Liver Cancer Therapeutics Market Size

| Study Period | 2019 - 2029 |

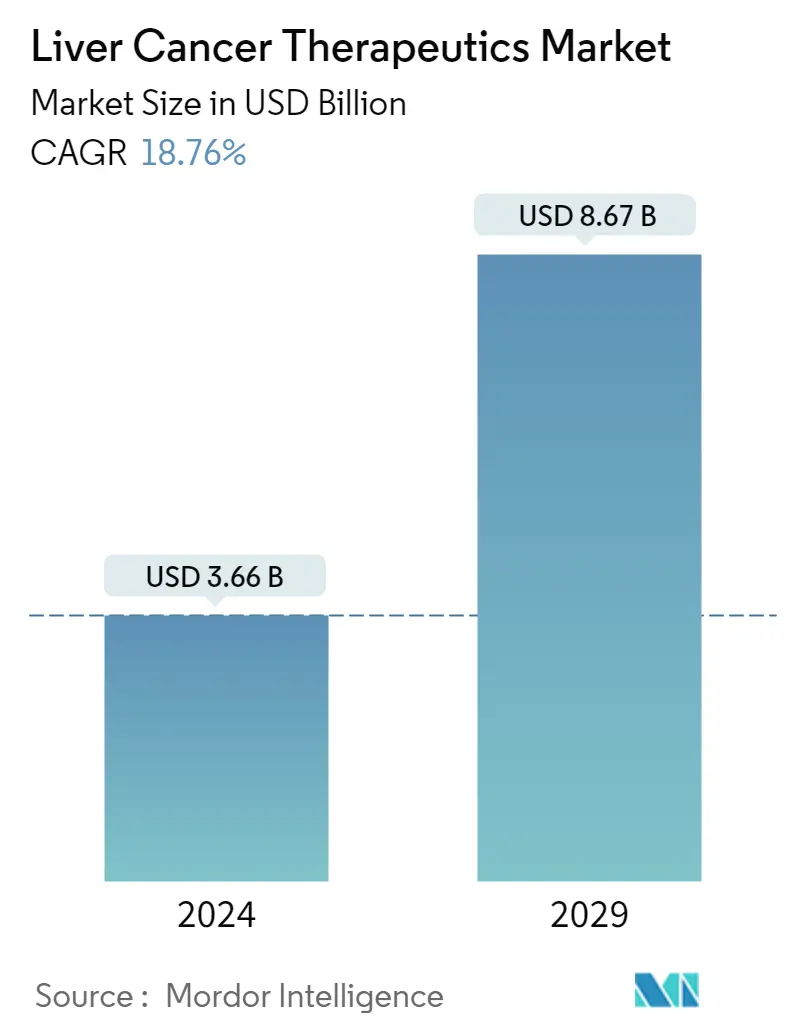

| Market Size (2024) | USD 3.66 Billion |

| Market Size (2029) | USD 8.67 Billion |

| CAGR (2024 - 2029) | 18.76 % |

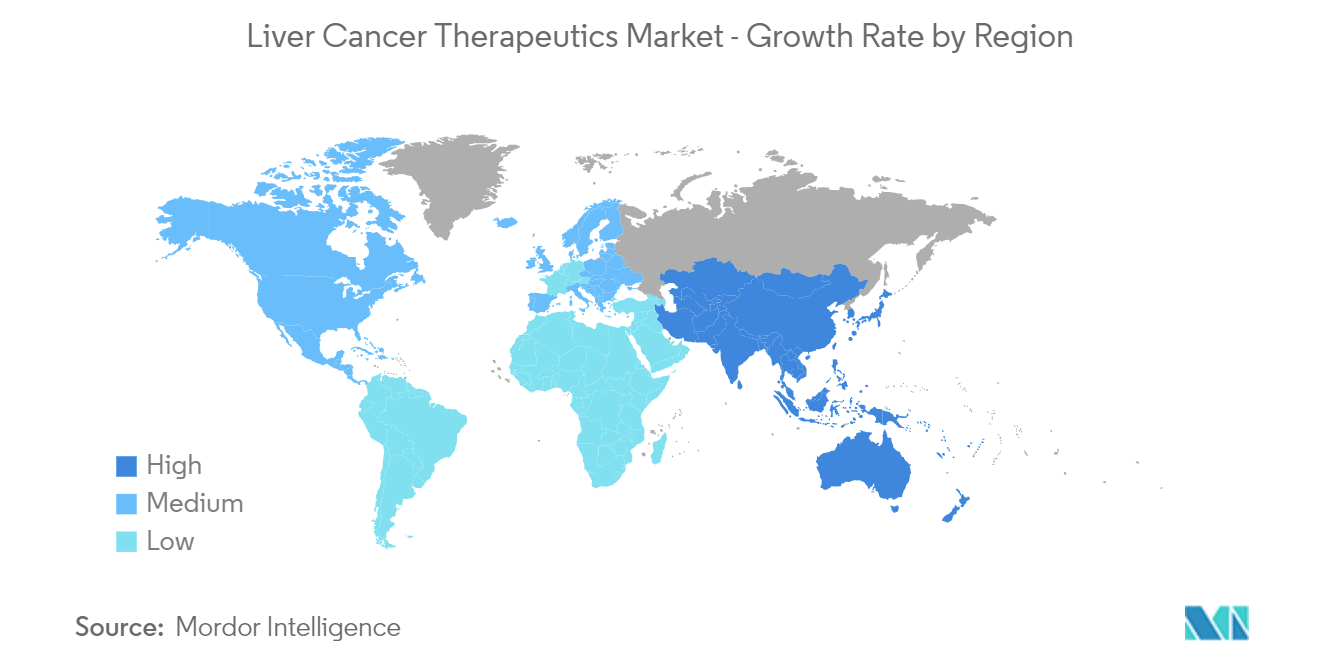

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Liver Cancer Therapeutics Market Analysis

The Liver Cancer Therapeutics Market size is estimated at USD 3.66 billion in 2024, and is expected to reach USD 8.67 billion by 2029, growing at a CAGR of 18.76% during the forecast period (2024-2029).

- The emergence of COVID-19 had a major impact on patients other than COVID-19 due to the high burden on healthcare resources owing to the high infection rate of the SARS-CoV-2 virus. People with liver cancer were also impacted by the pandemic, as due to COVID-19, there was a delay or rescheduling of the diagnostics and treatment procedures. Also, people with comorbidity were at higher risk of contracting COVID-19, which led to a decline in the patient pool in hospitals for treatment and diagnostics of new cases.

- For instance, according to a research study published in February 2021 in PubMed, the normal treatment of patients with liver cancer was significantly impacted by the first wave of the COVID-19 epidemic, and changes to the algorithms for screening, diagnosing, and treating patients may have materially harmed their prognosis during the pandemic. However, as the number of COVID-19 cases decreases, the liver cancer therapeutics market is expected to gain its full growth potential in the coming years due to the increase in research and development for cancer therapeutics and intense competition between the key players to introduce various pipeline assets for liver cancer therapies.

- The major factors driving the market growth include the rising burden of liver cancer, increasing research and development investments for the development of novel therapies, and government initiatives to increase cancer awareness.

- According to the Cancer Australia 2022 statistics, 2,905 new cases of liver cancer were diagnosed in Australia (2,113 males and 792 females) in 2022. Also, a person had a 1 in 103 (or 0.97%) risk of being diagnosed with liver cancer by the age of 85 (1 in 70 or 1.4% for males and 1 in 195 or 0.51% for females) in 2022 in Australia. Hence, the demand for effective and advanced liver cancer therapeutics is expected to increase over the years, fuelling market growth. The change in the current lifestyle led to the exposure of a large population to certain risk factors that contribute to liver cancer. The risk factors include type 2 diabetes, hepatitis, metabolic disorders, excess body weight, alcohol consumption, and smoking, which are further expected to augment the liver cancer therapeutics market's growth over the forecast period.

- Moreover, the increasing research activities and funding in the area are further expected to boost the market's growth as a positive outcome from these studies may pave the way for a novel treatment for liver cancer. For instance, in March 2023, New Castle University Scientists received nearly GBP 6 million (USD 7.4 million) from Cancer Research UK to fund their fight against the disease in adults and children. Patients with liver cancer are estimated to benefit from nearly GBP 2 million (USD 2.4 million).

- Furthermore, various liver cancer awareness campaigns are being conducted, which further paves the path for patient education and the importance of liver cancer therapies, which is expected to fuel the market growth over the forecast period. For instance, in July 2022, Qatar Cancer Society (QCS), in cooperation with Qatar Red Crescent, launched the 'Protect Yourself' campaign to raise awareness of liver cancer. Also, the campaign contained several workshops and speeches aimed at promoting awareness, particularly in workers' centers.

- Therefore, the high burden of liver cancer and its risk factors, coupled with ongoing research and development activities, is expected to boost the market's growth over the forecast period. However, factors such as side effects associated with certain medications, the high cost of cancer therapies, and stringent regulatory scenarios are expected to impede market growth over the forecast period.

Liver Cancer Therapeutics Market Trends

Hepatocellular Carcinoma Segment is Expected to Occupy a Significant Share Over the Forecast Period

- Hepatocellular carcinoma (HCC) is a common form of liver cancer that occurs in people suffering from chronic liver diseases like cirrhosis. Since HCC usually grows slowly in its early stages, it can often be cured if discovered early enough with proper treatment options.

- Factors such as an increase in strategic activities by the key players, awareness relating to liver cancer treatments, and a rise in research studies related to the treatments for HCC are expected to bolster segment growth over the forecast period.

- Various therapies have emerged for treating HCC, which made the segment more exposed to research and development. For instance, as per the article published in April 2021 in Nature Journal, the best available first-line treatment for advanced HCC is a combination of PDL1 blockade with atezolizumab and VEGF blockade with bevacizumab. Immunotherapy is likely to synergize with local and locoregional interventions in earlier stages of HCC. Thus, the introduction of new immunotherapies in HCC is expected to bolster segment growth over the forecast period.

- Furthermore, a rise in approvals and strategic activities by the key players is expected to augment the market growth. For instance, in February 2023, Genoscience Pharma received a Food Drug Administration (FDA) Orphan Drug Designation for ezurpimtrostat to treat hepatocellular carcinoma (HCC). Ezurpimtrostat (GNS561) is a first-in-class, first-in-human autophagy inhibitor whose anticancer activity is linked to PPT-1 inhibition.

- Also, in October 2022, the National Medical Products Administration (NMPA) of China approved the supplemental New Drug Application (sNDA) for CYRAMZA (ramucirumab) by Innovent Biologics, Inc., in patients with hepatocellular carcinoma (HCC, also known as liver cancer), who have an alpha-fetoprotein of more than or equal to 400 ng/mL and have been treated with sorafenib. Also, in March 2022, Innovent and Lilly expanded their strategic partnership in oncology.

- Therefore, due to the increase in research activities and strategic initiatives by the key players coupled with product launches, the studied segment is expected to witness significant growth over the forecast period.

North America is Anticipated to Hold a Significant Market Share Over the Forecast Period

- North America is expected to hold a significant share of the studied market owing to the rising incidence of liver cancer in the region, the presence of key market players, and the launch of novel products coupled with various investments as well as funding for liver cancer therapeutics development. For instance, as per the Canadian Cancer Society 2022 statistics, 3,500 Canadians were diagnosed with liver cancer in Canada.

- The substantial prevalence of liver cancer in the region is anticipated to be the key driving force for the market. As awareness of liver cancer continues to rise and its burden increases, there is a corresponding surge in the adoption and demand for treatment procedures. This is expected to exert a favorable influence on the market under examination.

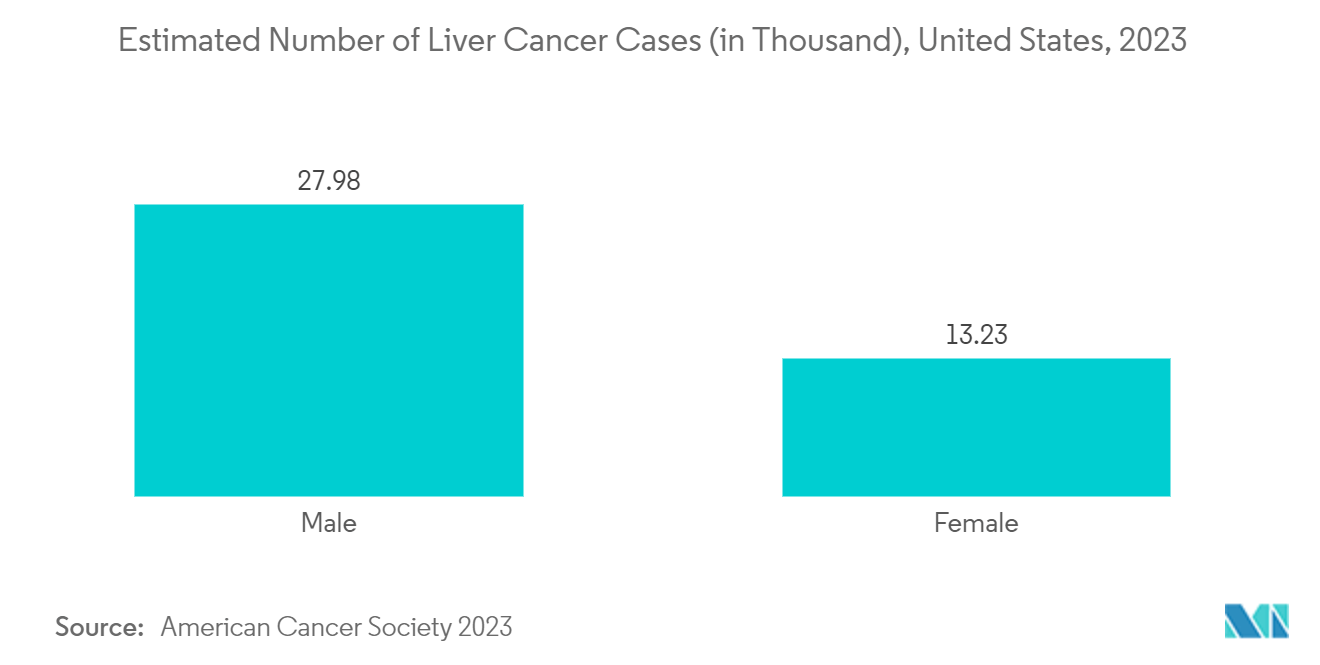

- For instance, according to the 2023 report of the American Cancer Society, about 41,210 new cases of liver and intrahepatic bile duct cancer are expected to be diagnosed in the United States in 2023, which is expected to have a positive impact on liver cancer therapeutics market. Further, the increasing research and development activities and strategic activities by the key players in the development of novel therapeutics for the liver are also expected to drive market growth.

- For instance, in March 2021, Boston Scientific Corporation received FDA approval for the TheraSphere Y-90 Glass Microspheres, developed for the treatment of patients with hepatocellular carcinoma (HCC). Similarly, in January 2022, Merck received conditional liver cancer treatment approval for its drug Keytruda based on its second confirmatory study. Keytruda slashed the risk of death by 21% over placebo in hepatocellular carcinoma patients in Asia.

- Therefore, the increased incidence of liver cancer and the rise in strategic activities by the key players increase the demand for liver cancer treatment in the studied region, which is driving the market over the forecast period.

Liver Cancer Therapeutics Industry Overview

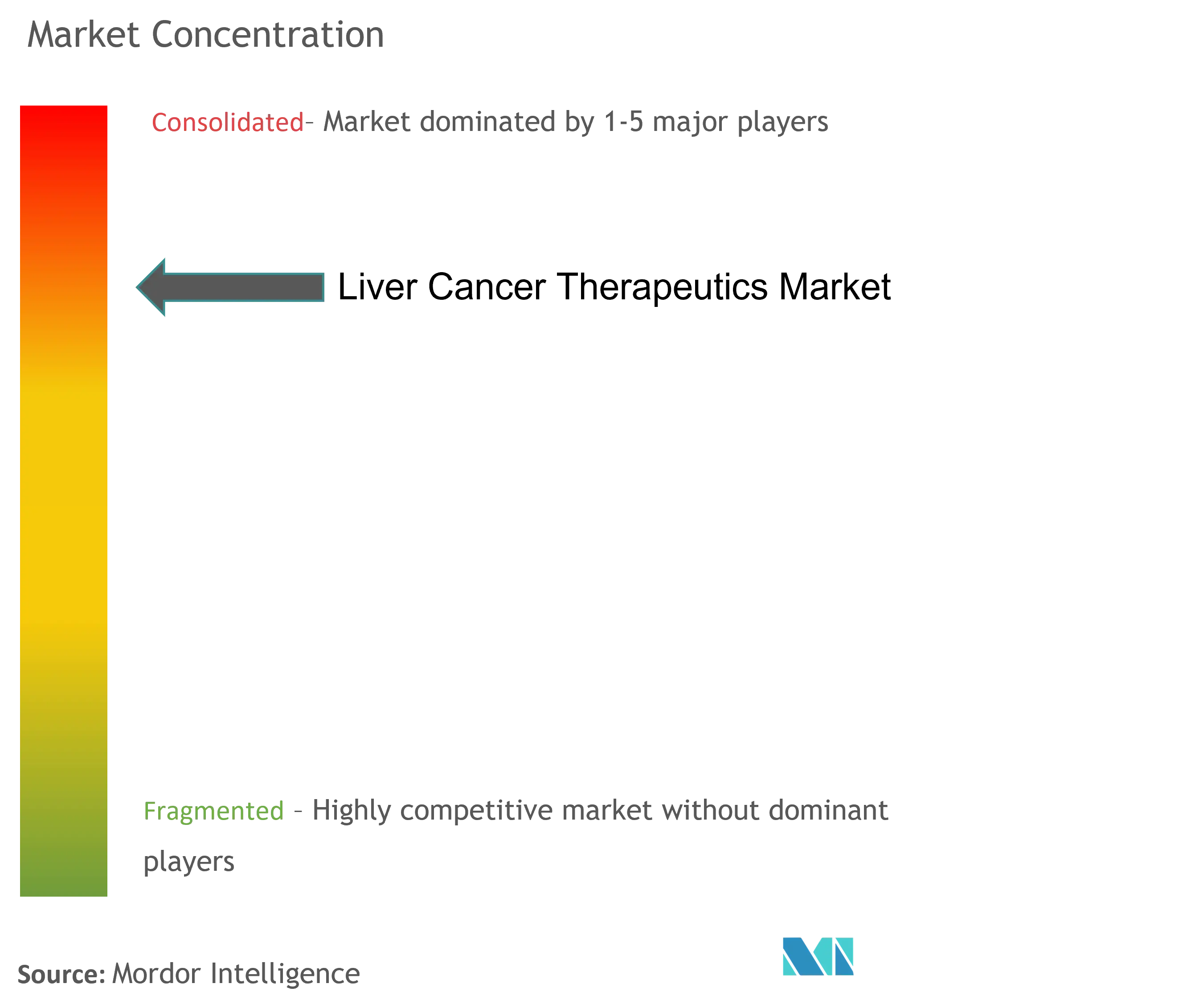

The liver cancer therapeutics market studied is consolidated in nature owing to the presence of a few major market players. The key market players are focusing on R&D to bring innovative treatments for the treatment of liver cancer. The key market players are F. Hoffmann-La Roche Ltd, Bayer AG, Bristol Myers Squibb Company, Eisai Co. Ltd, and Exelixis Inc., among others.

Liver Cancer Therapeutics Market Leaders

Bristol‑Myers Squibb Company

Eisai Co., Ltd.

Exelixis Inc

Merck & Co. Inc.

Bayer AG

*Disclaimer: Major Players sorted in no particular order

Liver Cancer Therapeutics Market News

- March 2023: The University of Southern California (USC) collaborated with Auransa Inc. on a phase 1 clinical trial to evaluate a new kind of treatment for cancers of the liver and solid tumors with liver-dominant disease. The drug, known as AU409, was developed by Auransa, a clinical-stage drug development company focused on identifying novel drug candidates for oncology, inflammatory diseases, and diseases of the central nervous system.

- February 2023: AstraZeneca's Imfinzi (durvalumab) and Imjudo (tremelimumab) immunotherapy combinations were approved in the European Union (EU) for the treatment of advanced liver and lung cancers. The approvals authorize Imfinzi in combination with Imjudo for the 1st-line treatment of adult patients with advanced or unresectable hepatocellular carcinoma (HCC) and Imfinzi in combination with Imjudo and platinum-based chemotherapy for the treatment of adult patients with metastatic (Stage IV) non-small cell lung cancer (NSCLC).

Liver Cancer Therapeutics Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definitions

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Rising Burden of Liver Cancer

4.2.2 Increasing R&D Investments for the Development of Novel Therapies

4.2.3 Government Initiatives to Increase the Cancer Awareness

4.3 Market Restraints

4.3.1 Side Effects Associated with Certain Medications Coupled with High Cost of Cancer Therapies

4.3.2 Stringent Regulatory Scenario

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

5.1 By Type

5.1.1 Hepatocellular Carcinoma

5.1.2 Cholangio Carcinoma

5.1.3 Hepatoblastoma

5.1.4 Other Types

5.2 By Therapy

5.2.1 Targeted Therapy

5.2.2 Radiation Therapy

5.2.3 Immunotherapy

5.2.4 Chemotherapy

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Italy

5.3.2.5 Spain

5.3.2.6 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 Australia

5.3.3.5 South Korea

5.3.3.6 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 GCC

5.3.4.2 South Africa

5.3.4.3 Rest of Middle East and Africa

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 F. Hoffmann-La Roche Ltd

6.1.2 Bayer AG

6.1.3 Bristol Myers Squibb Company

6.1.4 Celsion Corporation

6.1.5 Eisai Co. Ltd

6.1.6 Exelixis Inc.

6.1.7 Eli Lilly and Company

6.1.8 Merck & Co. Inc.

6.1.9 Pfizer Inc.

6.1.10 AbbVie Inc.

6.1.11 Amgen Inc.

6.1.12 AstraZeneca PLC

6.1.13 Johnson & Johnson

6.1.14 Sanofi SA

6.1.15 Novartis AG

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Liver Cancer Therapeutics Industry Segmentation

Liver cancer is cancer that begins in the liver cells. It is a chronic, life-threatening, and progressive disorder that begins in the cells of the liver. Liver cancer can be of different types, such as cancer that begins in hepatocyte cells, known as primary hepatic cancer, and cancer that spreads to the liver from other parts of the body, known as metastatic cancer.

The liver cancer therapeutics market is segmented by type (hepatocellular carcinoma, cholangiocarcinoma, hepatoblastoma, and other types), therapy (targeted therapy, radiation therapy, immunotherapy, and chemotherapy), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (USD) for the above-mentioned segments.

| By Type | |

| Hepatocellular Carcinoma | |

| Cholangio Carcinoma | |

| Hepatoblastoma | |

| Other Types |

| By Therapy | |

| Targeted Therapy | |

| Radiation Therapy | |

| Immunotherapy | |

| Chemotherapy |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Liver Cancer Therapeutics Market Research FAQs

How big is the Liver Cancer Therapeutics Market?

The Liver Cancer Therapeutics Market size is expected to reach USD 3.66 billion in 2024 and grow at a CAGR of 18.76% to reach USD 8.67 billion by 2029.

What is the current Liver Cancer Therapeutics Market size?

In 2024, the Liver Cancer Therapeutics Market size is expected to reach USD 3.66 billion.

Who are the key players in Liver Cancer Therapeutics Market?

Bristol‑Myers Squibb Company, Eisai Co., Ltd., Exelixis Inc, Merck & Co. Inc. and Bayer AG are the major companies operating in the Liver Cancer Therapeutics Market.

Which is the fastest growing region in Liver Cancer Therapeutics Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Liver Cancer Therapeutics Market?

In 2024, the North America accounts for the largest market share in Liver Cancer Therapeutics Market.

What years does this Liver Cancer Therapeutics Market cover, and what was the market size in 2023?

In 2023, the Liver Cancer Therapeutics Market size was estimated at USD 3.08 billion. The report covers the Liver Cancer Therapeutics Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Liver Cancer Therapeutics Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Liver Cancer Therapeutics Industry Report

Statistics for the 2024 Liver Cancer Therapeutics market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Liver Cancer Therapeutics analysis includes a market forecast outlook to for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.