Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

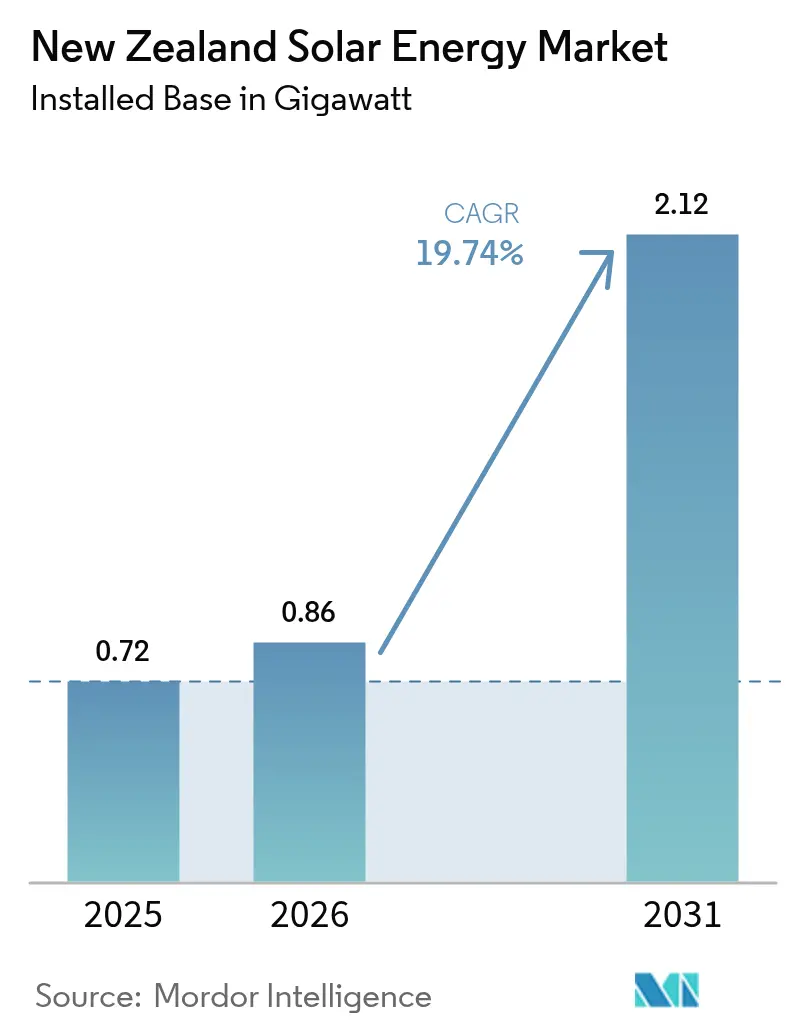

| Base Year Market Size (2025) | 0.72 gigawatt |

| Market Volume (2026) | 0.86 gigawatt |

| Market Volume (2031) | 2.12 gigawatt |

| Growth Rate (2026 - 2031) | 19.74% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

New Zealand Solar Energy Market Analysis by Mordor Intelligence

The New Zealand Solar Energy Market size was valued at 0.72 gigawatt in 2025 and estimated to grow from 0.86 gigawatt in 2026 to reach 2.12 gigawatt by 2031, at a CAGR of 19.74% during the forecast period (2026-2031).

Falling levelised generation costs, escalating corporate renewable procurement, and accelerated grid-modernization programs are repositioning solar photovoltaic (PV) technology as a central pillar of the country’s energy transition. Investment momentum signals a structural shift away from the hydro-dominated legacy mix toward a diversified portfolio in which solar capacity is projected to triple within the period. Data-center power-purchase agreements (PPAs), led by Microsoft’s NZD 4.3 billion (USD 2.6 billion) cloud investment, are reshaping demand profiles while stimulating utility-scale build-outs.[1]Microsoft Corporation, “Cloud Infrastructure Sustainability Commitments,” microsoft.com Meanwhile, nationwide smart-meter penetration supports granular settlement, which raises returns for distributed generation, and the Transpower Renewable Energy Zone (REZ) framework reduces grid connection risk for clustered projects.[2]Transpower New Zealand, “Renewable Energy Zone Consultation,” transpower.co.nz Overall, on-grid installations dominate, but robust off-grid growth highlights the market’s widening application spectrum.

Key Report Takeaways

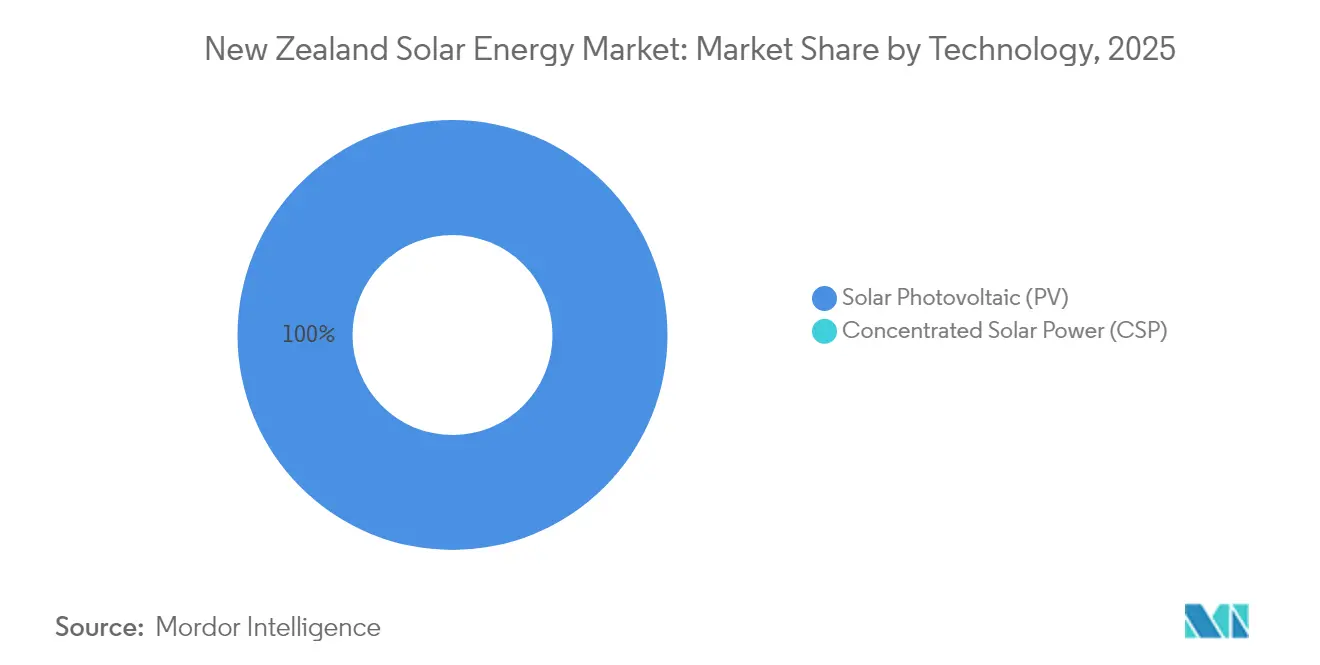

- By technology, solar PV held 100.00% of the New Zealand solar energy market share in 2025 and is projected to grow at a 19.85% CAGR through 2031.

- By connection type, on-grid systems led the New Zealand solar energy market with 97.65% of the market size in 2025, while off-grid installations are expected to record the fastest growth, at a 22.10% CAGR, to 2031.

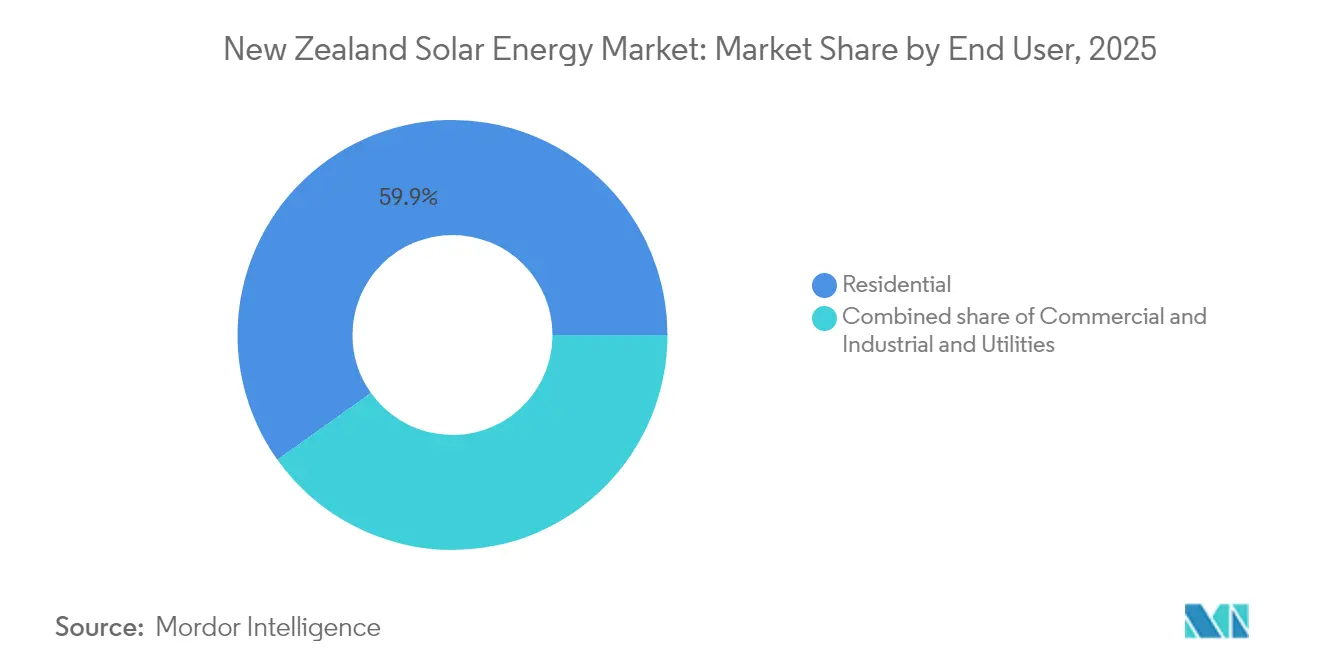

- By end user, residential rooftops commanded 59.85% of the New Zealand solar energy market in 2025; utility-scale projects are forecast to expand at a 21.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

New Zealand Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid decline in levelised cost of solar electricity | +4.2% | National with emphasis on Auckland and Canterbury | Short term (≤ 2 years) |

| Corporate-PPA boom from data centers & hyperscalers | +3.8% | Concentrated in the North Island with spillover to the South Island | Medium term (2-4 years) |

| Smart-meter roll-out enabling half-hour settlement | +2.1% | National roll-out with urban priority areas | Medium term (2-4 years) |

| Emerging solar-plus-agrivoltaics pilots on dairy farms | +1.4% | Canterbury, Waikato, Taranaki dairy regions | Long term (≥ 4 years) |

| Transpower Renewable-Energy-Zone model | +2.9% | Designated zones across both islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in Levelised Cost of Solar Electricity

The levelised cost of electricity for PV systems fell to NZD 0.08–0.12 per kWh (USD 0.048-0.072) in 2024, matching wholesale spot prices for the first time. Gains stem from global scale economies and module efficiencies topping 22%, creating viable economics across residential and commercial segments. Solar-leasing programs, such as solarZero’s service model, lower upfront costs and raise adoption. As storage prices soften, self-consumption rates improve, reinforcing competitiveness against hydro-peaking imports during dry years. The trajectory supports sustained cost leadership over fossil peakers.

Corporate-PPA Boom from Data Centers & Hyperscalers

Microsoft’s long-term renewable PPA with Meridian Energy anchors a surge of hyperscale procurement commitments. AWS and Google Cloud are evaluating similar arrangements, offering 15-20-year revenue stability for solar developers while providing corporations cost certainty. These bilateral contracts reduce merchant risk, catalyze financing, and reallocate generation away from spot exposure. Utility-scale projects linked to PPAs are therefore rising as prime growth vehicles.

Smart-Meter Roll-Out Enabling Half-Hour Settlement

Advanced metering now covers 87% of households, enabling half-hourly settlement that rewards flexible distributed resources. Solar owners can arbitrage peak-evening prices through paired batteries, boosting project internal rates of return up to 18% beyond simple net-metering cases. Vector’s analytics show how granular pricing signals encourage load shifting and virtual power plant aggregation, strengthening the economics of rooftop PV.

Emerging Solar-Plus-Agrivoltaics Pilots on Dairy Farms

Pilots in Canterbury and Waikato demonstrate the dual use of land, where elevated arrays lower evapotranspiration by 15-20% and yield 800-1,200 kWh per kW annually.[3]AgResearch, “Agrivoltaics Dairy Farm Trials 2024,” agresearch.co.nz Early data suggest that shading can extend grazing seasons and mitigate livestock heat stress, aligning with dairy methane reduction targets. Commercial roll-out depends on tailored finance and streamlined consents, yet pilot success signals promising co-benefits in rural regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Distribution-network hosting-capacity constraints | -2.7% | Auckland, Wellington, Christchurch urban zones | Short term (≤ 2 years) |

| Lengthy resource-consent process under the RMA | -1.8% | National with heightened impact in sensitive districts | Medium term (2-4 years) |

| Limited domestic PV-trained workforce | -1.2% | Nationwide shortages, acute in rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Distribution-Network Hosting-Capacity Constraints

Auckland’s Vector and Christchurch’s Orion networks have imposed moratoriums where rooftop penetration saturates local transformers, causing voltage violations. Reinforcement and smart-inverter retrofits require up to 24 months, which can slow approvals for new residential systems. Hosting-capacity maps and dynamic operating envelopes are under trial, but near-term bottlenecks persist.

Lengthy Resource-Consent Process Under the RMA

Utility-scale projects typically face approval periods of 12-18 months, which can extend beyond three years if appeals are filed.[4]Ministry for the Environment, “RMA Consenting Statistics 2024,” mfe.govt.nz Fast-track legislation enacted in 2024 shortens timelines for designated projects, yet procedural complexity remains, especially on high-value agricultural land. Smaller developers, lacking deep legal resources, perceive an elevated risk, which dampens pipeline diversity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Solar PV Dominance Reflects Resource Constraints

Solar PV holds 100.00% share of the New Zealand solar energy market in 2025 and advances at a 19.85% CAGR through 2031. Crystalline-silicon modules account for 85% of the built capacity, with mono-PERC arrays gaining traction due to their higher power density and aesthetic appeal. The New Zealand solar energy market size for PV projects is expected to rise in tandem with Transpower’s REZ build-out, while concentrated solar power remains underutilized due to high diffuse radiation levels.

Perovskite-silicon tandem cells, forecasted to reach over 30% efficiency by 2028, could accelerate repowering cycles and enhance urban yield potential. Thin-film solutions retain niche positions in building-integrated contexts where flexibility and partial shading tolerance offset lower module efficiency. Technological learning rates ensure PV’s continued cost decline and sustained market leadership.

By Connection Type: Off-Grid Acceleration Despite On-Grid Dominance

On-grid systems controlled 97.65% of the New Zealand solar energy market share in 2025, underpinned by net metering policies and an extensive network reach. Grid-tied arrays exhibit 15-20% higher capacity factors compared to standalone systems, owing to optimized inverter loading and zero battery cycling losses.

Off-grid deployment, although accounting for only 2.35% of the New Zealand solar energy market size, is growing at a 22.10% CAGR. Remote farms, telecom relays, and micro-grids adopt hybrid PV-battery units where line extensions cost more than NZD 50,000 per km. Falling storage prices and resilience requirements strengthen the business case even as grid connections dominate aggregate capacity.

By End User: Utility-Scale Momentum Challenges Residential Leadership

The residential category retained 59.85% of 2025 installations, driven by rebates, seven- to ten-year payback periods, and solar-as-a-service contracts. Typical systems average 5 kW and leverage smart-meter settlement to monetize peak exports.

Utility-scale assets, driven by hyperscale PPAs, are projected to accelerate at a 21.90% CAGR, outpacing all other segments. Projects such as Meridian’s 130 MW Ruakākā and Genesis Energy’s 63 MW Canterbury installations demonstrate economies of scale and grid service capability. Commercial & industrial rooftops continue steady growth as demand-charge abatement and ESG reporting drive behind-the-meter adoption.

Geography Analysis

The North Island hosts approximately 69.60% of the cumulative PV capacity, led by Auckland’s 180 MW distributed base, which draws on an annual irradiance of 1,650–1,750 kWh/m². The regional New Zealand solar energy market size expands under data-center demand but faces hosting-capacity constraints that saturate urban feeders. Transpower’s REZ planning prioritizes additional bulk supply points to alleviate congestion.

Canterbury stands out as the South Island’s rising hub, enjoying 1,800+ kWh/m² irradiance and abundant flat land. The province is forecast to capture 35.10-39.90% of new utility-scale capacity additions to 2031, supported by agrivoltaics pilots and streamlined consents. Large dairy operations integrate elevated arrays that protect pasture moisture while supplying on-site loads, illustrating dual-benefit models.

Otago and Hawke’s Bay are secondary growth nodes owing to robust solar resources and proximity to high-demand horticultural processing. The West Coast and Southland lag behind due to persistent cloud cover and sparse population, although niche off-grid tourism and aquaculture projects are emerging to serve isolated sites. Overall, geographic deployment reflects resource-load alignment and grid-capacity availability, with the New Zealand solar energy market continuing its north-south diffusion trend.

Regulatory Landscape

New Zealand solar deployment is governed primarily through the Electricity Authority (EA) and the Electricity Industry Participation Code 2010, including Part 6 rules for distributed generation connections and compliance expectations tied to AS/NZS 4777.2:2020 (with Amendments). In May 2026, Code changes introduced a default 10 kW export limit for small-scale distributed generation on low-voltage networks, formalizing how lines companies manage backfeed and voltage impacts as rooftop penetration rises.

Planning and consenting settings are also shifting to explicitly enable renewables. The National Policy Statement for Renewable Electricity Generation (NPS REG) Amendment 2025 took effect on 15 January 2026, directing decision-makers to provide for renewable electricity generation assets and activities across locations, for both utility-scale projects and enabling infrastructure. Alongside these changes, a Ministry-led sector review launched on 7 May 2026 targets reductions in regulatory costs and complexity for residential and small-to-medium solar, while EA network-connection reforms are scheduled to roll out in stages from 1 December 2026 for distributed generation connections.

Competitive Landscape

The industry is moderately fragmented, yet consolidation accelerates as incumbents pursue vertical integration. Meridian Energy, Mercury NZ, and Genesis Energy leverage balance-sheet strength to develop, own, and retail solar power, capturing full value-chain margins. Specialized firms such as solarZero and Lodestone Energy compete through service innovation, offering leasing plans and agrivoltaics concepts that address niche customer needs.

Hardware differentiation is limited because most installers source from global tier-1 suppliers, including JinkoSolar, Trina Solar, and Canadian Solar. Consequently, competition pivots toward financing creativity, digital monitoring platforms, and bundled storage. Emerging aggregators assemble distributed PV and batteries into virtual power plants that sell reserve services, signaling a pivot toward platform-based revenue models. Utilities respond by acquiring installer networks and investing in customer-side analytics to protect downstream relationships.

Mergers, joint ventures, and corporate PPAs drive intensifying market concentration. Contact Energy’s partnership with Lightsource bp on the 400 MW Te Rahui project exemplifies how local and international alliances accelerate scale and capital access. Workforce-training initiatives launched by the Solar Energy Association of New Zealand address installer shortages, supporting execution capacity amid the sector’s rapid growth.

New Zealand Solar Energy Industry Leaders

Meridian Energy Ltd

Mercury NZ Ltd

solarZero Ltd

Lodestone Energy Ltd

Genesis Energy Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Corporate procurement and utility-scale build-outs create whitespace beyond the historically residential-led base. In 2025, New Zealand exceeded 96% renewable electricity generation during October to December, while utility-scale solar output grew by more than 70% versus 2024, which points to capacity for solar to contribute to energy diversity in a renewables-dominant system. Developer actions in 2026 further reinforce momentum, including Lightsource bp and Contact Energy reaching financial close on the 171 MWdc Glorit plant near Auckland (June 2026), and Contact Energy completing module installation at the 150 MW Kowi Park project at Christchurch Airport (June 2026). These developments support an addressable market across EPC, O&M, grid-connection services, and long-duration contracting.

Distributed solar and flexibility-oriented offerings are also expanding as the regulatory framework tightens around exports and network management. The Electricity Authoritys move to a default 10 kW export limit (announced April 2026 and effective May 2026) increases the value of self-consumption solutions such as batteries, smart inverters, and dynamic export management, particularly in constrained urban networks. Fast-track consenting is also enabling large projects, exemplified by Lodestone Energys fast-track approval for the Haldon Solar Farm in the Mackenzie Basin (July 2026) and the construction start enabled by Harmony Energy and First Renewables financial close for the 202 MWp Tauhei Solar Farm (January 2026), supporting a deeper pipeline for grid upgrades, storage pairing, and bankable offtake structures such as corporate PPAs.

Recent Industry Developments

- June 2026: Contact Energy completed installation of solar modules at the 150 MW Kowi Park solar PV plant at Christchurch Airport. The milestone advances one of the countrys largest solar builds toward completion and expands near-term demand for grid-connection works and utility-scale O&M capabilities.

- September 2025: Meridian Energy and Nova Energy agreed to form a joint venture to build and operate the 400 MW Te Rahui solar farm at Rangitaiki near Taupo. The partnership structure pools development and retail capabilities, supporting scale-up of utility solar and adding depth to the corporate and retailer-backed offtake market.

- August 2024: Christchurch Airport broke ground on a 162 MW airfield-adjacent solar project. Locating a large PV plant next to a major load and existing infrastructure highlights the value of siting strategy for reducing connection risk and accelerating delivery of utility-scale capacity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

In this report, we size the New Zealand solar energy market as the installed solar power capacity added and operating in the country, captured in gigawatts and tied to grid connected and off grid systems.

Scope exclusions: We do not count broader renewable generation value, retail electricity tariffs, or downstream power trading margins as part of the solar energy market size.

Segmentation Overview

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Connection Type

- On-Grid

- Off-Grid

- By End-User

- Residential

- Commercial and Industrial

- Utilities

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the fact base on solar deployments, policy settings, and grid integration constraints in New Zealand before any modeling starts. We rely on public statistics and technical releases such as national energy balance and electricity data from government agencies, grid operator and network planning documents, and solar related connection and distributed generation guidance.

To avoid over relying on one dataset, additional context is taken from sources such as national building and consenting publications, customs and trade statistics for relevant equipment categories, peer reviewed journals on PV performance and degradation in oceanic climates, and industry association updates on installation trends. Company filings, investor presentations, and reputable press are then used to sanity check project pipelines, tender activity, and timing of major build outs, supported by paid subscriptions for company financials and patent screening where it helps clarify technology direction. These examples are not exhaustive, and many other public and paid sources were also referenced for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to confirm how demand is forming across residential rooftops, commercial sites, and utility scale projects in New Zealand, and then to tighten assumptions that are not visible in public datasets. We speak with installers, project developers, EPC participants, distributors, and large buyers, and the discussion is balanced across the main demand centers and also smaller regions where grid constraints and permitting can shift timelines.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | |

| Mid tier: 54% | Functional/Unit leaders: 37% | |

| Smaller Players: 18% | Managers: 51% |

Market-Sizing & Forecasting

The core model starts from a top down reconstruction of installed solar capacity, where yearly additions are built using project commissioning timelines, distributed generation adoption signals, and system performance factors that affect effective capacity over time. To keep the totals realistic, the results are corroborated with selective bottom-up approximations such as sampled installer throughput checks, supplier and channel discussions on shipment direction, and typical system size mixes applied to observed connection activity.

Key inputs we use include grid connected versus off grid share shifts, utility scale project pipeline and commissioning slippage, rooftop penetration by household and small business demand pool, average system size trends, and equipment cost movement that changes payback timing. When data is missing for small regions or older years, gaps are handled by using conservative interpolation tied to known policy changes and grid upgrade cycles, and then rechecked with interviews so the curve does not jump without an explanation. Forecasts are generated using scenario analysis, where base, faster build, and delayed grid cases are set with expert feedback, and then annual capacity additions are translated into the forward market size path.

Data Validation & Update Cycle

Outputs are checked in several steps so unusual jumps are caught early, and so the final numbers remain explainable with simple drivers. Analysts compare the modeled capacity path against independent signals such as commissioning news, policy effective dates, and grid connection constraints, and then variances are investigated before sign off.

The report is refreshed annually, and interim updates are made when a material project, policy, or supply shift is confirmed. Before delivery, a fresh review pass is completed so the latest public releases and primary feedback are reflected in the final view clients receive.

Mordor Intelligence's New Zealand Solar Energy Market Estimate Compared With Other Published Estimates

Published market values for New Zealand solar energy often do not match because different studies mix capacity based sizing with revenue based sizing, and then apply different time windows and conversion assumptions. Differences also show up when one estimate treats storage, services, or electricity value as part of solar, even though the core market signal is installed PV capacity.

Some external numbers are stated in USD and appear to bundle solar equipment, installation services, and sometimes battery storage revenue into one total. In Mordor Intelligence, the market size is expressed as installed capacity in New Zealand, which keeps the figure anchored to commissioning and connection activity rather than pricing swings.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.72 B (2025) | |

| Global Consultancy A | USD 1.00 B (2024) | Reported in USD and appears to size a broader solar value pool that can include equipment, installation activity, and policy incentive effects, which can inflate totals versus a capacity based read. |

| Regional Consultancy B | USD 1.10 B (2024) | Uses a revenue valuation approach and may fold in adjacent components like storage and service revenues, and the base year is different, so currency timing and price assumptions can shift the final number. |

The spread across the table is mainly explained by unit choice and what is counted inside the market. When scope is kept to installed capacity and then checked against project timelines and connection signals, the result stays easier to validate year to year and simpler to reproduce with clear inputs.

Key Questions Answered in the Report

How fast is solar capacity growing in New Zealand?

Installed PV is forecast to triple from 860 MW in 2026 to 2,120 MW by 2031, equating to a 19.74% CAGR.

Which region will add the most new solar projects by 2031?

Canterbury is expected to host 35.10-39.90% of upcoming utility-scale additions, leveraging high irradiance and REZ-enabled grid access.

What share of installations are on-grid versus off-grid?

On-grid arrays held 97.65% share in 2025, although off-grid systems are expanding at a 22.10% CAGR from a small base.

Who are the leading companies in large-scale solar?

Meridian Energy, Mercury NZ, Genesis Energy, and Contact Energy headline utility-scale development, often partnering with international PV specialists.

What policy change most benefits residential adopters?

The nationwide smart-meter roll-out allows half-hourly settlement, lifting rooftop solar returns by up to 18% compared with simple net metering.

Page last updated on: