Malaysia Data Center Cooling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

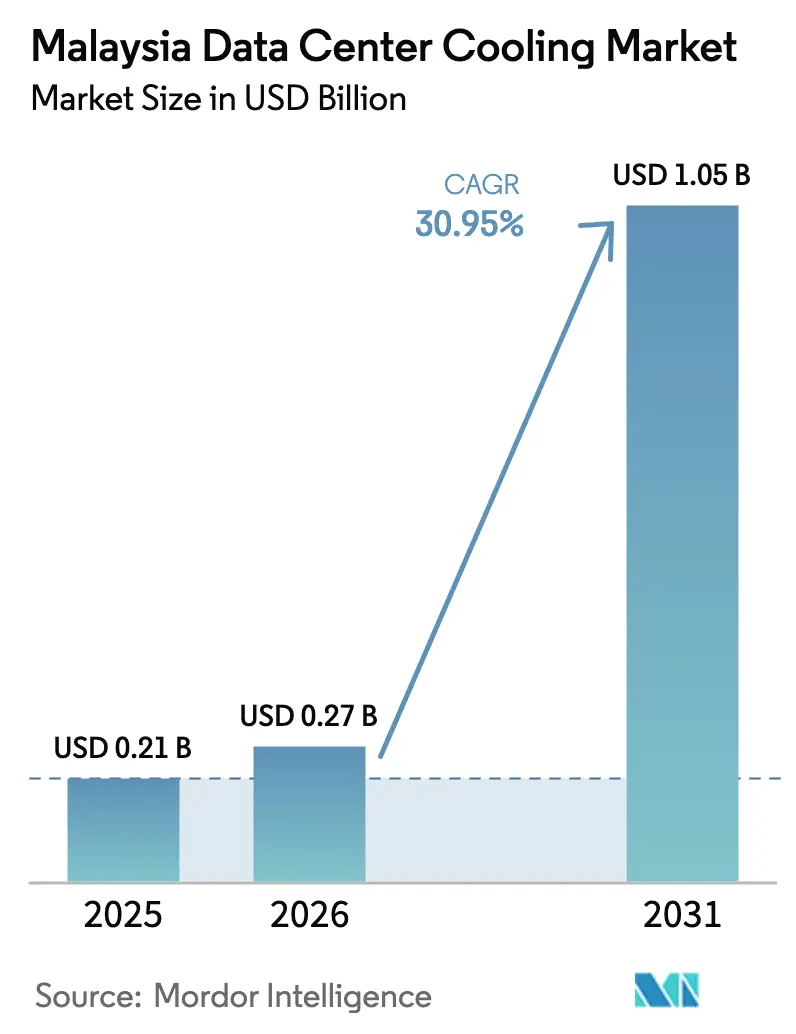

| Base Year Market Size (2025) | USD 0.21 Billion |

| Market Size (2026) | USD 0.27 Billion |

| Market Size (2031) | USD 1.05 Billion |

| Growth Rate (2026 - 2031) | 30.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Data Center Cooling Market Analysis by Mordor Intelligence

The Malaysia data center cooling market size is projected to expand from USD 0.21 billion in 2025 and USD 0.27 billion in 2026 to USD 1.05 billion by 2031, registering a CAGR of 30.95% between 2026 to 2031. Surging hyperscale construction activity in Johor, the pivot from air to liquid technologies for graphics-processing workloads, and generous tax breaks under the MyDIGITAL Blueprint are reinforcing Malaysia’s position as Southeast Asia’s fastest-growing digital infrastructure hub. Accelerated rack-density growth above 40 kilowatts per rack is pushing existing chilled-air plants toward thermal limits, while grid-modernization programs that unlock long-term renewable power purchase agreements are lowering the risk profile of high-capacity liquid systems. Competitive pressure among equipment vendors is intensifying as global OEMs introduce AI-driven controls that promise sub-1.30 power usage effectiveness, shortening payback periods despite capital-cost premiums. Operators are capitalizing on spill-over demand from Singapore’s data-center moratorium, but must navigate volatility in electricity tariffs and a shortage of liquid-cooling specialists, which can delay commissioning schedules.

Key Report Takeaways

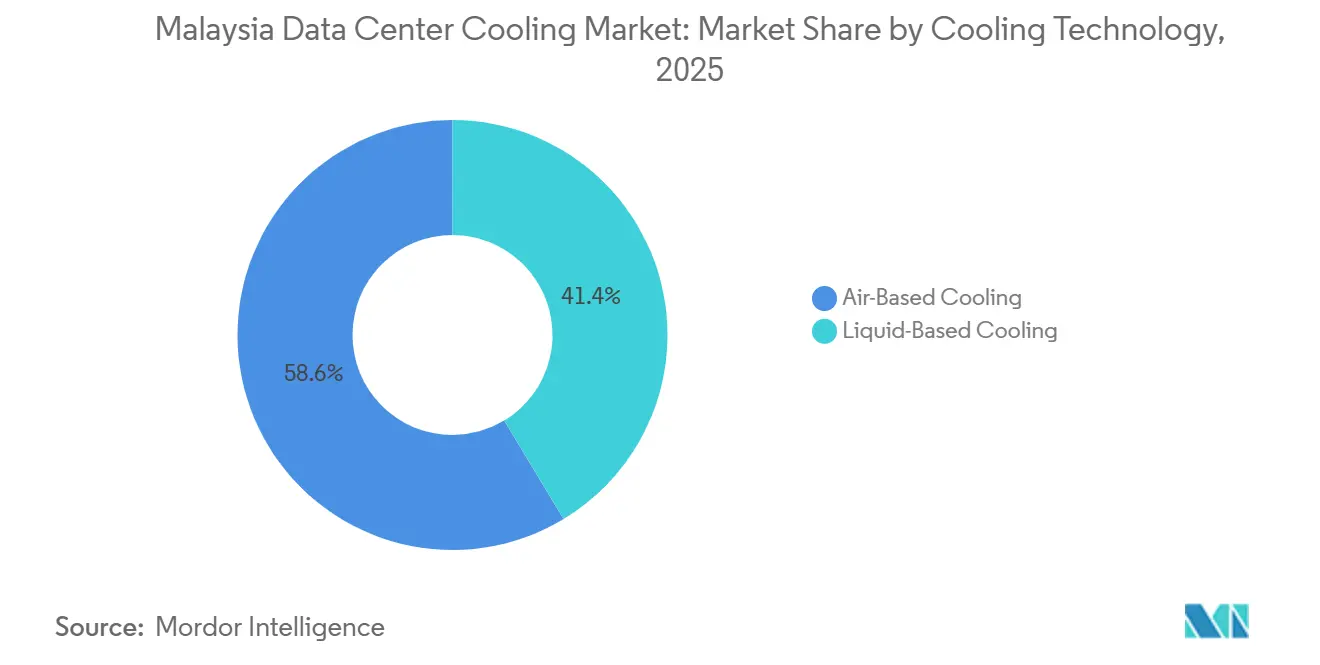

- By cooling technology, liquid systems are on track to record the fastest growth at 31.43% CAGR through 2031, lifting their share well above the 41.36% recorded in 2025.

- By component, pumps and valves are forecast to outpace all other categories at 31.77% CAGR to 2031, overtaking the 40.47% share held by computer-room air handlers and chillers in 2025.

- By tier type, tier 4 projects are advancing at a 31.84% CAGR, whereas tier 3 facilities led with 51.82% market share in 2025.

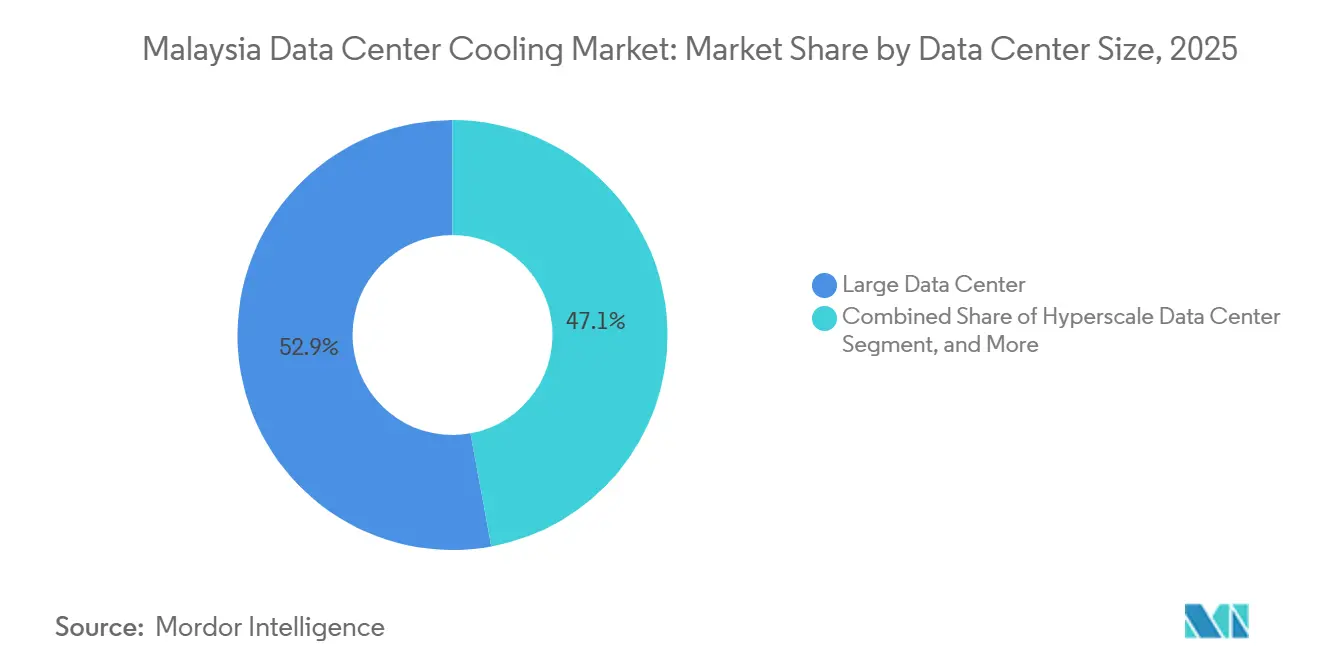

- By data center size, hyperscale campuses are projected to expand at a 31.68% CAGR, eclipsing the 52.88% share held by large data centers in 2025.

- By data-center type, hyperscaler and cloud-provider facilities are growing at a 31.52% CAGR, challenging the 53.07% share held by colocation operators in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Data Center Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI and GPU Workload Density Triggering Shift to Advanced Liquid Cooling | +8.2% | Johor, Cyberjaya, Selangor | Medium term (2-4 years) |

| Surge in Hyperscale and Colocation Investments Accelerating Cooling Demand | +7.5% | National, concentration in Johor and Selangor | Short term (≤ 2 years) |

| Singapore Data Center Cap Driving Spill-Over Build-Outs in Johor | +6.1% | Johor (Iskandar Puteri, Nusajaya, Gelang Patah) | Short term (≤ 2 years) |

| Government Tax Incentives and MyDIGITAL Blueprint Supporting Data Center Build-Out | +4.8% | National, early gains in Johor, Cyberjaya, Penang | Medium term (2-4 years) |

| Strategic Location of Malaysia as Regional Hub in Asia-Pacific | +2.9% | National, spill-over to ASEAN corridors | Long term (≥ 4 years) |

| National Grid-Modernization CRESS and Renewable Power Purchase Enabling High-Power Data Centers | +2.4% | National, pilot deployments in Johor and Selangor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI and GPU Workload Density Triggering Shift to Advanced Liquid Cooling

Artificial-intelligence clusters are already driving rack-level power to 40-60 kilowatts in Malaysia’s newest campuses, a density that forces operators to abandon traditional computer-room air handlers. YTL Data Centre’s JDC2 facility allocated 80% of its 100-megawatt IT load to direct-to-chip loops, demonstrating how quickly liquid designs have become baseline rather than premium. Vertiv responded by introducing the CoolLoop oil-free centrifugal chiller, which operates at leaving-water temperatures of 25 °C and ties into mixed air-and-liquid loops, shaving 18% off upfront capital compared with parallel plants. TM Nxera’s 280-megawatt campus in Iskandar Puteri embedded similar technology to meet hyperscaler service-level agreements that prohibit thermal throttling. The rapid pivot has tightened the labor pool; two Johor projects reported handover delays in early 2025 because contractors lacked experience balancing dual-loop manifolds.

Surge in Hyperscale and Colocation Investments Accelerating Cooling Demand

Operators announced more than USD 3 billion in greenfield capacity between January 2025 and February 2026, translating into multi-year cooling orders often placed before design-finalization milestones. AirTrunk’s JHB2, scalable to 270 megawatts, targets a PUE of 1.25 by relying on high-temperature liquid circuits and optimized chiller staging. STT GDC broke ground on a 16-megawatt first phase at Nusa Cemerlang Industrial Park in February 2026 while banking land for a 120-megawatt build-out, embedding AI analytics in cooling controls from day one. Construction velocity is straining supply chains; lead times for centrifugal chillers have doubled to 28 weeks as OEMs prioritize projects with secured power connections.

Singapore Data Center Cap Driving Spill-Over Build-Outs in Johor

Singapore’s indefinite development pause is redirecting about 60% of regional hyperscale demand into Johor, where cross-border fiber supports sub-2-millisecond latency. Johor booked 260 megawatts of take-up in the first half of 2025 and amassed a 5.8-gigawatt pipeline by year-end, compressing cooling-water availability and prompting a state-level moratorium on evaporative systems until mid-2027.[1]Ken Wong, “Singtel and TM Break Ground on Johor Data Centre Campus,” HardwareZone Singapore, hardwarezone.com.sg Microsoft’s zero-water deployment in Johor Bahru showcased closed-loop air-cooled chillers coupled with warm-water liquid racks that eliminate freshwater withdrawal, setting a benchmark now embedded in new state permitting guidelines.[2]Dashveenjit Kaur, “Microsoft’s Zero-Water Datacenter Cooling Strategy,” TechWire Asia, techwireasia.com Spill-over timelines are aggressive; builds that once took 30 months in Singapore are now targeting 18 months in Johor, elevating commissioning risk.

Government Tax Incentives and MyDIGITAL Blueprint Supporting Data Center Build-Out

Malaysia offers a 10-year income-tax holiday and import-duty relief on mechanical and electrical components, trimming total project capex by up to 15%.[3]Jazlin Zakri, “Telekom Malaysia Secures Power Supply for Data Centre,” EdgeProp.my, edgeprop.my The CRESS framework lets operators negotiate dedicated power lines above 200 megawatts and accelerates environmental approvals for projects that incorporate liquid or hybrid cooling. Bridge Data Centres and DayOne each secured more than 400 megawatts under the scheme in 2024-2025, but approvals hinge on strict water-use thresholds that favor closed-loop designs. State governments in Selangor and Penang added property-tax rebates for LEED-certified facilities, influencing retrofit decisions toward high-efficiency chillers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Electricity Tariffs and Emerging Carbon-Pricing Uncertainty | -3.8% | National, acute in Selangor and Johor | Short term (≤ 2 years) |

| Higher Energy Consumption and Water Needs for Data Center Cooling | -2.6% | Johor (water-stressed), Selangor (grid-constrained) | Medium term (2-4 years) |

| Limited Recycled-Water Infrastructure for Sustainable Cooling | -1.4% | Johor, pilot projects in Iskandar Puteri | Medium term (2-4 years) |

| Skills Gap in Liquid-Cooling Design and Maintenance Workforce | -1.1% | National, shortages in Johor and Penang | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Electricity Tariffs and Emerging Carbon-Pricing Uncertainty

Tenaga Nasional Bhd’s tariff restructure lifted rates for ultra-high-voltage customers by 10-14% in late 2024, raising annual operating expense by up to USD 20 million for a 100-megawatt site. Operators face further uncertainty as Malaysia prepares to align carbon pricing with ASEAN frameworks by 2027, potentially adding 5-8% to power bills for plants running on the present 60% fossil mix. Equinix Malaysia began scouting alternative energy providers in July 2025, confirming that tariff risk now influences site selection. Volatile fuel surcharges complicate return-on-investment models for advanced chillers whose efficiency gains can be negated by a single tariff hike.

Higher Energy Consumption and Water Needs for Data Center Cooling

Cooling accounts for 30-40% of facility energy in Malaysia’s tropical climate and can rise to 45% in legacy air-cooled halls. Johor’s water cap until mid-2027 forces operators to adopt dry coolers or closed-loop liquid systems that cost 25-35% more to install but eliminate millions of liters of annual evaporation. AirTrunk evaluated treated greywater to serve its JHB2 campus, illustrating how water scarcity extends permitting by up to nine months. Liquid cooling lowers total energy by 20-30% versus air at equal density, yet concentrates thermal load into pumps and manifolds that demand higher-grade power redundancy, lifting capex for Tier IV builds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Technology: Liquid Systems Gain As AI Racks Exceed Air Limits

Liquid solutions captured a growing slice of the Malaysia data center cooling market in 2025 and are set to record 31.43% CAGR through 2031, eclipsing the 58.64% share still held by air-based methods in 2025. The Malaysia data center cooling market size for liquid technologies is anticipated to outstrip that of air systems by the end of the forecast, reflecting the inability of computer-room air handlers to sustain racks above 30 kilowatts. Immersion remains below 3% but rear-door heat exchangers and direct-to-chip loops are scaling fast at hyperscale campuses.

Air remains dominant in edge and enterprise locations, where rack loads rarely exceed 15 kilowatts and capital discipline favors CRAH units tied to perimeter towers. Hybrid loops using high-temperature chillers and warm-water liquid drops extend legacy plants without full replacement costs. Policy limits on evaporative cooling in Johor will further reinforce liquid adoption, making the Malaysia data center cooling market a proving ground for zero-water techniques pioneered by hyperscalers.

By Cooling Component: Pumps And Valves Surge Alongside Liquid Retrofits

Computer-room air handlers and chillers accounted for 40.47% of the market in 2025. However, pumps and valves are forecast to lead component growth at a 31.77% CAGR as liquid distribution networks multiply across high-density halls. The Malaysia data center cooling market share for pumps will climb as operators deploy redundant N+1 or 2N pumping arrays to satisfy Tier IV uptime targets.

Integrated control software is shifting from siloed building-management systems toward AI-enabled platforms that co-optimize chiller staging and pump speed. Southco’s Blind Mate Floating Mechanism improves serviceability of direct-to-chip quick-disconnects, reducing leak risk and downtime. Modular dry coolers are gaining ground on water-constrained sites, even as they incur a 10-15% efficiency penalty compared to wet towers.

By Tier Type: Tier 4 Builds Accelerate For AI Uptime Guarantees

Tier 3 facilities still accounted for the largest share, at 51.82%, in 2025. However, tier 4 value is projected to rise 31.84% annually as AI workloads demand 99.995% availability. The Malaysia data center cooling market for tier 4 will expand rapidly, driven by 2N liquid-loop redundancy and fault-tolerant chiller trains.

Tier 1 and Tier 2 remain relevant for edge nodes. However, incremental growth is skewed toward tier 3 colocation retrofits that add rear-door exchangers without full Tier 4 cost. Vendors are under margin pressure as operators insist on tier 4 resilience at near-tier 3 pricing, compelling OEMs to modularize chillers and distributors to negotiate fleet contracts.

By Data Center Size: Hyperscale Campuses Reshape Thermal Infrastructure

Large facilities held 52.88% of the market share in 2025. Hyperscale builds above 50 megawatts are projected to grow at a 31.68% CAGR, making them the dominant volume driver for the Malaysia data center cooling market. Central utility plants with multiple centrifugal units and AI-driven optimization are replacing skid-mounted chillers, improving partial-load efficiency.

Medium and small sites continue to rely on proven air-cooled solutions. However, hyperscale standardization on liquid skids shortens deployment to eight weeks, pressuring smaller plants to upgrade or risk customer churn. Vendor roadmaps now prioritize pre-fabricated manifolds to align with hyperscale delivery models.

By Data Center Type: Hyperscalers And Cloud Providers Drive Liquid Adoption

Colocation assets captured 53.07% share in 2025, but hyperscaler and cloud units are expanding 31.52% annually, shifting future share toward single-tenant campuses that optimize every variable for GPU racks. The Malaysia data center cooling industry is witnessing hyperscalers vertically integrate design and procurement, bypassing traditional contractors for direct OEM engagement. This purchasing leverage allows them to standardize liquid loop specifications across multiple Malaysian campuses, driving down lifecycle costs and accelerating deployment schedules.

Colocation operators respond with liquid-cooling-as-a-service pricing and hybrid upgrade paths that minimize tenant disruption. Enterprise and edge demand remains steady in secondary cities, though rising power tariffs may catalyze migration into efficient colocation halls. Providers in Cyberjaya and Penang are also bundling renewable power options with advanced cooling retrofits to meet tightening sustainability scorecards.

Geography Analysis

Johor, Selangor, and Cyberjaya collectively accounted for roughly 85% of 2025 cooling spend, anchored by the spill-over effect from Singapore’s capacity restrictions. Johor alone tallied 260 megawatts of take-up in the first half of 2025 and boasted a 5.8-gigawatt pipeline by year-end. Microsoft, TM Nxera, and AirTrunk headline the roster of liquid-ready megacampuses that now define the Malaysia data center cooling market in the state.

Cyberjaya and Selangor benefited from mature fiber routes and proximity to Kuala Lumpur’s enterprise core. However, these regions face land scarcity and rising tariffs, which slow large-scale expansion. Retrofit activity is vibrant, with operators pursuing LEED credits and high-efficiency chillers to qualify for state tax rebates.

Penang holds a smaller share, serving northern manufacturing clusters with mid-sized air-cooled halls. Future upside depends on grid upgrades that could harness offshore wind for renewable cooling power. Johor’s moratorium on evaporative towers until 2027 is catalyzing zero-water innovation, a trend likely to radiate north as environmental scrutiny intensifies.

Competitive Landscape

The Malaysia data center cooling market is moderately consolidated, and these consolidation trends are emerging as hyperscalers gravitate toward vertically integrated platforms. Schneider Electric, Vertiv, and Huawei secure most awards of> 50 megawatts because their portfolios bundle chillers, pumps, and AI control in a single support contract. Regional challengers such as Daikin, Stulz, and Munters focus on midsized halls where service proximity outweighs integrated analytics.

Local specialists retain relevance in retrofit and mechanical-ventilation scopes. iCents Group’s RM 29.38 million in 2026 awards illustrates how small engineering firms capture CRAH and ductwork assignments even as liquid cooling ascends. Technology disruptors add competitive tension; Southco’s quick-connect innovation eases hot-swap maintenance, while Vertiv’s sensor suite forecasts component failure 30-60 days out, reducing unscheduled downtime.

Hyperscalers are gradually self-performing cooling design. Microsoft’s direct OEM engagement for its Johor Bahru zero-water plant bypassed local contractors, foreshadowing a margin squeeze for integrators that rely on build-only contracts. Private-equity interest in assembling nationwide service networks is rising, but elevated valuations and uncertain tariff trajectories kept large M and A dormant through early 2026.

Malaysia Data Center Cooling Industry Leaders

Schneider Electric SE

Rittal Gmbh & Co. KG

Vertiv Group Corp.

Johnson Controls Inc.

Alfa Laval AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: AirTrunk unveiled its second Malaysian facility, JHB2 in Johor, scalable beyond 270 megawatts and designed for AI workloads using high-temperature liquid loops.

- February 2026: STT GDC broke ground on STT Johor 1, a 16 -megawatt phase within a 22-acre campus that can reach 120 megawatts and will operate on smart energy-management systems.

- January 2026: TM Nxera secured a 280-megawatt electricity agreement with Tenaga Nasional Bhd to power its AI-ready green campus in Iskandar Puteri.

- January 2026: Southco Asia released its Blind Mate Floating Mechanism for liquid connectors, supporting ±4 millimeters radial movement and 300 psig burst compliance.

Malaysia Data Center Cooling Market Report Scope

Data center cooling is a set of techniques and technologies to maintain optimal operating temperatures in data center environments. Data center cooling is critical as data center facilities house many computer servers and network equipment that generate heat during operation. Efficient cooling systems are used to dissipate this heat and prevent equipment from overheating, ensuring continued reliable operation of the data center. Various methods, such as air conditioning, liquid cooling, and hot/cold aisle containment, are commonly used to control temperature and humidity in data centers.

The Malaysia Data Center Cooling Market Report is Segmented by Cooling Technology (Air-Based Cooling, and Liquid-Based Cooling), Cooling Component (CRAH/CRAC, Chillers and Heat-Exchanger Units, Cooling Towers and Dry Coolers, Pumps and Valves, and Control and Monitoring Software), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Size (Small, Medium, Large, and Hyperscale), Data Center Type (Colocation, Hyperscalers/CSPs, and Enterprise and Edge). The Market Forecasts are Provided in Terms of Value (USD).

| Air-Based Cooling | CRAH |

| Chiller and Economizer | |

| Cooling Tower (Direct, Indirect, Two-Stage) | |

| Others | |

| Liquid-Based Cooling | Immersion Cooling |

| Direct-to-Chip Cooling | |

| Rear-Door Heat Exchanger |

| Computer-Room Air Handlers (CRAH/CRAC) |

| Chillers and Heat-Exchanger Units |

| Cooling Towers and Dry Coolers |

| Pumps and Valves |

| Control and Monitoring Software |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Small Data Center |

| Medium Data Center |

| Large Data Center |

| Hyperscale Data Center |

| Colocation Data Center |

| Hyperscalers Data Center/CSPs |

| Enterprise and Edge Data Center |

| By Cooling Technology | Air-Based Cooling | CRAH |

| Chiller and Economizer | ||

| Cooling Tower (Direct, Indirect, Two-Stage) | ||

| Others | ||

| Liquid-Based Cooling | Immersion Cooling | |

| Direct-to-Chip Cooling | ||

| Rear-Door Heat Exchanger | ||

| By Cooling Component | Computer-Room Air Handlers (CRAH/CRAC) | |

| Chillers and Heat-Exchanger Units | ||

| Cooling Towers and Dry Coolers | ||

| Pumps and Valves | ||

| Control and Monitoring Software | ||

| By Tier Type | Tier 1 and 2 | |

| Tier 3 | ||

| Tier 4 | ||

| By Data Center Size | Small Data Center | |

| Medium Data Center | ||

| Large Data Center | ||

| Hyperscale Data Center | ||

| By Data Center Type | Colocation Data Center | |

| Hyperscalers Data Center/CSPs | ||

| Enterprise and Edge Data Center | ||

Key Questions Answered in the Report

How large will Malaysia’s data-center cooling spend become by 2031?

It is forecast to reach USD 1.05 billion by 2031, rising at a 30.95% CAGR from 2026.

Which cooling technology is growing fastest in Malaysia?

Liquid systems are projected to grow 31.43% annually as AI racks exceed the thermal limits of air handlers.

What is driving hyperscale investment into Johor?

Singapore’s capacity cap, sub-2-millisecond fiber latency, and state-level tax incentives steer hyperscale builders southward into Johor.

How are operators addressing water scarcity in Johor?

They deploy closed-loop liquid systems, dry coolers, and zero-water strategies such as Microsoft’s Johor Bahru design.

Why are electricity tariffs a concern for Malaysian data centers?

A late-2024 tariff restructure raised ultra-high-voltage rates 10-14%, increasing annual OPEX for 100-megawatt sites by up to USD 20 million.

Which vendors dominate hyperscale cooling contracts?

Schneider Electric, Vertiv, and Huawei secure most more than 50-megawatt awards owing to integrated hardware and AI analytics.

Page last updated on: