Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 8.01 Billion |

| Market Size (2031) | USD 10.18 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Packaging Tapes Market Analysis by Mordor Intelligence

The North America Packaging Tapes Market size is estimated at USD 8.01 billion in 2026, and is expected to reach USD 10.18 billion by 2031, at a CAGR of 4.92% during the forecast period (2026-2031). Sustained e-commerce fulfillment automation, the relocation of light assembly under USMCA, and retailer sustainability mandates collectively underpin this steady trajectory. Plastic-based products still dominate the packaging tapes market because they offer tensile strength that withstands harsh logistics environments, yet kraft and other paper variants are winning contracts where repulpability and food-grade compliance drive purchasing decisions. Hot-melt and acrylic chemistries thrive in automated case-sealing lines because they develop handling strength in under one second, mitigating costly work-in-process queues. At the same time, water-based acrylics and water-activated tapes are capturing premium applications that demand low-VOC formulations or overt tamper evidence. Competitive intensity is edging higher: multinationals protect share through vertical integration, while regional converters target short-run, custom-printed orders that large plants struggle to service.

Key Report Takeaways

- By material type, plastic held 77.11% revenue in 2025, whereas paper is projected to advance at a 5.61% CAGR through 2031

- By adhesive type, acrylic led with 47.40% of the packaging tapes market share in 2025; the Others category is set to grow at a 5.07% CAGR through 2031.

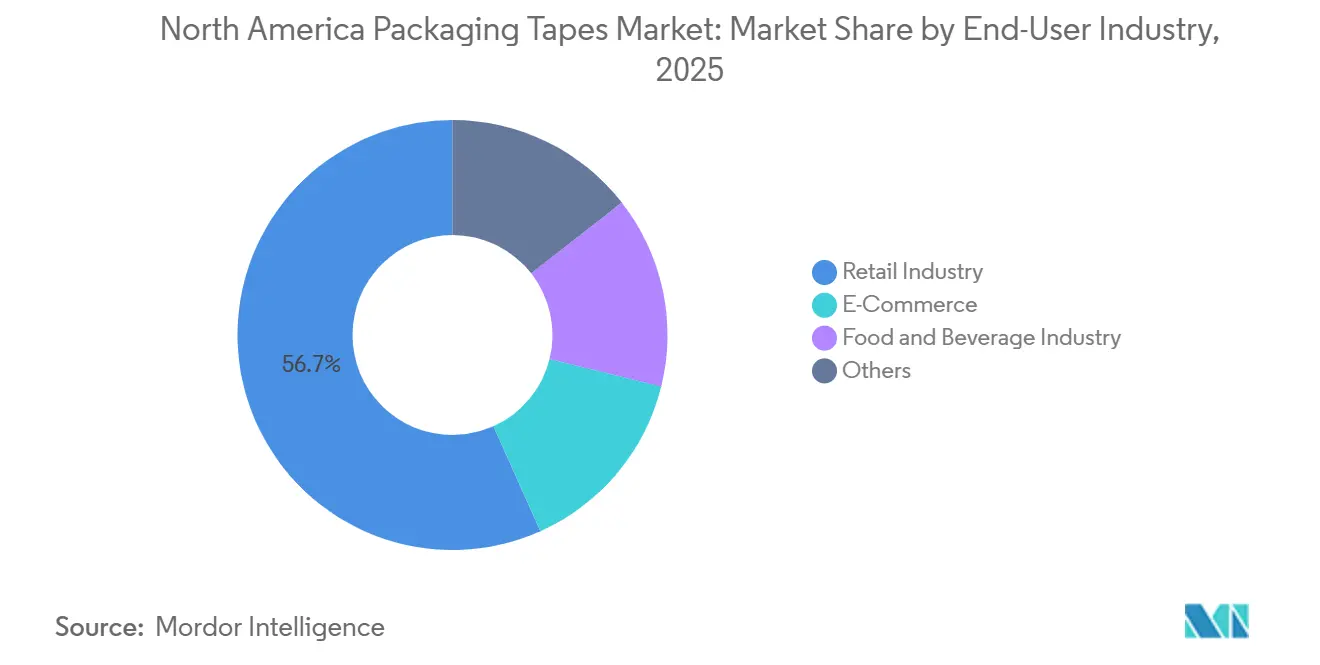

- By end-user industry, retail commanded 56.72% share of the packaging tapes market size in 2025, while e-commerce is forecast to expand at a 7.15% CAGR through 2031.

- By geography, the United States accounted for an 82.85% share of the packaging tapes market size in 2025 and is poised for a 5.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Packaging Tapes Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Resilient e-commerce and omni-channel logistics demand | +1.8% | United States (primary), Canada (secondary), Mexico (emerging cross-border) | Medium term (2-4 years) |

| Food-grade compliance accelerating paper and WAT adoption | +1.2% | United States and Canada (FDA, CFIA enforcement zones) | Long term (≥ 4 years) |

| Automation-ready hot-melt PSA lines at NA fulfillment hubs | +1.0% | United States (Midwest, Southeast fulfillment corridors) | Short term (≤ 2 years) |

| Near-shoring boosts tape demand in cross-border trade zones | +0.7% | Mexico (border states), United States (Texas, Arizona logistics hubs) | Medium term (2-4 years) |

| Digitally-printed, brand-protection tapes gain traction | +0.5% | United States and Canada (high-value goods, pharmaceuticals, electronics) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Resilient E-Commerce And Omni-Channel Logistics Demand

Automation is ratcheting up tape consumption per carton sealed. Amazon’s 2024 warehouse expansion added additional capacity equipped with case sealers that process boxes at a steady rate, each requiring hot-melt tapes that deliver instant grab. Fulfillment providers consolidate inventory into fewer, larger hubs, raising average throughput and ensuring the packaging tapes market continues to expand even if e-commerce penetration levels off. Robotics eliminates manual dwell time, favoring adhesives that bond in under one second, while level-wound rolls support uninterrupted runs on high-speed equipment. Because downtime costs can be high, operators willingly pay premiums for splice-free, automation-grade tapes that guarantee process reliability.

Food-Grade Compliance Accelerating Paper And WAT Adoption

In response to FDA 21 CFR 175.105 and Canada's CFIA regulations, there's a heightened demand for proof that adhesives won't leach into food. This push has nudged buyers towards opting for water-based acrylics or water-activated chemistries on kraft backings. Despite these tapes commanding a price premium, food and beverage brands are willing to absorb the extra cost to safeguard their export certifications. Henkel's AQUENCE PS range, boasting food contact certification, is now penetrating beverage and chilled-food sectors, where a low-temperature tack is essential. With PFAS restrictions tightening, 3M is set to completely withdraw from that chemical class by the close of 2025, necessitating a reformulation of its legacy products. Retailers, aligning supplier scorecards with ESG metrics, view paper tapes as an efficient solution to reduce plastic usage and sidestep EPR fees, positioning them as pivotal players in reshaping the packaging tapes landscape.

Automation-Ready Hot-Melt PSA Lines At NA Fulfillment Hubs

Graco's tankless melters, by cutting energy use, have enabled line speeds previously unattainable with just plastic tapes[1]GRACO, “Tankless Hot-Melt Systems,” graco.com. ExxonMobil's newly launched ENBA copolymer in 2024 further reduces set times, ensuring strong bonds on recycled corrugated surfaces with lower energy. Capital investments per line carry a payback for facilities processing more than 5,000 cartons per shift, solidifying adoption. Once installed, automated lines lock in adhesive specifications, giving tape suppliers long contracts—an advantage that keeps growth in the packaging tapes market resilient even during macro slowdowns.

Near-Shoring Boosts Tape Demand In Cross-Border Trade Zones

In 2023, Mexico overtook China to become the largest goods trading partner of the United States. This shift spurred growth in Mexican packaging demand and bolstered northbound shipments, particularly those dependent on high-tensile BOPP tapes[2]USITC, “USMCA Automotive Rules of Origin,” usitc.gov . International Paper operates corrugating plants close to Laredo and El Paso, enabling them to deliver cartons and tape to automotive and electronics assemblers on both sides of the border by the next day. Given the temperature fluctuations—from the intense desert heat to the chill of refrigerated railcars—products need to be rated for a range of -20°F to 180°F. This requirement has led to Shurtape’s HP-232 securing contracts specifically for cold-chain lanes. As a result, near-shoring has solidified multi-year volume commitments, providing a buffer for the packaging tapes market against spending slowdowns seen in other sectors.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile propylene and rubber feedstock prices | -0.9% | United States and Canada (Gulf Coast and Alberta petrochemical clusters) | Short term (≤ 2 years) |

| Rising state plastic-waste EPR fees on BOPP/PVC tapes | -0.6% | California, Colorado, Maine, Oregon (state-level enforcement) | Medium term (2-4 years) |

| Capital cost of converting legacy lines to water-based systems | -0.4% | United States and Canada (converter facilities requiring retrofit) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Propylene And Rubber Feedstock Prices

In 2024, spot propylene prices fluctuated across Gulf Coast hubs. This volatility led to a reduction of BOPP margins within a single quarter. Similarly, rubber raw materials experienced price swings, largely attributed to weather disruptions in Southeast Asia. While larger manufacturers can hedge against these fluctuations using multi-year contracts, regional converters often lack this advantage. As a result, they are compelled to pass on the volatility to buyers, albeit with a delay. This delay strains their relationships with high-volume retailers, who typically budget for annual tape costs months in advance. Consequently, even as the packaging tapes market sees a rise in volume, spikes in feedstock prices dampen profit expectations.

Rising State Plastic-Waste EPR Fees On BOPP/PVC Tapes

California's SB 54, set to introduce producer fees in 2027, aims for a reduction in plastic waste by 2032. This legislation has already led to an uptick in costs for non-recyclable tapes. Meanwhile, similar laws in Colorado, Maine, and Oregon have created a compliance maze. Distributors now find themselves needing to stock state-specific SKUs, which can inflate their working capital annually for each state. Companies like Tesa have been proactive, launching recycled-PET tapes that pass curbside-recycling tests. However, these tapes come with a price premium, making them less appealing in low-margin markets. As a result, EPR tariffs are hindering the transition to alternative plastic grades in the packaging tapes market, particularly for commodity uses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Paper Adoption Outpaces Plastics In Sustainability-Focused Accounts

Paper tapes are forecast to rise 5.61% CAGR through 2031, eclipsing overall packaging tapes market growth as brands target substrates that move seamlessly through recycling mills. Plastic grades retained 77.11% of 2025 revenue because BOPP resists humidity and maintains tensile strength in export shipments, yet national retailers have committed to eliminating unrecyclable components by 2030. These pledges allow paper variants to cannibalize low-risk SKUs, especially in e-commerce channels where tape visibility also supports branding.

Kraft backings paired with water-activated adhesives seal fiber-based cartons without contaminating paper streams, making them a preferred option in states that impose EPR fees. Reinforced paper tape closes historical strength gaps, enabling paper to secure medium-duty loads previously reserved for plastic. Conversely, frozen food and cross-continent routes still demand plastic grades that withstand extreme temperatures. Adhesive formulators respond by tailoring tack to recycled corrugate, ensuring both substrates retain their share in their respective niches as the packaging tapes market diversifies.

By Adhesive Type: Acrylics Dominate While Water-Based Platforms Accelerate

Acrylic chemistries controlled 47.40% of 2025 revenue because they endure wide temperature swings and satisfy FDA food-contact rules. Hot-melt grades remain the workhorses of automated lines, yet water-based and silicone formulations headline the fastest-growing Others category, set to expand 5.07% CAGR.

Driven by automation incentives, suppliers are racing to reduce set times. For instance, ExxonMobil's ENBA copolymer achieves a significant reduction in cure windows, enabling tapes to bond with recycled boxes swiftly. Water-based acrylics are securing contracts, especially when low-VOC operations or curbside recyclability are prioritized in RFPs. Although rubber matrices are losing ground in FDA or CFIA-regulated applications due to migration concerns, they remain a cost-effective choice for light-duty carton sealing. The delicate balance of speed, temperature adaptability, and regulatory adherence is reshaping adhesive choices, creating diverse opportunities within the packaging tapes market.

By End-User Industry: E-Commerce Is Small But Fast, Retail Remains Core

Retail distribution centers consumed 56.72% of 2025 demand thanks to high-volume carton sealing, yet e-commerce posts the briskest expansion, tracking a 7.15% CAGR to 2031. Every new automation-ready fulfillment hub leverages hot-melt tapes optimized for robotic application, lifting value per carton even before overall parcel counts climb.

Food and beverage processors are opting for water-based acrylics and water-activated paper. These choices ensure compliance with food-contact standards and cold-chain requirements, particularly in scenarios where condensation poses a risk of adhesive failure. In the 'Others' category, pharmaceuticals and electronics are investing more per carton. This is largely due to the premium pricing of tamper-evident and digitally printed security tapes. Such premium segments introduce lucrative avenues, bolstering supplier margins. This is especially notable as more commoditized applications face sporadic price pressures. As a result, the packaging tapes market is diversifying its growth avenues, rather than relying on a singular vertical.

Geography Analysis

The United States anchors 82.85% of regional revenue and will expand at a 5.11% CAGR through 2031 as Midwest and Southeast fulfillment hubs ramp robotic case sealing lines. In California, the push from the state's EPR law is hastening a shift towards paper and recycled-PET tapes. This shift has birthed a dual-tier market, where sustainable offerings command impressive premiums. The scale advantages in the industry are starkly highlighted by a facility that churns out a staggering amount of tape each year. This output allows for a just-in-time replenishment capability, a feat that regional converters find hard to replicate. Furthermore, the enforcement of FDA 21 CFR 175.105 has raised the compliance stakes, steering orders towards suppliers who can provide documented migration testing.

In Canada, despite its smaller size, there's a pronounced per-capita usage of cold-temperature tape. This is largely attributed to the country's prolonged winters, which push logistics networks to operate below 0°F. The CFIA standards in Canada closely align with U.S. regulations, subtly guiding buyers towards water-based or paper solutions that mitigate migration risks. Local facilities are strategically positioned, slashing lead times for cold-chain clients and supplying acrylics that maintain their tackiness even in sub-zero temperatures.

Mexico is reaping the benefits of near-shoring under the USMCA agreement, capturing an increasing share of the automotive and electronics assembly sectors. These sectors have a growing demand for high-tensile BOPP grades. Border-adjacent corrugators are adeptly meeting same-day demands. Meanwhile, versatile dual-temperature portfolios are adept at managing both the sweltering desert heat and the needs of refrigerated railcars. This interconnectedness is further underscored by the movement of U.S.-made adhesives heading south and finished cartons making their way north, solidifying an integrated supply chain that bolsters the overarching packaging tapes market.

Competitive Landscape

The North American packaging tapes market is moderately consolidated. Integrated production of both adhesive mass and finished tape lets these incumbents guarantee lot-to-lot consistency demanded by automated lines. 3M’s RoboTape platform marries equipment and consumables, locking customers into multiyear tape contracts that carry above-market margins. Regional converters compete on custom printing, rapid turnaround, and flexible minimums. Digital inkjet has slashed setup costs, allowing security graphics and QR codes on runs as small as 500 cartons. This capability attracts mid-tier brands keen to elevate parcel presentation without absorbing plate fees. As a result, the packaging tapes market supports both mass-scale commodity volumes and profitable micro-niches. The need to reformulate ahead of PFAS prohibitions places small entrants at a disadvantage, because regulatory compliance requires a dedicated technical staff and multi-million-dollar pilot lines.

North America Packaging Tapes Industry Leaders

3M

Intertape Polymer Group Inc.

Shurtape Technologies LLC

Avery Dennison Corporation

Amcor plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Vibac Group, a producer of packaging adhesive tapes for food packaging, opened a Tennessee operation to shorten lead times and raise United States service levels.

- January 2025: Tesa launched tesafilm Paper, its first paper-carrier variant in the tesafilm range, reinforcing its sustainability roadmap.

North America Packaging Tapes Market Report Scope

Packaging tape is a pressure-sensitive tape used to seal and close boxes, packages, and other containers. It is typically made of a thin plastic film with an adhesive coating on one side. Packaging tape is used to keep items secure during shipping and storage and to label and identify packages.

The packaging tapes market is segmented by material type, adhesive type, end-user industry, and geography. By material type, the market is segmented into plastic and paper. By adhesive type, the market is segmented into acrylic, hot-melt, rubber-based, and other adhesive types (synthetic rubber adhesive, pressure-sensitive adhesive, and others). The end-user industry is segmented into e-commerce, food and beverage industry, retail industry, and other end-user industries (cosmetics, textiles, and pharmaceuticals). The report also covers the market size and forecasts for three countries across the regions. For each segment, the market sizing and forecasts were made on the basis of value (USD).

By Material Type

| Plastic |

| Paper |

By Adhesive Type

| Acrylic |

| Hot-Melt |

| Rubber-Based |

| Others |

By End-User Industry

| E-Commerce |

| Food and Beverage Industry |

| Retail Industry |

| Others |

Geography

| United States |

| Canada |

| Mexico |

| By Material Type | Plastic |

| Paper | |

| By Adhesive Type | Acrylic |

| Hot-Melt | |

| Rubber-Based | |

| Others | |

| By End-User Industry | E-Commerce |

| Food and Beverage Industry | |

| Retail Industry | |

| Others | |

| Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the value of the North American packaging tapes market?

The packaging tapes market size is USD 8.01 billion in 2026, reaching USD 10.18 billion by 2031, registering a 4.92% CAGR.

How fast is the U.S. segment expected to grow?

The United States is forecast to expand at a 5.11% CAGR between 2026 and 2031.

Which material type is gaining traction due to sustainability mandates?

Paper tapes are growing at a 5.61% CAGR because they align with repulpability and EPR objectives.

Why are acrylic adhesives so widely adopted?

They offer broad temperature tolerance and FDA food-contact compliance while suiting high-speed automation.

What factor most influences tape demand in cross-border trade?

Near-shoring under USMCA boosts high-tensile BOPP tape volumes for automotive and electronics exports.

Page last updated on: