Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.82 Trillion |

| Market Size (2026) | USD 12.92 Trillion |

| Market Size (2031) | USD 20.13 Trillion |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

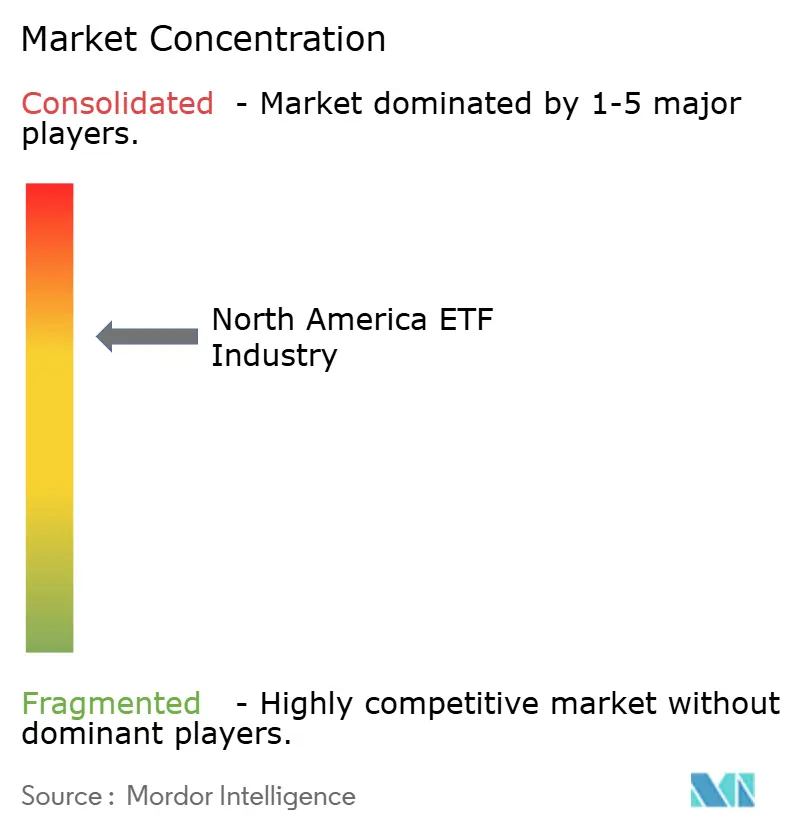

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America ETF Market Analysis by Mordor Intelligence

The North America ETF market size was valued at USD 11.82 trillion in 2025 and estimated to grow from USD 12.92 trillion in 2026 to reach USD 20.13 trillion by 2031, at a CAGR of 9.28% during the forecast period (2026-2031). The uptrend mirrors a decisive migration from mutual funds toward lower-cost ETFs, sustained record inflows at the largest providers, and a proliferation of both passive and active strategies. Retail investors, now controlling a 54.4% slice of assets, continue to accelerate adoption through commission-free trading apps that blur the lines between professional and self-directed investing. Active ETFs, though still a fraction of total assets, are growing almost twice as fast as the overall North America ETF market, encouraged by the 2019 SEC ETF Rule 6c-11 and the arrival of non-transparent wrappers. Fixed-income ETFs are the breakout asset class as institutions favor them for liquidity management during volatile conditions. Meanwhile, Mexico’s rapid 12.9% CAGR underscores the nearshoring boom, while competitive fee compression is forcing issuers to lean on innovation rather than cost alone to protect margins.

Key Report Takeaways

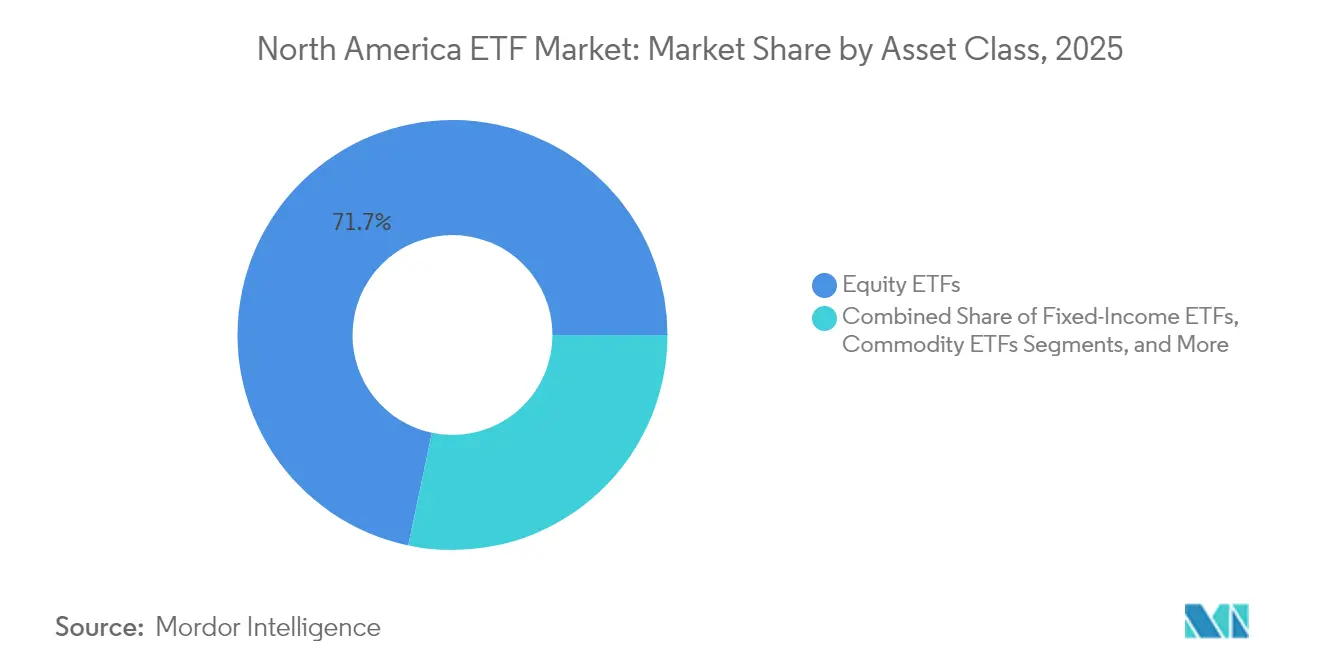

- By asset class, equity retained 71.70% of the 2025 North America ETF market share, while fixed-income products are projected to capture the fastest growth with an 11.34% CAGR through 2031.

- By investment strategy, passive offerings led with 93.20% revenue share of the North America ETF market in 2025, while active ETFs posted the highest 17.77% CAGR through 2031.

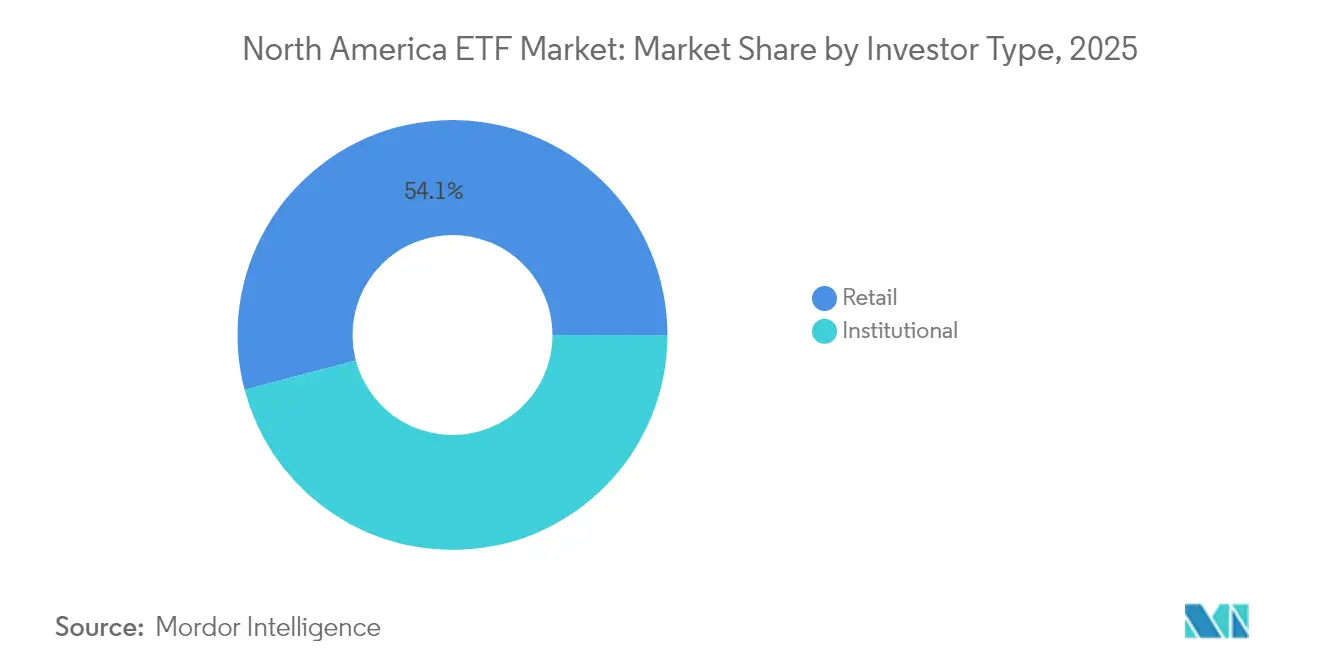

- By investor type, retail investors commanded 54.10% share of the North America ETF market size in 2025 and are expected to outpacing institutions at a 10.52% CAGR.

- By distribution channel, institutional channels held 35.70% of 2025 assets of the North America ETF market, while direct and digital retail platforms are projected to advance at 13.28% CAGR.

- By geography, the United States dominated with 91.70% North America ETF market share in 2025; Mexico is expected to record the strongest 12.53% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America ETF Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of passive investing among retail investors | +2.3% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Expansion of commission-free trading platforms | +1.8% | United States, Canada | Medium term (2-4 years) |

| Regulatory approval of innovative ETF structures | +1.2% | United States, spillover to Canada | Medium term (2-4 years) |

| Institutional portfolio rebalancing toward fixed-income ETFs | +0.9% | United States, Canada | Short term (≤ 2 years) |

| Rising demand for thematic and ESG ETFs | +1.1% | United States, Canada | Medium term (2-4 years) |

| Accelerated migration from mutual funds to ETFs | +1.7% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Commission-Free Trading Platforms

Zero-commission brokerage models lowered entry barriers, igniting a surge of small-ticket ETF purchases that collectively influence flows. Charles Schwab’s digital platform holds a large trove of ETF assets and now offers advanced portfolio optimizers once reserved for fee-based advisers. A 2025 Amundi poll found 77% of global retail investors—and 68% of those aged over 50—use digital interfaces to transact, demonstrating cross-generation adoption[1]Amundi, “2025 Amundi Retail Investor Survey,” amundi.com. Scale economics from these platforms reinforce fee competition and enhance liquidity, fueling the North America ETF market’s velocity.

Regulatory Approval of Innovative ETF Structures

The SEC’s 6c-11 rule unified the approval pathway, enabling faster product launches and catalytic growth in active ETFs. Non-transparent wrappers let portfolio managers hide daily holdings while preserving in-kind creation and redemption, protecting intellectual property, and sharpening tax efficiency. Since 2020, active ETFs have captured a disproportionate share of net inflows, attracting managers such as Fidelity and T. Rowe Price into the North America ETF market[2]U.S. Securities and Exchange Commission, “Rule 6c-11 Fact Sheet,” sec.gov. The smoother pipeline has shifted legacy mutual fund specialists toward converting entire sleeves into ETFs, broadening competitive depth.

Institutional Portfolio Rebalancing Toward Fixed-Income ETFs

Institutions now use fixed-income ETFs as tactical liquidity sleeves, citing smoother execution during the 2020 volatility episode. Cerulli Associates research indicates that a majority of pension and endowment professionals plan to raise ETF allocations for cash and risk management purposes. These flows have underpinned the growth of bond ETFs, reinforcing their systemic importance in the North America ETF market and improving price discovery within the broader credit ecosystem.

Accelerated Migration from Mutual Funds to Low-Cost ETFs

BlackRock documents reveal ETFs captured a major share of fixed-income flows during 2024, while U.S. mutual funds endured sustained outflows. Vanguard’s 2025 fee cut across 53 ETF classes intensified cost pressure, compelling rivals to follow. J.P. Morgan forecasts significant active ETF AUM growth this decade. This migration underscores the North America ETF market’s structural tailwind, though it also compresses issuer margins and elevates the need for scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Liquidity risks in niche ETFs during market stress events | -0.7% | United States, Canada | Medium term (2-4 years) |

| Potential regulatory tightening on leveraged and inverse ETFs | -0.5% | United States, Canada | Short term (≤ 2 years) |

| Competitive fee wars eroding profitability for ETF issuers | -0.8% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Concentration risk due to the dominance of top sponsors limiting market entry | -0.6% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Liquidity Risks in Niche ETFs During Market Stress Events

Specialty ETFs focused on thinly traded assets may trade at steep discounts when volatility spikes. 2020 offered a stress test in high-yield and emerging-market debt segments, where some funds deviated notably from NAV, according to BIS transaction studies[3]Bank for International Settlements, “ETF Liquidity under Stress,” bis.org. Regulators acknowledge ETFs’ role in secondary-market price discovery yet warn of potential fire-sale dynamics in narrow exposures. As the North America ETF market diversifies into concentrated themes, diligence around underlying depth and creation-unit mechanics remains vital, tempering adoption speed for exotic products.

Competitive Fee Wars Eroding Profitability

Fee compression pushed average revenue yields from 9.9 basis points in 2019 to 8.2 basis points in 2023, squeezing smaller sponsors. Vanguard’s February 2025 broad-based cuts sparked another wave of response pricing, illustrating scale advantages. Issuers now seek differentiation through technology, model portfolios, or portfolio construction tools. Persistently low fees can limit reinvestment in research and marketing, potentially slowing product development despite robust demand within the North America ETF market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Asset Class: Fixed-Income ETFs Outpace While Equity Retains Scale

Equity retained a 71.70% North America ETF market share in 2025, aided by the technology-heavy S&P 500’s resilience. Investors continue to favor broad market, sector, and factor tilts to harness concentrated U.S. mega-cap leadership. Commodity ETFs resurfaced as inflation hedges, real-estate ETFs lagged under higher rates, and alternative strategies—buffer or option-written funds—added defensive features. Collectively, these developments diversify the toolkit's breadth and deepen the North America ETF market’s resilience. Fixed-income products are projected to expand at an 11.34% CAGR between 2026 and 2031, the swiftest among major categories. Bond yields near decade highs and institutional liquidity needs fueled USD flows, propelling the segment to a larger slice of the North America ETF market. Treasury and investment-grade corporate exposures benefit as investors value transparent, all-day liquidity.

Equity inflows remained concentrated in market-cap-weighted vehicles, yet tactical rotations toward semiconductors and clean energy themes added incremental flow. Commodity ETFs saw renewed gold and energy interest during inflation upticks, underscoring multi-asset appetite within the North America ETF market. Real-estate exposures faced valuation pressure but attracted value-oriented investors. Alternative ETFs, such as PGIM’s January 2025 Buffer suite, offer defined outcomes that resonate with investors bracing for volatility shocks. The broader asset-class mosaic keeps the North America ETF market size on a dynamic growth track.

By Investment Strategy: Active ETFs Challenge the Passive Stronghold

Passive vehicles retained a dominant 93.20% North America ETF market share in 2025, propelled by their cost advantage and automatic inclusion in model portfolios. Yet active ETFs are advancing at an 17.77% CAGR, capturing mindshare among advisers seeking alpha and risk management. The North America ETF market size tied to active vehicles is slated to climb meaningfully as converted mutual fund assets migrate into wrapper-efficient formats. Managers highlight bond segments where active security selection can exploit pricing anomalies, creating fertile ground for performance dispersion.

Passive issuers battle on expense ratios and liquidity depth, leading to a commoditization trend in flagship broad-market offerings. Factor-based and smart-beta hybrids blur traditional labels, as do semi-transparent active designs integrating systematic tilts. Success in the North America ETF market increasingly hinges on content, analytics, and adviser partnerships rather than a strict active versus passive dichotomy.

By Investor Type: Retail Ascendancy Steepens Digital Adoption Curve

Retail assets formed 54.10% of the North America ETF market size in 2025 and are compounding at 10.52% through 2031. A large wealth transfer toward Gen-X and millennials amplifies ETF preference due to cost sensitivity and platform familiarity. Amundi research confirms older cohorts are also embracing online access, reflecting cross-demographic traction. Model portfolios, fractional shares, and AI-driven robo-allocations make ETFs the de facto wrapper for diversified exposure.

Institutions continue to deploy ETFs for tactical re-weightings, cash equitization, and overlay strategies. Cerulli Associates finds most pension managers intend to boost ETF usage over the next two years, citing operational efficiency. Convergence is visible as institutions adopt retail-style thematic ideas, while households apply factor filters once unique to quant desks. This blending further enlarges the addressable North America ETF market.

By Distribution Channel: Digital Platforms Rewrite the Sales Playbook

Institutional channels held 35.70% of the North America ETF market size in 2025, supported by consultant model endorsements and portfolio overlay mandates. Adviser and wealth-manager segments integrate ETFs within fee-based advice frameworks, driving balanced inflows. Banks and full-service brokers roll out white-label platforms such as Citi Velocity ETFs, slated for a 2025 launch, to retain client assets in-house. Multi-channel strategies ensure broad distribution coverage across the North America ETF market, mitigating any single-channel risk.

Direct-to-consumer portals and online brokerages are projected to grow at a 13.28% CAGR, translating user-experience improvements into tangible flows. Commission-free access, alongside embedded planning tools, entrenches ETFs within daily financial apps. Charles Schwab, Robinhood, and new banking entrants integrate curated ETF lineups, enhancing shelf visibility and reinforcing North America ETF market growth.

Geography Analysis

The United States commanded 91.70% North America ETF market share in 2025 and remains the global innovation hub. Record net inflows, boosted by the continued rotation from mutual funds, vaulted U.S. assets to fresh highs. Active fixed-income launches, cryptocurrency futures ETFs, and AI-centric thematic funds showcase the pace of evolution. Policy stability and deep secondary liquidity sustain a vibrant ecosystem that anchors the broader North America ETF market.

Canada’s ETF AUM experienced significant growth over the years, showcasing a notable increase in market size and investor interest. The market distinguishes itself through heavier active ETF penetration, which absorbed 42% of 2024 inflows. Early regulatory clarity allowed Canada to list the world’s first spot Bitcoin ETFs, putting the country at the forefront of crypto experimentation. The favourable framework attracts cross-border listings, expanding the North America ETF market size beyond U.S. borders.

Mexico, though a fraction of total assets, is the fastest-growing node. A 12.53% CAGR through 2031 reflects nearshoring-driven economic momentum and monetary easing that encouraged domestic equity participation. February 2025 tariff relief and a 50-basis-point rate cut propelled local ETFs like iShares MSCI Mexico (EWW) to notable gains. Limited fund variety today signals white-space opportunity, suggesting a broader spectrum ahead as the North America ETF market targets under-served South American investors.

Competitive Landscape

BlackRock (iShares), Vanguard, State Street (SPDR), Invesco, and Charles Schwab collectively dominate the market, showcasing a highly concentrated structure. Vanguard’s low-cost ethos steadily narrows the gap with BlackRock, aided by sustained royalties from passive flagship products. State Street leverages institutional bridges, yet has ceded relative share to new entrants. Recent mutual-fund-to-ETF conversions by Dimensional Fund Advisors and JPMorgan illustrate how legacy asset managers now challenge incumbents within the North America ETF market.

Strategic positioning has diversified. BlackRock invests heavily in its Aladdin risk platform and crypto ETF lineup. Vanguard leans on member-owned governance to reinvest in price leadership. State Street focuses on liquidity advantages in large-cap equity and sector baskets. Schwab expands advisory tech under the Schwab Intelligent Portfolios banner. Invesco and WisdomTree court thematic niches, while PGIM experiments with buffered outcomes. This breadth reflects an urgent race to escape pure-price competition as fee wars intensify.

Issuers increasingly form alliances with fintech start-ups and robo-advisers to widen distribution. White-label manufacturing from firms such as Exchange Traded Concepts lowers barriers for boutique sponsors, while Citi Velocity ETFs aims to accelerate active launches in 2025. Innovation in active fixed-income, ESG reporting tools, and portfolio analytics will shape the next phase of the North America ETF market, as scale alone no longer guarantees differentiation.

North America ETF Industry Leaders

BlackRock, Inc. (iShares)

Vanguard Group, Inc.

State Street Global Advisors (SPDR)

Invesco Ltd.

Charles Schwab Investment Management, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: VanEck introduced a Quantum ETF to capitalize on early gains in quantum computing.

- May 2025: CIBC launched the CCLO ETF, offering AAA-rated U.S. CLO exposure with currency hedging.

- February 2025: Vanguard cut fees across 53 ETF share classes, deepening cost competition.

- January 2025: PGIM rolled out Buffer ETF series with 12% and 20% downside levels at a 0.50% expense ratio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North American exchange-traded fund (ETF) market as the sum of assets under management held by all publicly listed ETFs domiciled in the United States, Canada, and Mexico, irrespective of asset class, structure, or replication style.

Exchange-traded notes, closed-end funds, and private pooled vehicles fall outside this boundary and are expressly excluded.

Segmentation Overview

- By Asset Class

- Equity ETFs

- Fixed-Income ETFs

- Commodity ETFs

- Currency ETFs

- Real-Estate ETFs

- Alternative ETFs

- By Investment Strategy

- Active

- Passive

- By Investor Type

- Retail

- Institutional

- By Distribution Channel

- Direct and Digital Retail Platforms

- Financial Advisors and Wealth Managers

- Institutional Channels

- Traditional Banks and Full-Service Brokers

- By Country

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts supplement desk work with semi-structured interviews and pulse surveys covering ETF issuers, authorized participants, wealth-management platforms, and custody banks across the United States and Canada. These discussions clarify hard-to-observe variables, net creation drivers, pipeline product counts, and retail advisory adoption rates that materially influence our sizing assumptions and scenario weights.

Desk Research

We begin with a structured scan of authoritative, open-access datasets such as Investment Company Institute fund statistics, Canadian ETF Association monthly dashboards, U.S. Federal Reserve Financial Accounts, and International Organization of Securities Commissions filings. Regulatory disclosures from the Securities and Exchange Commission, prospectus libraries, and audited 10-K statements supply issuer-level flows, fee schedules, and share-class conversions. Quantitative cues on trading velocity and bid-ask behavior are extracted through Dow Jones Factiva feed analysis, while D&B Hoovers provides cross-checks on promoter revenues. These and numerous additional public sources collectively build the reference spine for volumes, pricing, and historical baselines.

Market-Sizing & Forecasting

A blended top-down and bottom-up model anchors the 2025 baseline. Top-down reconstruction rolls national fund statistics, cross-border listing data, and asset-class penetration rates into a regional AUM pool, which is then stress-tested against sampled promoter roll-ups, bottom-up, and average spread-adjusted asset prices. Key model inputs include: (1) quarterly net inflow ratios, (2) equity-bond allocation shifts within multi-asset portfolios, (3) active-to-passive share migration, (4) fee compression trajectories, and (5) retail platform wallet share. Forecasts to 2030 deploy multivariate regression, linking those drivers to macro indicators like disposable income growth and policy-rate outlooks, with scenario buffers for market shocks. Data gaps, most often in Mexico's nascent segment, are bridged by triangulating custodial statistics with regional trading tape analytics before conservative scaling.

Data Validation & Update Cycle

Outputs pass a two-level peer review, variance screens versus independent flow trackers, and automated anomaly alerts. Reports refresh annually, and any event that shifts AUM by five percent or more triggers an interim recalibration so clients receive an up-to-date view.

Why Mordor's North America ETF Industry Size & Share Analysis Baseline Commands Reliability

Published estimates diverge because firms mix geographies, treat converted mutual funds differently, or apply disparate currency bases.

Key Gap Drivers, Scope: some publishers quote U.S. figures only, inflating or deflating totals when compared with a true tri-country view. Assumptions: others presume straight-line fee erosion or aggressive crypto-ETF adoption, whereas Mordor models elastic fee curves and scenario caps. Refresh cadence: several values still cite 2024 snapshots; our baseline incorporates Q2 2025 flows.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 11.82 T (2025) | Mordor Intelligence | - |

| USD 10.35 T (2024) | Regional Consultancy A | Excludes Canadian and Mexican listings; 2025 flows not captured |

| USD 11.83 T (2025) | Industry Database B | Treats synthetic ETNs as ETFs, inflating equities bucket |

| USD 7.07 T (2024) | Global Consultancy C | Uses issuer self-reported AUM only; omits secondary-market appreciation |

These comparisons show that Mordor's disciplined scope definition, timely data feed integration, and dual-track modelling deliver a balanced, transparent baseline that decision-makers can trace and reproduce with confidence.

Key Questions Answered in the Report

What is the current size of the North America ETF market?

The North America ETF market size stands at USD 12.92 trillion in 2026 and is projected to reach USD 20.13 trillion by 2031.

Which asset class is growing fastest within ETFs?

Fixed-income ETFs are expanding at an 11.34% CAGR as institutions deploy them for liquidity and rate-sensitive income.

How dominant are retail investors in North American ETFs?

Retail investors hold 54.10% of assets and are growing at a 10.52% CAGR, driven by commission-free digital platforms.

Why are active ETFs gaining ground?

Regulatory streamlining and semi-transparent structures enable managers to protect proprietary strategies while offering ETF cost and tax efficiencies, spurring an 17.77% CAGR for active products.

What is the major risk facing ETF issuers today?

Intensifying fee wars are compressing average revenue yields, pressuring profitability and prompting issuers to focus on product innovation and technology.

Page last updated on: