase AI investment, which supports the move toward richer solution suites where AI features are embedded into everyday work rather than sold as separate products.

Solutions are projected to expand at a 20.48% CAGR through 2031, which keeps this category at the center of new contract activity in the South America digital workplace market. Services remain smaller in share, but they continue to grow in importance as customers need implementation, integration, change management, and ongoing support as workplace platforms become more intelligent and connected. Kyndryl’s April 2026 launch of its AI-powered Digital Twin for the Workplace shows how service-oriented firms are moving beyond labor-based delivery to offer workplace monitoring, prediction, and operational improvement as part of the wider platform model. That shift suggests the digital workplace industry is no longer splitting neatly between software and services, as large deals increasingly depend on both. Over time, the stronger vendors in the South America digital workplace market are likely to be those that can pair software depth with credible delivery, governance, and operational support across the full workplace environment.

By Deployment Mode: Cloud-Native Momentum Accelerates Across Enterprise Tiers

Cloud held 58.32% of the South America digital workplace market share in 2025, and cloud is also the fastest-growing deployment mode with a 20.64% CAGR through 2031. This leadership reflects a clear regional shift toward platforms that can scale more easily across distributed teams, mobile users, and growing data needs without the heavier maintenance burden of fully local environments. The South America digital workplace market for cloud deployment continues to benefit from stronger local infrastructure, as buyers are more willing to place sensitive collaboration and workflow functions on cloud platforms when latency and locality concerns are easier to manage. Microsoft’s BRL 14.7 billion (USD 2.9 billion) investment in Brazil supports that change by strengthening the underlying environment for enterprise cloud and AI adoption.

Hybrid deployment still holds an important place in the South America digital workplace market because some enterprises need a staged path that keeps selected workloads closer to internal systems or sensitive data controls. This is especially relevant where organizations run older applications that cannot be moved quickly, or where sector rules and internal policy still favor a mixed architecture during transition. On-premises deployment is losing relative weight, but it remains present in parts of government, critical operations, and organizations that are still early in digital modernization. Colombia’s role as host to 12.8% of the region’s digital firms also supports cloud-oriented demand, because many digital-native businesses adopt modern collaboration and security tools earlier and with less legacy friction than older enterprises. The result is that cloud remains the main growth engine across the South America digital workplace market, while hybrid serves as a practical bridge for customers modernizing in stages rather than in one step.

By Organization Size: Large Enterprises Anchor, SMEs Accelerate

Large enterprises captured 59.12% of the market in 2025, which reflects their larger budgets, broader compliance needs, and more complex transformation programs. In the South America digital workplace market, these organizations often need a connected stack that can support many locations, varied user groups, and stricter governance around identity, data handling, and access control. This keeps large enterprises closely tied to multi-vendor deployments, managed support, and structured change programs that smaller firms do not always require at the same scale. Microsoft’s 2026 case with TIM Brasil, where around 12,000 endpoints were secured in under 20 days, illustrates how large regional organizations use integrated workplace and security platforms to handle scale and operational complexity.

SMEs are projected to grow at a 20.51% CAGR through 2031, making them the fastest-growing segment in the South America digital workplace market. Their growth is supported by a lighter legacy burden, faster decision cycles, and a greater willingness to adopt standardized cloud-first tools without large migration programs. The Linux Foundation found that 95% of medium-sized enterprises adopting AI were already reporting positive ROI or breaking even, which suggests that smaller and mid-sized firms can justify workplace technology spending with quicker payback than many larger organizations expect. Colombia’s concentration of digital firms also matters here, because a larger base of technology-native companies creates stronger early demand for scalable workplace tools designed for growth-oriented teams. As a result, the South America digital workplace market is still anchored by large enterprise contracts, but the next layer of acceleration is coming from SMEs that can adopt modern workplace stacks with fewer structural delays.

By End-User Industry: BFSI Leads, Healthcare Generates Structural Demand

BFSI held the largest end-user industry share at 22.48% of regional revenue in 2025, underscoring the sector’s role as the primary adopter of secure, governed, and always-available workplace systems. The sector’s lead in the South America digital workplace market reflects the need to support distributed staff, sensitive customer information, internal approvals, and highly controlled access to data and workflows. Banks and financial institutions also tend to adopt integrated identity, communication, and security models earlier than many other industries because business continuity and trust are essential to their daily operations. This keeps BFSI demand broad, because spending is rarely limited to collaboration tools alone and usually extends into access control, device management, workflow automation, and internal knowledge support.

Healthcare is projected to expand at a 22.06% CAGR through 2031, making it the fastest-growing vertical in the South America digital workplace market. The South America digital workplace market in healthcare is growing as interoperability and digital health programs are forcing providers and public institutions to modernize how staff access, share, and govern clinical information. HL7 International reported in June 2026 that Colombia’s national HL7 FHIR Release 4 framework is designed to process approximately 400 million clinical data documents per year across thousands of providers serving more than 53 million patients, creating direct demand for secure, identity-managed workplace environments. The Inter-American Development Bank also approved USD 85 million to support digital health transformation in Argentina’s Mendoza province as the first tranche of a USD 700 million conditional credit line program, underscoring that public funding is expanding the regional healthcare modernization base. Together, these developments support a stronger and more durable healthcare pipeline inside the South America digital workplace market than was visible only a few years ago.

Geography Analysis

Brazil accounted for 47.28% of regional revenue in 2025, making it the largest country in the South America digital workplace market. Its lead reflects the scale of its enterprise base, the depth of vendor activity, and the fact that many workplace, cloud, and AI decisions in the region are tested first in Brazil before spreading elsewhere. Microsoft’s BRL 14.7 billion (USD 2.9 billion) cloud and AI infrastructure commitment in Brazil supports this leadership by improving the local foundation for enterprise-scale workplace deployments. SAP’s 2025 regional AI report also showed Brazil leading the region, with 62% of decision-makers planning to increase AI investment, which aligns with the country’s role as the main commercialization hub for AI-enabled workplace platforms. Because of that mix of scale, platform activity, and local infrastructure, Brazil remains the primary anchor for the South America digital workplace market.

Colombia is the fastest-growing geography, with a 21.11% CAGR through 2031, and this growth is supported by both digital business formation and sector-specific modernization needs. The US Department of Commerce stated that Colombia hosts 12.8% of the region’s digital firms, indicating a strong base of technology-oriented companies that are more open to modern cloud and collaboration environments.[3]U.S. Department of Commerce, “Colombia, Digital Economy,” International Trade Administration, trade.gov Colombia’s June 2026 HL7 FHIR interoperability framework adds a major public and healthcare dimension to that growth path, as it requires the secure, coordinated handling of very large clinical data flows across the system. Chile has a smaller share, but it remains strategically important in the South America digital workplace market because enterprise buyers continue moving toward governed and security-ready workplace modernization, as shown by Kyndryl’s completion of CMPC’s enterprise-wide Microsoft 365 modernization in June 2026.

Argentina remains part of the South America digital workplace market, with a more selective demand pattern, where compliance needs and targeted modernization persist even when broader economic conditions are less supportive. The Inter-American Development Bank’s support for digital health transformation in Mendoza shows that public digital programs can still create meaningful workplace technology demand in the country. The rest of South America continues to represent a smaller, earlier-stage opportunity, with adoption more concentrated in urban enterprises, regulated institutions, and subsidiaries of larger regional groups. This means the South America digital workplace market remains uneven by geography, with Brazil and Colombia setting the pace, Chile adding strategic enterprise projects, and other countries building demand through narrower but still important modernization programs.

Competitive Landscape

The South America digital workplace market is moderately fragmented, with competition spread across global productivity platforms, cloud infrastructure providers, cybersecurity specialists, managed service firms, and regional integrators. No single vendor profile defines the market, because customers often buy a mix of software, infrastructure, support, and governance from multiple providers as workplace environments become broader and more connected. Microsoft remains influential because it combines productivity software, cloud infrastructure, security tooling, and AI investments in a way that aligns with large enterprise transformation programs in the region. SAP also holds a meaningful position in the South America digital workplace market, where workforce enablement, AI adoption planning, and integrated business platforms overlap, especially as companies prepare employees to use AI more widely. Kyndryl is strengthening its position by tying workplace operations to managed modernization and AI-enabled service improvement, rather than competing solely on labor-intensive implementation models.[4]Kyndryl, “Kyndryl Launches AI-Powered Digital Twin for the Workplace,” Kyndryl News, kyndryl.com

Strategic moves in 2026 show that competition in the South America digital workplace market is shifting toward bundled capabilities and practical outcomes. Microsoft’s infrastructure investment in Brazil signals a long-term commitment to regional cloud and AI demand, supporting its broader workplace ecosystem and partner activity. Kyndryl’s launch of an AI-powered Digital Twin for the Workplace in April 2026 shows how vendors are trying to differentiate through predictive operations and workplace performance management, not only through deployment services. Kyndryl’s June 2026 completion of CMPC’s enterprise-wide Microsoft 365 modernization in Chile also showed that large regional customers are buying integrated projects that combine security, compliance, identity, automation, and collaboration into a single program. These examples suggest that the South America digital workplace market is becoming more solution-led, even when services still play a major role in delivery.

The next phase of competition in the South America digital workplace market is likely to center on who can connect AI usefulness with secure deployment, smoother adoption, and sector-specific workflow control. Vendors that can demonstrate value in healthcare, regulated enterprise environments, and mid-sized cloud-first organizations should have the strongest openings, as those segments of demand are expanding for different reasons at the same time. The TIM Brasil case also shows that buyer confidence improves when providers can deliver measurable security outcomes quickly, making reference projects important for winning larger workplace programs. Overall, the South America digital workplace market favors vendors with ecosystem depth and delivery credibility, but it still leaves room for regional firms that can localize deployment, language support, and operational requirements more effectively than globally standardized offers.

South America Digital Workplace Industry Leaders

Microsoft Corporation

IBM Corporation

Accenture PLC

Google LLC

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Kyndryl completed an enterprise-wide Microsoft 365 modernization project for CMPC, a Chile-based paper and forest products company with global operations. Delivered through Kyndryl Consult, the engagement deployed Microsoft 365 with integrated security, compliance, identity management, and automation capabilities, improving hybrid global team workflows and positioning CMPC for Microsoft 365 Copilot adoption. The project represents a significant managed digital workplace contract win in Chile's industrial sector, where investment in workforce digitalization had lagged behind that of Brazilian and Colombian peers.

- June 2026: Colombia's HL7 FHIR Release 4 national health interoperability framework, the Resumen Digital de Atención en Salud (RDA), went live, targeting 400 million clinical data document exchanges per year across thousands of providers serving more than 53 million patients. Governed by the health ministry and aligned with international HL7 standards, the initiative establishes identity-managed, secure data exchange requirements that healthcare enterprises in Colombia must fulfill through compliant digital workplace platforms, thereby directly expanding the addressable market demand in the healthcare vertical.

- March 2026: Accenture and Microsoft jointly launched a Forward Deployed Engineering (FDE) practice designed to help organizations design, build, and operationalize AI across the enterprise in days rather than months. Joint teams co-innovate using Microsoft's Frontier Suite and proven accelerators, with Accenture leading change management and industry workflow integration. The practice is available to Brazilian and South American enterprise clients and represents one of the most significant collaborative AI workplace deployment models entering the regional market.

- January 2026: Tata Consultancy Services (TCS) announced plans to build its largest delivery center in Londrina, Brazil, with an initial investment of USD 37 million. The campus, expected to be completed in 2027, will create over 1,600 jobs and serve as a strategic hub supporting AI, cybersecurity, ERP, and cloud workplace technologies for South American enterprise clients. The investment follows TCS's September 2025 opening of a Pace Port innovation facility in São Paulo and a Google Cloud Gemini Experience Center in the same city.

South America Digital Workplace Market Report Scope

The South America Digital Workplace Market comprises solutions and services that enable organizations to create digitally connected work environments, facilitating seamless communication, collaboration, productivity, and access to enterprise resources across remote, hybrid, and office-based work settings. Digital workplace offerings include collaboration and communication platforms, virtual workspace solutions, employee experience applications, endpoint and device management tools, workflow automation software, identity and access management solutions, and managed workplace services.

The South America Digital Workplace Market Report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-sized Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Manufacturing, Retail, Government and Public Sector, Education, Energy and Utilities, Legal and Professional Services), and Geography (Brazil, Argentina, Chile, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | Unified Communication and Collaboration |

| Unified Endpoint Management | |

| Enterprise Mobility and Management | |

| Employee Experience Platforms and Intranet | |

| Workflow Automation and Knowledge Management | |

| Virtual Desktop Infrastructure and Cloud PC | |

| Services |

| Cloud |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| IT and Telecommunications |

| BFSI |

| Healthcare |

| Manufacturing |

| Retail |

| Government and Public Sector |

| Education |

| Energy and Utilities |

| Legal and Professional Services |

| Other End-User Industries |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Rest of South America |

| By Component | Solutions | Unified Communication and Collaboration |

| Unified Endpoint Management | ||

| Enterprise Mobility and Management | ||

| Employee Experience Platforms and Intranet | ||

| Workflow Automation and Knowledge Management | ||

| Virtual Desktop Infrastructure and Cloud PC | ||

| Services | ||

| By Deployment Mode | Cloud | |

| Hybrid | ||

| On-Premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By End-User Industry | IT and Telecommunications | |

| BFSI | ||

| Healthcare | ||

| Manufacturing | ||

| Retail | ||

| Government and Public Sector | ||

| Education | ||

| Energy and Utilities | ||

| Legal and Professional Services | ||

| Other End-User Industries | ||

| By Geography | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America |

Key Questions Answered in the Report

What is the South America digital workplace market size through 2031?

The South America digital workplace market size was USD 4.16 billion in 2025, reached USD 4.95 billion in 2026, and is forecast to reach USD 12.35 billion by 2031 at a 20.08% CAGR.

Which deployment model is leading across South America?

Cloud led with 58.32% share in 2025 and is also the fastest-growing deployment mode, with a 20.64% CAGR through 2031.

Why is healthcare growing faster than other end-user segments?

Healthcare is projected to grow at a 22.06% CAGR because interoperability mandates and digital health programs are creating direct demand for secure, identity-managed workplace platforms.

Which country is driving most regional demand?

Brazil remained the largest country in 2025 with 47.28% of regional revenue, supported by its enterprise scale, vendor presence, and continued cloud and AI infrastructure investment.

What is pushing AI adoption in workplace platforms across the region?

Enterprises are moving beyond pilots as SAP reported stronger AI investment plans and the Linux Foundation reported productivity gains and cost reductions from AI use.

Are SMEs becoming more important in this space?

Yes. SMEs are projected to grow at a 20.51% CAGR through 2031, supported by faster adoption cycles, lighter legacy burdens, and stronger early ROI from AI-enabled tools.

Page last updated on: