Non-Small Cell Lung Cancer (NSCLC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

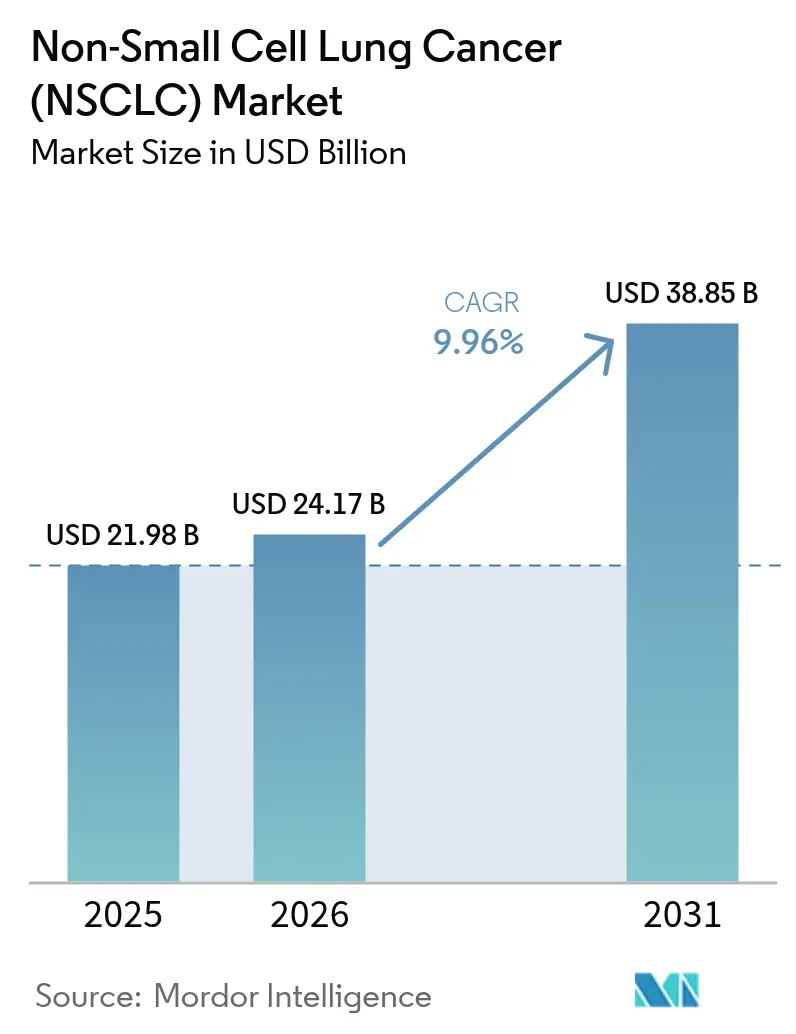

| Market Size (2026) | USD 24.17 Billion |

| Market Size (2031) | USD 38.85 Billion |

| Growth Rate (2026 - 2031) | 9.96% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

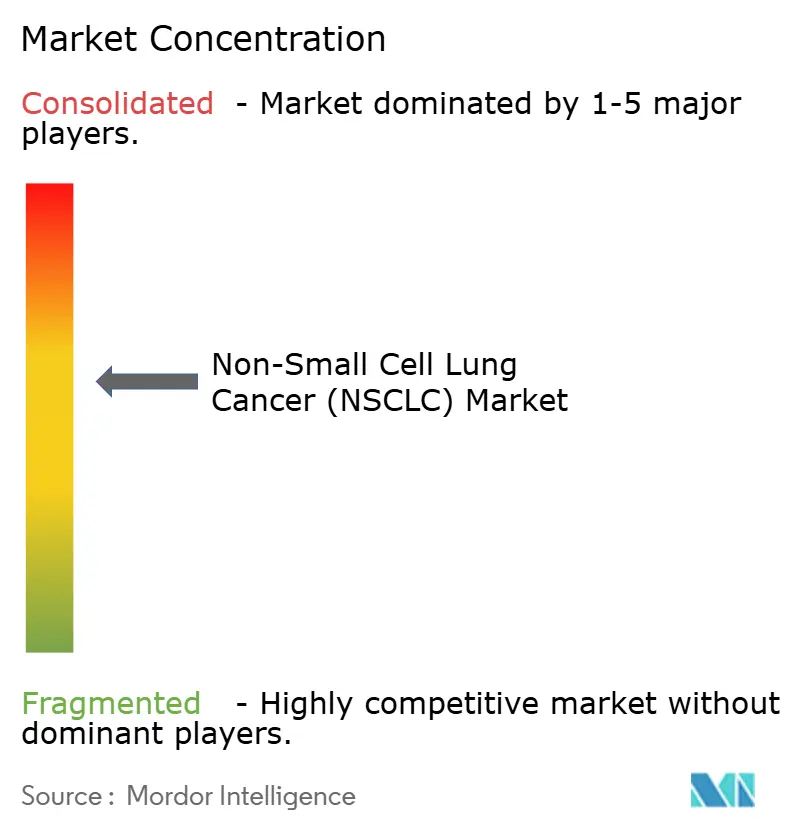

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-Small Cell Lung Cancer (NSCLC) Market Analysis by Mordor Intelligence

Non-Small Cell Lung Cancer market size in 2026 is estimated at USD 24.17 billion, growing from 2025 value of USD 21.98 billion with 2031 projections showing USD 38.85 billion, growing at 9.96% CAGR over 2026-2031. Surging demand for breakthrough immunotherapies, rapid FDA approvals of antibody-drug conjugates (ADCs), and steady progress in radiopharmaceutical precision targeting are accelerating revenue growth. Competitive intensity is rising as pharmaceutical leaders pivot toward artificial-intelligence–enabled biomarker platforms, while liquid-biopsy companion diagnostics expand the addressable patient pool for targeted medicines. Although supply constraints for complex ADC payloads persist, premium-priced alternatives are gaining traction as clinicians seek to bypass chemotherapy shortages. Evolving reimbursement frameworks that reward real-world survival gains and the migration of checkpoint inhibitors into earlier disease stages further reinforce long-term expansion of the Non-Small Cell Lung Cancer market.

Report Key Takeaways

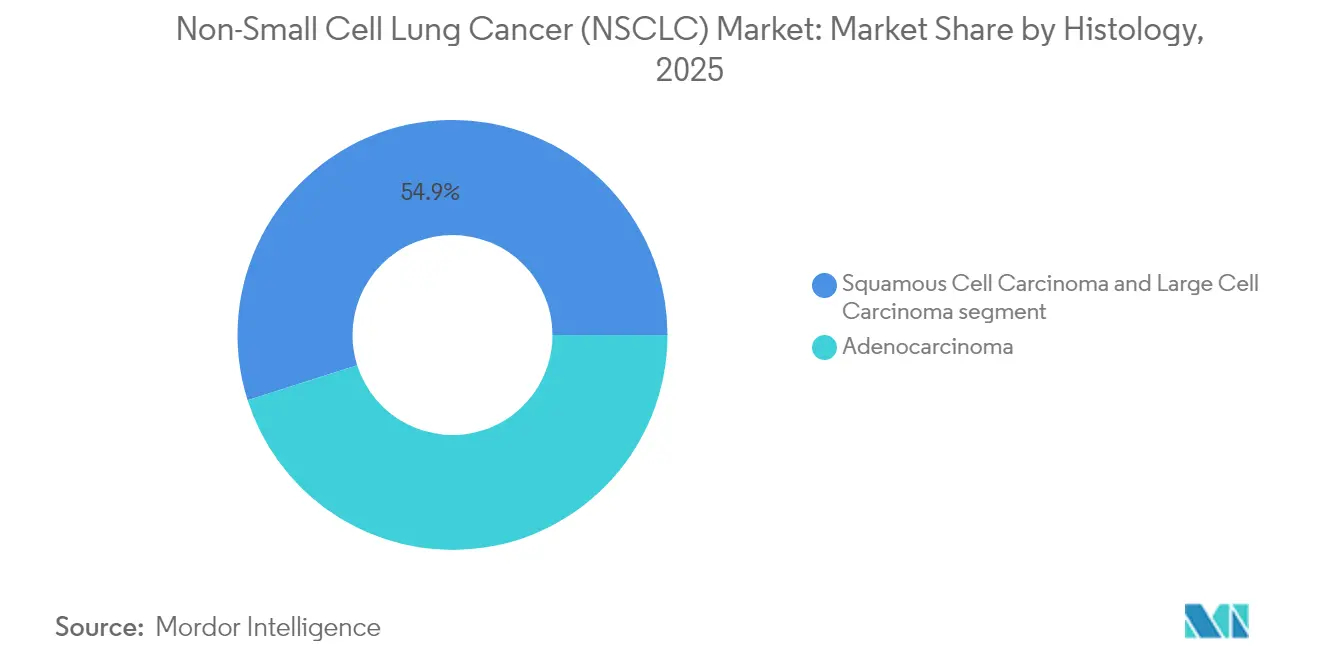

- By histology, adenocarcinoma led with 45.10% of Non-Small Cell Lung Cancer market share in 2025; large-cell carcinoma is forecast to expand at an 11.05% CAGR through 2031.

- By treatment modality, immunotherapy commanded a 37.25% revenue share in 2025, while radiopharmaceuticals are projected to grow at a 12.03% CAGR to 2031.

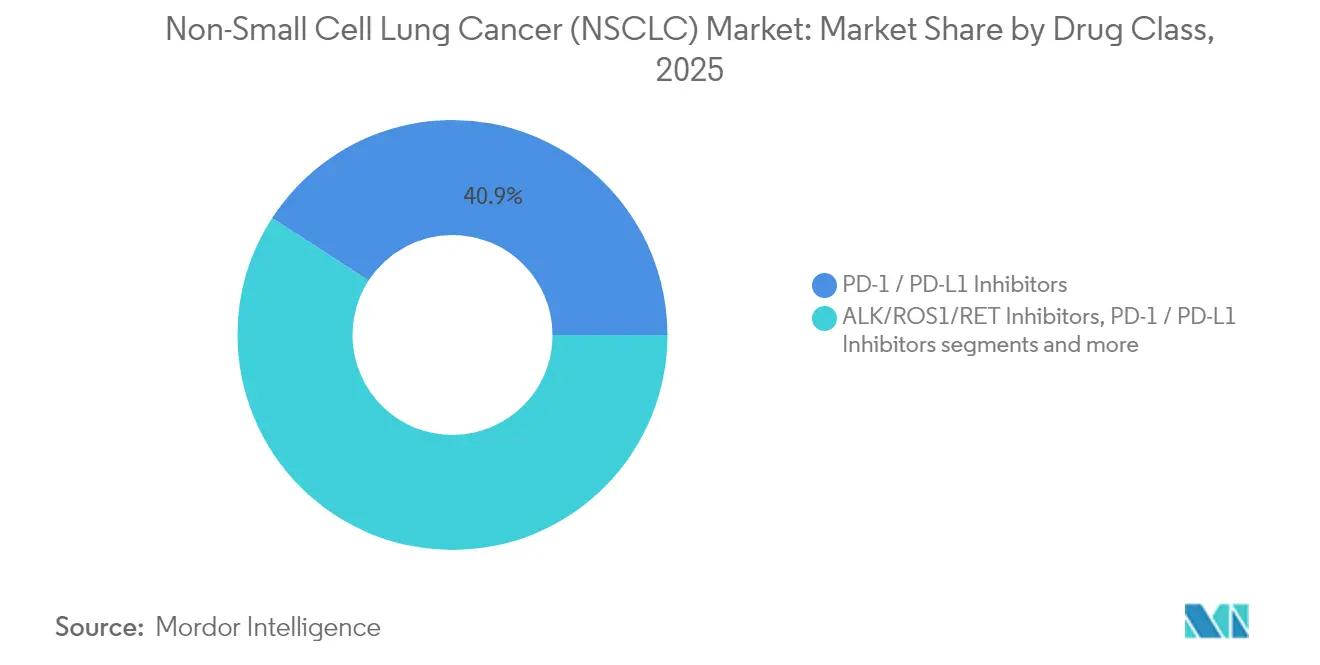

- By drug class, PD-1/PD-L1 inhibitors held 40.85% share of the Non-Small Cell Lung Cancer market size in 2025; ADCs represent the fastest-growing class at an 11.74% CAGR.

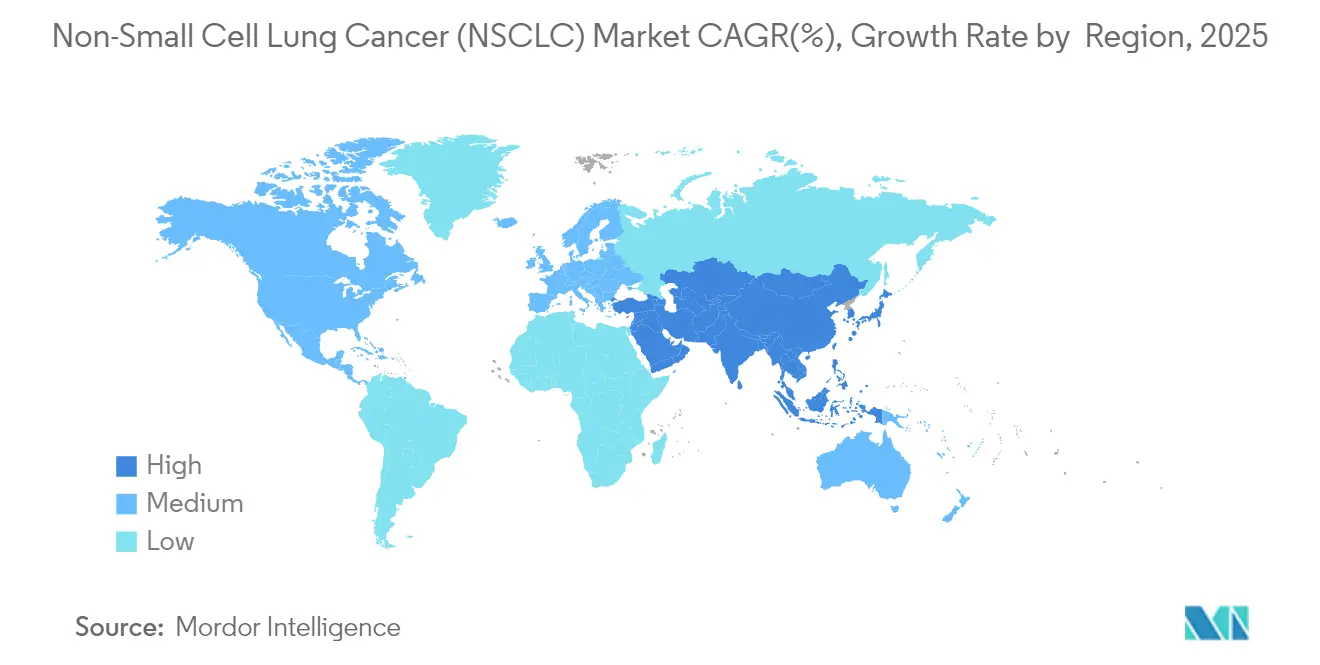

- By geography, North America accounted for 41.95% of market share in 2025, whereas Asia-Pacific is advancing at a 12.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-Small Cell Lung Cancer (NSCLC) Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Check-point inhibitor dominance in 1L metastatic setting | 2.80% | Global, strongest in North America & EU | Medium term (2-4 years) |

| Rapid uptake of EGFR/ALK targeted therapies in resectable early-stage NSCLC | 2.10% | Global, especially APAC | Short term (≤ 2 years) |

| Liquid-biopsy companion diagnostics adoption | 1.40% | North America & EU, widening to APAC | Medium term (2-4 years) |

| Radiopharmaceutical pipeline breakthroughs | 1.90% | Global, manufacturing hubs in US & EU | Long term (≥ 4 years) |

| AI-guided trial design & faster FDA approvals | 1.20% | Global, US-led | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Check-point Inhibitor Dominance in First-Line Metastatic Setting

Checkpoint blockade regimens have displaced platinum doublets in first-line metastatic disease across major markets, reshaping clinical guidelines and payer policies. China’s National Medical Products Administration approval of pembrolizumab plus chemotherapy for resectable stage II-IIIA NSCLC illustrates the class’s expansion into curative-intent settings. Emerging bispecifics such as ivonescimab have shown a 49% reduction in progression risk versus pembrolizumab in PD-L1–high tumors, signaling future erosion of incumbent share. To secure reimbursement, manufacturers now embrace value-based contracts pegged to real-world progression-free survival, while clinicians rely on biomarker-driven selection to maximize benefit-risk ratios. These trends collectively reinforce the growth trajectory of the Non-Small Cell Lung Cancer market while increasing competitive churn among checkpoint brands.

Rapid Uptake of EGFR/ALK Targeted Therapies in Resectable Early-Stage NSCLC

Osimertinib’s 39.1-month median progression-free survival in unresectable stage III EGFR-mutated disease has redefined standards by shifting targeted therapy earlier in the continuum of care. Combination regimens such as amivantamab plus lazertinib cut death risk by 25% versus osimertinib monotherapy, accelerating substitution in first-line adjuvant settings. Surgeons increasingly integrate genomic profiling preoperatively, and Asia-Pacific health systems are scaling next-generation sequencing labs to serve high EGFR-mutation prevalence populations. These advances shorten treatment initiation and increase uptake, cementing precision therapy as a catalyst for the Non-Small Cell Lung Cancer market.

Liquid-Biopsy Companion Diagnostics Adoption

Roche’s AI-powered TROP2 assay, designated by the FDA as a breakthrough device, showcases how computational pathology boosts biomarker accuracy and widens eligibility for ADCs like datopotamab deruxtecan. Circulating-tumor-DNA analysis now detects resistance mutations months ahead of imaging, enabling on-therapy switch strategies that prolong benefit duration. Centralized laboratories improve economies of scale, whereas point-of-care devices cut turnaround from 10 days to under 48 hours in community settings. Regulatory guidance permitting adaptive algorithms further legitimizes real-time genomic monitoring, broadening the Non-Small Cell Lung Cancer market.

Radiopharmaceutical Pipeline Breakthroughs

Novartis’s USD 1 billion acquisition of Mariana Oncology underpins investor confidence in targeted alpha therapy assets for lung malignancies [1]Source: Novartis, “Novartis Enters Agreement to Acquire Mariana Oncology,” novartis.com . Eli Lilly’s USD 1.1 billion alliance with Aktis Oncology highlights similar momentum in miniprotein-guided radiopharmaceutical delivery. Supply limitations of actinium-225 have prompted domestic isotope investments, while new FDA guidance clarifies theranostic development pathways. Collectively, these developments underpin the 12.23% CAGR expected for the radiopharmaceutical segment of the Non-Small Cell Lung Cancer market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price caps & HTA push-backs in Europe | -1.80% | EU-27 | Medium term (2-4 years) |

| Diagnostic biomarker testing capacity gaps in emerging Asia | -1.20% | India & Southeast Asia | Short term (≤ 2 years) |

| PD-(L)1 class saturation & payer rebate squeeze | -1.50% | Global mature markets | Medium term (2-4 years) |

| Manufacturing bottlenecks for ADC payloads | -0.90% | Global supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price Caps & HTA Push-backs in Europe

European health technology assessment agencies have tightened cost-effectiveness thresholds, challenging premium immuno-oncology pricing. Germany’s IQWiG rejected several checkpoint combinations for insufficient incremental survival over standards of care, forcing manufacturers to adopt risk-sharing schemes. Parallel reference pricing in France and Italy cascades reimbursement pressure globally, tempering top-line growth for the Non-Small Cell Lung Cancer market. Managed-entry agreements, however, still create footholds for innovative agents willing to align reimbursement with real-world evidence.

Diagnostic Biomarker Testing Capacity Gaps in Emerging Asia

Molecular pathology resources remain concentrated in urban centers, delaying therapy initiation in rural India where out-of-pocket costs exceed 60% of treatment expenditure. Limited next-generation sequencing platforms constrain adoption of EGFR, ALK, and ROS1 testing, directly slowing uptake of precision therapies. Tele-pathology and AI-enabled digital slide review are being piloted to bridge gaps, yet scale-up is at least two years away, moderating growth momentum for the Non-Small Cell Lung Cancer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Histology: Adenocarcinoma Drives Targeted Therapy Innovation

Adenocarcinoma captured 45.10% of Non-Small Cell Lung Cancer market share in 2025 owing to its high prevalence among never-smokers and its responsiveness to EGFR and ALK inhibitors. Osimertinib’s move into unresectable stage III disease has expanded the treated adenocarcinoma population, while bispecifics and ADCs promise further gains. Squamous cell carcinoma, limited by fewer actionable mutations, is beginning to benefit from FGFR inhibitors and chemo-immunotherapy pairings that extend survival. Large-cell carcinoma holds a smaller baseline but is projected to grow at 11.05% CAGR as AI-enhanced pathology improves subtype recognition and clinical trial enrollment.

The Non-Small Cell Lung Cancer market size for adenocarcinoma is forecast to rise in tandem with global expansion of comprehensive genomic profiling labs. Early-stage molecular testing has increased the eligible pool for neoadjuvant targeted therapy, improving resectability rates. Pharmaceutical pipelines now routinely stratify trials by histology, ensuring alignment between mechanism of action and tumor biology. Consequently, investors regard histology-specific assets as a competitive advantage in the broader Non-Small Cell Lung Cancer market.

By Treatment Modality: Immunotherapy Leadership Faces Radiopharmaceutical Disruption

Immunotherapy maintained a 37.25% revenue share in 2025, supported by broad checkpoint inhibitor adoption and an expanding set of bispecifics that deepen response in PD-L1-high tumors. Integrated chemo-immunotherapy regimens have improved pathologic complete response in neoadjuvant settings, consolidating immunotherapy's role across the disease spectrum. Conversely, radiopharmaceuticals—currently less than 3% of sales—are poised for a 12.03% CAGR on the strength of alpha-emitting conjugates that deliver tumor-selective radiation.

The Non-Small Cell Lung Cancer market size for radiopharmaceuticals is projected to expand sharply once isotope supply constraints ease and companion diagnostics mature. ADCs blur modality boundaries by combining targeted delivery with cytotoxic payloads, thereby siphoning share from both chemotherapy and immunotherapy. Surgical uptake remains stable but benefits from neoadjuvant IO combinations that raise operability. Overall, modality diversification grants clinicians flexible tools, positioning the Non-Small Cell Lung Cancer market for sustained growth.

By Drug Class: PD-1/PD-L1 Dominance Challenged by ADC Innovation

PD-1/PD-L1 inhibitors held 40.85% of the Non-Small Cell Lung Cancer market in 2025 and anchor the standard of care in both metastatic and adjuvant settings. Competition intensifies as bispecific antibodies report superior progression-free survival and as CTLA-4 and LAG-3 agents join combination regimens. ADCs recorded the fastest trajectory at 11.74% CAGR, spearheaded by datopotamab deruxtecan's 42.7% objective response in heavily pretreated EGFR-mutated disease.

ALK/ROS1/RET inhibitors continue to address niche molecular subgroups, with taletrectinib achieving a 90% response rate in ROS1-positive treatment-naive patients. EGFR TKIs broaden into earlier settings, and resistance-ameliorating combinations are under evaluation. Collectively, expanding drug-class diversity safeguards optionality for clinicians and widens the therapeutic canvas of the Non-Small Cell Lung Cancer market.

Geography Analysis

North America accounted for 41.95% of the Non-Small Cell Lung Cancer market in 2025 thanks to rapid regulatory approvals, advanced insurance coverage, and concentrated research infrastructure. Six new lung cancer therapies gained FDA clearance in 2024 alone, including two ADCs and one bispecific antibody, underscoring regulatory agility. The region is investing in domestic ADC payload production to mitigate supply bottlenecks, a move expected to stabilize future pricing and ensure consistent drug availability.

Asia-Pacific is projected to register a 12.23% CAGR through 2031, making it the fastest-growing component of the Non-Small Cell Lung Cancer market. Rising healthcare expenditures, improved diagnostic coverage, and high EGFR-mutation prevalence underpin demand. China has accelerated local approvals of imported checkpoint inhibitors and ADCs, shrinking the lag against FDA decisions. Nonetheless, rural testing gaps constrain equitable access, prompting expansion of tele-pathology and public–private genomic testing partnerships.

Europe combines sophisticated molecular medicine uptake with price-containment discipline. Stringent HTA assessments produce managed-entry agreements that permit early access while collecting post-marketing evidence. Brexit-related logistics disruptions have increased lead times for certain biologics, but the European Medicines Agency's centralized process continues to streamline multistate approvals. Middle East & Africa and South America represent nascent opportunities; initiatives such as Brazil's public oncology partnerships and Gulf states' cancer center expansions could gradually enlarge the regional Non-Small Cell Lung Cancer market as infrastructure matures.

Competitive Landscape

The Non-Small Cell Lung Cancer market is moderately consolidated, characterized by a handful of global pharmaceutical majors holding significant but not overwhelming share. High development costs, complex biologic manufacturing, and specialized distribution channels erect formidable entry barriers. Strategic alliances are proliferating: Bristol Myers Squibb’s pact with BioNTech on bispecific antibody BNT327 showcases big-pharma agility in accessing novel platforms [2]Source: Bristol Myers Squibb, “BioNTech and Bristol Myers Squibb Announce Global Partnership,” news.bms.com.

Precision-diagnostics-plus-therapeutics ecosystems create switching costs that favor incumbents capable of bundling companion assays with drugs. Artificial-intelligence–guided discovery is compressing timelines; Roche’s investment in computational pathology exemplifies this shift. Yet white-space opportunities remain in resistance-ameliorating combinations and cost-effective regimens for emerging markets. Long-term differentiation will hinge on demonstrating real-world survival advantages aligned with payer value frameworks.

Leading firms continue to strengthen vertical integration in radiopharmaceuticals to capture supply chain synergies. Novartis has invested more than USD 1.7 billion in radioligand acquisitions since 2024, broadening its isotope manufacturing footprint. Eli Lilly’s USD 1.4 billion outlay for alpha-therapy startups furthers this consolidation trend. Collectively, these moves reinforce competitive moats while signaling confidence in precision-radiation modalities as future growth engines within the Non-Small Cell Lung Cancer market.

Non-Small Cell Lung Cancer (NSCLC) Industry Leaders

F. Hoffmann-La Roche Ltd.

Bristol-Myers Squibb Company

Pfizer Inc.

AstraZeneca

Novartis AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Taletrectinib received FDA approval for ROS1-positive NSCLC, achieving 90% objective response in first-line patients.

- June 2025: Bristol Myers Squibb and BioNTech launched a global partnership for bispecific BNT327.

- May 2025: Telisotuzumab vedotin obtained FDA accelerated approval for c-Met–high NSCLC.

- April 2025: Zongertinib entered FDA priority review for HER2-mutant NSCLC.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the non-small cell lung cancer (NSCLC) market as all prescription therapeutics, including surgery-enabling drugs, chemotherapy, targeted therapy, immunotherapy, radiopharmaceuticals, and antibody-drug conjugates, sold for the treatment of adenocarcinoma, squamous cell carcinoma, and large-cell carcinoma across 17 countries during 2019-2030.

Scope exclusion: Treatments that are specific to small-cell lung cancer are outside the present analysis.

Segmentation Overview

- By Histology

- Adenocarcinoma

- Squamous Cell Carcinoma

- Large Cell Carcinoma

- By Treatment Modality

- Surgery

- Radiation Therapy

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- Radiopharmaceuticals

- By Drug Class

- EGFR TKIs

- ALK/ROS1/RET Inhibitors

- PD-1 / PD-L1 Inhibitors

- CTLA-4 & LAG-3 Inhibitors

- Antibody-Drug Conjugates (ADC)

- By Region

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed oncologists, hospital pharmacists, and reimbursement specialists in North America, Europe, and key Asia-Pacific markets. Discussions clarified real-world adherence, patient assistance penetration, and off-label crossover, and they validated incidence-to-treatment funnels suggested by desk work.

Desk Research

We began with published epidemiology from sources such as the World Health Organization, Centers for Disease Control and Prevention, and the International Agency for Research on Cancer, using incidence, prevalence, and mortality to size the addressable patient pool. Market-wide pricing and volume clues were obtained from national reimbursement lists, FDA and EMA drug approval dossiers, and quarterly filings that reveal unit sales trends. To enrich geographic splits, customs import data and patent family statistics (Questel) helped us trace molecule flows and life-cycle timing.

Company 10-Ks, investor decks, and oncology-focused journals such as JCO provided average course lengths, typical line-of-therapy switches, and competitive launch timelines, allowing us to benchmark uptake curves. These sources are illustrative, not exhaustive; many additional scientific, regulatory, and trade datasets were tapped for cross-checks.

Market-Sizing & Forecasting

A top-down epidemiological build, population, smoking prevalence, NSCLC incidence, treatment-eligible share, and average treatment cost yield initial 2025 revenue. We then reconcile this with bottom-up checkpoints such as sampled ASP by volume roll-ups from select distributors before adjusting for patient migration and combination therapy overlaps. Core variables include PD-1/PD-L1 inhibitor adoption, antibody-drug conjugate launches, median treatment duration shifts, pricing dynamics post-biosimilar entry, and regional reimbursement timelines. A multivariate regression forecasts each driver; scenario analysis around pipeline approvals adds upside and downside bands. Data gaps in channel sales were bridged by proportional allocation based on known market shares from audited hospital procurement lists.

Data Validation & Update Cycle

Outputs pass variance screens against independent mortality trends and quarterly sales flashes. Any anomaly triggers re-contact with field experts, followed by analyst peer review. Reports refresh annually, with interim updates when material regulatory or trial outcomes surface.

Why Mordor's Non-Small Cell Lung Cancer Baseline Earns Decision-Maker Trust

Published values often diverge because firms draw lines differently around histology mix, therapy settings, or off-label spillovers.

Key gap drivers include treatment scope breadth, assumed launch timing, and refresh cadence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.98 B | Mordor Intelligence | - |

| USD 19.78 B | Regional Consultancy A | Omits radiopharmaceutical revenues and applies uniform ASP across regions |

| USD 24.24 B | Global Consultancy B | Uses aggressive uptake curve for pipeline KRAS therapies not yet approved in major EU markets |

| USD 28.61 B | Industry Association C | Combines NSCLC with recurrent SCLC treatments, inflating base |

These comparisons show that when scope, launch timing, and geography are aligned, our carefully triangulated figures give clients a balanced, transparent baseline that can be traced back to verifiable incidence data and clearly stated pricing assumptions.

Key Questions Answered in the Report

What is the current size of the Non-Small Cell Lung Cancer market?

The Non-Small Cell Lung Cancer market size reached USD 24.17 billion in 2026 and is projected to continue expanding at a 9.96% CAGR.

Which treatment modality leads the market today?

Immunotherapy leads with 37.25% revenue share in 2025, driven by widespread uptake of PD-1/PD-L1 checkpoint inhibitors.

Which region is growing the fastest?

Asia-Pacific is forecast to grow at a 12.23% CAGR through 2031, supported by rising healthcare spending and accelerated regulatory approvals.

Which region has the biggest share in Global Non-Small Cell Lung Cancer (NSCLC) Market?

Antibody-drug conjugates are the fastest-growing class, expected to post an 11.74% CAGR through 2031 owing to multiple FDA breakthrough designations.

How are European price caps affecting market growth?

Stringent HTA thresholds in Europe reduce CAGR by an estimated 1.8% as payers impose value-based pricing and delay broad reimbursement for high-cost combinations.

Page last updated on: