Nitrogen Oxide (NOx) Control Systems Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.69 Billion |

| Market Size (2031) | USD 10.78 Billion |

| Growth Rate (2026 - 2031) | 6.99% CAGR |

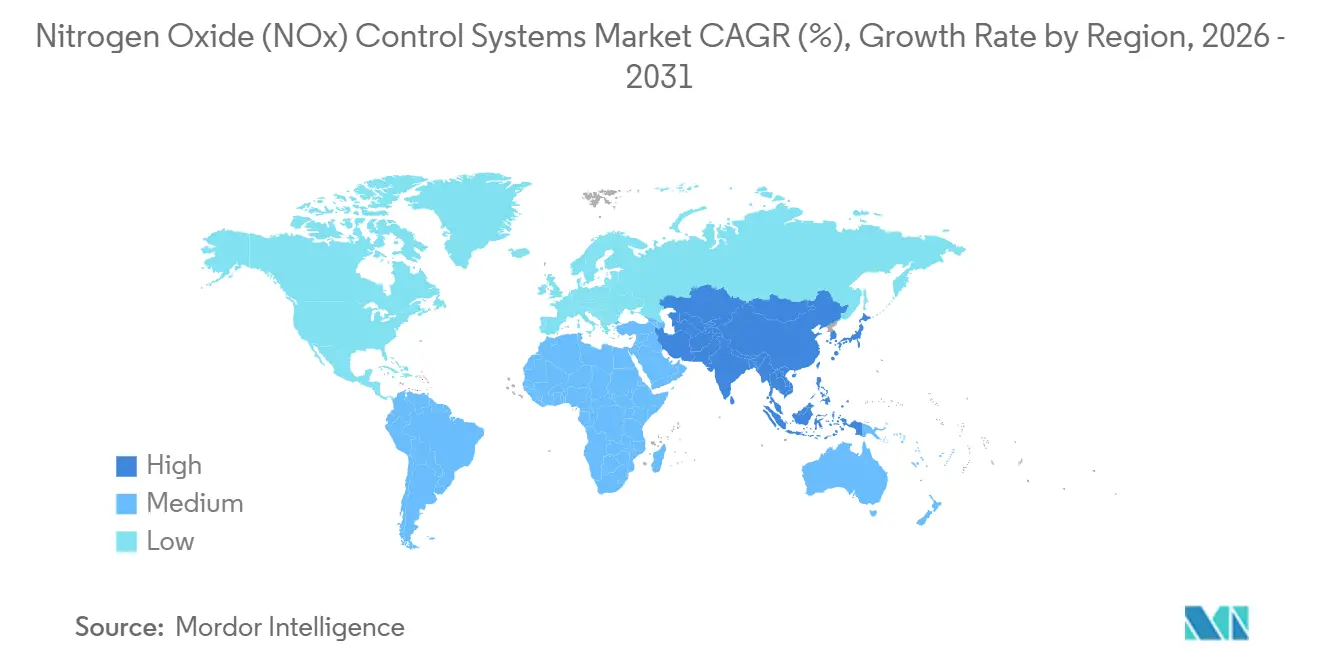

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nitrogen Oxide (NOx) Control Systems Market Analysis by Mordor Intelligence

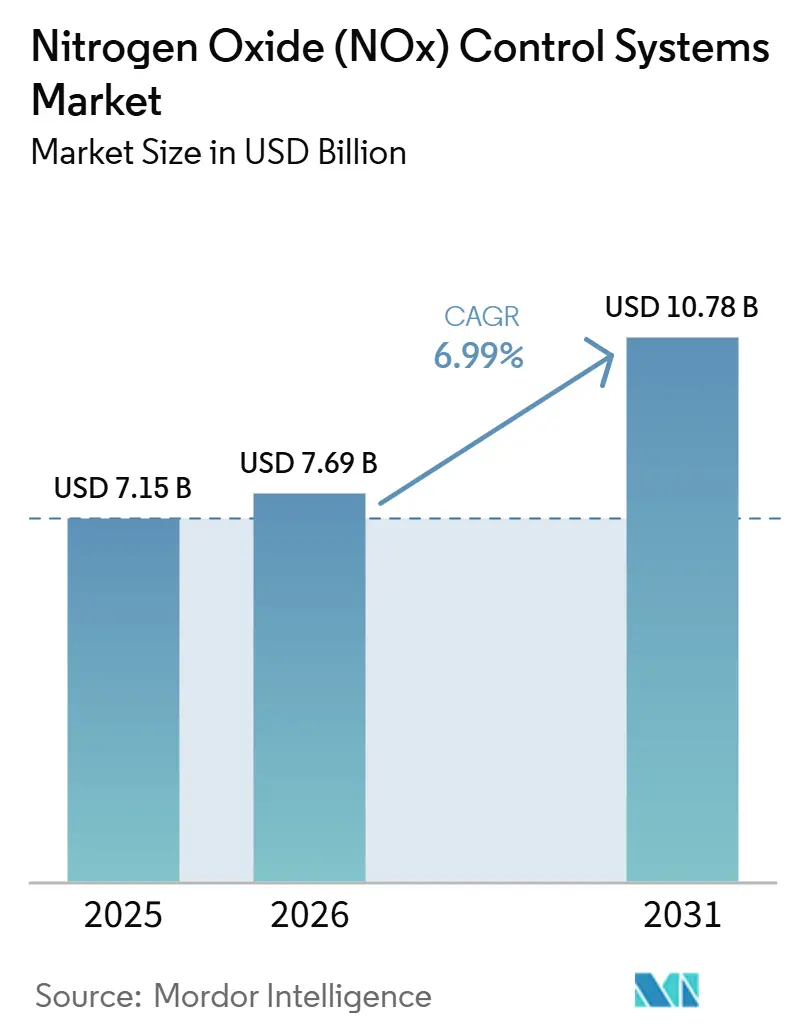

The Nitrogen Oxide Control Systems Market size is expected to grow from USD 7.15 billion in 2025 to USD 7.69 billion in 2026 and is forecast to reach USD 10.78 billion by 2031 at 6.99% CAGR over 2026-2031. A synchronized tightening of emission rules in power, transportation, and maritime sectors is accelerating compliance spending, while decarbonization pathways such as hydrogen and ammonia combustion raise thermal-NOx formation, expanding the addressable base for the nitrogen oxide control systems market.[1]U.S. Environmental Protection Agency, “Good Neighbor Plan Final Rule,” EPA.gov March 2026 supply shocks in the Strait of Hormuz exposed the fragility of global reagent chains, prompting operators to diversify ammonia and urea sourcing strategies.[2]Financial Times, “Strait of Hormuz Tensions Disrupt Urea Exports,” FT.com Simultaneously, demonstration projects using 100% ammonia fuel proved technical feasibility but confirmed that next-generation low-temperature catalysts and AI-driven monitoring will be essential for stable operations. Moderate competitive intensity persists as incumbent catalyst suppliers defend long-cycle power-plant and marine contracts, even as smaller firms commercialize slip-abatement and adsorption modules that broaden solution portfolios.

Key Report Takeaways

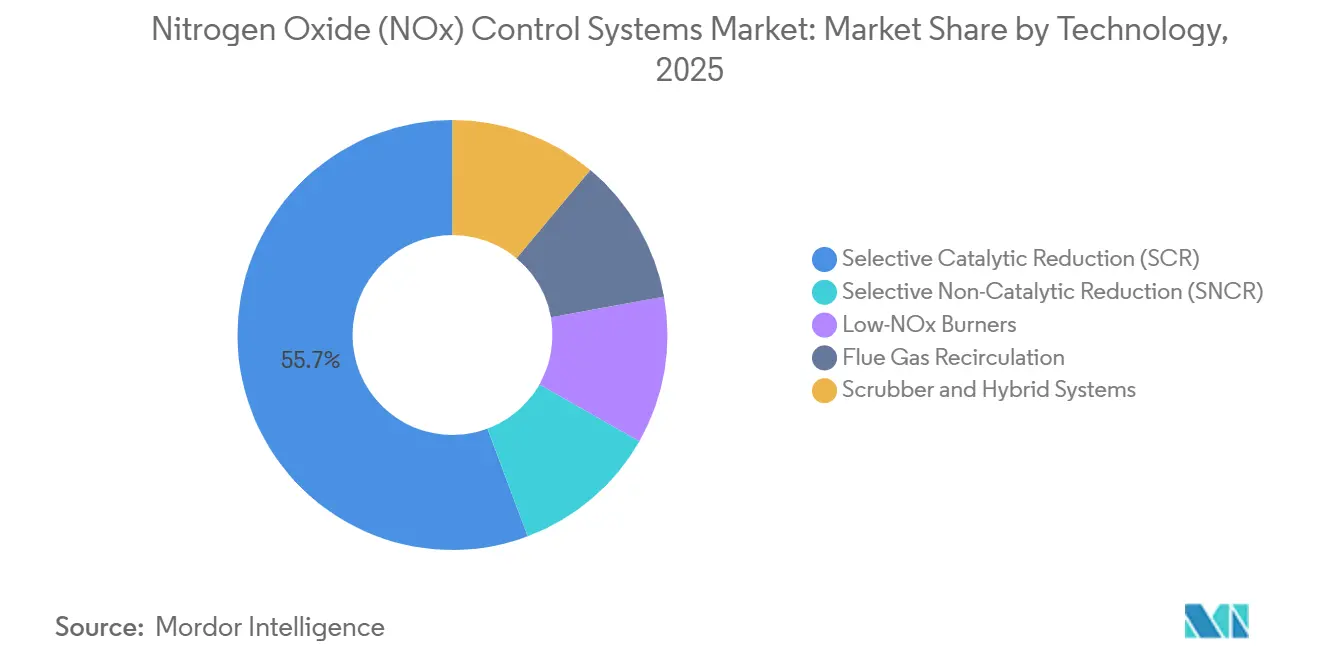

- By technology, selective catalytic reduction held 55.7% of the nitrogen oxide control systems market share in 2025 and is forecast to grow at a CAGR of 8.0% through 2031.

- By application, power generation accounted for 38.1% of revenue share in 2025, while marine engines are expected to register the fastest CAGR of 9.6% over 2026-2031, driven by expanding IMO Tier III enforcement.

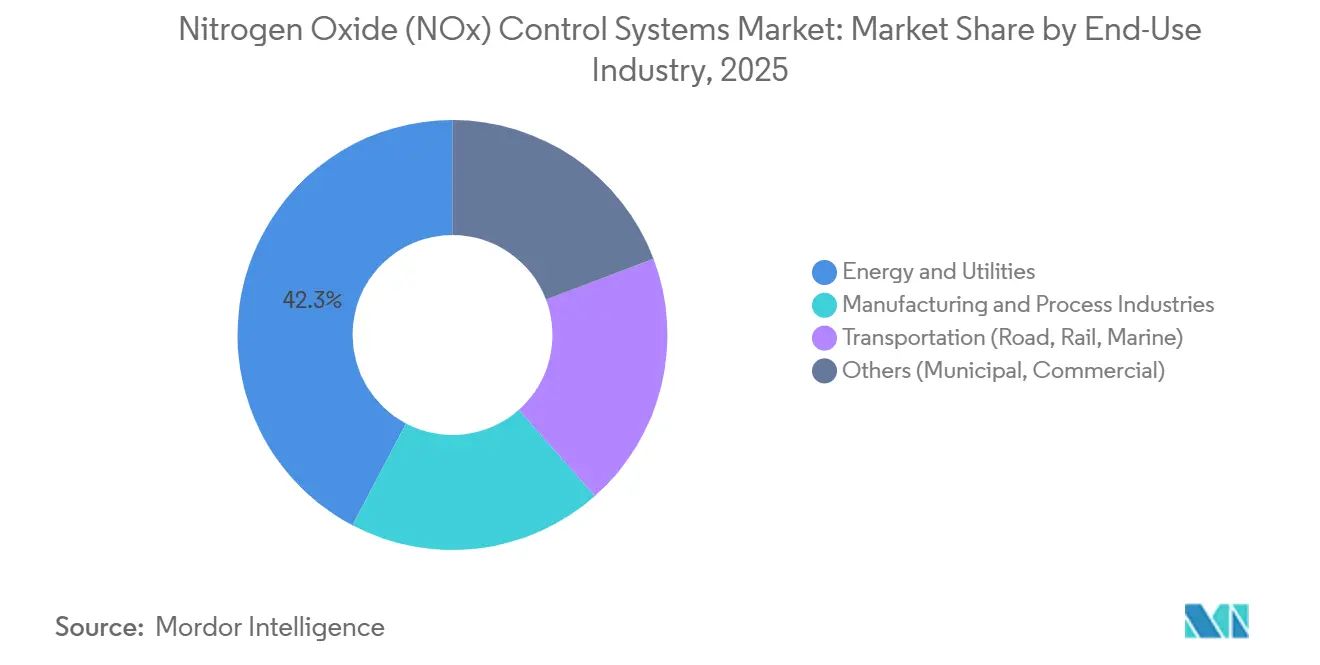

- By end-use industry, energy and utilities led with a 42.3% share in 2025; transportation is projected to post a CAGR of 8.5%, supported by heavy-duty fleet upgrades and remote OBD telematics adoption.

- By region, Asia-Pacific accounted for 44.6% of 2025 revenue and is expected to grow at a CAGR of 7.7%, driven by China's ultra-low-emission mandate and India's cost-optimized retrofit programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nitrogen Oxide (NOx) Control Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter multi-sector NOx emission caps (U.S. Good Neighbor, EU Euro VII, IMO Tier III) | +1.8% | Global, with North America & EU leading regulatory stringency; Asia-Pacific following with national ultra-low standards | Medium term (2-4 years) |

| Accelerated SCR retrofits in coal-fired & gas turbine power plants | +1.2% | Asia-Pacific core (China, India), spill-over to North America and EU legacy fleets | Medium term (2-4 years) |

| Diesel vehicle stock driving DEF consumption & on-road SCR adoption | +0.9% | Global, with Asia-Pacific and North America heavy-duty fleets as primary demand centers | Short term (≤ 2 years) |

| Industrial boiler revamps with low-NOx burners in chemicals & cement | +0.7% | Asia-Pacific (China cement sector), Europe (IED compliance), North America (refinery upgrades) | Long term (≥ 4 years) |

| AI-enabled remote-OBD compliance unlocking carbon-credit subsidies | +0.5% | North America (CARB telematics mandates), EU (fleet monitoring directives), early adoption in China urban fleets | Short term (≤ 2 years) |

| Hydrogen-based low-temperature SCR catalysts moving from lab to pilot | +0.4% | Japan, South Korea, Germany pilot corridors; commercial scale 2028-2030 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Multi-Sector NOx Emission Caps Drive Compliance Investments

The alignment of the U.S. Good Neighbor Rule, Euro VII on-road limits, and IMO Tier III marine standards are compressing compliance timelines across stationary and mobile assets. Litigation delays in 2024-2025 postponed some U.S. retrofit awards; however, the underlying rule remained in effect, and utilities are now releasing backlogged purchase orders. Euro VII's real-driving-emissions protocol lowers permissible NOx factors to 1.43 by 2027, adding USD 800-1,200 per vehicle for close-coupled SCR and slip catalysts. The inclusion of the Mediterranean in the Emission Control Area in 2026 extended Tier III obligations to an additional 4,300 vessels, lifting annual marine-sector demand for the nitrogen oxide control systems market.[3] International Maritime Organization, “MEPC Approves Mediterranean ECA,” Imo.org California's 0.02 g/hp-hr heavy-duty rule, effective 2027, increases sensing precision requirements tenfold, driving demand for parts-per-million detection modules. Together, these regulatory caps support predictable long-term demand visibility across the nitrogen oxide control systems market.

Accelerated SCR Retrofits in Coal-Fired and Gas-Turbine Power Plants

Retrofitting legacy plants remains the largest stationary source opportunity. China has directed coal generators to trial 10% ammonia co-firing by 2027, a move that increases thermal NOx emissions unless high-activity, multi-layer catalysts are installed. India has capped new-build units at 100 mg/Nm³ and legacy fleets at 450 mg/Nm³; state utilities favor lower-cost SNCR for older assets, while new combined-cycle blocks standardize on SCR, maintaining a strong pipeline for the nitrogen oxide control systems market. In North America, GE Vernova's 83 GW gas-turbine backlog, paired with a USD 600 million catalyst facility, reflects sustained retrofit and greenfield activity. Canadian refiners are combining wet-gas scrubbing with high-efficiency SCR to meet provincial airshed quotas, demonstrating how multi-pollutant compliance requirements expand system-integration scope. Together, these factors support an 8.0% annual growth rate for SCR solutions.

Diesel Vehicle Stock Driving DEF Consumption and On-Road SCR Adoption

Despite ongoing electrification, the global heavy-duty diesel fleet continues to grow, supporting 6-8% annual growth in automotive-grade urea demand and, consequently, reagent supply agreements within the nitrogen oxide control systems market. The March 2026 Strait of Hormuz disruption increased U.S. Gulf Coast urea prices by USD 70/short-ton, prompting fleets to hedge reagent exposure and adopt telematics that reduce dosing overshoot. In 2025, Shanghai connected more than 200,000 heavy trucks to real-time OBD portals, granting 92,000 inspection exemptions and indicating a regulatory preference for continuous verification models that incorporate catalyst performance analytics. In California, Geotab's CARB-certified T-harness enables operators to avoid USD 42,450 in penalties by demonstrating uninterrupted SCR functionality, establishing monetizable data streams as an integral component of fleet economics. Together, continued diesel reliance and compliance digitalization sustain on-road deployment growth in the nitrogen oxide control systems market.

Industrial Boiler Revamps with Low-NOx Burners in Chemicals and Cement

Cement kilns and process heaters account for up to 12% of China's national NOx load. Regulators are increasingly prescribing retrofit timetables that favor staged combustion or SNCR over full SCR to manage capital intensity. European kilns have achieved 60% reductions using nitrogen-diluted ammonia SNCR, while new calciner designs with flue gas recirculation offer reagent-free paths to sub-500 mg/Nm³ performance. Refinery and petrochemical boilers in North America are replacing burners and adding advanced controls to comply with the U.S. Industrial Emissions revision due in July 2026, expanding burner-retrofit order books.[4]European Commission, “Euro VII Proposal Details,” Europa.eu Petrobras' decision to integrate SNOX technology, which converts NOx into saleable sulfuric acid, illustrates how by-product valorization can offset retrofit costs and diversify technology adoption within the nitrogen oxide control systems market. As a result, low-NOx burners and hybrid systems are positioned for steady, if niche, growth through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX-OPEX of SCR & SNCR solutions | -0.8% | Global, with acute pressure in emerging Asia-Pacific markets (India, ASEAN) and cost-sensitive industrial segments | Medium term (2-4 years) |

| Volatile urea/DEF pricing squeezes end-user budgets | -0.6% | Global, concentrated in regions dependent on Middle East urea exports (North America, Europe, Asia-Pacific) | Short term (≤ 2 years) |

| Ammonia-slip limits adding secondary abatement cost | -0.4% | North America & EU (stringent environmental standards), Asia-Pacific (urban air-quality zones) | Medium term (2-4 years) |

| Fleet electrification curbing future transport NOx demand | -0.5% | Europe (aggressive EV mandates), China (BEV penetration >30%), North America (light-duty transition) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX-OPEX of SCR and SNCR Solutions

Large-scale SCR costs can exceed USD 0.51 billion annually for a 660 MW coal unit in India, a burden that state generators consider unjustifiable for assets retiring before 2035. Catalyst replacement every 3-5 years adds USD 2-8 million per power block, while reagent consumption can cost an additional USD 1.2 million annually for a 500 MW plant, eroding dispatch margins in competitive power markets. For marine retrofits, 30-ton SCR reactors require structural reinforcement costing USD 3 million or more, limiting uptake in the aging bulk-carrier segment. These economics constrain adoption and reduce the nitrogen oxide control systems market CAGR forecast by 0.8 percentage points.

Volatile Urea and DEF Pricing Squeezes End-User Budgets

Natural gas price fluctuations, geopolitical export restrictions, and fertilizer demand seasonality drive year-over-year movements of more than 30% in diesel exhaust fluid expenses, destabilizing operations and maintenance budgets for transport and industrial fleets. The March 2026 Strait of Hormuz crisis took 25% of global urea exports offline, pushing New Orleans spot prices to USD 620 per short ton and increasing fleet operating costs by 15%. Supply disruptions in Q1 2025 left several EU logistics operators idling trucks due to DEF scarcity, highlighting how supplier concentration among ten major suppliers increases market vulnerability. Such volatility discourages prospective retrofits and reduces near-term spending in the nitrogen oxide control systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: SCR Retains Leadership While Adsorptive Systems Emerge

Selective catalytic reduction accounted for 55.7% of the nitrogen oxide control systems market share in 2025, and the segment is forecast to post an 8.0% CAGR through 2031, supported by power plant retrofits and IMO Tier III marine adoption.

Selective non-catalytic reduction holds a relatively smaller share due to its lower capital intensity; however, operational temperature requirements above 850°C limit its uptake to cement and boiler applications. Low-NOx burners and flue-gas recirculation are gaining traction in new industrial furnaces where reagent logistics are challenging. Adsorptive and hybrid systems could grow to triple their current size by 2031, as regenerative sorbents demonstrate 95% removal without ammonia, expanding the nitrogen oxide control systems market in remote hydrogen microgrids.

By Application: Marine Engines Outpace Legacy Power Assets

Power generation accounted for 38.1% of 2025 revenue. However, the nitrogen oxide control systems market segment derived from marine engines is expected to record the fastest growth at a 9.6% CAGR, driven by Mediterranean Emission Control Area enforcement from 2026 and a backlog of ammonia-ready vessels.

On-road diesel remains a significant revenue contributor, supported by 200,000 Shanghai trucks transmitting real-time OBD data and California fleets utilizing CARB-certified telematics to avoid fines of up to USD 42,450. Industrial boilers, kilns, and heaters also contribute to revenue, with refinery upgrades integrating NOx and SOx controls into a single system, supporting broader adoption. Cement kilns favor SNCR technology to maintain cash costs below USD 2.5 per ton of clinker.

By End-Use Industry: Transportation Narrows the Gap With Utilities

Energy and utilities accounted for 42.3% of revenue in 2025, but growth is expected to decelerate as renewable energy build-outs displace thermal plants, even as ammonia co-firing creates new retrofit cycles. The transportation segment is projected to lead the nitrogen oxide control systems market, expanding at a CAGR of 8.5%, driven by heavy-duty fleet regulations requiring 0.02 g/hp-hr performance standards in the United States.

Manufacturing and process industries are adopting blended solutions, as demonstrated by Petrobras converting NOx into sulfuric acid for resale at the RNEST refinery. Municipal waste-to-energy plants and district-heating boilers represent a niche but stable segment, with demand supported by turnkey EPC contracts bundled with 10-year catalyst service plans.

Geography Analysis

Asia-Pacific accounted for 44.6% of global revenue in 2025 and is projected to sustain a 7.7% CAGR through 2031, driven by China's 50 mg/Nm³ emission ceiling for new coal units and India's preference for lower-cost SNCR systems in older fleets. Shanghai's OBD platform has already achieved a 22% regional NOx reduction, reflecting a shift toward data-driven enforcement models that are increasing demand for connected systems.

North America's revenue is anchored by the 2027 EPA and CARB 0.02 g/hp-hr regulation, which increases the demand for sensor precision tenfold and supports investment in catalyst health analytics. In the United States, 46% of hyperscale data centers are located in non-attainment zones with annual NOx limits between 25 and 50 tons, prompting developers to adopt ultra-low-emission turbines. In Canada, refineries are implementing wet-gas scrubbers to meet multi-pollutant compliance requirements, while Mexico's cement industry is transitioning to staged-combustion burners despite inconsistent state-level regulatory enforcement.

Europe's revenue is generated under tighter margins due to Euro VII standards and the July 2026 revisions to the Industrial Emissions Directive, which require continuous monitoring for facilities exceeding 100 MW thermal capacity. Germany and the United Kingdom lead regional orders, while Norway's offshore fleet is accelerating SCR retrofits. Projects in Russia remain stalled due to sanctions. In South America, growth is supported by Petrobras' commercialization of SNOX technology. In the Middle East and Africa, pilot projects are advancing to explore ozone-injection and regenerative adsorption technologies as alternatives to address ammonia logistics challenges.

Competitive Landscape

The nitrogen oxide control systems market remains moderately concentrated. Johnson Matthey's vanadium-titania blend retains 95% conversion over 15,000 hours, supporting its position with OEM engine manufacturers.

BASF tailors zeolite formulations for sub-250 °C hydrogen exhaust, expanding its product range as utilities test 100% ammonia turbines. Niche players such as Krajete are commercializing regenerative adsorption systems that operate down to –30 °C, securing pilot projects at Audi and Chilean copper mines, and offering compliance pathways that do not rely on ammonia.

Mergers and divestitures continue to reshape company portfolios. Kanadevia Corporation acquired Babcock & Wilcox's renewables arm for USD 87 million in June 2024 and is scaling its Danish operations to pursue EU waste-to-energy mandates. Digital capabilities are also differentiating offerings; Proventia's 24/7 cloud telemetry helps fleets secure low-carbon credits, while SensorComm's IoT-based catalyst health alerts have reduced unplanned downtime by 18%.

Nitrogen Oxide (NOx) Control Systems Industry Leaders

Johnson Matthey

Babcock & Wilcox Enterprises

Mitsubishi Heavy Industries

GE Vernova (GE Power)

Kanadevia Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: According to guidance issued by the Environmental Protection Agency (EPA), US diesel engines can now switch from urea quality sensors (UQS) back to nitrous oxide (NOx) sensors.

- March 2025: Babcock & Wilcox posted a 15% year-over-year revenue uplift to USD 200.8 million and confirmed a USD 889.6 million bookings surge, with a BrightLoop hydrogen project slated for 2026 completion.

- February 2025: ANDRITZ acquired LDX Solutions, securing wet electrostatic precipitator and regenerative thermal oxidizer know-how complementary to SCR systems.

- January 2025: Primoris Services began constructing the world’s largest SCR on Unit 4 at Grand River Energy Center in Oklahoma.

Global Nitrogen Oxide (NOx) Control Systems Market Report Scope

Nitrogen Oxide control systems, such as Selective Catalytic Reduction (SCR) and Selective Non-Catalytic Reduction (SNCR), are pivotal in curbing harmful nitrogen oxide emissions from industrial boilers, power plants, and engines. SCR enhances efficiency using catalysts along with ammonia or urea, whereas SNCR functions at elevated temperatures without the need for a catalyst.

The nitrogen oxide control systems market is segmented by technology, application, end-use industry, and geography. By technology, the market is segmented into selective catalytic reduction, selective non-catalytic reduction, low-NOx burners, flue gas recirculation, scrubber and hybrid systems. By application, the market is segmented into power generation, industrial boilers and furnaces, cement manufacturing, chemicals and petrochemicals, on-road and off-road automotive, and marine engines. By end-use industry, the market is segmented into energy and utilities, manufacturing and process industries, transportation, and others. The report also covers the market size and forecasts for the nitrogen oxide control systems market in 19 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Selective Catalytic Reduction (SCR) |

| Selective Non-Catalytic Reduction (SNCR) |

| Low-NOx Burners |

| Flue Gas Recirculation |

| Scrubber and Hybrid Systems |

| Power Generation |

| Industrial Boilers and Furnaces |

| Cement Manufacturing |

| Chemicals and Petrochemicals |

| On-road and Off-road Automotive |

| Marine Engines |

| Energy and Utilities |

| Manufacturing and Process Industries |

| Transportation (Road, Rail, Marine) |

| Others (Municipal, Commercial) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Technology | Selective Catalytic Reduction (SCR) | |

| Selective Non-Catalytic Reduction (SNCR) | ||

| Low-NOx Burners | ||

| Flue Gas Recirculation | ||

| Scrubber and Hybrid Systems | ||

| By Application | Power Generation | |

| Industrial Boilers and Furnaces | ||

| Cement Manufacturing | ||

| Chemicals and Petrochemicals | ||

| On-road and Off-road Automotive | ||

| Marine Engines | ||

| By End-Use Industry | Energy and Utilities | |

| Manufacturing and Process Industries | ||

| Transportation (Road, Rail, Marine) | ||

| Others (Municipal, Commercial) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the global nitrogen oxide control systems market ?

The Nitrogen Oxide Control Systems Market size is expected to grow from USD 7.15 billion in 2025 to USD 7.69 billion in 2026 and is forecast to reach USD 10.78 billion by 2031 at 6.99% CAGR over 2026-2031.

Which application will expand quickest by 2031?

Marine engines, forecast to grow at a 9.6% CAGR as the Mediterranean Emission Control Area widens IMO Tier III coverage.

What region commands the largest share today?

Asia-Pacific, holding 44.6% of 2025 revenue and expected to keep leadership through 2031.

How volatile are urea costs for fleet operators?

March 2026 prices in New Orleans jumped USD 70 a short ton to USD 620, adding roughly 15% to per-mile expenses.

Which technology suits hydrogen or ammonia combustion exhaust?

Copper-zeolite catalysts and regenerative adsorption systems show >90% NOx conversion below 250 °C, addressing low-temperature hydrogen exhaust.

What role does telematics play in compliance?

Real-time OBD data allow fleets to avoid penalties up to USD 42,450 and monetize low-carbon credits while verifying catalyst efficiency.

Page last updated on: