Global Axial Spondyloarthritis (axSpA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

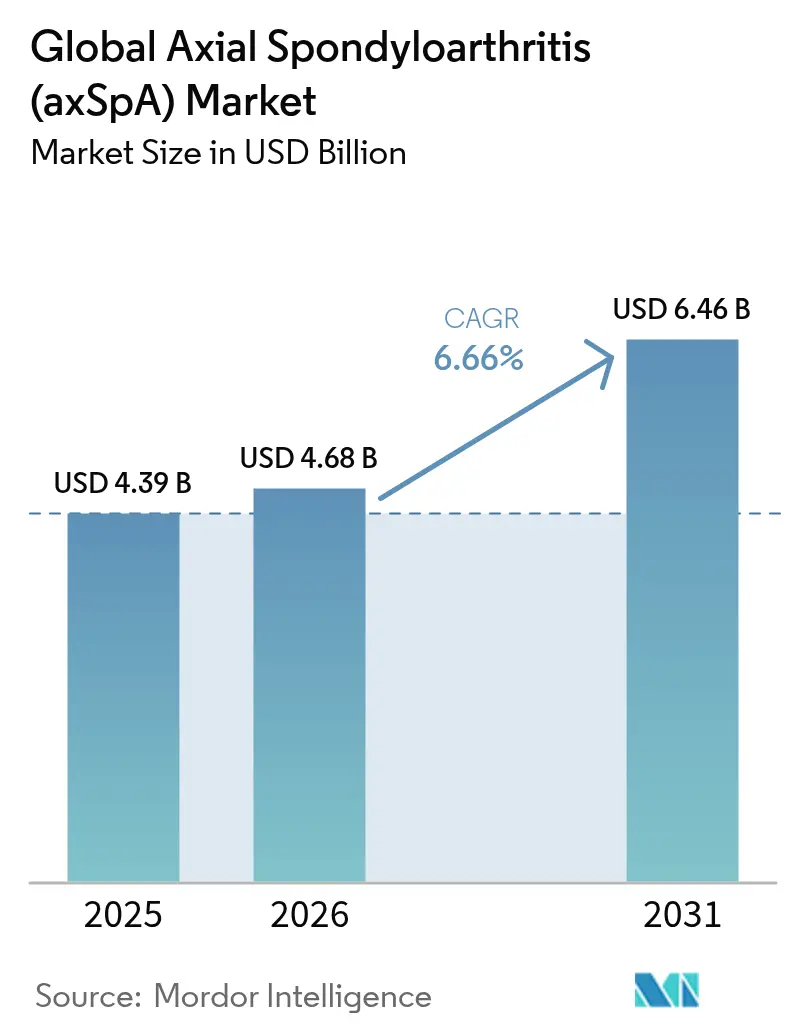

| Market Size (2026) | USD 4.68 Billion |

| Market Size (2031) | USD 6.46 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Axial Spondyloarthritis (axSpA) Market Analysis by Mordor Intelligence

The axial spondyloarthritis market size was valued at USD 4.39 billion in 2025 and estimated to grow from USD 4.68 billion in 2026 to reach USD 6.46 billion by 2031, at a CAGR of 6.66% during the forecast period (2026-2031). Earlier diagnosis through MRI advocacy, the entry of dual IL-17A/IL-17F and JAK inhibitors, and broader patient‐assistance programs are expanding the axial spondyloarthritis market size and widening treatment access[1]S. Ramiro, “ASAS-EULAR Recommendations for the Management of Axial Spondyloarthritis,” Annals of the Rheumatic Diseases, ard.bmj.com. Uptake of subcutaneous biologics remains strong, yet oral JAK inhibitors are winning share as convenience considerations grow. Biosimilar adalimumab variants continue to reset formularies, reinforcing price competition[2]Express Scripts, “2024 Formulary Updates—Preferred Biosimilar Adalimumab Options,” express-scripts.com. Geographically, North America retains leadership, but Asia-Pacific is the fastest‐growing arena as healthcare infrastructure matures and biologic reimbursement widens[3]J. Blackstone, “Real-World Adherence Outcomes with Adalimumab Biosimilars,” Center for Biosimilars, centerforbiosimilars.com.

Key Report Takeaways

- By drug class, disease-modifying antirheumatic drugs (DMARDs) held 49.02% of axial spondyloarthritis market share in 2025; the same segment is expanding at a 7.11% CAGR through 2031.

- By route of administration, subcutaneous formulations led with 45.82% of the axial spondyloarthritis market size in 2025, while oral therapies are predicted to grow at 7.28% CAGR.

- By distribution channel, hospital pharmacies accounted for 43.11% revenue share in 2025; online pharmacies post the quickest growth at 7.22% CAGR.

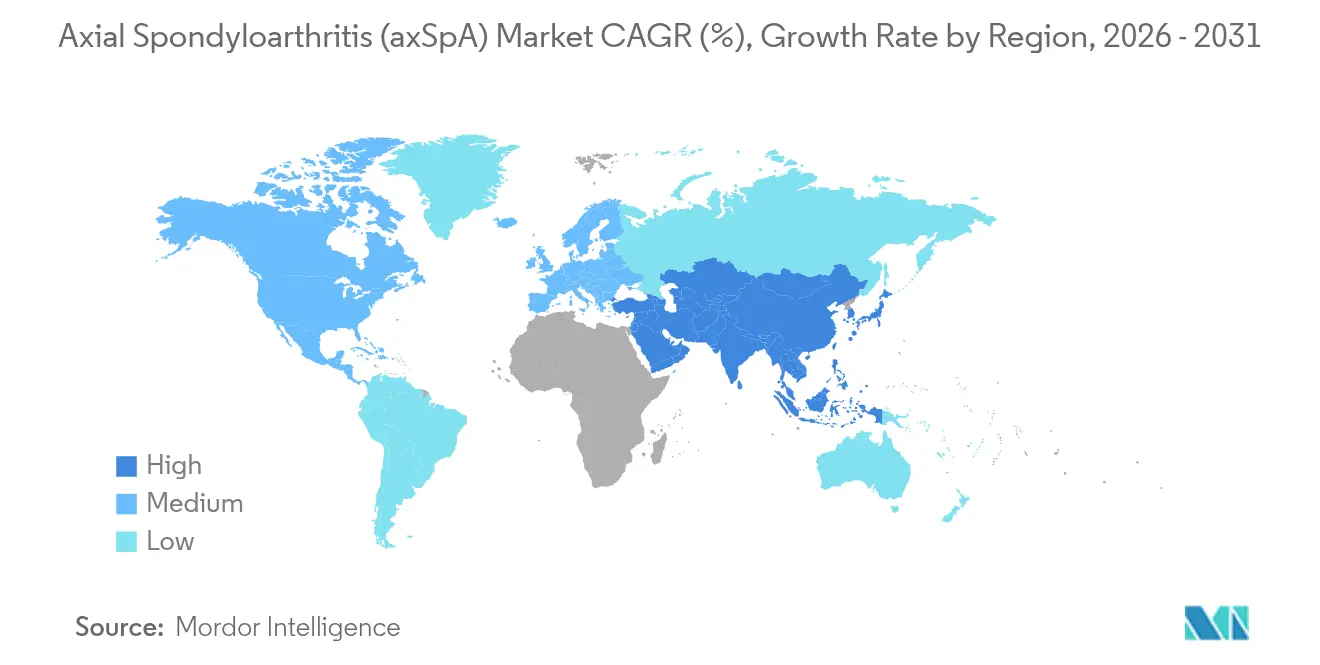

- By geography, North America commanded 39.78% market share in 2025; Asia-Pacific is forecast to grow at 7.19% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Axial Spondyloarthritis (axSpA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diagnosis rates due to MRI advocacy programs | +1.2% | Global, with strongest impact in North America & EU | Medium term (2-4 years) |

| Rapid uptake of IL-17 & JAK inhibitors in treatment guidelines | +1.8% | Global, led by developed markets | Short term (≤ 2 years) |

| Expansion of biosimilar TNF-α inhibitors improves affordability | +0.9% | Global, particularly emerging markets | Long term (≥ 4 years) |

| Growing employer-sponsored specialty pharmacy benefits | +0.7% | North America primary, expanding to EU | Medium term (2-4 years) |

| AI-assisted MRI algorithms enabling earlier detection | +0.6% | Developed markets initially, global expansion | Long term (≥ 4 years) |

| Microbiome-targeted adjuvant therapies showing disease-modifying potential | +0.3% | Research centers globally, clinical translation pending | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising diagnosis rates due to MRI advocacy programs

Updated ASAS classification and insurance alignment have cut diagnostic delay from more than eight years to roughly three in centers that mandate MRI for early back-pain evaluation. Enhanced Dixon sequencing now reaches 96% diagnostic accuracy, unlocking larger treatable populations and fueling the axial spondyloarthritis market. Early identification also prevents structural damage and supports long-term work productivity, strengthening payers’ cost-saving arguments.

Rapid uptake of IL-17 & JAK inhibitors in treatment guidelines

The 2022 ASAS/EULAR recommendations promoted IL-17 and JAK inhibitors once NSAIDs and at least one TNF blocker fail. Bimekizumab, approved in 2024, delivered ASAS40 responses above 44%, setting a new efficacy bar and providing the first dual cytokine blockade option. Upadacitinib and other JAK agents broaden oral alternatives despite cardiovascular warnings, enlarging the axial spondyloarthritis market as second-line therapy is standardized.

Expansion of biosimilar TNF-α inhibitors improves affordability

Formulary switches by pharmacy benefit managers to prefer biosimilars such as Cyltezo and Hyrimoz have trimmed annual patient costs by USD 3,500, sparking wider biologic initiation in cost-sensitive regions. Emerging markets gain the most, seeing 30-50% price decreases that lift biologic penetration and further expand the axial spondyloarthritis market.

Growing employer-sponsored specialty pharmacy benefits

Employers link early biologic use with reduced absenteeism, so plans now bundle specialty coverage, financial assistance, and adherence coaching. Programs like COSENTYX Connect ease copays and injection training, raising treatment persistence and propelling revenue growth, chiefly in North America.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently high treatment costs of novel biologics | -1.4% | Global, most pronounced in emerging markets | Long term (≥ 4 years) |

| Limited long-term safety data for JAK inhibitors | -0.8% | Global, regulatory focus in developed markets | Medium term (2-4 years) |

| Access inequality in low-income regions for imaging & biologics | -0.6% | Emerging markets, rural areas in developed countries | Long term (≥ 4 years) |

| Cold-chain logistics bottlenecks for biologic distribution | -0.4% | Global, particularly challenging in tropical regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistently high treatment costs of novel biologics

Bimekizumab’s USD 8,281 per injection illustrates ongoing affordability barriers despite biosimilar rivalry. Total annual therapy outlays hover near USD 10,000, straining payer budgets and limiting uptake in lower-income settings. Added monitoring, administration overhead, and adverse-event management inflate economic burden and temper the axial spondyloarthritis market’s fullest potential.

Limited long-term safety data for JAK inhibitors

Cardiovascular and malignancy signals from the ORAL Surveillance trial triggered FDA and EMA warnings that confine JAK use to TNF failures, encourage older-patient caution, and mandate extra monitoring. Such guardrails curb prescriber enthusiasm and slow axial spondyloarthritis market expansion for orally delivered options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Non-radiographic Momentum Builds

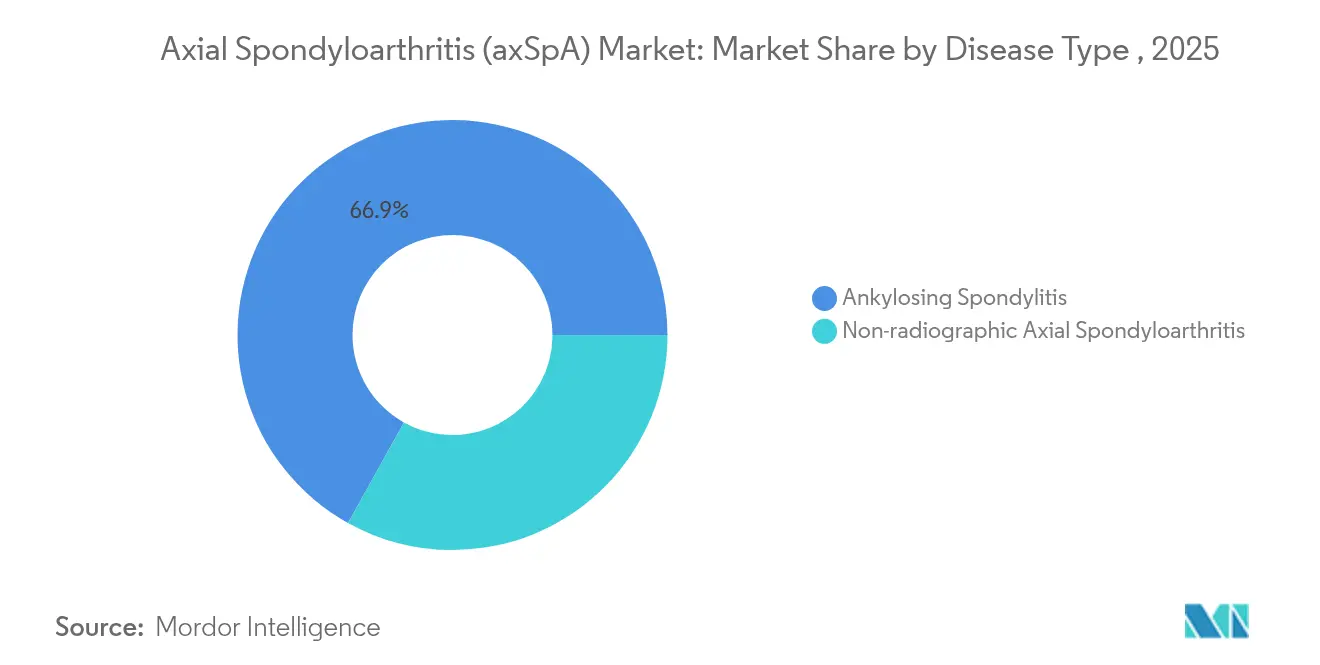

Ankylosing spondylitis led revenue with 66.92% share in 2025, yet non-radiographic presentations are rising at a 7.69% CAGR to 2031. Early MRI adoption now picks up inflammatory lesions before structural damage, swelling the non-radiographic patient base inside the axial spondyloarthritis market. Clinical trials report similar biologic response rates for both phenotypes, validating aggressive treatment earlier in the disease course. Inter-regional contrasts are pronounced; Asian cohorts show just 14.4% non-radiographic incidence, half that of Western peers, reflecting divergent genetics and care accessibility. Harmonized nomenclature and ASAS criteria continue to raise awareness, sustaining double-digit gains for diagnostically driven volumes and enlarging axial spondyloarthritis market opportunity across all drug classes.

Elevated research interest centers on biomarkers that predict radiographic conversion, aiming to target therapy before irreversible fusion. Commercial upside lies in companion diagnostics that would differentiate aggressiveness, potentially justifying premium pricing. Education campaigns by patient groups further speed recognition, while tele-rheumatology may shrink urban-rural gaps, reinforcing structural tailwinds that support prolonged segment expansion within the axial spondyloarthritis market.

By Drug Class: DMARD Innovation Takes Center Stage

DMARDs represented 49.02% of global revenue in 2025 and are set for 7.11% CAGR, propelled by biologic and targeted synthetic launches. Dual IL-17 inhibition through bimekizumab augments this category, offering superior ASAS40 outcomes. JAK agents deepen flexibility, though monitoring demands persist. The axial spondyloarthritis market size for DMARDs is forecast to climb steadily as real-world data strengthen payer confidence and formulary positions broaden.

NSAIDs and glucocorticoids remain crucial for symptom flare control but face stagnant growth, mainly due to gastrointestinal and bone-density risk profiles. Novel entrants like NLRX1 agonists and microbiome modulators promise to diversify mechanisms, ensuring continuous pipeline replenishment. Observational registries will likely influence guideline placement, particularly if newer molecules prove durable with clean long-term safety signatures, thus safeguarding DMARD dominance inside the axial spondyloarthritis market.

By Route of Administration: Oral Therapies Gain Ground

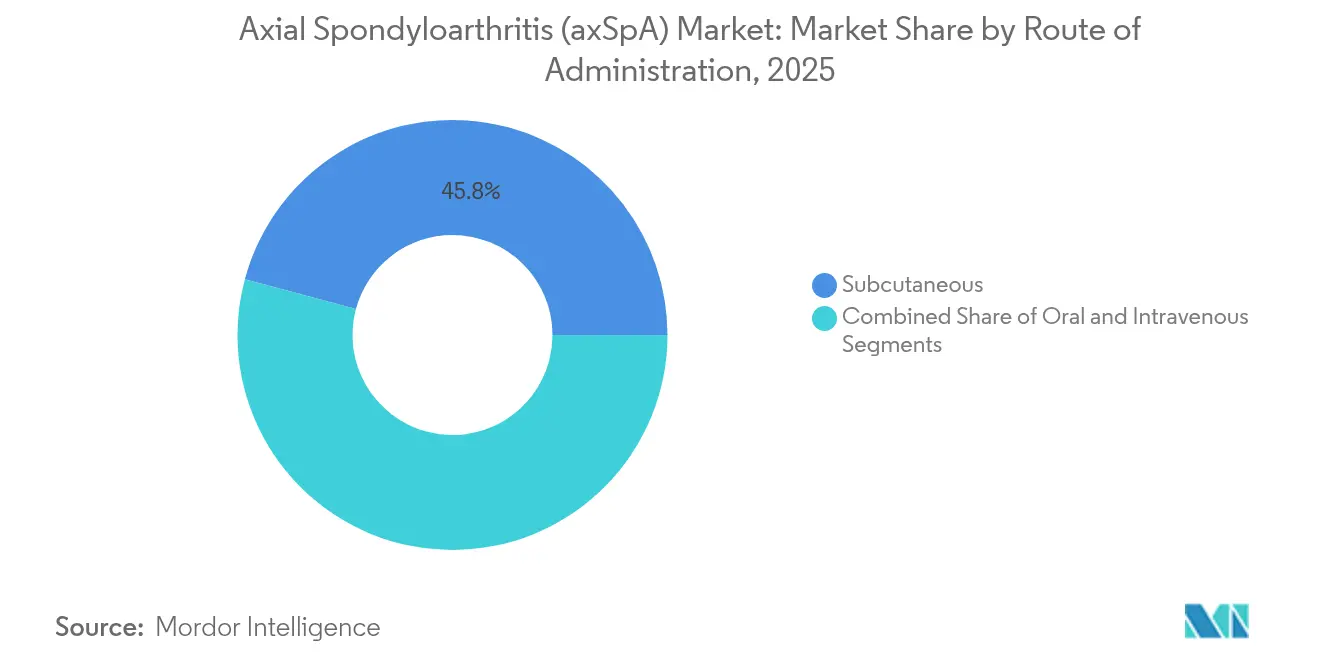

Subcutaneous injections captured 45.82% revenue in 2025 on the back of established TNF and IL-17 agents. Oral formulations, however, enjoy a 7.28% CAGR as young, working-age patients gravitate toward pill regimens that simplify travel and lifestyle management. Payors welcome the lower administration costs, nurturing market shift toward tablets within the axial spondyloarthritis market.

Intravenous delivery holds a narrower place for high-severity or hospital-based dosing scenarios. Long-acting injectables are under study to cut frequency to quarterly or biannual visits, which could reshape adherence metrics. Safety debates around JAKs may slow oral momentum in select cohorts, yet convenience and cost dynamics still point to sustained growth in this modality.

By Distribution Channel: Digital Dispensing Accelerates

Hospital pharmacies owned 43.11% of sales in 2025 thanks to initiation protocols and cold-chain stewardship. Nevertheless, online channels exhibit the fastest 7.22% CAGR as telehealth familiarity and home-delivery reliability improve. Specialty e-pharmacies bundle financial aid, nurse coaching, and IoT shipping sensors to protect drug integrity, unlocking new revenue streams and reinforcing axial spondyloarthritis market expansion across dispersed geographies.

Retail outlets continue to serve chronic NSAID users and refill biologic pens yet face margin pressure from mail-order rivals. Manufacturers increasingly partner with integrated digital hubs to collect real-time adherence data, feeding value-based contracts. Regions with fragmented logistics still rely on hospital sites, but policy reforms and private investment in refrigerated last-mile transport promise to democratize access.

Geography Analysis

North America anchors 39.78% of global revenue and benefits from high biologic penetration, employer-funded specialty benefits, and streamlined FDA approval pathways. MRI density and AI-enabled reading tools have trimmed average diagnostic latency to 2.7 years, amplifying treated prevalence. Biosimilar diffusion is reshaping rebates and opening space for novel agents without swelling payer budgets, sustaining revenue leadership across the axial spondyloarthritis market.

Asia-Pacific records the quickest 7.19% CAGR through 2031 as China broadens reimbursement and hospital capacity. Ankylosing spondylitis prevalence of up to 0.42% implies sizable underdiagnosis. Japan exhibits high biologic utilization tied to universal coverage, whereas India still struggles with specialist scarcity and out-of-pocket limits. Regional public–private projects to add MRI scanners and tele-rheumatology services will likely raise drug volumes. Cultural integration of yoga and Tai Chi into standard care underscores local adaptation in managing axial disease.

Europe remains a mature market with universal coverage, but access variability lingers. Central and Eastern states lag in biologic uptake (27.9%) and endure longer diagnostic delays (4.2 years), muting growth. The continent nevertheless pioneers biosimilar policy, fostering competitive pricing. Middle East & Africa trail, constrained by fiscal capacity and cold-chain gaps, yet targeted donor programs and urban clinic build-outs are stirring incremental demand. South America offers mid-single-digit expansion tempered by macroeconomic volatility and reimbursement lag.

Competitive Landscape

Competitive intensity is rising as dual cytokine blockers, JAKs, and biosimilars jostle for position. AbbVie, Johnson & Johnson, Novartis, and UCB controlled roughly 62% of global revenue in 2024 by leveraging broad immunology franchises, co-pay assistance, and large-scale manufacturing. UCB’s BIMZELX has quickly disrupted TNF incumbents, winning guidelines mentions and stimulating head-to-head trials.

Pipeline strategies now focus on mechanistic novelty—NLRX1 agonists, IL-23 blockade, and microbiome adjuncts—over marginal reformulations. M&A activity, exemplified by AbbVie’s Landos Biopharma deal, secures access to first-in-class molecules before Phase 3 onset. Biosimilar producers exploit expiring patents to challenge originators; major PBMs have already de-listed Humira in favor of cheaper alternatives, triggering defensive contracting and patient-support enhancements.

Digital health is another battleground. Companies integrate AI dosing algorithms, Bluetooth-enabled autoinjectors, and real-world evidence dashboards to strengthen payer negotiations and differentiate brands. As cold-chain technology improves, regional players in emerging markets can viably distribute high-value biologics, heightening price pressure yet broadening overall axial spondyloarthritis market reach.

Global Axial Spondyloarthritis (axSpA) Industry Leaders

Janssen Biotech

AbbVie

UCB

Novartis Pharmaceuticals Corporation

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Johnson & Johnson reported positive Phase 3 APEX results for guselkumab in psoriatic arthritis, reinforcing IL-23 inhibition’s utility.

- September 2024: UCB gained FDA approval for BIMZELX (bimekizumab-bkzx) across non-radiographic axial spondyloarthritis and ankylosing spondylitis.

- July 2024: Spine BioPharma signed a USD 155 million deal with Ensol BioSciences to expand SB-01 indications into fibrotic diseases.

- March 2024: AbbVie completed the USD 137.5 million acquisition of Landos Biopharma, adding oral NLRX1 agonist NX-13 to its pipeline.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the axial spondyloarthritis (axSpA) market as worldwide prescription revenues from medicines treating radiographic ankylosing spondylitis and non-radiographic axSpA. It covers innovator and biosimilar biologics, targeted synthetic and conventional DMARDs, NSAIDs, and supportive corticosteroids distributed through hospital, retail, and online pharmacies. Values are booked at ex-manufacturer level and modeled from 2019 to 2030.

Scope exclusions: surgical spinal fusion, rehabilitation services, and stand-alone diagnostic imaging are outside scope.

Segmentation Overview

- By Disease Type

- Ankylosing Spondylitis (Radiographic axSpA)

- Non-radiographic Axial Spondyloarthritis

- By Drug Class

- Non-steroidal Anti-inflammatory Drugs (NSAIDs)

- Glucocorticoids

- Disease-modifying Antirheumatic Drugs (DMARDs)

- Others

- By Route of Administration

- Oral

- Subcutaneous

- Intravenous

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed rheumatologists, hospital pharmacists, and payer advisors across North America, Europe, and Asia-Pacific. Insights on treated-patient share, dose persistence, and biosimilar erosion were folded into the model.

Desk Research

We compiled epidemiology, drug approval, and reimbursement data from the World Health Organization, EULAR, the U.S. CDC, national formularies, customs shipments, and peer-reviewed journals. Financial details from company 10-Ks, investor calls, and D&B Hoovers, plus news retrieved through Dow Jones Factiva, supplied launch prices and volume hints. The sources noted are illustrative; additional open datasets underpinned cross-checks.

Market-Sizing & Forecasting

A top-down prevalence-to-treated methodology converts country burden into drug demand. Then, selective bottom-up roll-ups of key molecule sales validate totals. Core variables include diagnosed prevalence, average biologic days of therapy, annual price per patient, biosimilar discount depth, switch rate to JAK inhibitors, and uptake of dual IL-17 blockers. Multivariate regression combined with scenario analysis projects 2025-2030 growth; regional gaps are bridged with calibrated proxies vetted in primary calls.

Data Validation & Update Cycle

Outputs pass variance checks against prescription audits and customs records, with anomalies escalated for senior review. Reports refresh annually, and before release, a Mordor analyst re-runs the model so clients receive the freshest view.

Why Our Axial Spondyloarthritis Baseline Commands Reliability

Published estimates vary because firms differ on scope, pricing assumptions, patient funnel ratios, and update cadence.

Key Gap Drivers: Some include imaging or physiotherapy revenue. Others use list prices, ignoring country rebates. A few extrapolate pre-biosimilar volumes and miss 2024 dual IL-17 launches that our model captures.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 4.39 B USD (2025) | Mordor Intelligence | - |

| 6.12 B USD (2025) | Global Consultancy A | Bundles diagnostics and therapy services |

| 4.87 B USD (2024) | Trade Journal B | Uses historic ASPs, omits 2025 rebate cuts |

| 4.41 B USD (2025) | Regional Consultancy C | Excludes nr-axSpA patient segment |

Taken together, the comparison shows that our disciplined scope selection, regularly refreshed inputs, and dual validation steps give decision-makers the most dependable baseline.

Key Questions Answered in the Report

What is the current value of the axial spondyloarthritis market?

The market is valued at USD 4.68 billion in 2026 and is projected to reach USD 6.46 billion by 2031.

Which therapy class holds the largest share of revenue?

DMARDs lead with 49.02% of axial spondyloarthritis market share in 2025.

Why is Asia-Pacific growing faster than other regions?

Expanding reimbursement, rising diagnostic capacity, and large undiagnosed prevalence in countries such as China are propelling a 7.19% CAGR.

How are biosimilars influencing treatment costs?

Preferred formulary placement for adalimumab biosimilars has cut annual patient expenses by roughly USD 3,500.

What are the key safety concerns for JAK inhibitors?

Cardiovascular events and malignancy risks in older patients with comorbidities have led regulators to restrict use to those failing TNF blockers.

Which companies are leading innovation in axial spondyloarthritis?

UCB with bimekizumab, AbbVie through its Landos acquisition, and Johnson & Johnson via guselkumab expansion are notable innovators.

Page last updated on: