Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.69 Billion |

| Market Size (2031) | USD 13.21 Billion |

| Growth Rate (2026 - 2031) | 11.43% CAGR |

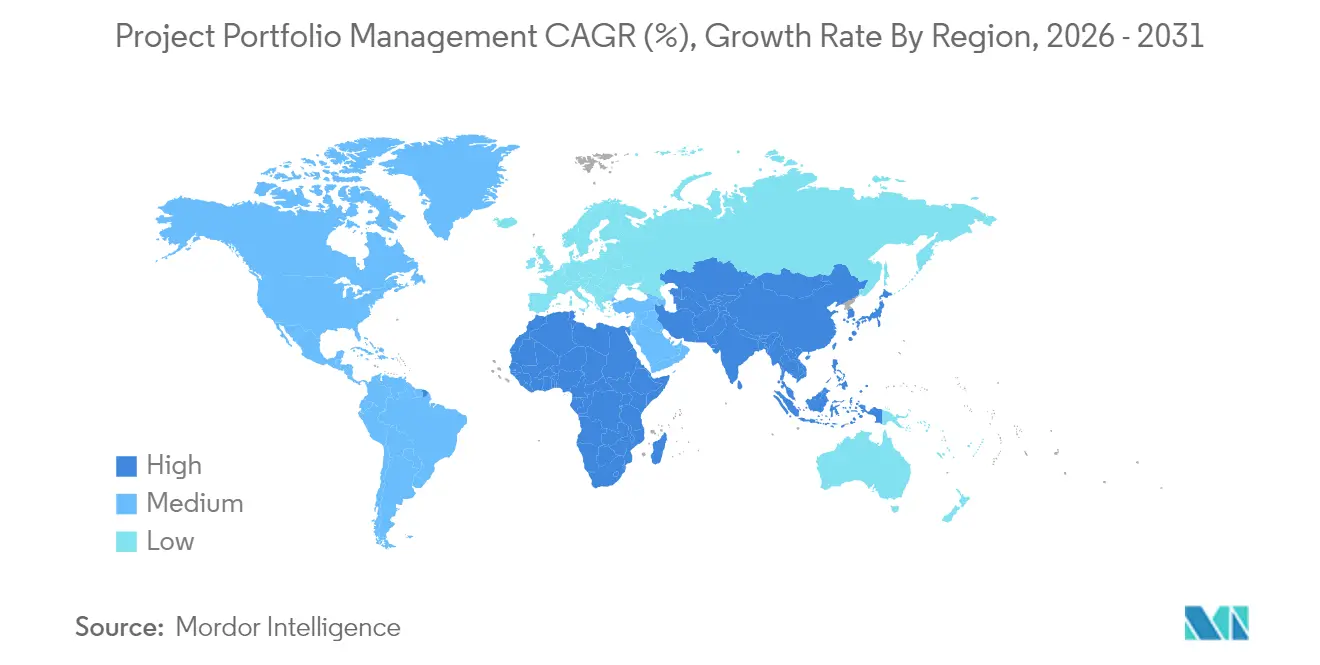

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Project Portfolio Management Market Analysis by Mordor Intelligence

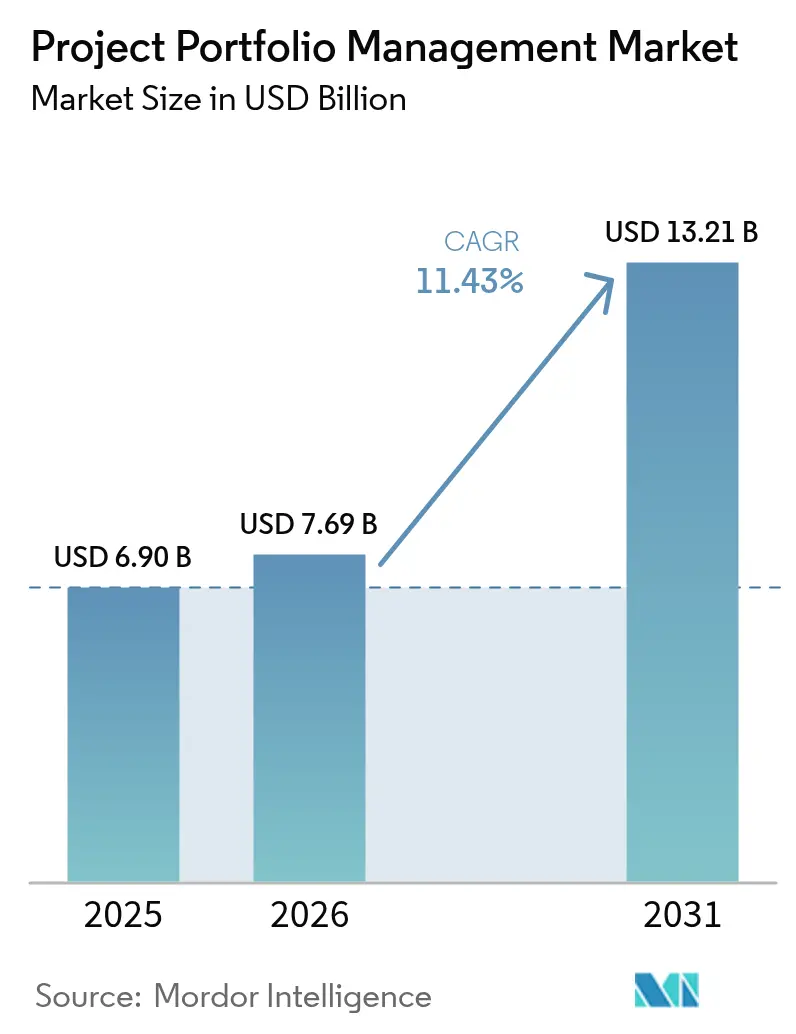

The project portfolio management market size is expected to grow from USD 6.90 billion in 2025 to USD 7.69 billion in 2026 and is forecast to reach USD 13.21 billion by 2031 at 11.43% CAGR over 2026-2031. Demand accelerates as hybrid work norms, AI-enabled forecasting, and stricter governance requirements make traditional point tools inadequate for multi-cloud, cross-functional programs. Organizations now treat project portfolio management platforms as strategic infrastructure that unifies financial governance with ESG-aligned capital deployment, sharpening competitive differentiation and enhancing resilience. Cloud deployment dominates because subscription pricing speeds time-to-value, while embedded analytics surfaces real-time insights that reduce budget overruns and resource idle time. Consolidation among vendors—backed by private-equity capital—signals confidence in long-term growth and raises barriers to entry through broader functionality, deeper integrations, and expanded geographic reach.

Key Report Takeaways

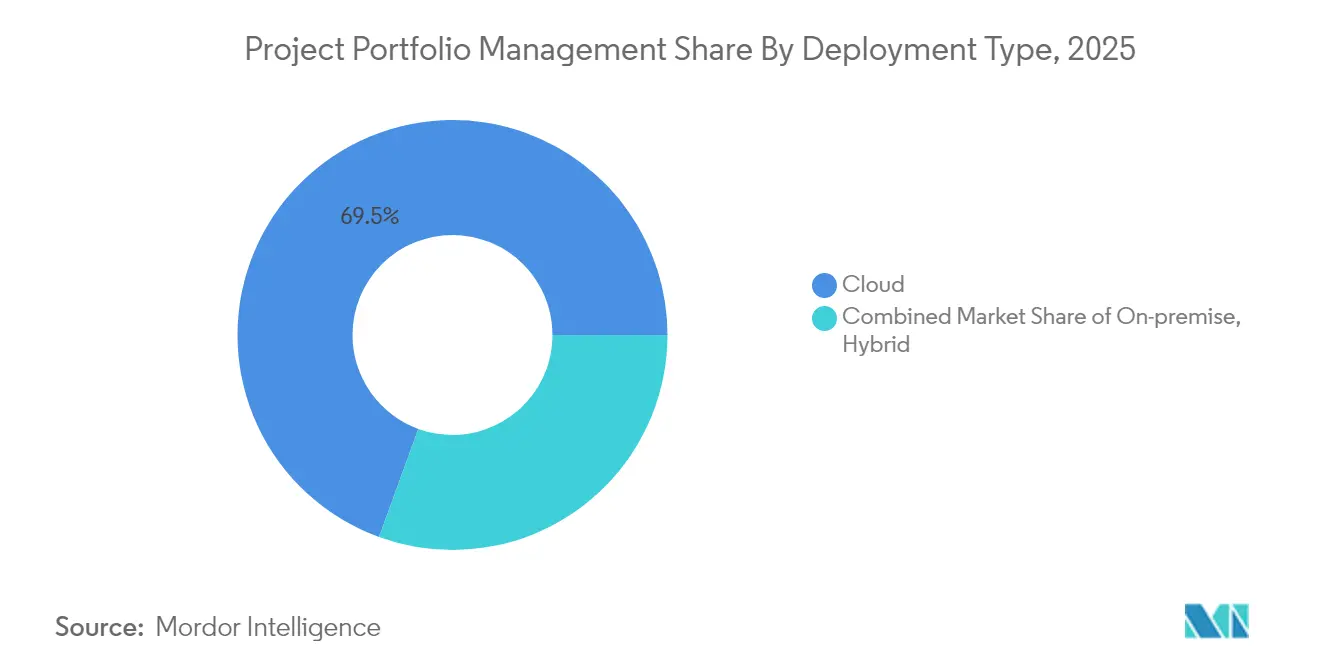

- By deployment type, cloud solutions held 69.45% of 2025 revenue while expanding at a 16.85% CAGR through 2031.

- By component, solutions accounted for 68.40% of 2025 revenue; services represent the fastest-growing component at a 11.74% CAGR to 2031.

- By organization size, large enterprises commanded 60.30% of 2025 spending, whereas SMEs are set to grow at a 12.60% CAGR to 2031.

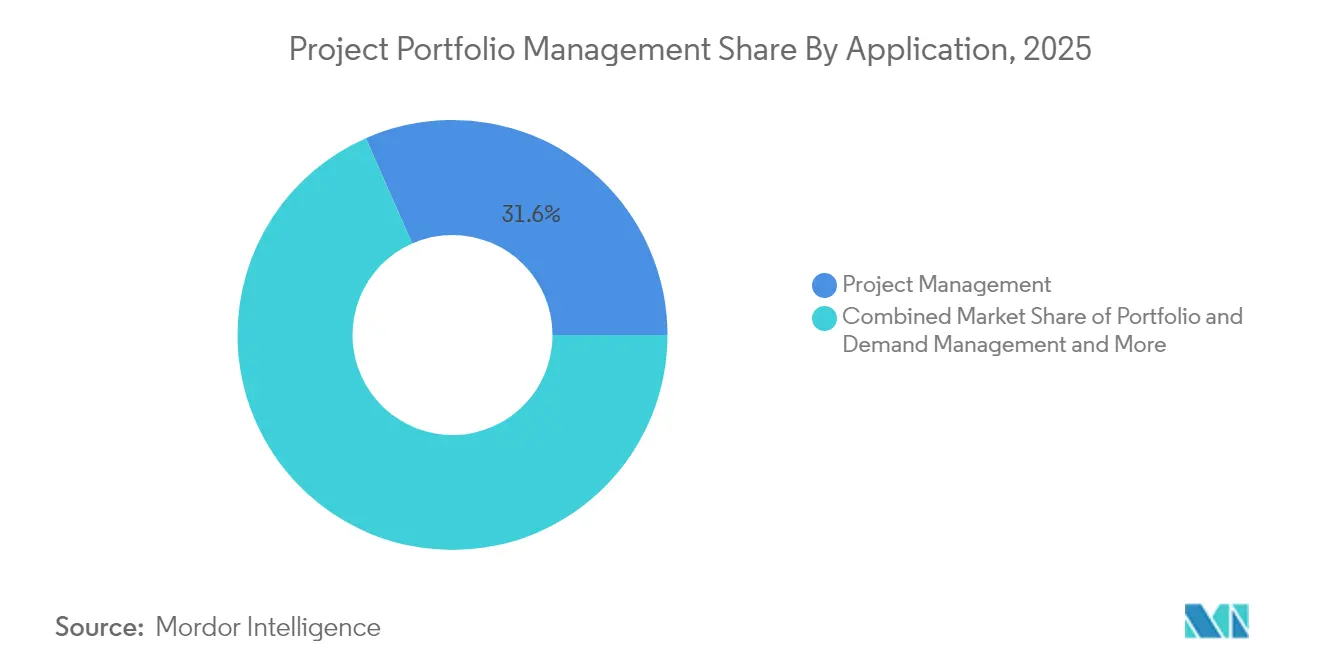

- By application, project management captured 31.60% of the 2025 project portfolio management market share, while resource and capacity management is poised for a 14.78% CAGR.

- By end-user vertical, IT and telecom captured 35.60% of 2025, healthcare & life sciences posts the fastest 13.58% CAGR, fueled by clinical-trial digitization, FDA 21 CFR Part 11 validation, and telehealth infrastructure rollouts.

- By geography, North America led with 39.40% of 2025 revenue; APAC is forecast to rise at an 10.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Project Portfolio Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid/remote-work acceleration requires centralized resource visibility | +2.1% | Global; strongest in North America and Europe | Short term (≤ 2 years) |

| Rise of cloud-native, AI-augmented PPM suites | +2.8% | Global; led by North America, expanding in APAC | Medium term (2-4 years) |

| Integration of Agile & DevOps with strategic portfolio planning | +1.9% | North America and Europe core; spill-over to APAC | Medium term (2-4 years) |

| Demand for real-time project financial governance amid cost inflation | +1.7% | Global; acute in developed markets | Short term (≤ 2 years) |

| Vertical-specific compliance boosting niche PPM uptake | +1.4% | Regulated markets globally, concentrated in NA & EU | Long term (≥ 4 years) |

| ESG-driven capital-allocation scrutiny | +1.3% | Europe leading; NA following; emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hybrid/Remote-Work Acceleration Requires Centralized Resource Visibility

Distributed work now anchors corporate operating models. Seventy-nine percent of knowledge workers collaborate across time zones, forcing enterprises to seek real-time dashboards that surface utilization gaps, predict bottlenecks, and maintain accountability. Traditional Gantt-centric oversight cannot track asynchronous workloads, so adoption of enterprise-wide resource engines is surging. These platforms support instant cross-portfolio re-prioritization, enabling managers to redeploy scarce skills without disrupting delivery commitments. By creating a single source of truth, organizations both improve productivity and de-risk regulatory audits that demand transparent labor reporting.

Rise of Cloud-Native, AI-Augmented PPM Suites

Cloud implementations provision in weeks rather than quarters and eliminate capital hardware outlays, generating 40-80% cost savings while releasing IT staff for higher-value tasks [1]Oracle, “Cloud PPM: Everything You Need to Know,” cdp-inc.com . Embedded machine-learning models predict risk, auto-schedule tasks, and recommend resource swaps, lifting on-time delivery rates and sharpening strategic alignment. Twenty-one percent of project managers already use AI frequently, and 82% of executives expect material operational impact within five years [2]Project Management Institute, “Preparing Project Managers for an AI-Driven Future,” pmi.org . As decision velocity becomes a board-level mandate, AI-enabled portfolio optimization shifts PPM from retrospective reporting to forward-looking orchestration.

Integration of Agile & DevOps with Strategic Portfolio Planning

Enterprises blend agile sprints with long-horizon business roadmaps, making bidirectional data flows between delivery tools and governance layers indispensable. Modern platforms plug into Jira, Azure DevOps, and Microsoft Planner to fuse backlog status with financial and capacity views. Unified telemetry cuts manual reconciliation by 50% and elevates visibility for C-suite stakeholders, ensuring iterative releases stay tethered to enterprise value streams.

Demand for Real-Time Project Financial Governance Amid Cost Inflation

Cost volatility requires continuous budget validation rather than quarter-close snapshots. Advanced PPM suites ingest live price feeds, model currency swings, and recalibrate contingencies, enabling proactive mitigation of material spikes. Automated variance alerts and multi-currency ledgers uphold fiscal discipline across global portfolios, supporting CFO mandates for leaner capital allocation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shadow-IT and data-sovereignty risks in multi-cloud PPM roll-outs | -2.10% | Europe, APAC, regulated industries globally | Short to medium term (1–3 yrs) |

| Long pay-back periods in the SME segment | -1.70% | Global; strongest impact in emerging markets | Medium term (2–4 yrs) |

| Vendor-lock-in concerns with single-stack ecosystems | -1.50% | Global | Medium term (2–4 yrs) |

| Skills shortage in value-realisation offices (VROs) | -1.20% | North America, Europe, Asia-Pacific | Medium term (2–4 yrs) |

| Source: Mordor Intelligence | |||

Shadow-IT & Data-Sovereignty Risks in Multi-Cloud Roll-outs

As business units spin up cloud services independently, duplicate PPM instances fragment data and complicate governance. Misconfigured permissions enlarge cyber-attack surfaces, while regional privacy statutes limit cross-border data flows. Enterprises must institute strict provisioning policies and invest in unified identity management before reaping the full benefits of federated architectures.

Long Pay-Back Periods in SME Segment

PPM license fees of USD 60-100 per user monthly and implementation costs reaching USD 100,000 stretch SME cash flows. With smaller project volumes, breakeven often arrives after 18-36 months. Vendors that unbundle advanced modules, offer tiered pricing, and embed guided onboarding lower the adoption hurdle yet still face buyer hesitation when near-term ROI is unclear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Dominance Accelerates

Cloud deployments accounted for 69.45% of 2025 revenue, generating the largest slice of the project portfolio management market size and expanding at a 16.85% CAGR. Enterprises favor web-based access, elastic capacity, and automatic upgrades that eliminate lengthy patch cycles. Hybrid models serve organizations needing on-premise data segregation while tapping cloud elasticity for collaboration. As multi-tenant architectures mature, total cost of ownership declines, fueling further migration from legacy instances. Continuous security updates from hyperscale providers mitigate vulnerability exposure, a persuasive argument for boards seeking stronger cyber postures amid rising breach costs.

On-premise installations retain footholds in defense, government, and heavily regulated finance where data residency or air-gapped environments trump modernization speed. Even here, containerization allows selective workloads to move outward over time, signaling that pure on-premise footprints will contract. By 2031, analysts expect cloud to underpin the majority of strategic program governance, positioning SaaS vendors as natural consolidators of adjacent analytics and automation tools.

By Component: Solutions Lead, Services Accelerate

Solutions contributed 68.40% of 2025 spending, underscoring buyer preference for integrated suites that bundle scheduling, resource, and financial controls into a single workspace. These platforms reduce swivel-chair inefficiencies and standardize reporting semantics across business units. As AI modules embed deeper into core code, solutions revenue will remain the anchor of the project portfolio management market.

Services, however, are the growth catalyst at a 11.74% CAGR as enterprises seek advisory support for process redesign, system integration, and change management. Advanced implementations now involve mapping value streams, configuring predictive algorithms, and aligning dashboards with ESG frameworks—tasks that demand specialized consultants. Managed-service agreements extend vendor influence post-go-live, yielding recurring revenue while ensuring the client extracts full transformational value.

By Organization Size: Large Enterprises Dominate, SMEs Show Promise

Large enterprises drove 60.30% of 2025 outlays and continue to rely on PPM to coordinate hundreds of concurrent initiatives, optimize scarce expert skills, and meet stringent audit requirements. Their global footprints amplify the need for unified governance to support acquisitions, product launches, and regulatory filings across jurisdictions. The project portfolio management market size for large enterprises is forecast to keep pace with GDP expansion, but growth will plateau as penetration nears saturation.

SMEs deliver the highest incremental CAGR at 12.60% as subscription pricing, low-code configurations, and templated best practices democratize sophisticated oversight. Nonetheless, long pay-back periods and limited change-management capacity remain barriers. Vendors courting this cohort emphasize quick-start accelerators, freemium trials, and embedded learning paths to compress time-to-value and justify the investment calculus.

By Application: Project Management Leads, Resource Management Surges

Project management modules held 31.60% of 2025 revenue, reflecting their role as the entry point for buyers. They standardize task sequencing, milestone tracking, and status visibility—capabilities no portfolio initiative can forgo. Yet resource & capacity management is the star performer with a 14.78% CAGR, propelled by chronic skill shortages and the shift to outcome-based planning. This segment alone will add a significant portion to the project portfolio management market size by 2031 as organizations pivot from static headcount plans to dynamic, skill-centric deployment.

Demand and portfolio management extensions mature adoption paths by introducing scenario modeling and investment scoring. Financial and risk management add defensibility in inflationary climates, where every capital request competes for scarce budget. Together, these applications transform PPM from a scheduling dashboard into a corporate capital allocator.

By End-User Vertical: IT & Telecom Leads, Healthcare Accelerates

IT & telecom captured 35.60% of 2025 revenue and uses PPM to synchronize digital transformation waves, infrastructure upgrades, and DevOps pipelines that span hybrid-cloud estates. Continuous delivery cadences make real-time governance indispensable, driving deeper integrations with code repositories and monitoring stacks.

Healthcare & life sciences posts the fastest 13.58% CAGR, fueled by clinical-trial digitization, FDA 21 CFR Part 11 validation, and telehealth infrastructure rollouts. Compliance mandates dovetail with patient-safety imperatives, making audit-ready documentation and risk logs central to funding decisions. Manufacturing, BFSI, construction, and public sector each contribute diversified use cases ranging from predictive maintenance scheduling to budget oversight of infrastructure megaprojects—underscoring the broadening relevance of the project portfolio management market.

Geography Analysis

North America generated 39.40% of 2025 revenue, underpinned by mature cloud ecosystems, robust capital budgets, and a concentration of leading vendors. Board mandates for AI-driven insight and ESG reporting fuel steady license renewals and module add-ons. Government incentives for digital resilience further support adoption across critical infrastructure, healthcare, and defense.

Europe shows healthy expansion as manufacturers and utilities modernize operations to meet Green Deal objectives and granular data-sovereignty statutes. Cloud adoption proceeds under strict privacy frameworks, prompting demand for platforms offering regional hosting options and in-product compliance accelerators. Health-system investments in e-hospital frameworks and cross-border research consortia sustain momentum.

APAC is the fastest-growing region at an 10.95% CAGR, reflecting massive infrastructure spending, mobile-first work cultures, and intensifying competition for digital talent. Chinese and Indian enterprises scale PPM suites to orchestrate multiregional programs and mitigate supply-chain volatility. SME digitalization incentives in Southeast Asia also unlock green-field opportunities, making the region pivotal to global expansion strategies.

Competitive Landscape

The market remains moderately consolidated, with technology majors leveraging integrated stacks while specialty vendors deepen vertical functionality. Microsoft and Oracle cross-sell PPM into ERP and collaboration clouds, creating switching-cost moats. SAP embeds portfolio governance inside S/4HANA workflows, knitting together financial and operational data streams.

Planview’s February 2025 acquisition of Sciforma broadens enterprise reach and enriches agile and strategic planning modules, illustrating a platform roll-up strategy aimed at midmarket expansion [3]Tracxn, “Sciforma – 2025 Company Profile,” tracxn.com . Smartsheet’s USD 8.4 billion privatization by Vista Equity Partners and Blackstone in September 2024 supplies capital for R&D acceleration and underscores private-equity conviction in double-digit growth.

Competitive advantage increasingly hinges on AI depth, ecosystem extensibility, and compliance toolkits. Vendors invest in natural-language risk queries, resource heat-maps, and ESG scorecards to secure renewals and expand average contract value. Partnerships with systems integrators and hyperscalers accelerate global roll-outs, especially in highly regulated or multilingual environments.

Project Portfolio Management Industry Leaders

Oracle Corporation

Microsoft Corporation

SAP SE

ServiceNow Inc.

Broadcom (CA PPM/Clarity)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Planview completed its acquisition of Sciforma, enhancing enterprise portfolio functionality and expanding midmarket coverage

- September 2024: Smartsheet entered a USD 8.4 billion take-private agreement with Vista Equity Partners and Blackstone, reflecting substantial investor confidence

- June 2024: Celoxis introduced advanced ROI analytics and real-time dashboards to sharpen project prioritization

- March 2024: TechTarget reported that 93% of project managers achieved positive ROI from AI-enabled tools, signaling rapid mainstreaming of intelligent PPM

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Project Portfolio Management (PPM) market as the global revenue generated by purpose-built software suites and related cloud subscriptions that help enterprises prioritize, budget, schedule, and track multiple projects within a unified portfolio. PPM tools cover demand intake, resource and capacity planning, financial governance, risk alignment, analytics, and workflow orchestration across IT, engineering, construction, and other project-driven domains.

Scope exclusion: Stand-alone task boards, generic collaboration apps, and one-time professional consulting fees sit outside the modeled market scope.

Segmentation Overview

- By Deployment Type

- Cloud

- On-premise

- Hybrid

- By Component

- Solutions

- Services

- By Organization Size

- Large Enterprises

- Small and Mid-sized Enterprises (SMEs)

- By Application

- Project Management

- Portfolio and Demand Management

- Resource and Capacity Management

- Financial and Risk Management

- Others (Collaboration, Reporting)

- By End-user Vertical

- IT and Telecom

- Healthcare and Life Sciences

- Manufacturing

- Construction and Engineering

- Retail and Consumer Goods

- BFSI

- Government and Public Sector

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

- Asia

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of APAC

- Middle East and Africa

- Middle East

- GCC

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed PPM product managers, enterprise PMO heads, and implementation partners spanning North America, Europe, Asia Pacific, and the Middle East. Discussions focused on seat deployment ratios, typical renewal discounts, cloud migration timelines, and planned budget shifts, allowing us to challenge desk findings, fill regional gaps, and align scenario drivers with on-ground sentiment.

Desk Research

We began with reputable public sources such as the US Bureau of Labor Statistics technology investment tables, Eurostat's ICT enterprise surveys, and UNCTAD digital-economy indicators, which outline the base pool of software spending across regions. White papers from the Project Management Institute and position papers by the International Project Management Association shed light on certified practitioner growth and evolving portfolio governance practices. Company 10-Ks, investor decks, and procurement portals provided average selling prices and seat counts, while patent filings reviewed through Questel highlighted emerging AI-driven functionality that influences future adoption curves. Paid intelligence from D&B Hoovers and Dow Jones Factiva helped size vendor revenue splits and regional mix. The sources listed are illustrative; many additional documents informed data gathering, validation, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction starts with enterprise software outlays by region, which are then filtered through PPM penetration rates derived from our primary interviews. Select bottom-up checks, such as sampled vendor license counts multiplied by blended annual subscription prices, anchor totals and expose outliers. Key variables include cloud share of new deals, average seats per 1,000 employees, certified PM workforce growth, remote-worker percentage, and median software price erosion. Multivariate regression links these drivers to historical spend so we can forecast to 2030 under base, bullish, and adverse scenarios, with missing bottom-up datapoints bridged through nearest-neighbor proxies and channel checks.

Data Validation & Update Cycle

Outputs pass a multi-step analyst review that flags variance versus external spending benchmarks, quarterly earnings, and macro signals. Before sign-off, anomalies are re-queried with respondents. We refresh every twelve months, issuing interim revisions when events such as major vendor mergers or regulatory shifts materially move the baseline.

Why Mordor's Project Portfolio Management Baseline Commands Reliability

Published values often diverge because firms pick different component stacks, regional mixes, and refresh cadences.

Key gap drivers include exclusion of services revenue by some sources, varied treatment of SME licenses, and the use of straight-line CAGR extrapolation where Mordor applies driver-based modeling and an annual primary research refresh.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.90 bn (2025) | Mordor Intelligence | - |

| USD 6.31 bn (2025) | Global Consultancy A | Narrower component coverage and limited SME interviews |

| USD 6.54 bn (2025) | Industry Research Provider B | Excludes professional services and relies on historical CAGR roll-forward |

These comparisons show that, by anchoring numbers to clearly traced variables and freshly validated assumptions, Mordor delivers a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

How are SMEs affecting market dynamics?

SMEs grow at a 12.60% CAGR as subscription pricing and low-code platforms lower barriers, though long pay-back periods remain a restraint.

What is the projected value of the project portfolio management market by 2031?

It is expected to reach USD 13.21 billion, growing at an 11.43% CAGR.

Which deployment model is gaining the most traction?

Cloud solutions dominate with 69.45% of 2025 revenue and are expanding at a 16.85% CAGR.

Why are AI-enabled features critical for PPM adoption?

AI improves schedule accuracy, predicts risks, and boosts ROI; 93% of project managers report positive returns from AI tools.

Which vertical shows the fastest growth?

Healthcare and life sciences leads with a 13.58% CAGR due to stringent compliance and digitization of clinical processes.

Page last updated on: